The recent surge in chip design mergers continues, following the acquisition of the industry’s third loss-making company (reference: Beiyi Micro Acquires Xingan Semiconductor: 12 Years of Chip Entrepreneurship, 130 Million Loss, 295 Million Valuation), with two more merger announcements.Interestingly, both of these cases involve mergers in the RF SoC chip sector, with one being a publicly listed RF SoC chip company as the buyer and the other being a startup RF SoC chip company as the seller.In the announcement regarding Tailin Micro’s acquisition of 100% equity in Panqi Micro, both parties have Bluetooth RF SoC chip product lines, and Panqi Micro complements Tailin Micro with its Sub-1G, 5G-A passive cellular IoT product line and industrial-grade customer base in power, water meters, and industrial control.

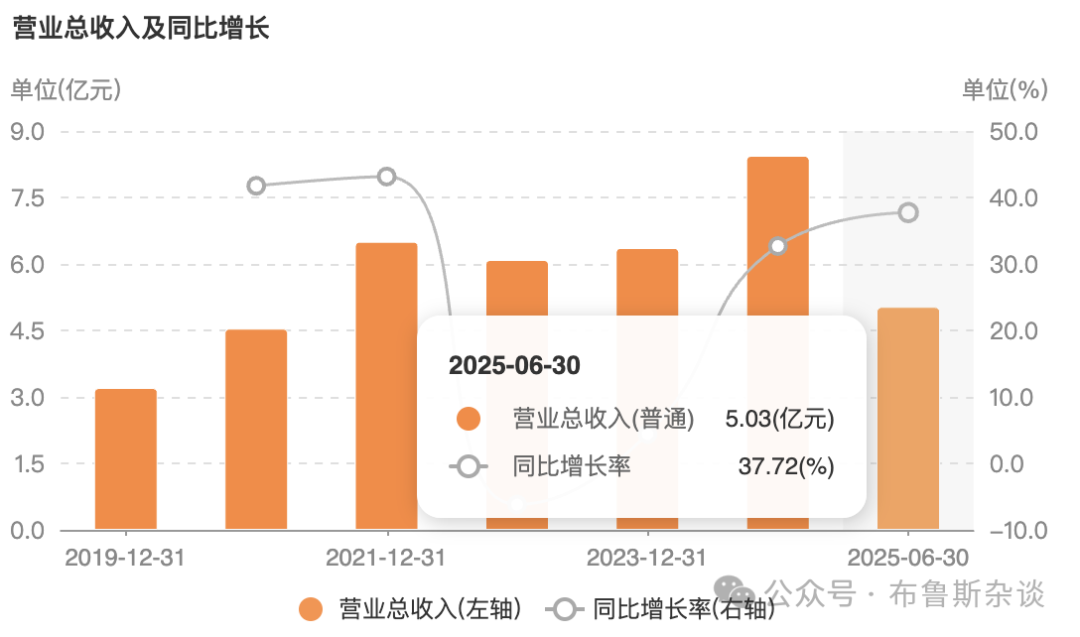

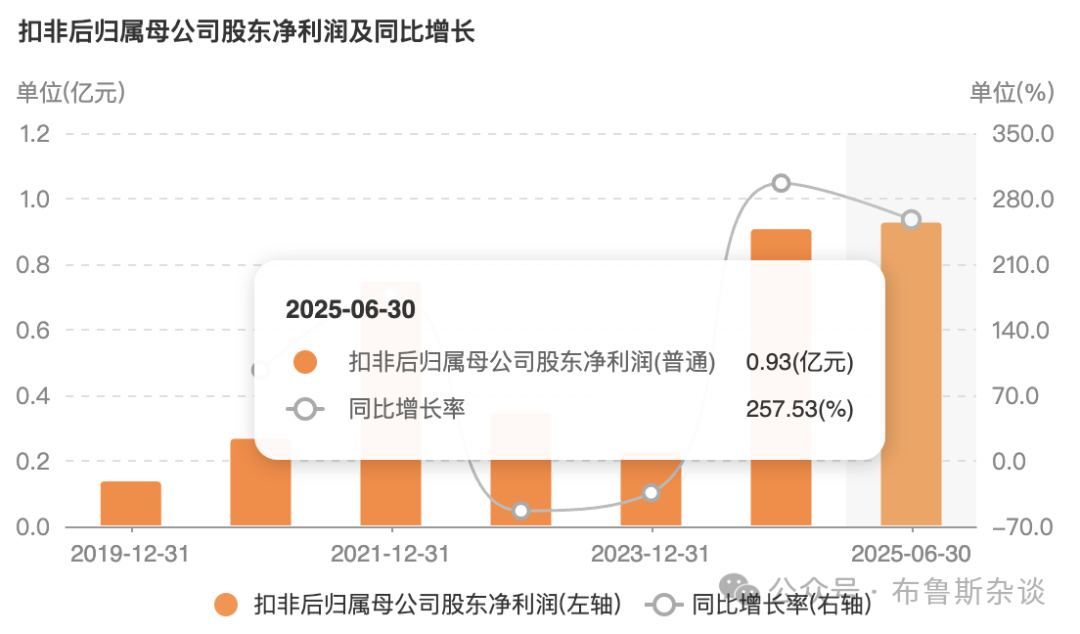

In the recently released mid-year report for 2025, Tailin Micro’s performance is impressive: revenue of 503 million yuan, a year-on-year increase of 37.72%; net profit attributable to the parent company of 93 million yuan, exceeding last year’s total; gross margin of 50.61% and net profit margin of 18.48%, both ranking in the top 20 among A-share chip design companies.

In the recently released mid-year report for 2025, Tailin Micro’s performance is impressive: revenue of 503 million yuan, a year-on-year increase of 37.72%; net profit attributable to the parent company of 93 million yuan, exceeding last year’s total; gross margin of 50.61% and net profit margin of 18.48%, both ranking in the top 20 among A-share chip design companies.

