THANK YOUClick the blue text to follow us

Recently, foreign media such as Reuters reported that the Trump administration is considering approving the sale of NVIDIA’s H200 artificial intelligence chip to China, and the related export control policy adjustments have entered the review stage. However, no final decision has been made yet, and changes are still possible.

01 PARTWhat is the NVIDIA H200 Chip?

The NVIDIA H200 is anext-generation upgrade of the Hopper architecture, released in November 2023. As the successor to the H100, it is currently one of the most powerful AI chips globally, designed specifically forlarge model training/inference, high-performance computing (HPC), and generative AI, addressing the computational bottlenecks of the “large model era” (such as insufficient memory, communication delays, and low energy efficiency).

The core value of the H200 lies insolving the “computational bottleneck” of large model training/inference (insufficient memory, communication delays, low energy efficiency). Through technologies such as HBM3e memory, fourth-generation NVLink, and dynamic power management, it achieves a balance of “performance-energy efficiency-cost”. Although domestic chips have made breakthroughs in specific scenarios, the H200 remains the “flagship benchmark” for global AI computing power, suitable for industrial-grade scenarios requiring “large models and high computational density”.

02 PARTHistory of Export Controls on NVIDIA Chips

History of Export Controls on NVIDIA Chips: A Business Game of “Cat and Mouse” and Technological Breakthroughs

1. 2022: The Curtain Rises on Controls, NVIDIA’s “Amputation for Survival”

In October 2022, the U.S. government listed high-end AI chips such as the NVIDIA A100 and H100 on the export control list to China under the guise of “national security”, prohibiting their sale to Chinese companies. This move directly severed NVIDIA’s “cash cow” in the Chinese market—at that time, NVIDIA held a 95% market share in China’s AI chip market, with A100/H100 chips being the “core computing engines” for major model manufacturers like Tencent and Alibaba.

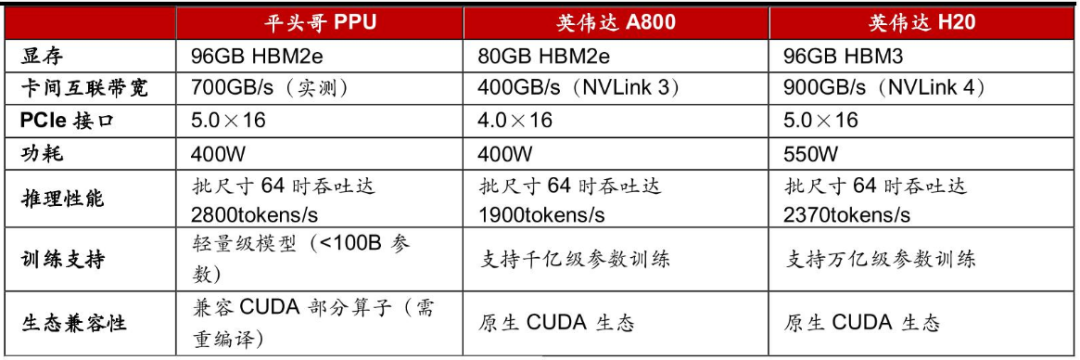

To cope with the controls, NVIDIA quickly launched two “special supply version” chips: the A800 and H800. By reducing the transmission rate (the NVLink bandwidth of the A800 was reduced from 600GB/s to 400GB/s), they just fell within the control threshold, allowing continued sales to China. This “castration” strategy proved effective, with A800/H800 accounting for 15% of NVIDIA’s total revenue in China in 2023, temporarily preserving market share.

2. 2023: Control Upgrades, No More “Special Supply Versions”

In October 2023, the U.S. Department of Commerce further upgraded control rules, adding the A800 and H800 to the banned sales list. NVIDIA’s “special supply cards” became completely ineffective, and revenue from the Chinese market plummeted to 5% (Q3 2025 data). To “extend its life”, NVIDIA launched the H20 chip—this is a “simplified version” of the H100, with computing power about 1/7 that of the H100, but retaining HBM3 memory (141GB) and NVLink interconnect technology, suitable for vertical model training and inference.

