1. Global FPGA Market: European and American Giants Lead with 66% Gross Margin, while Chinese Companies Accelerate R&D with 77% Investment

2. Chip cooling startup Corintis completes $24 million Series A funding, Intel CEO Pat Gelsinger joins the board

3. GlobalFoundries partners with Zensemi to develop 40nm automotive chips

4. “Chip” Movement Shines | Jinghua Microelectronics Impresses at the 2025 Shanghai Sensor Expo

5. Kai-Fu Lee: AI Agents are the Core Technology CEOs Should Focus On

1. Global FPGA Market: European and American Giants Lead with 66% Gross Margin, while Chinese Companies Accelerate R&D with 77% Investment

Dominated by Giants, Emerging Forces Rising

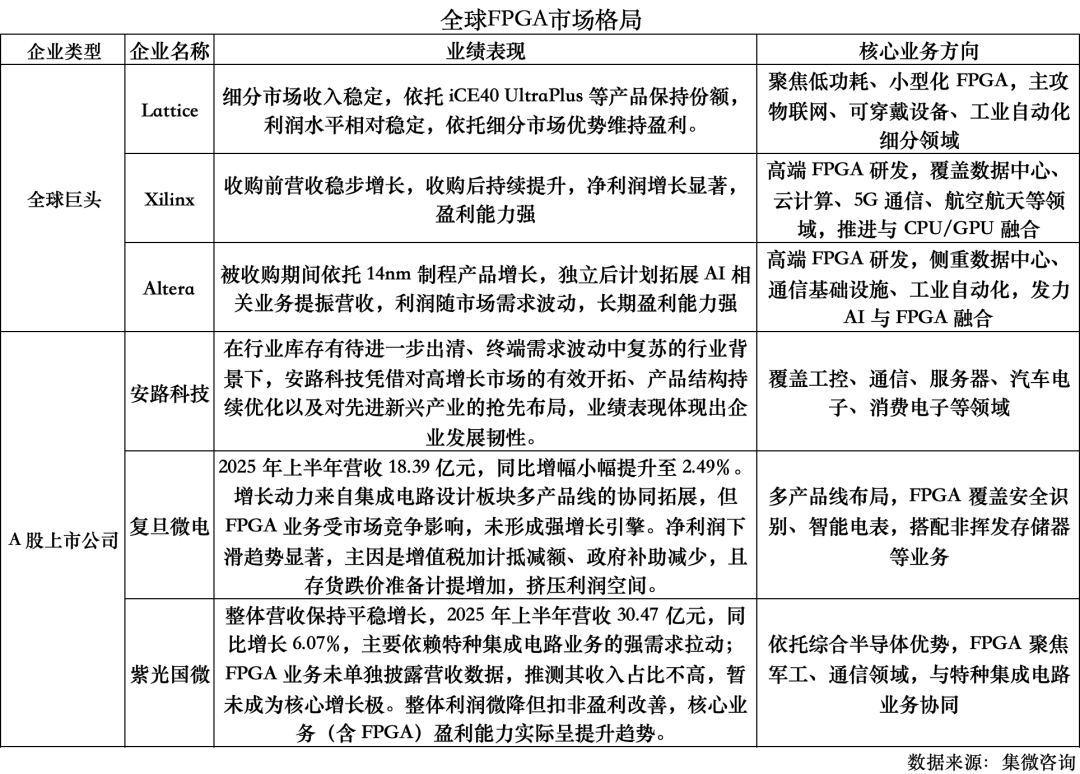

Currently, the global FPGA market is dominated by European and American companies, which have established a leading position through long-term technological accumulation and high R&D investment. Companies like Xilinx and Altera have a significant advantage in the high-end market, with products widely used in cutting-edge fields such as data centers, cloud computing, 5G communication, artificial intelligence, and aerospace. Lattice has carved out a niche in the low-power, small-sized FPGA segment through a differentiated strategy. Japanese and Korean companies, having started earlier, have achieved breakthroughs in certain key technology areas by focusing on specific fields, although their overall market share remains relatively limited.