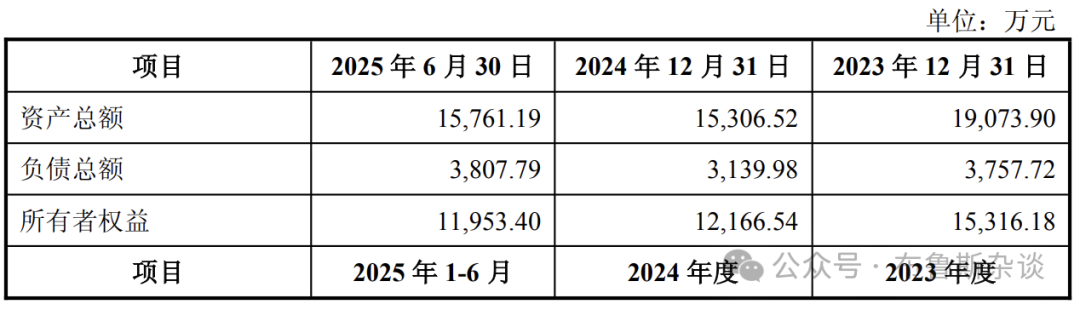

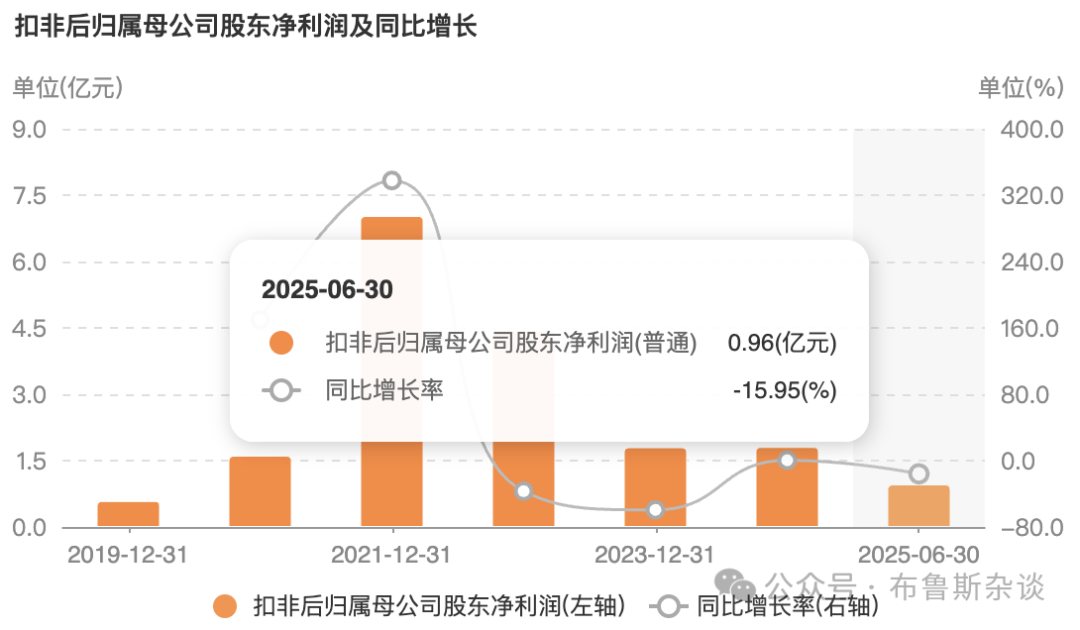

Founded in 2011, Panqi Micro has gone through six rounds of financing. According to the announcement, the revenues for 2023, 2024, and the first half of 2025 are projected to be 119 million yuan, 129 million yuan, and 75 million yuan, with net losses of 40.39 million yuan, 31.49 million yuan, and 2.13 million yuan respectively.This marks the fourth loss-making company in the chip design industry to be acquired.As of June 30, 2025, Panqi Micro’s net assets are 119 million yuan.The valuation and plan for this acquisition have not yet been determined. Considering Panqi Micro’s historical financing exceeding 200 million yuan and the two previous loss-making company acquisitions being valued at a price-to-sales ratio within 4 times, it is speculated that this valuation will be within 500 million yuan.Tailin Micro has a cash reserve of approximately 1.9 billion yuan, which should be sufficient for payment, but the company still chooses to pay through a combination of private placement and cash.The specific plan is expected to be released soon.The acquisition of Xingchen Technology’s 53.3087% stake in Furui Kun is an even more interesting case.Xingchen Technology was previously mentioned as a mature team starting anew, and is currently the youngest chip design company in the A-share market (established in December 2017).

Founded in 2011, Panqi Micro has gone through six rounds of financing. According to the announcement, the revenues for 2023, 2024, and the first half of 2025 are projected to be 119 million yuan, 129 million yuan, and 75 million yuan, with net losses of 40.39 million yuan, 31.49 million yuan, and 2.13 million yuan respectively.This marks the fourth loss-making company in the chip design industry to be acquired.As of June 30, 2025, Panqi Micro’s net assets are 119 million yuan.The valuation and plan for this acquisition have not yet been determined. Considering Panqi Micro’s historical financing exceeding 200 million yuan and the two previous loss-making company acquisitions being valued at a price-to-sales ratio within 4 times, it is speculated that this valuation will be within 500 million yuan.Tailin Micro has a cash reserve of approximately 1.9 billion yuan, which should be sufficient for payment, but the company still chooses to pay through a combination of private placement and cash.The specific plan is expected to be released soon.The acquisition of Xingchen Technology’s 53.3087% stake in Furui Kun is an even more interesting case.Xingchen Technology was previously mentioned as a mature team starting anew, and is currently the youngest chip design company in the A-share market (established in December 2017).

