【Scan the QR code in the image or click the mini program below to join the community and access all materials】

【Scan the QR code in the image or click the mini program below to join the community and access all materials】

In mid-November, the communication industry continues to maintain a high level of prosperity, with active rotations in sub-sectors such as AI, 5.5G, and satellite communications. Last week, the Shenwan Communication Index corrected by 4.77%, but the core topics within the industry focused on the shortage of upstream chips for optical modules and the upcoming maiden flight of the Zhuque-3 rocket, with related leading companies continuing to attract investment attention.

This article systematically reviews the market performance of the communication industry, changes in supply and demand along the industrial chain, key technologies, and movements of key companies, focusing on this week’s sector trends and mainstream corporate dynamics as well as overseas investment highlights.

1. Sector Performance Review

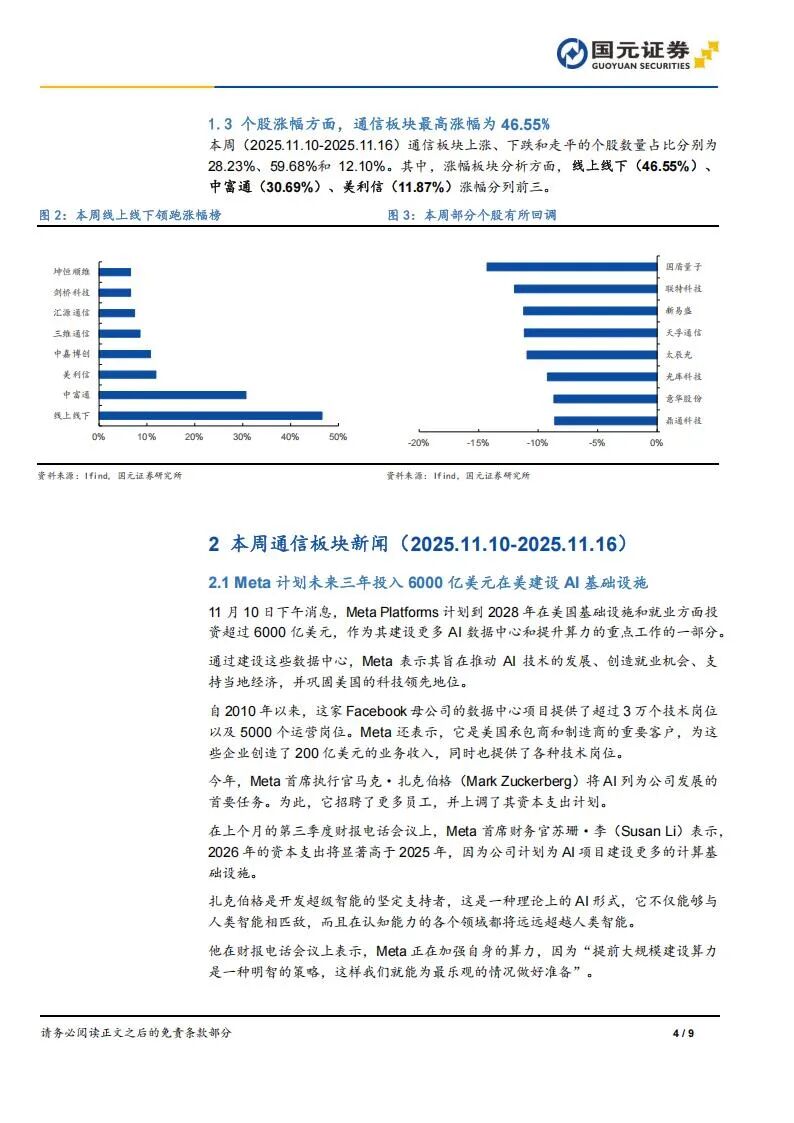

Last week (2025.11.10-11.16), the communication sector faced pressure, with the Shanghai Composite Index correcting by 0.18%, the Shenzhen Component Index by 1.40%, and the ChiNext Index by 3.01%. The Shenwan Communication Sector corrected by 4.77%. In terms of sub-sectors, the communication engineering and services sector rose by 1.57%, while the communication network equipment and devices sector corrected by 6.98%. On the individual stock level, the online and offline stocks saw a rise of 46.55%, with Zhongfutong and Meilixin rising by 30.69% and 11.87%, respectively.

