Analysis Report on the Chinese Semiconductor Industry Chain

Release Date November 24, 2025

From “Catching Up” to “Running Alongside”: A Key Turning Point

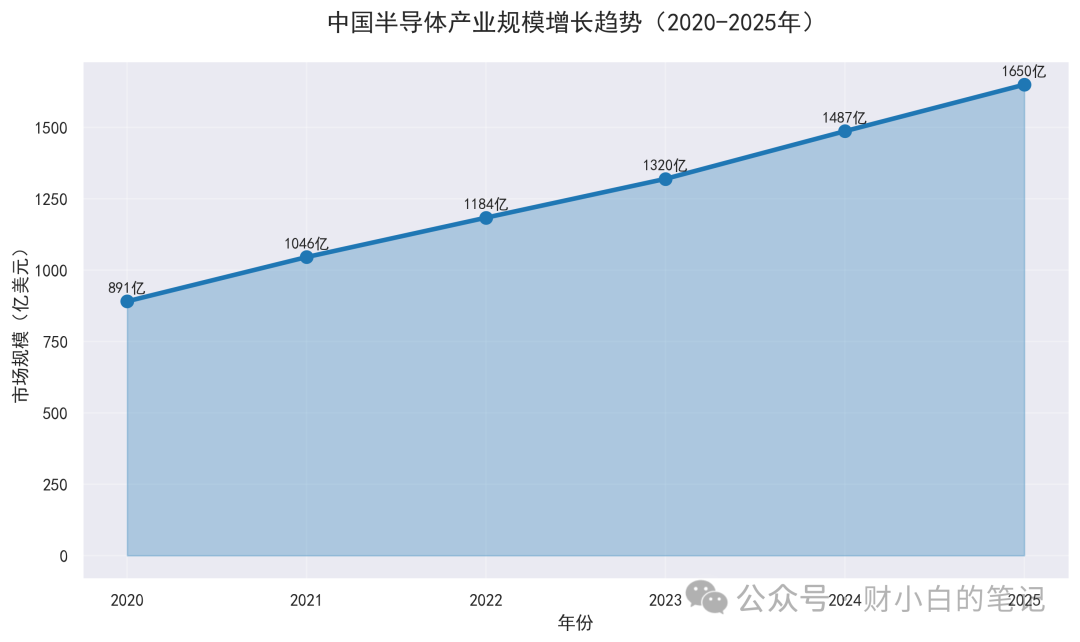

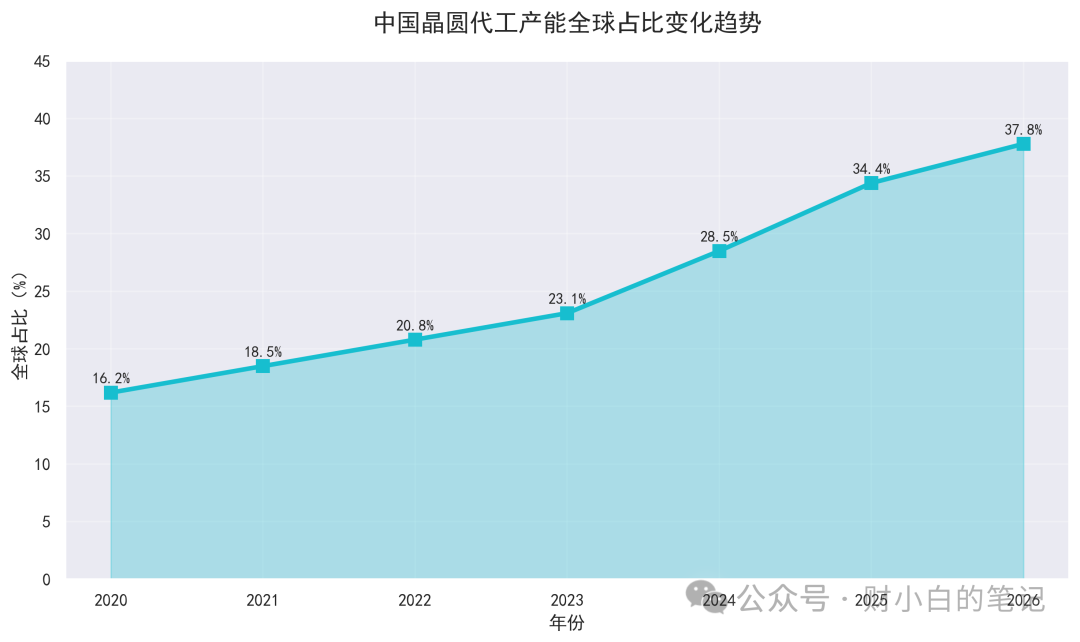

In 2025, the global semiconductor market has quietly reached a new milestone of $700 billion, with China becoming the world’s largest production region for the first time, holding 34.4% of wafer foundry capacity.