The core team of MStar followed Boss Lin to create SigmaStar. Due to the long-term cooperation foundation with many clients, the company achieved over 700 million yuan in ISP chip revenue within two years of establishment, reaching breakeven, and quickly began IPO operations, successfully going public in 2024. Although performance has fluctuated due to industry cycles, the revenue scale has maintained above 2 billion, and the market value post-IPO has exceeded 30 billion, allowing the team to benefit.

Bruce Wan, WeChat Public Account: Bruce’s Talks on Insights from 2024 Chip Design Company Mergers

After going public, although the revenue scale remains above 2 billion and the company is still profitable, the decline in profitability is quite evident.

The acquired Furui Kun specializes in Bluetooth SoC chips, with products shipped in consumer, industrial, medical, and automotive sectors, but its performance is not outstanding, with revenue approaching 100 million yuan in 2024, still in the red, and expected to turn profitable in the first half of 2025.

The acquired Furui Kun specializes in Bluetooth SoC chips, with products shipped in consumer, industrial, medical, and automotive sectors, but its performance is not outstanding, with revenue approaching 100 million yuan in 2024, still in the red, and expected to turn profitable in the first half of 2025.

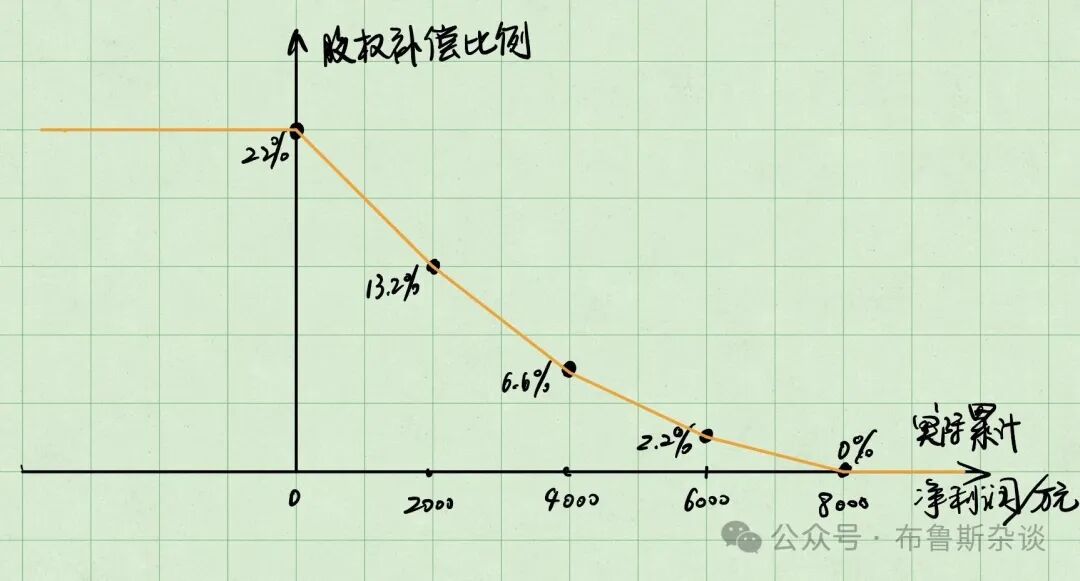

According to disclosures from Xingchen Technology, the purpose of this acquisition is to strengthen its own AI SoC capabilities in near-field sensing, device interconnectivity, low-power control, and audio processing, better capturing the application demands of edge-side AI.This acquisition is straightforward, with a cash purchase of 4.11 million yuan for 53.3087% equity.Interestingly, all the acquired shares are from investment institutions exiting, while the founders retain their shares (which cannot be liquidated).The founding team also bears performance commitments: a cumulative net profit of no less than 100 million yuan from 2026 to 2028. If the performance commitment is less than 80% fulfilled, they need to compensate with equity, thus the PE valuation based on performance commitments is approximately 15.41 times.The equity compensation plan is also intriguing; in the worst-case scenario of net profit loss, they need to compensate 22% of equity, and based on the fulfillment of performance commitments, the compensation is divided into four ranges: 0-80%, with equity compensation of 40%, 30%, 20%, and 10% respectively, as detailed in the following image.