Chinese FPGA companies are in a rapid catch-up phase. Benefiting from national policy support and a large domestic market demand, companies like Anlu Technology, Fudan Microelectronics, and Unisoc are continuously increasing their R&D investment, achieving partial domestic substitution in the mid-to-low-end product areas, and actively exploring emerging application scenarios. Although domestic companies face challenges such as technological blockades and talent shortages, they are gradually narrowing the gap through continuous innovation.

Performance of Global Giants

Lattice: In terms of revenue, Lattice’s total revenue for 2024 is projected to be $509.4 million. In the second quarter of 2025, revenue is expected to be $123.97 million, remaining stable quarter-over-quarter and increasing by 3.2% year-over-year. Its revenue stability is attributed to long-term customer resources and brand advantages in specific segments such as IoT, wearable devices, and industrial automation. For instance, in the IoT sector, the iCE40 UltraPlus series products meet the stringent requirements for power consumption and size, ensuring stable market demand.

In terms of profit, the gross margin for 2024 is expected to be 66.8%, with diluted earnings per share of $0.44, and net profit and net profit margin of $61.1 million and 12%, respectively. Adjusted EBITDA is projected to be $162 million. In the second quarter of 2025, GAAP gross margin is expected to be 68.4%, with non-GAAP gross margin reaching 69.3%. However, GAAP net profit is only expected to be $2.91 million, a year-over-year decrease of 87.1%, mainly due to increased R&D and selling, general and administrative (SG&A) expenses. Nevertheless, excluding one-time or non-core projects, non-GAAP net profit remains at $31.43 million, a year-over-year increase of 6%. This indicates that despite short-term profit declines due to investments, the core business’s profitability remains solid, and future profits are expected to improve as it expands into industrial automation and AI edge computing.

Xilinx: Before being acquired by AMD, Xilinx was already showing good growth trends, with the third-quarter report for 2022 showing operating revenue of $2.825 billion, a year-over-year increase of 23.03%, and net profit of $741 million, a year-over-year increase of 61.56%. After the acquisition, AMD is integrating resources from both companies and increasing R&D investment in the FPGA business, with R&D expenses expected to remain at 15%-20%.

In terms of market performance, Xilinx products dominate the high-end FPGA market. For example, the Versal adaptive compute acceleration platform combines AMD’s high-performance computing architecture with Xilinx’s flexible programmable logic advantages, excelling in scenarios such as data center cloud computing, big data analytics, and AI training, significantly driving revenue growth. With AMD’s continued investment, the product’s applications in high-performance computing, 5G communication infrastructure, and automotive autonomous driving are continuously expanding, and revenue is expected to keep rising, solidifying its leading position in the high-end market.

Altera: During its acquisition by Intel, Altera leveraged Intel’s technology and resources to launch the Stratix 10 series using 14nm process technology, making a significant impact in the high-end market, widely used in data centers, communication infrastructure, and high-end industrial automation, driving revenue and profit growth.

After operating independently, in April 2025, private equity firm Silver Lake Capital became the controlling shareholder, and the new CEO plans to build “the world’s leading FPGA solution provider,” increasing the R&D investment ratio to 20%-25%, focusing on AI and FPGA integration technology development. Its performance is significantly affected by market demand fluctuations; when demand in data centers and AI markets is strong, product sales rise, leading to revenue and profit growth; when investment in related industries slows, performance is impacted. However, with deep technological accumulation and a high-end product layout, it still possesses strong profitability and market competitiveness in the long run.

Performance of A-Share Listed Companies

Fudan Microelectronics: In 2024, Fudan Microelectronics achieved operating revenue of approximately 3.590 billion yuan, a year-over-year increase of about 1.51%; in the first half of 2025, operating revenue was 1.839 billion yuan, a year-over-year increase of 2.49%. The slight revenue growth is attributed to actively expanding new products and markets, with multiple product lines in the integrated circuit design sector showing growth.

However, profit performance is poor, with net profit attributable to the parent company in 2024 being approximately 573 million yuan, a year-over-year decrease of about 20.43%; in the first half of 2025, net profit attributable to the parent company was 194 million yuan, a year-over-year decrease of 44.38%. The decline in profit is due to reduced VAT deductions and government subsidy verifications, as well as increased provisions for inventory write-downs due to inventory issues. In terms of product structure, in the first half of 2025, revenue from FPGA and other products was 681 million yuan, accounting for 36.98%. Although there are some synergistic advantages in certain scenarios, market competition has affected product prices. In the future, it is necessary to optimize the product mix and increase the proportion of high-value-added products to improve profitability.

