What data and rankings are worth paying attention to this week?

Omdia: An average of 5-8 millimeter wave radars expected for Level 3 and above autonomous driving systems

Omdia released a report stating that cameras, millimeter wave radars, ultrasonic radars, and LiDAR are currently common sensors in the field of autonomous driving. The development and advancement of sensor technology are crucial for enhancing vehicles’ perception capabilities in complex driving environments.

The report pointed out that in 2019, the average number of cameras installed in each car worldwide was only 2.2, and this number is expected to double by 2026.

Regarding millimeter wave radars, Omdia predicts that Level 3 and above autonomous driving systems will be equipped with an average of 5-8 millimeter wave radars to achieve functions such as Blind Spot Detection (BSD), Lane Change Assistance (LCA), and Rear Collision Warning (RCA).

As for LiDAR, the report states that future LiDAR will trend towards miniaturization, high resolution (64-channel, 128-channel, and even 200-channel), and low-cost solid-state solutions. Additionally, integrating LiDAR into a single chip will become a long-term technical research direction.

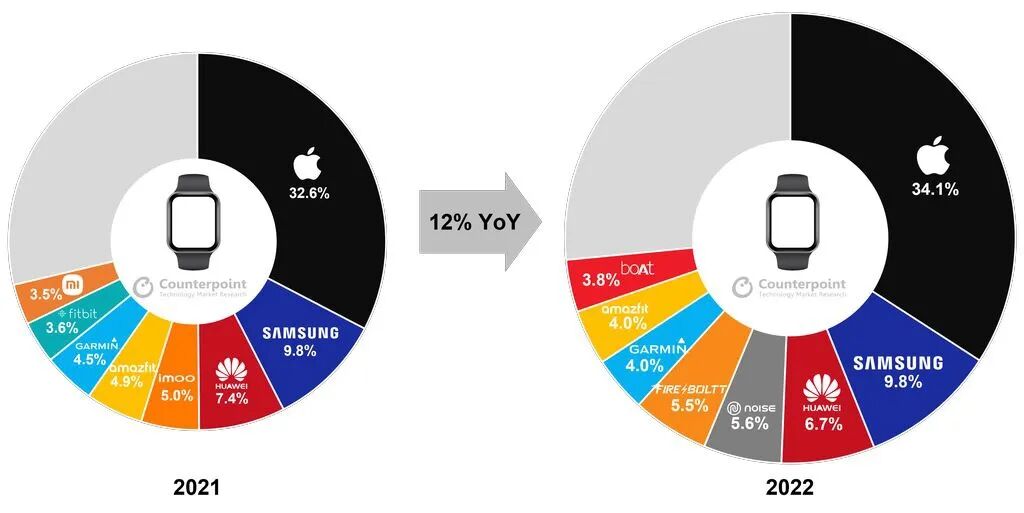

Counterpoint: Apple Watch Dominated Last Year’s Smartwatch Market with a 34.1% Shipment Share

According to statistics released by market research firm Counterpoint, the Apple Watch held a dominant position in the 2022 smartwatch market, with a shipment share of 34.1% and a revenue share of 60%.

Additionally, Samsung and Huawei ranked second and third, with market shares of 9.8% and 6.7%, respectively. Compared to the previous year, Samsung’s market share remained unchanged, while Huawei saw a slight decline.

Omdia: AMOLED Display Driver Chip Shipments Expected to Grow by 14% Year-on-Year This Year

Omdia’s latest report shows that OLED display panel shipments still experienced a year-on-year decline of 6% in 2022, while OLED display driver chip (DDIC) shipments fell by 5% year-on-year.

The report indicates that in 2023, with the recovery of demand for smartphones, smartwatches, OLED TVs, and portable computers, AMOLED DDIC shipments are expected to grow by 14% year-on-year, reaching 1.16 billion units.

Omdia predicts that by 2029, the penetration rate of AMOLED will reach 30% of the total display panel volume, with AMOLED DDIC shipments increasing from 1 billion units in 2022 to 2.2 billion units in 2029, representing a compound annual growth rate (CAGR) of 12%.

Counterpoint: Excess Smartphone AP/SoC Inventory Expected to Normalize in the Second Half of This Year

Counterpoint released an analysis report stating that the smartphone market will remain flat year-on-year in 2023. Inventory adjustments are expected in the first half of 2023, while demand is anticipated to rebound in the second half. By the end of the second half of 2023, excess smartphone AP/SoC inventory is expected to return to normal levels.