After its launch, the H20 quickly became a “hot commodity” in the Chinese market: in the first quarter of 2025, Tencent, Alibaba, and ByteDance collectively ordered over 1 million H20 chips, with a total value exceeding $12 billion. With the H20, NVIDIA barely maintained its “presence” in the Chinese market.

3. 2024: Intensified Sino-U.S. Game, Alternating Between “Bans” and “Lobbying”

In 2024, the Sino-U.S. technological game entered a “white-hot” phase: the U.S. continued to tighten controls, prohibiting NVIDIA from selling any high-end AI chips to Chinese companies; on the other hand, NVIDIA CEO Jensen Huang embarked on a “global lobbying tour”—he visited China multiple times, meeting with executives from Tencent, Alibaba, and others, emphasizing that “the Chinese market is NVIDIA’s core growth engine”; at the same time, he also met with officials from the Trump administration, lobbying for “easing chip export restrictions to China”.

During this period, Chinese companies accelerated their “de-NVIDIA-ization”: Huawei’s Ascend 910B chip (competing with the NVIDIA A100) achieved mass production, and companies like Baidu’s Kunlun chip and Alibaba’s Tianshu also launched their self-developed AI chips. By the end of 2024, domestic AI chips captured 35% of the Chinese market share, surpassing NVIDIA for the first time (30%).

4. 2025: Repeated “Bans” and “Restorations”, Business Logic Triumphs Over Politics

In 2025, the “game” over chip controls between China and the U.S. reached its peak:

- April: The U.S. government announced a “ban on NVIDIA selling H20 chips to China”, citing that “H20 could be used for military AI development”. NVIDIA’s stock price plummeted 8% that day, evaporating $160 billion in market value.

- July: Jensen Huang visited China again for “final negotiations” with the Trump administration. He emphasized: “Abandoning the Chinese market would mean NVIDIA losing growth opportunities for the next decade”; at the same time, NVIDIA promised that “H20 chips would not be used for military purposes” and accepted the U.S. Department of Commerce’s “batch approval” conditions.

- July 15: The U.S. Department of Commerce suddenly “softened”, approving NVIDIA to sell H20 chips to China. The reason was: “H20 is an ‘outdated product’, selling it can still make a quick profit while suppressing China’s AI development through technological iteration”.

This decision brought NVIDIA back to life: orders for the H20 chip surged by 50% in July, and companies like Tencent and Alibaba quickly resumed purchases. However, Chinese companies did not “sit idly by”: orders for Huawei’s Ascend 910B chip increased by 30% in July, and companies like Baidu and ByteDance began to “mix and match” NVIDIA and domestic chips to reduce dependence on a single supplier.