Unisoc: Unisoc has a wide business layout, although it has not disclosed FPGA business revenue data separately, its overall operations are stable. In the first half of 2025, the company achieved operating revenue of 3.047 billion yuan, a year-over-year increase of 6.07%; net profit attributable to the parent company decreased by about 6% year-over-year, while non-recurring net profit was 653 million yuan, a year-over-year increase of 4.39%. In the second quarter, revenue increased by 97% quarter-over-quarter and 17% year-over-year; non-recurring net profit increased by 451% quarter-over-quarter and 39% year-over-year, with significant growth in the special integrated circuit business.

Its FPGA products have been applied in military and communication fields, enhancing performance through optimized design and leveraging supply chain advantages to ensure supply and cost. With continued investment in the FPGA business, if it can further increase market share in specific markets, the FPGA business is expected to contribute significantly to the company’s overall revenue and net profit growth.

Anlu Technology: In terms of revenue, in the first half of this year, Anlu Technology achieved revenue of 223 million yuan, with a 39.4% quarter-over-quarter increase in the second quarter, showing a strong recovery trend, with core development momentum continuously strengthening. As a leading domestic FPGA product supplier, Anlu Technology has developed a rich variety of product models, widely applied in multiple fields, with an increasing number of segmented scenarios covered. In the second quarter of this year, as signs of recovery emerged in downstream application fields, Anlu Technology achieved nearly 40% quarter-over-quarter revenue growth, with a stable increase in the number of new customers and new product introduction projects, indicating a clear trend of performance stabilization and recovery, laying a solid foundation for future growth.

Anlu Technology is generous in R&D investment, with the R&D investment ratio soaring to 77.84% in the first half of 2025, and R&D expenses reaching 364 million yuan in 2024. High R&D investment has led to technological achievements, with a total of 482 intellectual property applications as of June 30, 2025, including 280 invention patents. As technological achievements are transformed into product advantages, it is expected to consolidate its position in existing fields such as industrial control and network communication, while exploring new markets to improve revenue and profit conditions.

Conclusion

Currently, the market presents a competitive landscape of “European and American giants dominating the high-end, while Chinese companies catch up in the mid-to-low-end”: Xilinx and Altera, with decades of technological accumulation and high R&D investment, have built strong barriers in high-end fields such as data centers and aerospace, while Lattice has established a foothold in the low-power niche market with its differentiated advantages; domestic companies, despite facing challenges such as revenue fluctuations and profit pressures, have shown the potential and resilience of domestic substitution through Anlu Technology’s high-intensity R&D, Fudan Microelectronics’ multi-product synergy, and Unisoc’s deep cultivation in specific fields.

In the future, as emerging scenarios such as artificial intelligence, edge computing, and automotive electronics continue to drive demand for FPGAs, the industry will welcome new growth opportunities. It is foreseeable that under the dual drive of technological innovation and market competition, the global FPGA market will continue to expand, and if domestic companies can seize opportunities and address shortcomings, they are likely to occupy a more important position in the global landscape, pushing the industry into a new stage of diversified competition and collaborative development.

2. Chip cooling startup Corintis completes $24 million Series A funding, Intel CEO Pat Gelsinger joins the board

As artificial intelligence (AI) drives the demand for higher-performance semiconductor thermal management tools, Swiss startup Corintis has completed $24 million in Series A funding, with Intel CEO Pat Gelsinger joining its board. Sources indicate that Corintis is valued at approximately $400 million after this funding round.

The Series A funding was led by venture capital firm BlueYard Capital, with participation from Founderful, Acequia Capital, Celsius Industries, and XTX Ventures. To date, including pre-seed funding, the company’s total funding has reached $33.4 million.

Corintis plans to use this new funding to expand its team from the current 55 to 70 by the end of the year, increase production capacity, and open an office in the United States, where many of its customers are located.

Corintis stated that Gelsinger (who also serves as chairman of venture capital firm Walden International) was already a board member before being appointed Intel CEO in March. The company also added that Geoff Lyon, founder and former CEO of liquid cooling company CoolIT, has also joined the board.

