1. Policy Background and Market Impact

The Trump administration is set to launch the “Genesis Plan” to boost AI development while pressuring Congress to veto the GAIN AI Act, which restricts AI chip exports. NVIDIA, as a core beneficiary, is expected to expand its global market share. The combination of these two policies will stimulate a surge in global AI computing power demand, presenting clear short- to medium-term investment opportunities for the A-share computing power industry chain (NVIDIA supply chain, computing power infrastructure, CPO/silicon photonic chips, domestic AI chip replacements).

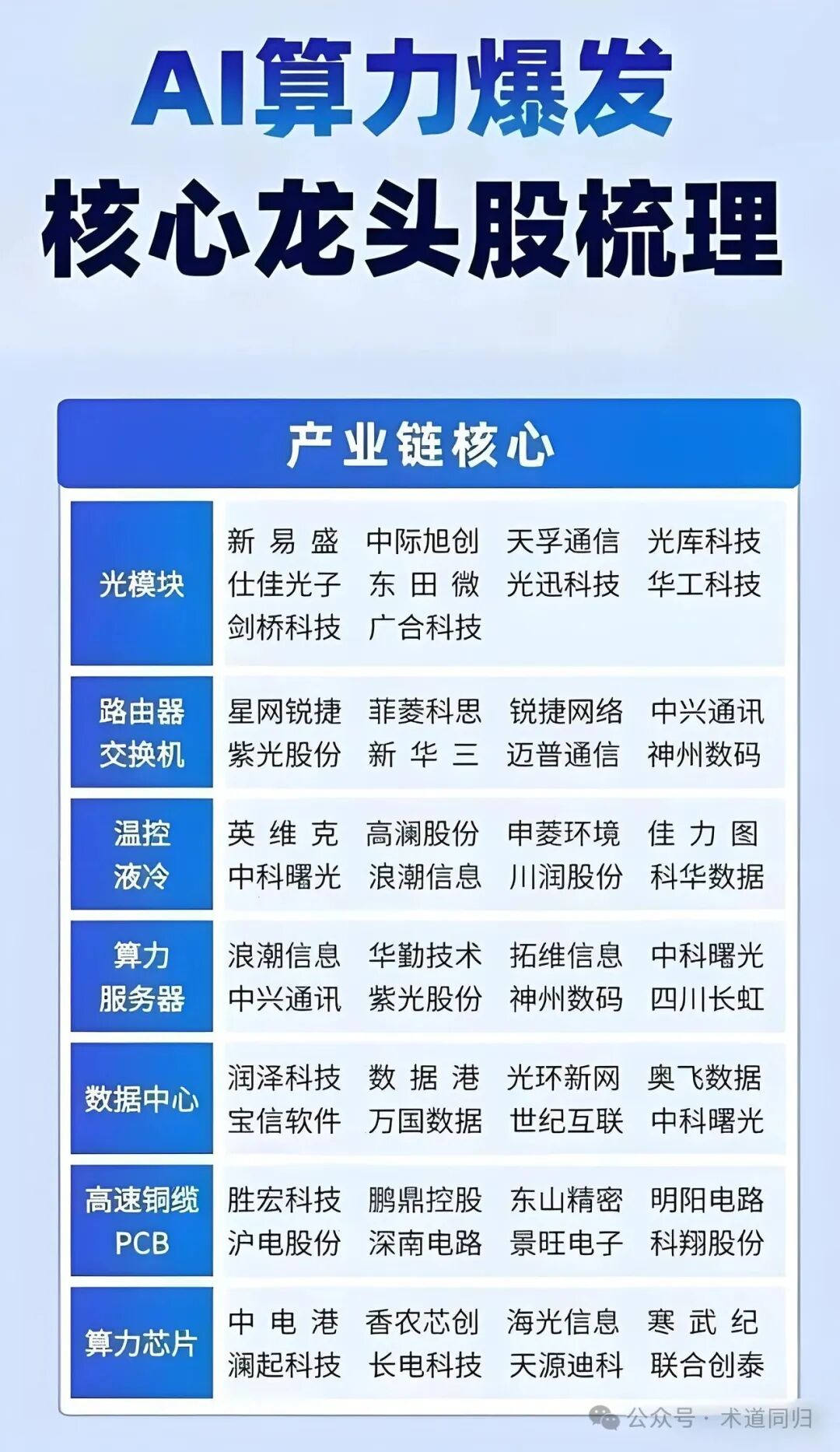

2. Investment Opportunities in NVIDIA Supply Chain Core Targets

2.1 Optical Module Sector

• Zhongji Xuchuang (300308.SZ): Exclusive supplier of NVIDIA’s 1.6T optical modules (accounting for 80% of demand), the only company globally to mass-produce 1.6T CPO optical modules, with over 50% market share in 800G products, leading in 3.2T module R&D, and a net profit increase of 90.05% year-on-year in the first three quarters of 2025. The actual controller, Wang Weixiu, holds a total of 17.54% voting rights.

• Xinyi Sheng (300502.SZ): Core supplier of NVIDIA’s 800G optical modules, 1.6T optical modules certified and delivered in small batches, exclusive supplier of LPO modules, with a net profit expected to surge by 355.68% in 2025. The actual controllers, Huang Xiaolei and Gao Guangrong, hold a total of 13.36% shares.

• Other Targets: Cambridge Technology (exclusive supplier of 800G LPO modules to Microsoft), Lian Te Technology (certified silicon photonic module manufacturer for NVIDIA), Tianfu Communication (core supplier of 1.6T optical engines, with orders of 1.4 million units).