5. November 2025: Latest Developments, “Limited Easing” Becomes the Norm

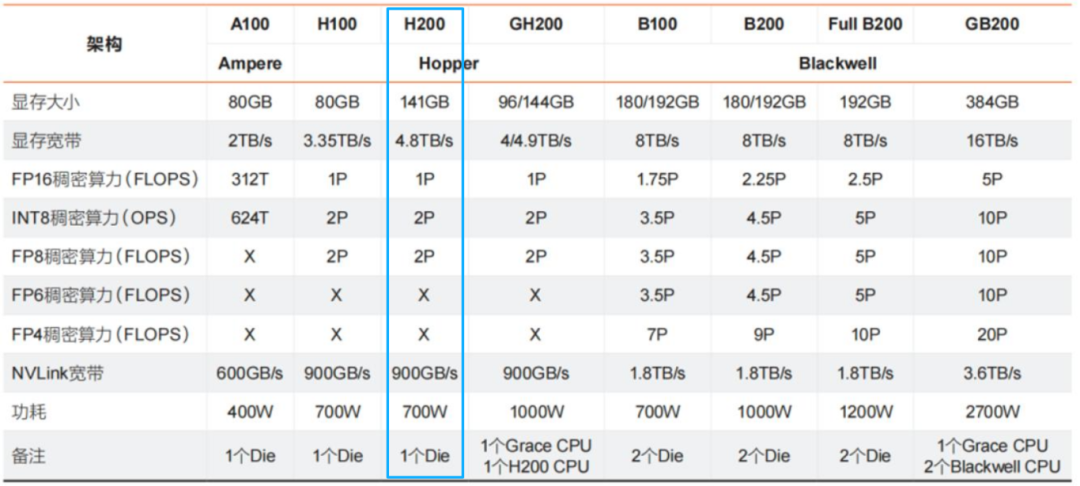

In November 2025, Reuters reported: The Trump administration is considering “limited easing” of the sale of NVIDIA’s H200 chip to China. The H200 is NVIDIA’s latest AI chip (FP8 computing power of 296 TFLOPS, 141GB HBM3 memory), with performance twice that of the H20.

03 PARTAnalysis of the Possibility of Easing H200 Exports

Analysis of the Possibility of Easing H200 Chip Exports:“Limited Easing” is the Core Conclusion, Balancing Business Logic and Strategic Game is Key

1. Core Conclusion: Short-term (within 6 months) probability of “limited easing” is about 40%, more likely to be implemented in the form of “batch approval + end-use review”

The H200, as the “previous generation flagship” of NVIDIA’s Hopper architecture (slightly inferior in performance to the latest Blackwell architecture), its export easing is not a “full release”, but rather a compromise between the U.S. in “maintaining technological advantage” and “protecting business interests”. The core logic of this compromise is:Allowing the H200 will not substantially threaten the U.S.’s leading position in AI technology (the Blackwell architecture has already formed a generational gap), but can alleviate NVIDIA’s business pressure, while maintaining “technological deterrence” against China through “end-use restrictions” (such as prohibiting military AI and batch approvals)..

2. Main Drivers Supporting Easing: Dual Drivers of Business Pressure and Strategic Compromise

- Business Pressure: NVIDIA’s “China Anxiety” Forces LobbyingChina is the world’s largest AI chip market (accounting for 38% of global demand in 2025), but since the tightening of controls in 2023, NVIDIA’s market share in China has plummeted from a peak of 90% to 5% (Q3 2025 data). Its specially customized “bloodied version” H20 chip has faced market rejection due to performance cuts (with computing power only 1/3 that of the H200), and in the third quarter of 2025, it missed bulk orders from giants like Tencent and Alibaba. NVIDIA CEO Jensen Huang publicly warned: “Excessive controls will only force China to develop independently, ultimately losing the U.S.’s leading advantage”.Additionally, competitors like Intel and AMD have also pressured the government, stating that continued controls have led to their market share being rapidly eroded by domestic Chinese chips (such as Huawei’s Ascend 910B and Alibaba’s Tianshu 800). The lobbying from these companies has become a direct reason for the U.S. to consider easing restrictions.

- Strategic Compromise: The Control Strategy of “Eliminating One Generation, Allowing Another”

- Emotional Easing of the Sino-U.S. Trade CeasefireIn 2025, China and the U.S. reached aphase trade ceasefire through multiple rounds of consultations (such as China suspending retaliatory tariffs on U.S. agricultural products, and the U.S. extending the exemption period for tariffs on fentanyl to China), providing a “political window” for easing H200 exports. Although the stability of the ceasefire is questionable, this “emotional easing” has given the U.S. room for “tentative concessions”.

The key premise for the U.S. to ease restrictions this time isthat NVIDIA has launched more advanced Blackwell architecture chips (which outperform the H200 by more than one generation). With the U.S. military already deploying new combat systems based on Blackwell chips, the U.S. government believes that allowing the H200 can alleviate corporate pressure without substantially threatening its national security advantage. This “eliminating one generation, allowing another” control strategy seeks to balance “technological suppression” and “interest maintenance”.