Testing by Corintis’ customer Microsoft has shown that the startup’s system (which delivers liquid through micro-channels etched on chips for cooling) is three times more efficient than standard methods.

As AI chips produced by companies like NVIDIA consume unprecedented amounts of power, traditional systems relying on cold air from data centers are under immense pressure, leading to a growing demand for new cooling methods. This heat can slow down chip performance and put even more strain on already overloaded power grids.

While most liquid cooling systems can only absorb heat from the chip surface, leaving hot spots, Corintis claims its technology can guide liquid into the chip itself, improving cooling efficiency and reducing power and water resource consumption.

The company automates the design of cooling systems using software and produces its cooling plates in Europe (located on top of the chip to transfer heat to the circulating liquid). This technology can serve as a direct upgrade to existing liquid cooling systems or be directly integrated into chips.

“Currently, we can produce about 100,000 cooling plates per year. Next year, we will increase our annual production to around 1 million plates,” said Corintis co-founder and CEO Remco van Erp.

Remco van Erp co-founded the startup in 2022 with two other founders, including COO Sam Harrison, after spinning out from the École Polytechnique Fédérale de Lausanne.

3. GlobalFoundries partners with Zensemi to develop 40nm automotive chips

GlobalFoundries (GF), the fifth-largest foundry in the world, announced its latest strategy for the Chinese market at a technology summit held in Shanghai on September 24. The company also announced a partnership with Chinese foundry Zensemi, focusing on mature 40nm process technology for automotive electronics CMOS products.

Hu Weiduo, president of GlobalFoundries China, made his first public appearance since taking office, stating that this move aims to deepen localization to meet the rapidly growing semiconductor demand in China.

Sudipto Bose, vice president of GlobalFoundries’ automotive business, pointed out that China is one of the fastest-growing markets for automotive electronics, with this business unit accounting for about 18% of the company’s total shipments. He emphasized that GlobalFoundries’ strategy is not only to “establish a presence in China and serve China” but also to respond quickly to local customer needs with “Chinese speed”.

Hu Weiduo, who took office on September 1, has over 25 years of experience in the semiconductor and technology industry, having worked at Qorvo, HTC, and Broadcom. He explained that the company will continue to focus on the localization supply needs of local OEMs, fabless companies, and multinational customers while gradually enhancing GlobalFoundries’ manufacturing and delivery capabilities in the Chinese market.