2.2 PCB Sector

• Huadian Co., Ltd. (002463.SZ): The largest supplier of NVIDIA AI server PCBs (over 70% of Q1 orders), with approximately 40% market share in GB300 high-layer boards, and 30% of the Thai factory’s capacity dedicated to NVIDIA, with related revenue expected to account for over 40% of total revenue in 2025.

• Other Targets: Shenghong Technology (50% market share in NVIDIA graphics card PCBs), Shengyi Technology (PTFE high-frequency copper-clad boards validated by NVIDIA), Jin’an Guoji (high-frequency high-speed boards certified by NVIDIA Gamma).

2.3 Power Supply and Supporting Sector

• Magmita (002851.SZ): Core supplier of NVIDIA’s GB200/GB300 series power supplies, with PowerShelf orders accounting for 20%, the only company from mainland China to qualify, and a liquid-cooled power supply conversion efficiency exceeding 97%.

• Other Targets: Meilian New Materials (indirect supplier of copper-clad boards to NVIDIA), Helin Micro-Nano (GPU chip probe supplier).

3. Investment Opportunities in AI Computing Power Infrastructure

3.1 AI Server Sector

• Inspur Information (000977.SZ): The global leader in AI server market share (over 30%), with domestic market share exceeding 50%, liquid cooling capacity of 100,000 units per year, and a year-on-year revenue increase of 165.3% in Q1 2025, with the Xinchuang business accounting for over 60% of revenue.

• Tuowei Information (002261.SZ): Core partner of Huawei’s Ascend ecosystem, with a year-on-year increase of 400% in Ascend server shipments, and expected revenue exceeding 5 billion yuan in 2025, with cumulative winning orders exceeding 8 billion yuan.

3.2 Liquid Cooling Temperature Control Sector

• Invid (002837.SZ): Domestic market share of approximately 35% in liquid-cooled data centers, with over 40% market share in cold plate liquid cooling, and PUE as low as below 1.2, serving major clients like ByteDance and Tencent.

• Fuxin Technology (688662.SH): TEC products ensure temperature control for CPO chips, directly benefiting from high-power heat dissipation demands.

3.3 Other Infrastructure Targets

Guanghuan New Network (over 50,000 core server cabinets), Baoxin Software (over 15% market share in Yangtze River Delta IDC cabinets), Kehua Data (18.6% market share in high-end UPS power supplies), Zhongheng Electric (35% market share in modular UPS).

4. Investment Opportunities in CPO Silicon Photonic Chip Industry Chain

4.1 Optical Chip Sector

• Shijia Photonics (688313.SH): IDM manufacturer of silicon photonic chips, mastering silicon-based modulator technology, compatible with NVIDIA’s GB200 architecture, with related revenue expected to increase by 72% in the first half of 2025.

• Changguang Huaxin (688048.SH): Leader in VCSEL chips, with products applied in Alibaba’s Zhangbei data center, and 200G PAM4 EML/PD compatible with 1.6T modules.

• Yuanjie Technology (688499.SH): A rare IDM model optical chip leader in China, with the highest global market share for 10G laser chips, mass production of 100G EML chips breaking overseas monopolies, and a 300mW high-power CW light source compatible with CPO packaging, samples sent to NVIDIA and received orders worth over 100 million yuan from Zhongji Xuchuang; expected revenue of 383 million yuan in the first three quarters of 2025 (year-on-year increase of 115.09%), with a net profit of 106 million yuan (turning profitable), and Q3 single-quarter revenue of 178 million yuan (year-on-year increase of 207.31%), with cumulative large orders of 266 million yuan, latest PE of 511.61, PB of 23.63.

• Yongding Co., Ltd. (600105.SH): Achieved full-process layout of optical chips through its subsidiary Dingxin Optoelectronics, with an 85% yield for 25G DFB chips (domestic average 60%-70%), and 100G EML chips compatible with 1.6T modules, receiving intention orders from major clients, and supplying Zhongji Xuchuang, Xinyi Sheng, etc.; expected net profit of 322 million yuan in the first three quarters of 2025 (basic earnings per share of 0.225 yuan), with optical chip-related business revenue accounting for over 40%, receiving orders worth over 4.4 billion yuan from Microsoft, Google, etc., and expected optical chip business revenue to exceed 5 billion yuan in 2026, latest PE of 63.62, PB of 6.42.

5. Investment Opportunities in Domestic AI Chip Replacements

5.1 Cloud AI Chip Sector

• Cambricon (688256.SH): One of the few domestic companies producing 7nm cloud AI chips in mass, with a replacement rate exceeding 30% for the Siyuan series, and revenue in Q1 2025 approaching the total for 2024, with two consecutive quarters of profitability.

• Haiguang Information (688041.SH): DCU chips compatible with x86 servers, achieving 80% performance of A100, securing 35% of Alibaba Cloud’s procurement share, with 2.8 billion yuan in commercial orders landed.

5.2 Other Replacement Targets

• Jingjia Micro (300474.SZ): Leader in military GPUs, with the JM9 series compatible with mainstream AI models, and over 40% market share in Xinchuang desktops.

• Other targets: Suiyuan Technology (over 60% market share in financial risk control), Biran Technology (BR100 competing with H100), Moore Threads (full-featured GPU mass production manufacturer), Baidu Kunlun Chip (won a 1 billion yuan order from China Mobile).

6. Strategic Recommendations

6.1 Strategic Recommendations

Focus on three types of leading enterprises:

First, companies with core technological barriers (optical chips, CPO packaging, etc.);

Second, suppliers with stable orders bound to giants like NVIDIA; Third, companies with outstanding domestic replacement capabilities in key links of the industry chain. Short-term focus on directly benefiting targets like optical modules and PCBs, and medium- to long-term layout in CPO/silicon photonic chips and domestic AI chip tracks, adopting a phased investment strategy to control high valuation risks.