3. Major Risks Against Easing: Concerns Over National Security and Technological Proliferation

- National Security Controversy: The “Potential Threat” of Military AIU.S. hawks have always worried that the powerful computing power of the H200 (141GB HBM3e memory, 4PFlops FP8 computing power) could be used by China formilitary AI development (such as precision strikes by drones, and cyber warfare code decryption). Although the H200’s performance is slightly inferior to the Blackwell, it is still sufficient to support the training and inference of “tactical-level AI”, which keeps the U.S. National Security Council highly vigilant about “technological proliferation”.

- Technological Proliferation Risk: Concerns Over “Civilian to Military” ApplicationsThe U.S. fears that even if the H200 is restricted to “civilian AI training”, Chinese companies may still transfer its computing power to military applications through “reverse engineering” or “software optimization”. For example, Huawei’s Ascend 910B chip (competing with the H100) has already been used in “intelligent command systems”, raising U.S. concerns about the “military applications of civilian chips”.

- Domestic Political Resistance: The Hawkish “Anti-China Stance” Hawkish lawmakers in the U.S. Congress (such as Republican Senator Marco Rubio) explicitly oppose easing H200 exports, arguing that it is a “compromise to China’s technological rise”. They emphasize: “America’s core interest is to maintain technological leadership, and any concession could allow China to close the gap”. This political resistance significantly increases the difficulty of implementing easing.

4. China’s Response Strategy: From “Passive Defense” to “Active Breakthrough”

- Short-term: “Mixed Feelings” Market ResponseChinese companies have amixed attitude towards the easing of the H200:

- Positive: Major model manufacturers like Tencent and Alibaba can leverage the computing power of the H200 to shorten the training cycle of large models (for example, the training time of the GPT-3 175B model can be reduced from “months” to “weeks”), lowering R&D costs.

- Negative: Having become accustomed to NVIDIA chips, the pace of domestic alternatives may be “slowed down”. For instance, an engineer from a leading AI company stated: “The CUDA ecosystem of the H200 (4 million developers, 56,000 open-source projects) still has advantages, and switching to domestic chips (like Huawei’s Ascend 910B) in the short term may require re-adapting models, increasing R&D costs.”

- Huawei Ascend 910B: In “vertical model training” (such as financial risk control and medical imaging), its “knowledge computing unit” (supporting structured data inference) outperforms the H200, and its ecosystem adaptation is better (compatible with PyTorch and MindSpore).

- Cambricon’s Siyuan 590: In “edge computing” (such as intelligent driving and industrial quality inspection), its “sparse computing” (reducing data transmission delays) outperforms the H200, making it suitable for “low power consumption and high real-time” scenarios. These “scenario-based replacements” have made China no longer “passive” in terms of “computing power dependence”.

5. The Essence of the Game is Balancing “Business Logic” and “Technological Breakthrough”

The essence of the easing of H200 exports is a “tactical adjustment” in the Sino-U.S. technological game: the U.S. attempts to maintain a balance between business interests and technological advantages by “allowing the previous generation of chips”; China, on the other hand, seeks to gradually break the “dependence on computing power” through “domestic alternatives”. For Chinese companies,the easing of the H200 is a “short-term benefit”, but “long-term risks” remain (such as the “repetitiveness” of U.S. policies). Therefore, Chinese companies need to seize the “easing window” and accelerate the “scenario adaptation of domestic alternatives” (such as Huawei’s Ascend 910B’s “knowledge computing unit” and Cambricon’s Siyuan 590’s “sparse computing”), ultimately achieving “computing power autonomy”.04 PARTImpact on A-shares

The H200 chip, as theprevious generation flagship AI chip of NVIDIA’s Hopper architecture (with performance about 2 times that of the H20), will have an impact on the A-share market characterized by“short-term structural differentiation and long-term logic reshaping”, with the core logic revolving around the game of “computing power supply recovery” and “domestic alternative progress”.

Below, we analyze its impact on A-shares from three dimensions: directly benefiting sectors, short-term pressured sectors, and long-term benefiting directions:

1. Directly Benefiting Sectors: NVIDIA Supply Chain Enterprises Welcoming Orders and Performance Elasticity

The potential release of the H200 chip will directly drive demand forservers, optical modules, high-end PCBs, and cooling equipment, with related companies as core suppliers of NVIDIA’s ecosystem, welcomingshort-term performance recovery andvaluation increases.