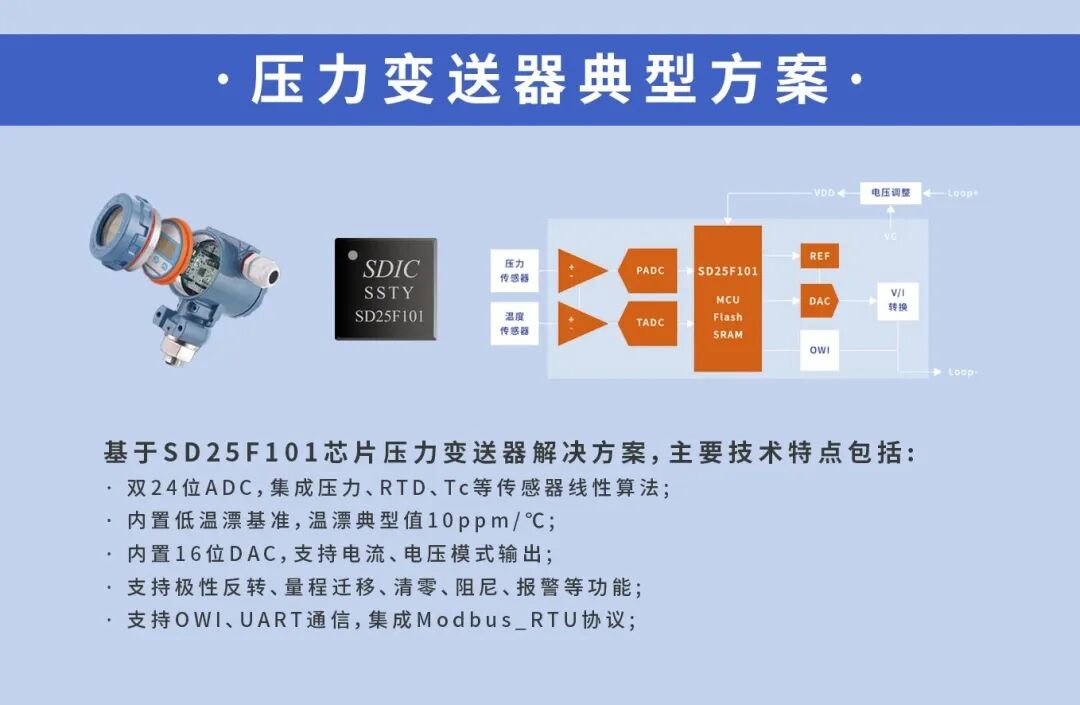

4. “Chip” Movement Shines | Jinghua Microelectronics Impresses at the 2025 Shanghai Sensor Expo

From September 24 to 26, the China (Shanghai) International Sensor Technology and Application Exhibition [SENSOR CHINA 2025] was grandly held at the Shanghai International Procurement Center.