Driven by strong demand in AI computing power, smart vehicles, and industrial intelligence, the Chinese semiconductor industry has completed a leap from “single-point breakthroughs” to “chain collaboration”: chip design companies have entered the global second tier, wafer manufacturing capacity is expanding at the fastest rate in the world, advanced packaging technology has achieved “curve overtaking”, and the localization rate of equipment and materials is steadily increasing.

This article mainly analyzes the five key segments of chip design, wafer manufacturing, packaging and testing, semiconductor equipment, and semiconductor materials, and provides trend predictions for the future.

Industry Scale Growth Trend (2020-2025)

Analysis of the Five Key Segments of the Industry Chain

Chip Design: Five Powers Stand Together, Ecosystem is King

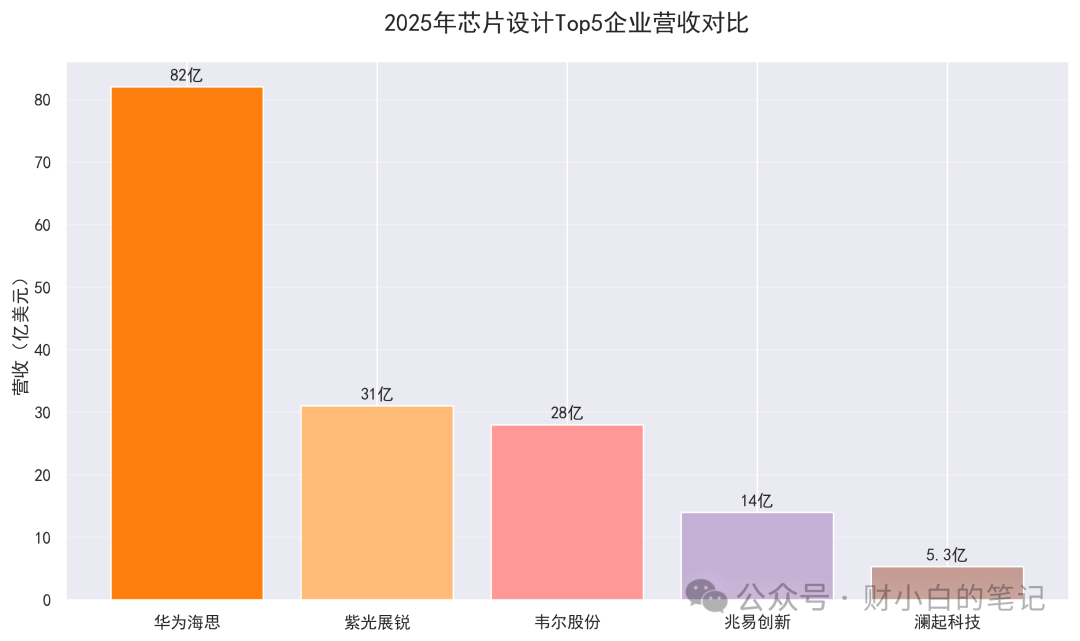

In 2025, the scale of the Chinese chip design market will exceed $75 billion, with five companies: Huawei HiSilicon, UNISOC, Will Semiconductor, GigaDevice, and Montage Technology, collectively holding about **28%** market share, covering almost all high-value tracks such as mobile SoC, CIS, storage, and interfaces, forming a competitive landscape of “five powers standing together”.

| Company | 2025 Revenue* | Global Market Share | Core Product Line | Technology / Customer Highlights |

|---|---|---|---|---|

| Huawei HiSilicon | $8.2 billion | Mobile AP 4% | Kirin 9000S, Ascend AI, Base Station Chips | 7 nm return, dual drive of Huawei terminals + operators |

| UNISOC | $3.1 billion | Mid-to-low-end SoC 10% | T820/770 Series, IoT Chips | Second globally for mobile SoC under $99, 25% share in cellular IoT |

| Will Semiconductor | $2.8 billion | CIS 11% | OV64B/OV50D Automotive CIS | Global leader in automotive CIS, Tier 1 for Tesla and BYD |

| GigaDevice | $1.4 billion | NOR Flash 18.5% | GD25/55 Series, Automotive MCU | Over 100 million automotive NOR shipments, main supplier for NIO and Xpeng |

| Montage Technology | $530 million | Memory Interface Chips 45% | DDR5 RCD/DB | Intel, AMD certified, standard for AI servers |