1. Server OEM and System Integration: Explosive Growth in Orders

- Industrial Fulian (601138): As acore OEM for NVIDIA’s GB200 servers (undertaking 70% of GB200 OEM orders), if the H200 is released, its server shipments will significantly increase with the demand for H200. In the first half of 2025, AI server revenue accounted for 35%, and the addition of H200 will further consolidate its leading position in the AI server field.

- Inspur Information (000977): The domestic AI server marketleader (with a market share of over 50%), has completed the adaptation work for the H200 chip, and previously restricted H200 orders have been scheduled until the second quarter of 2026. After the release of the H200, its server shipments will significantly increase, further capturing market share.

- Sunway (603019): A major supplier of supercomputers for top clients like Alibaba, Tencent, and ByteDance, its AI servers are compatible with the H200 chip and possess core technologies such as liquid cooling. The introduction of the H200 will enhance the performance of its supercomputing systems, consolidating its layout in the computing power ecosystem.

2. Optical Modules: Surge in Demand for High-Speed Optical Modules

Thehigh bandwidth demand of the H200 chip (requiring 1.6T optical modules) will directly boost the performance of optical module companies.

- InnoLight (300308): A global core supplier of high-speed optical modules (1.6T optical modules have completed R&D verification), its products can meet the bandwidth requirements of the H200 chip. With the release of the H200, the expansion of computing power clusters will drive demand for 1.6T optical modules, leading tocertain growth in InnoLight’s performance.

- NewEase (300502): Also deeply involved in the high-speed optical module field, its 1.6T optical module products have entered NVIDIA’s supply chain, and the release of the H200 will further enhance its market share in optical modules.

3. High-End PCBs and Cooling Equipment: Increased Supporting Demand

- Shenghong Technology (300476), Huadian Co., Ltd. (002463): As core suppliers ofhigh-end PCBs (circuit boards), the mass production of H200 servers will increase the demand for high-end PCBs (H200 requires high-layer, high-signal transmission rate PCBs). Both companies, leveraging their technological advantages, will undertake NVIDIA’s PCB orders, and their performance is expected to grow.

- Galen Technology (300499), Invec (002837): As core suppliers ofliquid cooling technology, the H200 chip’shigh power consumption (requiring liquid cooling) will drive demand for their liquid cooling products. Both companies have collaborated with NVIDIA, and their liquid cooling solutions will be widely applied with the release of the H200.

4. Distribution and Other Links: Channel Benefits

- China Electronics Port (001287): NVIDIA’s authorized distributor in China, if the H200 is released, the domestic data centers’ procurement demand for the H200 will be unleashed, and China Electronics Port, as a distributor, will directly benefit from sales.

2. Short-Term Pressured Sectors: Domestic AI Chip Companies Facing Competitive Pressure

Thehigh performance of the H200 chip (leading domestic AI chips by 1-2 generations) and itsmature ecosystem (the CUDA ecosystem has 4 million developers) will createshort-term emotional shocks for domestic AI chip companies, and some companies’ stock prices may decline due toorder diversion expectations.

1. Domestic AI Chip Leaders: Short-Term Emotional Disturbance

- Cambricon (688256): Its Siyuan 590 chip (competing with the H100) performs well in the cloud inference market, but still has performance gaps compared to the H200. After the release of the H200, some companies may slow down their procurement of Cambricon chips, leading to a decline in short-term order volume and potential stock price disturbances.

- Haiguang Information (688041): Its x86 compatible CPU is deeply integrated with the NVIDIA ecosystem, but the performance advantage of the H200 may still attract some customers to switch to NVIDIA, causing short-term market share pressure for Haiguang Information.

2. Core Logic of Short-Term Pressure

- Performance Gap: The H200’s FP8 computing power (296 TFLOPS) is 1.15 times that of domestic AI chips (such as Cambricon’s Siyuan 590’s 256 TFLOPS), and its memory bandwidth (4.8 TB/s) is 1.4 times that of domestic chips (such as Ascend 910B’s 3.35 TB/s), showing significant performance advantages.