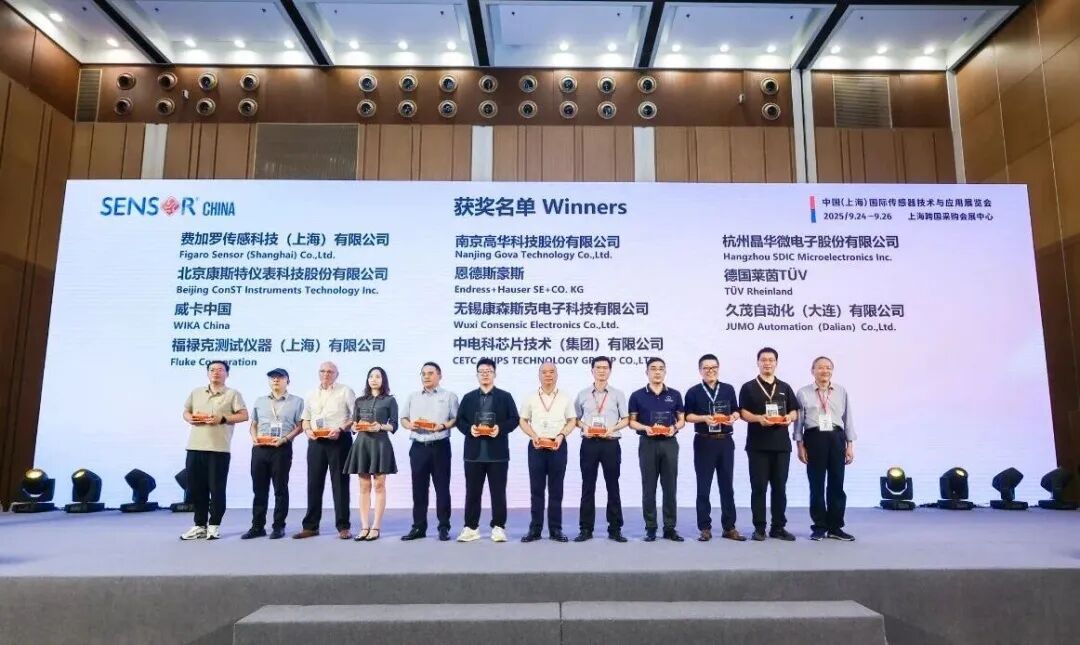

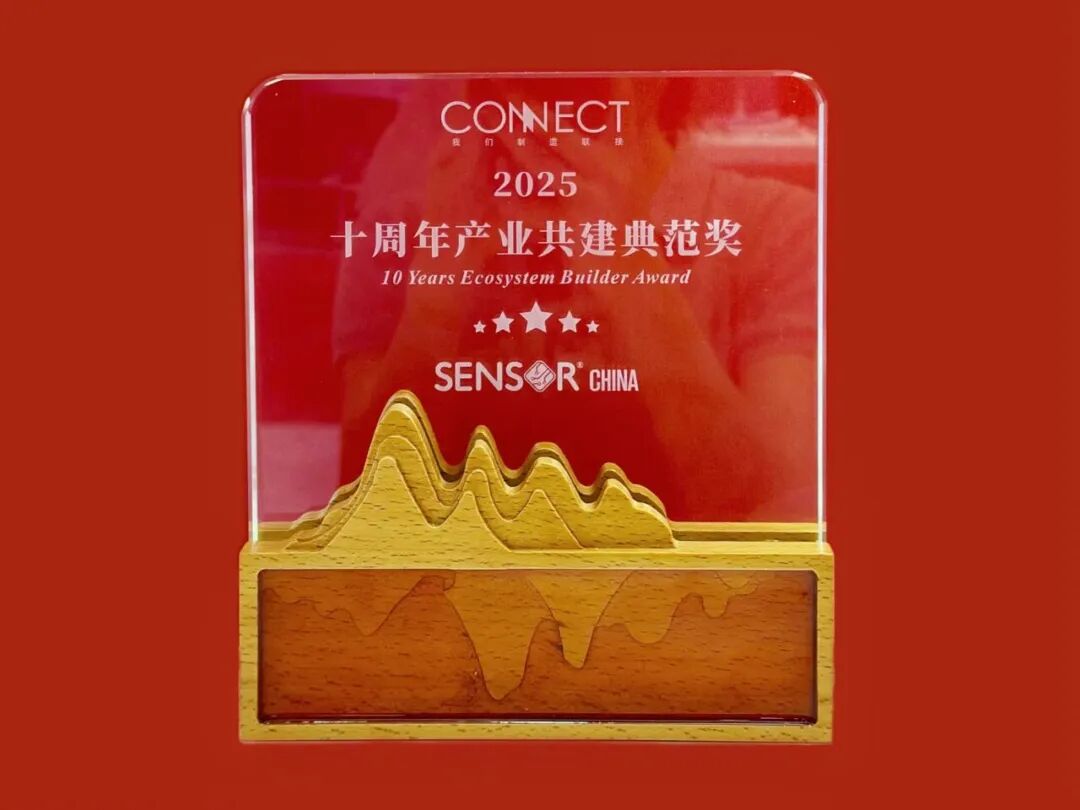

Hangzhou Jinghua Microelectronics Co., Ltd. (stock code: 688130) showcased multiple chip products and innovative solutions at this year’s exhibition. During the exhibition, Jinghua Microelectronics accepted media interviews at their booth and was awarded the “Industry Co-construction Model Award” at the concurrent “China Sensor and IoT Industry Night” event.

Jinghua Microelectronics – Frontline of the Exhibition

At this exhibition, Jinghua Microelectronics focused on showcasing a series of chip products and solutions covering industrial control and instrumentation, medical health and weighing instruments, smart home appliances, and BMS battery management systems, attracting a large number of guests for discussions and cooperation.