Top 5 Chip Design Revenue Comparison (2025)

Wafer Manufacturing: Three Giants Lead, Capacity is King

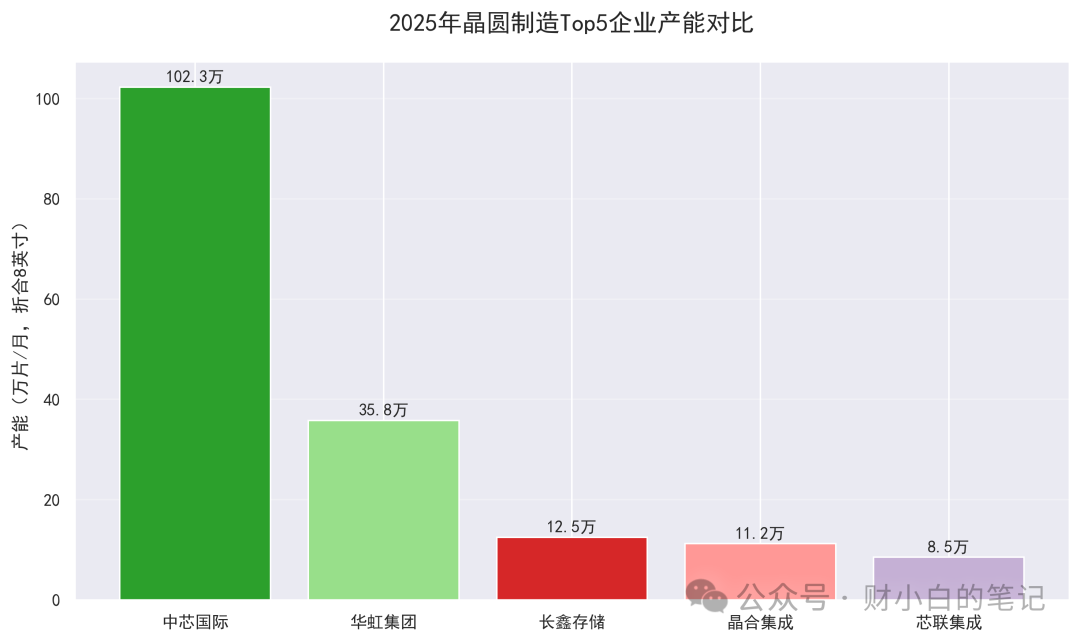

In 2025, the wafer foundry capacity in mainland China (equivalent to 8 inches) will reach 4.1 million wafers/month, accounting for **34.4%** of the global market, with five companies: SMIC, Hua Hong Semiconductor, ChangXin Memory Technologies, JCET, and Chipone contributing a total of 78% of the capacity, forming a tier of “three giants and two newcomers”.

| Company | 2025 Capacity* | Process Node | 2025 Revenue | Core Customers |

|---|---|---|---|---|

| SMIC | 1.023 million wafers/month | 7 nm–28 nm | $6.84 billion | Qualcomm, Huawei, GigaDevice |

| Hua Hong Semiconductor | 358,000 wafers/month | 55 nm–90 nm BCD | $2.54 billion | Infineon, BYD |

| ChangXin Memory Technologies | 125,000 wafers/month | 19 nm DRAM | $1.87 billion | Lenovo, HP |

| JCET | 112,000 wafers/month | 55 nm–110 nm | $910 million | North China Innovation, Geke Micro |

| Chipone | 85,000 wafers/month | 90 nm SiC | $730 million | NIO, Xpeng |

Top 5 Wafer Manufacturing Capacity Comparison (2025)