2. Shortage of Optical Module Chips

Driven by downstream demand from AI and cloud infrastructure, the supply and demand for optical modules and upstream chips remain tight. Module manufacturers are limited in expanding production due to a shortage of core chips, and leading domestic and foreign optical chip suppliers (such as Coherent and Lumentum) have not fully released their new production capacity. It is expected that chip supply will continue to be tight until the first half of 2026, with product prices remaining high. Huawei is set to release breakthrough technology in the AI field on November 21, which is expected to increase the industry’s computing power utilization rate from 30-40% to 70%, promoting the penetration of domestic chips. The industry believes that abundant computing resources will further reduce the cost of AI applications, leading to greater penetration of AI in vertical industries, and enhancing the value of domestic computing chain companies.

3. Satellite Industry Chain Events

On November 10, 2025, the Long March 12 rocket successfully completed the launch of 13 low-orbit satellites for satellite internet at the Hainan commercial space launch site, achieving a 100% success rate. Meanwhile, the domestically produced reusable rocket “Zhuque-3” is expected to make its maiden flight in mid to late November, potentially becoming China’s first operational reusable launch vehicle. The cost target for Zhuque-3 is 20,000 yuan per kilogram, comparable to SpaceX’s Falcon 9. This development is expected to break through the bottleneck of satellite launch capacity, accelerating the improvement of the domestic satellite industry chain and enhancing the industry’s closed-loop capabilities.

4. Capital Expenditure in AI and Cloud Infrastructure

Meta Platforms announced that it will invest over $600 billion in AI infrastructure in the U.S. by 2028, primarily for building AI data centers and enhancing computing power. Its third-quarter financial report revealed that capital expenditures in 2026 will be significantly higher than in 2025, further strengthening the reserve of computing power infrastructure. During the same period, CoreWeave reported third-quarter revenue of $1.4 billion, a year-on-year increase of 134%, with a backlog of customer orders reaching $55.6 billion, and capital expenditures deferred to 2026, reflecting the explosive demand for AI computing power and continued investment in the upstream industrial chain. A report from LightCounting also indicated that leading optical module and chip companies (such as Xuchuang Technology, Coherent, NewEase, Arista, Cisco, Nokia, Fujitsu, and Fabrinet) achieved record high revenues in the third quarter, driven by capital expenditures from cloud vendors and data centers.

5. Domestic Technology and Policy Advancements

The Ministry of Industry and Information Technology issued a notice, clarifying that by the end of 2027, a modern manufacturing pilot platform system will be basically established, focusing on key areas such as artificial intelligence, humanoid robots, and quantum technology, promoting the coordinated development of pilot platforms with high-tech zones and advanced manufacturing clusters. On November 13, Baidu released the new generation Kunlun chips M100 and M300, targeting AI chips for large model training and inference, promoting upgrades of AI computing nodes and strengthening the technical foundation of the domestic AI industry chain.

6. Summary of Key Companies

Optical Chips and Modules: Xuchuang Technology, Coherent, NewEase, Guangku Technology, Taicheng Light, Tianfu Communication, LianTe Technology

Network and System Equipment: Cisco, Nokia, Fujitsu, Arista, Fabrinet

Communication Engineering Services: Online and Offline, Zhongfutong, Meilixin, Zhongjiabochuang, Sanwei Communication, Huiyuan Communication, Cambridge Technology, Kunheng Shunwei

Satellite Rockets and Applications: China Aerospace Science and Technology Corporation, Shanghai Micro-Satellite Engineering Center, Hainan Commercial Space Launch Site

AI Computing Power and Platforms: Huawei, Baidu, Meta Platforms, CoreWeave

Scan to join the knowledge community for more industry reports

Disclaimer: This article is for industry research and academic exchange purposes only and does not constitute any investment advice or operational guidance. Market risks objectively exist, and decisions should be made based on independent judgment and thorough research.

Click “Read the original text” to download all materials