The report notes that the semiconductor industry is currently exhibiting cyclical rather than structural weakness. The market is expected to be sluggish in the first half of 2023; however, in the second half, as OEM manufacturers begin to replenish inventory and prepare to launch flagship products, the market is expected to see growth.

Counterpoint states that apart from high-end chips, Qualcomm has opportunities in the mid-to-low-end AP/SoC market, which has been more affected than the high-end market. Qualcomm will attempt to regain some market share from MediaTek in the mid-to-low-end segment.

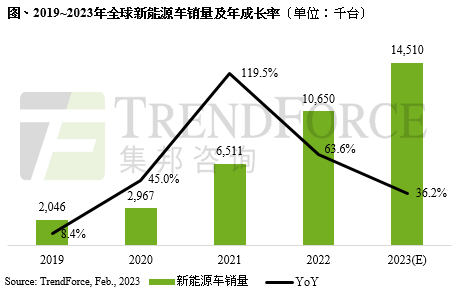

TrendForce: Global New Energy Vehicle Sales Exceeded 10 Million in 2022, with China Accounting for 63% of the Market

TrendForce released a report stating that global sales of new energy vehicles (NEVs, including pure electric vehicles, plug-in hybrid electric vehicles, and hydrogen fuel cell vehicles) reached approximately 10.65 million units in 2022, a year-on-year increase of 63.6%.

The report indicates that among these, pure electric vehicles (BEVs) accounted for 7.89 million units, a year-on-year increase of 68.7%; plug-in hybrid electric vehicles (PHEVs) accounted for 2.74 million units, a year-on-year increase of 50.8%. China and Western Europe remain the two major markets, but the market share gap is widening, with China accounting for 63% of the market and Western Europe at 29%.

Furthermore, TrendForce states that while the automotive market shows mixed signals, new energy vehicles will continue to rise, with sales expected to reach 14.51 million units this year, a year-on-year increase of 36.2%.

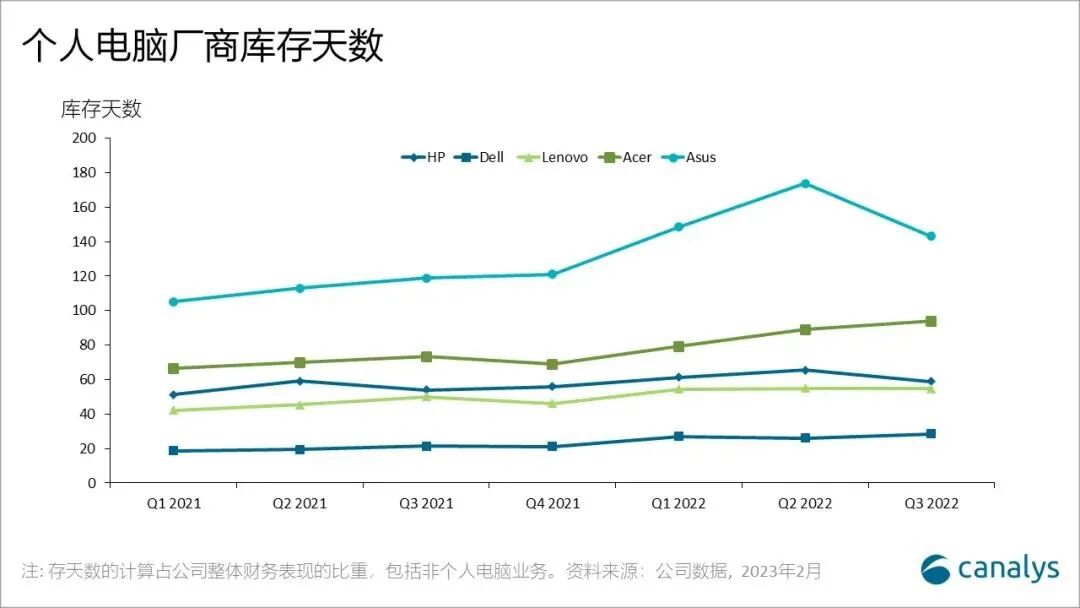

Canalys: Overall Inventory Days for Computer Manufacturers Expected to Improve in Q1, with Q2 Expected to Return to Normal Levels

Canalys released a report stating that in the fourth quarter of 2022, global shipments of desktop and laptop computers fell by 29%, dropping to 65.4 million units. Given the lengthy order process, inventory levels for channels and PC manufacturers should recover to normal levels earlier than upstream component manufacturers.