Packaging and Testing: Advanced Packaging, Chinese Teams Lead

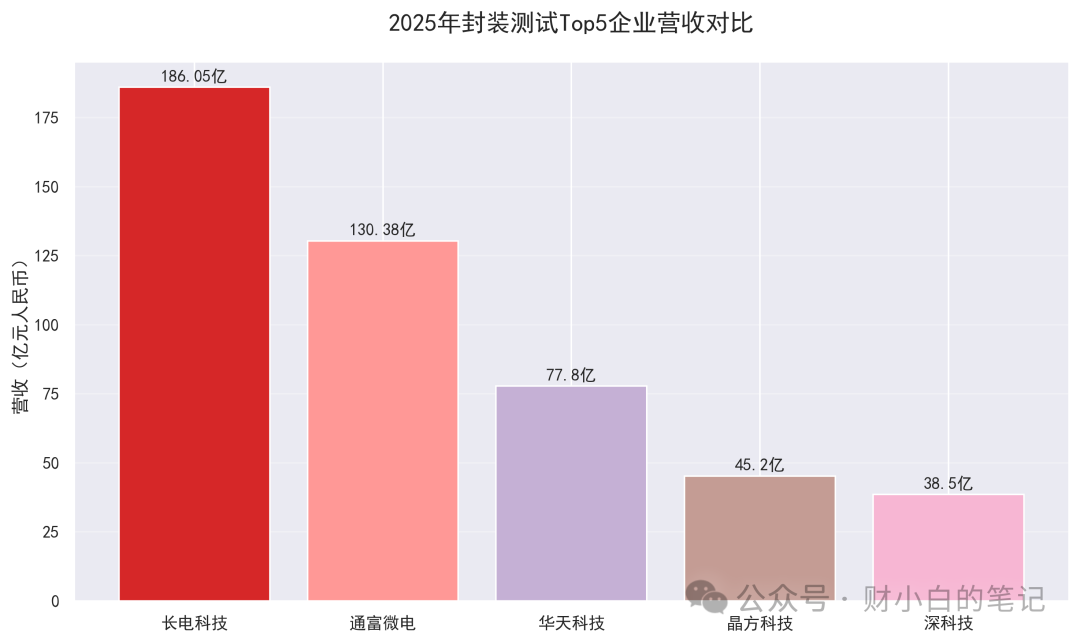

In 2025, the global advanced packaging market will reach $56.9 billion, with China’s three major OSAT (Outsourced Semiconductor Assembly and Test) giants: JCET, Tongfu Microelectronics, and Huatian Technology collectively holding over **50%** market share. Together with Chipone Technology and Shentian Technology, the five companies will achieve a total revenue of 45 billion yuan, forming a pattern of “three super and two strong”.

| Company | 2025 Revenue | Advanced Packaging Share | Technology Node | Core Customers |

|---|---|---|---|---|

| JCET | 18.6 billion yuan | 45% | 4 nm Chiplet mass production | Apple, NVIDIA, Huawei |

| Tongfu Microelectronics | 13 billion yuan | 40% | 5 nm FC-BGA | AMD, MediaTek |

| Huatian Technology | 7.8 billion yuan | 35% | 7 nm Fan-out | Sony, BYD |

| Chipone Technology | 3.2 billion yuan | 60% | 12″ WLCSP | OmniVision, Geke Micro |

| Shentian Technology | 2.4 billion yuan | 25% | SiP Modules | Xiaomi, OPPO |

Top 5 Packaging and Testing Revenue Comparison (2025)