Typical Product and Solution Display

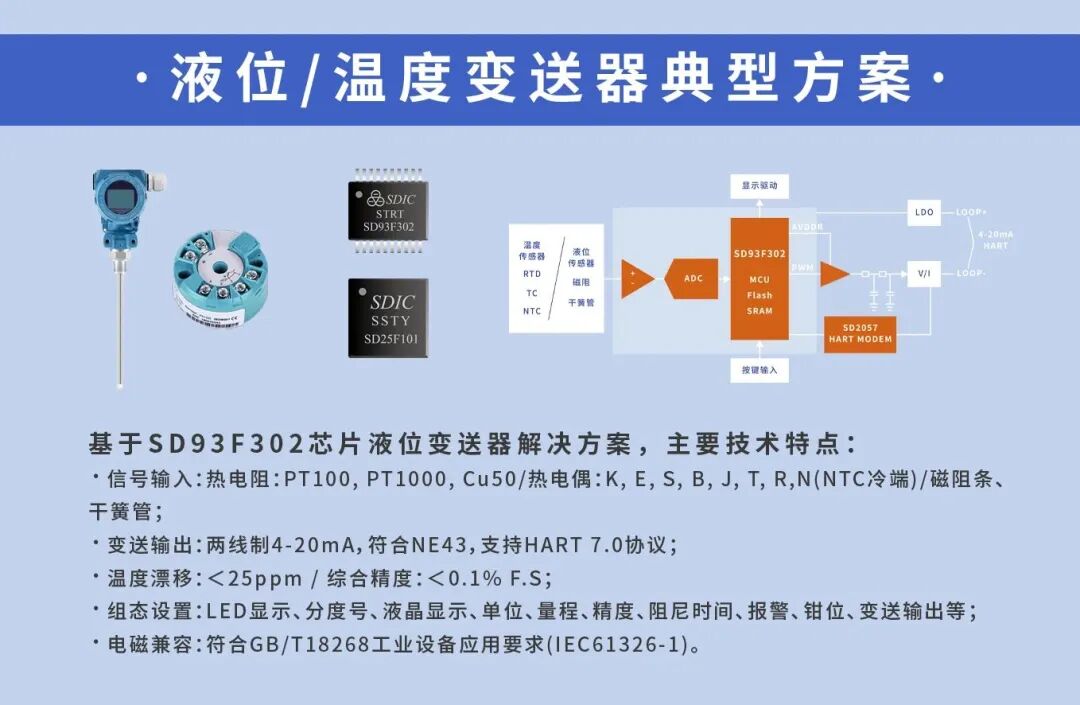

This time, Jinghua Microelectronics focused on showcasing typical solutions for pressure transmitters, liquid level/temperature transmitters, HCT blood glucose meters, refrigerator display boards, and high-precision AFE solutions for 7-17 series.

Media Interview with Industrial Control Network

On the morning of the 24th, Mr. Shi Junqiang, Deputy General Manager of Jinghua Microelectronics, accepted a media interview at the Jinghua Microelectronics booth, focusing on the company’s core chip products and solutions in the industrial control field, and discussing related technology applications and the process of domestic substitution.

Award Recognition

On the evening of the 24th, at the “China Sensor and IoT Industry Night” event held concurrently with the exhibition, Jinghua Microelectronics was awarded the “Industry Co-construction Model Award” for its years of professional technical accumulation and continuous innovation capabilities, actively contributing to the ecological construction and development of the sensor industry.

Jinghua Microelectronics – Looking to the Future

For twenty years, Jinghua Microelectronics has focused on the design and application development of professional mixed-signal integrated circuits, continuously promoting technological breakthroughs in smart sensing and industrial control fields, and is committed to providing customers with high reliability, high integration, and high precision chips and solutions. In the future, we are willing to work hand in hand with industry partners to create value together. We look forward to meeting again at the next exhibition!

5. Kai-Fu Lee: AI Agents are the Core Technology CEOs Should Focus On

Recently, Kai-Fu Lee, CEO of Sinovation Ventures, stated that AI Agents are the core technology that CEOs should focus on, with the most valuable application scenarios for AI Agents being in enterprises, becoming the core force driving intelligent transformation in companies. In the era of intelligent agents, AI Agents are the key executors of corporate transformation, and the value of AI is shifting from “tools” to “services,” and then from “services” to “results.” AI Agents will promote the implementation of “results-based business models.”

“Not AI for AI’s sake, but AI for growth,” Lee stated, emphasizing that when companies no longer pay for models but for “results” and “value,” the value created by AI will shift from cost reduction to efficiency enhancement. AI Agents make super digital employees accessible, further driving scalable growth for companies, with a portion of productivity in various industries gradually being automated through AI Agents, making the “Always On” production model possible. Undoubtedly, AI Agents are a crucial technology application that must be grasped to promote new productive forces and will become one of the key engines for economic growth in the coming decades.

Lee reiterated that the AI digital transformation of enterprises is a top-down initiative, requiring CEOs to personally participate in strategic design and form a “transformation community” with external technology partners, embedding AI deeply into business processes.

Hot Topics:

1.After the White House’s 10% equity stake, Apple may follow up with investment to “rescue chips”

2.Latest developments from the “Father of Chinese Semiconductors”!

3.Another Chinese company may face US investigation, as it is an Apple-certified supplier

4.Breaking! US agencies ban another technology from China

5.Next year, QLC SSDs may see explosive growth6.Reports of a major chip team disbanding, with two chips successfully taped out!7.$5 billion! GPU giant partners with CPU veteran to reshape the US chip landscape8.Multiple domestic AI chips showcased on CCTV! Key parameters exposed

Share

Like

Watching