The report indicates that based on the recent financial status of leading PC manufacturers (excluding Apple), HP and ASUS have begun to reduce their inventory days (DoI), while the other three manufacturers (Dell, Lenovo, and Acer) have seen a slight increase in their inventory days.

As all manufacturers have taken proactive measures to reduce production, overall inventory days are expected to further improve in the fourth quarter of 2022 and the first quarter of 2023, with a return to normal inventory levels anticipated in the second quarter of 2023.

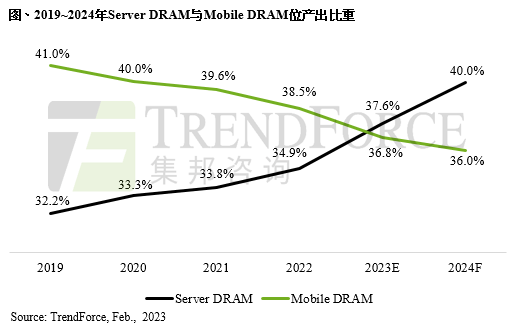

TrendForce: Server DRAM Bit Output Share Expected to Reach 37.6% in 2023, Surpassing Mobile DRAM

TrendForce released a report stating that the bit output share of Server DRAM in 2023 is expected to be approximately 37.6%, officially surpassing Mobile DRAM’s 36.8%.

The report indicates that since 2022, DRAM manufacturers have continuously shifted production capacity originally allocated to Mobile DRAM to the relatively strong Server DRAM segment, attempting to alleviate the supply-demand imbalance in the Mobile DRAM sector. In 2023, due to the conservative growth rate of smartphone shipment and average capacity growth, manufacturers’ product mix strategy is to continue increasing the share of Server DRAM.

In the Server DRAM segment, driven by new applications in AI and HPC, both the shipment and average capacity growth in the server field are expected to exceed those in the smartphone sector, making it the highest bit output share segment in the coming years. The average capacity growth rate for Server DRAM in 2023 is expected to reach 12.1%.

Omdia: Demand for LCD TVs Expected to Rebound in Q2 2023

Omdia released a report stating that the demand for LCD TV panels from leading Korean and Chinese manufacturers is expected to recover soon.

Omdia predicts a strong year-on-year rebound of 19% in Q2 2023, with procurement expected to reach 161.4 million units, an 8% year-on-year increase, and shipments of screens 50 inches and above will be even more significant. If the procurement plan for 2023 is implemented, the market will return to the peak procurement levels of 2020, exceeding the average levels of the past four years by 3%.

The report indicates that Samsung Electronics and LG Electronics have begun to plan their procurement volumes for 2023 in advance, and panel demand in 2023 may surge by 22% year-on-year from the 14-year low in 2022.

Top Chinese TV manufacturers set a historical high in panel procurement from Q3 2022 to Q4 2022, thereby gaining and enhancing their market share globally, especially in the North American market.

According to Omdia’s forecast, starting in 2023, global TV brands and OEM manufacturers will begin to increase panel orders and initiate a new replacement cycle, particularly for large-sized TVs.

TechInsights: Wi-Fi 7 Devices Expected to Surpass Wi-Fi 6E Shipments in 2025-2026

TechInsights’ latest report indicates that Wi-Fi will maintain its superior position in enterprise connectivity, with new Wi-Fi 6E/7 generations establishing and expanding their roles and utility, particularly in the 6GHz spectrum.

TechInsights states that Wi-Fi 7 devices will start shipping in 2023, and are expected to surpass Wi-Fi 6E shipments in 2025-2026. The first smartphone equipped with Wi-Fi 7, the Xiaomi 13 Pro, has already begun launching in China.

IDC: China’s Edge Cloud Market Reached 3.07 Billion Yuan in the First Half of 2022, a Year-on-Year Increase of 50.8%

IDC’s latest report shows that in the first half of 2022, China’s edge cloud market totaled 3.07 billion yuan, a year-on-year increase of 50.8%.

Among these, the market sizes for edge public cloud services, edge dedicated cloud services, and edge cloud solutions reached 1.71 billion, 440 million, and 920 million yuan, respectively.

IDC states that by 2026, 50% of CIOs in Chinese enterprises will require cloud and telecom partners to provide secure cloud-to-edge connectivity solutions to ensure the performance and consistency of data collection.

IDC predicts that from 2021 to 2026, the edge cloud market will have a compound annual growth rate of over 40%, driven by the emergence of more edge cloud collaborative scenarios and the increasing acceptance of the “as-a-service” model by traditional industry users, continuously injecting vitality into the market.

END