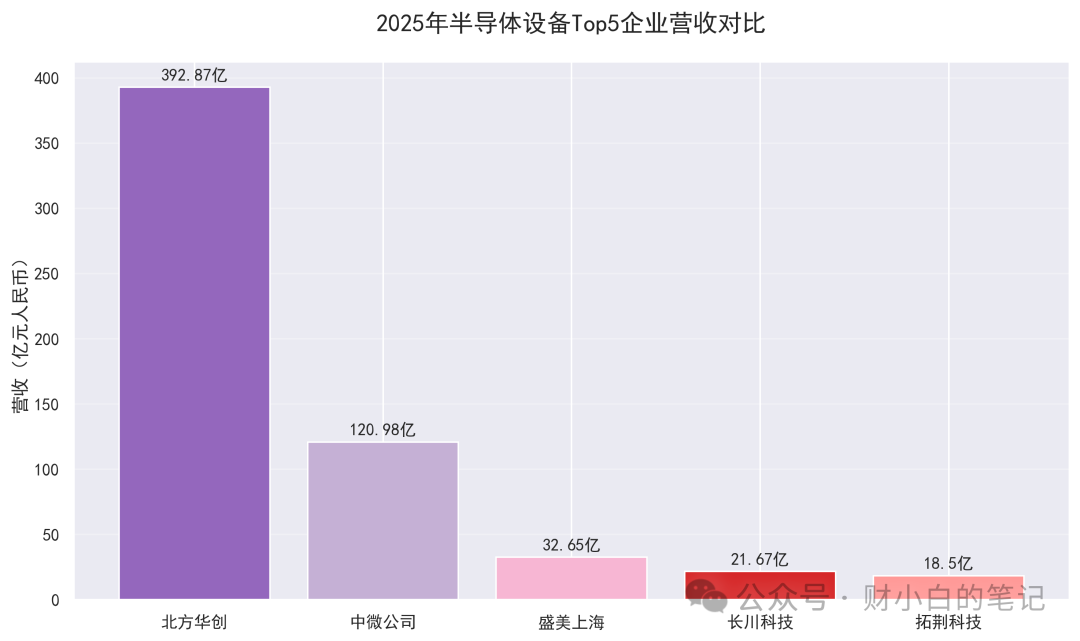

Semiconductor Equipment: Accelerating Domestic Substitution

In addition, by 2025, the scale of the Chinese semiconductor equipment market will reach 174 billion yuan, with five companies: North Huachuang, Zhongwei Company, Shanghai Semei, Changchuan Technology, and TuoJing Technology achieving a total revenue of over 60 billion yuan. The localization rate will increase from 23% in 2023 to **35%**, with remarkable breakthroughs achieved in key areas such as etching, thin films, cleaning, and testing.

| Company | 2025 Revenue | Core Equipment | Technology Node | Main Customers |

|---|---|---|---|---|

| North Huachuang | 39.3 billion yuan | Etching / PVD / CVD | 14 nm | SMIC, Yangtze Memory |

| Zhongwei Company | 12.1 billion yuan | CCP Etching | 5 nm | Taiwan Semiconductor Manufacturing Company, Micron |

| Shanghai Semei | 6.5 billion yuan | Cleaning / Plating | 7 nm | SK Hynix, Hua Hong |

| Changchuan Technology | 4.2 billion yuan | Testing Machines / Sorting Machines | 5 nm | ASE, Tongfu |

| TuoJing Technology | 3.8 billion yuan | ALD / PECVD | 28 nm | SMIC, Yuexin |

Top 5 Semiconductor Equipment Revenue Comparison (2025)

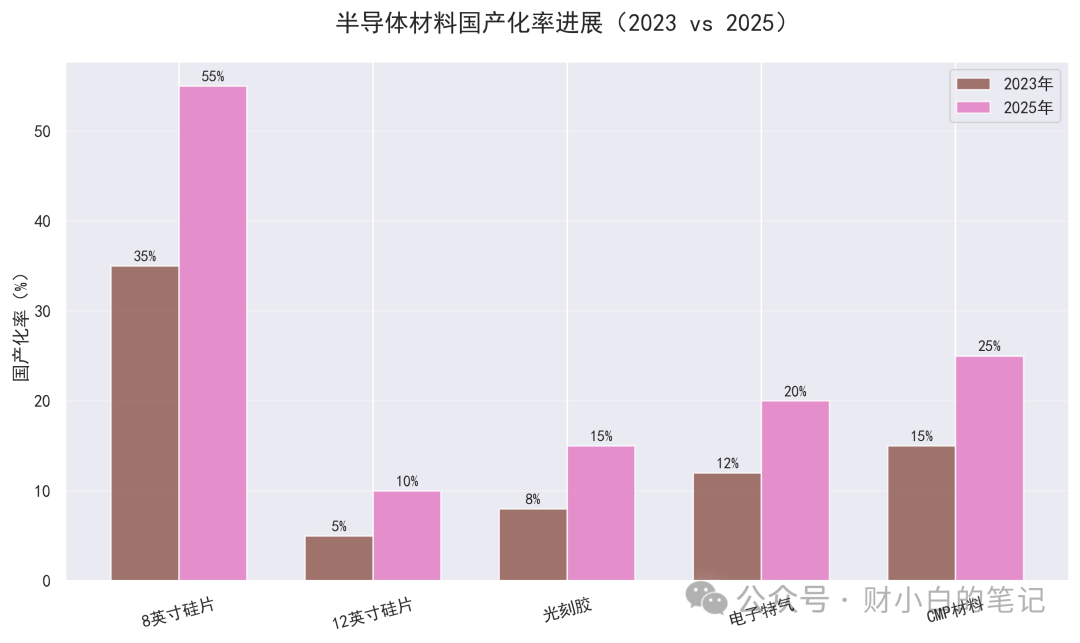

Semiconductor Materials: Steady Increase in Localization Rate, High-end Materials Still Face Severe “Bottleneck” Issues