- Ecosystem Maturity: The CUDA ecosystem has 4 million developers and 56,000 open-source projects, while domestic chips (like Ascend) rely on self-developed ecosystems (CANN, MindSpore), with long adaptation cycles (2-3 months), making it difficult to attract customers to switch in the short term.

3. Long-Term Benefiting Directions: AI Applications and Large Model Enterprises Gaining Computing Power Dividends

The release of the H200 chip willalleviate the computing power gap for domestic large model enterprises (currently, the computing power gap in domestic intelligent computing centers exceeds 30%), reducing model training costs and promoting AI applications from “usable” to “user-friendly”,AI applications and large model enterprises will benefit in the long term.

1. Large Model Enterprises: Accelerating Model Iteration

- iFLYTEK (002230): As a leader in the field of artificial intelligence, its large model training requires substantial computing power support. The release of the H200 will lower its model training costs (for example, the training time of the GPT-3 175B model can be reduced from “months” to “weeks”), accelerating the launch of intelligent office, intelligent education, and other application products, consolidating its industry advantage.

- Tuolisi (300229): Focused on text big data processing and AI applications, the computing power enhancement of the H200 will optimize the performance of its intelligent public opinion monitoring and intelligent content creation products, expanding market share.

2. AI Application Scenarios: Accelerating Commercialization

- Medical AI: For example, intelligent auxiliary diagnosis (requiring large models to process medical images), the computing power of the H200 will enhance diagnostic accuracy, promoting the commercialization of medical AI.

- Educational AI: For example, personalized learning (requiring large models to analyze student learning data), the computing power of the H200 will optimize learning path recommendations, enhancing user experience.

- Financial AI: For example, intelligent investment advisory (requiring large models to process financial data), the computing power of the H200 will enhance the accuracy of investment recommendations, promoting the development of financial AI.

4. Market Sentiment and Risk Alerts

1. Market Sentiment: Short-Term Volatility and Long-Term Differentiation

- Short-Term: NVIDIA concept stocks (such as Industrial Fulian and Inspur Information) will rise due to expectations of the H200’s release, while domestic AI chip stocks (such as Cambricon and Haiguang Information) may experiencepullbacks due tocompetitive pressures.

- Long-Term: The market will differentiate into two main lines: the “NVIDIA supply chain” benefiting from short-term order recovery, and the “domestic alternatives” benefiting from long-term self-controllable logic.

2. Risk Alerts

- Policy Uncertainty: The U.S. export policy for high-tech products to China remains influenced by geopolitical factors, and the timing and scale of the H200’s release are uncertain.

- Technological Replacement Risks: The technological advancements of domestic AI chips (such as Huawei’s Ascend 910B and Cambricon’s Siyuan 590) may divert demand for the H200, impacting the performance of NVIDIA supply chain companies.

- Market Sentiment Volatility: The valuation of the AI sector is at historically high levels, and after short-term benefits are realized, there may beprofit-taking pressure.

Conclusion: The Impact of the H200 Chip on A-shares is “Short-Term Structural Opportunities” and “Long-Term Logic Reinforcement”

The release of the H200 chip willbenefit NVIDIA supply chain supporting companies in the short term (such as servers, optical modules, and PCBs),put pressure on domestic AI chip companies in the short term, butlong-term benefits will accrue to AI applications and large model enterprises. For investors, it is necessary todistinguish between short-term opportunities and long-term logic:

- Short-Term: Focus on companies with deep ties to NVIDIA, high technological barriers, and strong order visibility (such as Industrial Fulian and InnoLight);

- Long-Term: Stick to domestic AI chips and high-end equipment with technological barriers (such as Huawei’s Ascend and Cambricon), asself-control is a national strategy, and the long-term logic of domestic alternatives remains unchanged.

Thank you for being with uson this journey

Thank you for being with uson this journey