In 2025, the scale of the Chinese semiconductor materials market will reach 174.08 billion yuan, with the global market share increasing from 9% in 2020 to **17.4%**, but in high-end silicon wafers, photoresists, and electronic specialty gases, there is still a high dependence on imports, with an overall localization rate of less than **30%**, and technical bottleneck issues still exist.

| Material Category | 2025 Market Size | Localization Rate | Domestic Leaders | Technical Progress |

|---|---|---|---|---|

| Silicon Wafers | 48 billion yuan | 12-inch 10% | Shanghai Silicon Industry | 300 mm silicon wafer monthly production of 750,000 wafers |

| Photoresists | 12 billion yuan | ArF 2% | Nanda Optoelectronics | ArF validated by SMIC |

| Electronic Specialty Gases | 10 billion yuan | 15% | Huate Gas | 55 products replacing imports |

| Sputtering Targets | 8 billion yuan | 38% | Jiangfeng Electronics | Second globally for ultra-pure tantalum targets |

| CMP Materials | 6 billion yuan | 20% | Anji Technology | Copper polishing solution enters TSMC |

Progress of Localization Rate of Semiconductor Materials (2020-2025)

Trend of China’s Wafer Foundry Capacity Global Share (2020-2025)

Technological Development Trends: Future Chiplet and SiC Become Dual Engines

The Chiplet technology has become an important path to “beyond Moore’s Law”, with the global Chiplet market expected to reach $3.1 billion in 2025, and to surge to $107 billion by 2033, with a compound annual growth rate of 42.5%. Companies like JCET and Tongfu Microelectronics have achieved 4 nm Chiplet mass production, providing key support for global AI computing power chips.

At the same time, SiC (Silicon Carbide) power devices are rapidly penetrating scenarios such as new energy vehicles and photovoltaic energy storage, with the global SiC market expected to reach $3 billion in 2025, and China’s market share increasing from 15% in 2023 to **25%**. Chipone’s 8-inch SiC production line will be put into operation in 2025, with a monthly production of 85,000 wafers, providing main drive inverter chips for NIO and Xpeng, with its SiC MOSFET on-resistance as low as 1.8 mΩ, performance comparable to Wolfspeed.

Challenges and Opportunities: Finding Breakthroughs Amidst “Bottlenecks”

Despite significant progress in the Chinese semiconductor industry by 2025, challenges remain in areas such as high-end lithography machines, EUV photoresists, and 12-inch silicon wafers. The export restrictions on ASML’s EUV lithography machines have hindered SMIC’s expansion of processes below 7 nm, and the localization rate of 12-inch silicon wafers is only **10%**, with high-end photoresists being 100% reliant on imports.

However, with the arrival of the 344 billion yuan funding for the third phase of the Big Fund, along with special funds from Shanghai, Shenzhen, Wuxi, and other places, the process of domestic substitution is expected to accelerate. By 2027, it is anticipated that:

- The localization rate of 12-inch silicon wafers will increase to 20%

- The localization rate of ArF photoresists will increase to 10%

- EUV photoresists are expected to achieve breakthroughs in laboratory settings

Future Outlook: The Blueprint for China’s Semiconductor Future

By 2027, the Chinese semiconductor industry is expected to achieve the following goals:

Capacity Wafer foundry capacity (equivalent to 8 inches) will exceed 5 million wafers/month, accounting for **40%** of the global market, becoming the world’s largest production region.

Technology The yield of 7 nm processes will increase to **95%**, and 5 nm processes will achieve small-scale mass production, with Chiplet technology leading globally.

Localization The localization rate of semiconductor equipment will increase to **50%**, and the localization rate of materials will increase to **30%**, with breakthroughs in high-end photoresists.

Ecosystem A fully controllable ecosystem of “design-manufacturing-packaging-testing-equipment-materials” will be formed, becoming an important pillar of the global semiconductor industry.

Conclusion: A Historical Leap from “Following” to “Leading”

By 2025, the Chinese semiconductor industry has shifted from “following” to “running alongside”, and has achieved a “leading” position in emerging fields such as Chiplet, advanced packaging, and SiC. Although high-end processes and materials still face challenges, with a large domestic market, continuous policy support, and innovative investments from enterprises, the Chinese semiconductor industry is poised for a historical leap from “quantitative change” to “qualitative change”. In the next three years, with technological breakthroughs and ecosystem improvements, China is expected to play an increasingly important role in the global semiconductor industry.