According to disclosures from Xingchen Technology, the purpose of this acquisition is to strengthen its own AI SoC capabilities in near-field sensing, device interconnectivity, low-power control, and audio processing, better capturing the application demands of edge-side AI.This acquisition is straightforward, with a cash purchase of 4.11 million yuan for 53.3087% equity.Interestingly, all the acquired shares are from investment institutions exiting, while the founders retain their shares (which cannot be liquidated).The founding team also bears performance commitments: a cumulative net profit of no less than 100 million yuan from 2026 to 2028. If the performance commitment is less than 80% fulfilled, they need to compensate with equity, thus the PE valuation based on performance commitments is approximately 15.41 times.The equity compensation plan is also intriguing; in the worst-case scenario of net profit loss, they need to compensate 22% of equity, and based on the fulfillment of performance commitments, the compensation is divided into four ranges: 0-80%, with equity compensation of 40%, 30%, 20%, and 10% respectively, as detailed in the following image. The general idea is that the higher the fulfillment of performance commitments, the smaller the proportion of equity that needs to be compensated.Xingchen Technology also offers the Furui Kun founding team rewards for exceeding performance commitments: for every additional 10 million in actual cumulative net profit beyond the commitment, an additional 4.02 million in cash or stock is awarded (up to a maximum of 80.4 million).After 2028, the founding team can attempt to liquidate their equity, provided the team remains intact, performance is not too poor, and the absolute valuation does not exceed 1.5 billion yuan, with the PE valuation expected not to exceed this acquisition.For the selling founding team, this is undoubtedly a very reasonable and considerate arrangement.It is somewhat lamentable that Furui Kun, established in 2014, has gone through eight rounds of financing, achieving revenue close to 100 million yuan, with losses only in the millions, and could have continued to survive on its own.However, under pressure from the exit of investment institution shareholders, they relinquished control of the company, with the founding team retaining shares and becoming employees.The excess equity returns that belong to entrepreneurs have turned into performance incentives for professional managers: good performance can earn rewards, while poor performance incurs penalties.The frenzy of capital has ended, and the founding team has given up on unrealistic overnight wealth, as the industry gradually returns to normal.Driving these two merger cases is the hot market in the RF SoC chip niche.As an important component of the IoT edge-side AI ecosystem, the market demand for RF SoC chips is indeed increasing, and the competitive landscape is relatively favorable. Tailin Micro’s performance growth as a leader in this niche is also evident.Therefore, this sector has recently attracted widespread attention from publicly listed chip design companies, with several listed companies expanding their RF SoC chip products through mergers or self-development.It can be seen that while demand is increasing, supply is also rapidly increasing.Whether this leads to flourishing growth or another chaotic situation depends on which grows faster: demand or supply.The frightening aspect of China’s speed is that the growth rate of supply exceeds that of any other country in the world.It often also exceeds any increase in global demand.

The general idea is that the higher the fulfillment of performance commitments, the smaller the proportion of equity that needs to be compensated.Xingchen Technology also offers the Furui Kun founding team rewards for exceeding performance commitments: for every additional 10 million in actual cumulative net profit beyond the commitment, an additional 4.02 million in cash or stock is awarded (up to a maximum of 80.4 million).After 2028, the founding team can attempt to liquidate their equity, provided the team remains intact, performance is not too poor, and the absolute valuation does not exceed 1.5 billion yuan, with the PE valuation expected not to exceed this acquisition.For the selling founding team, this is undoubtedly a very reasonable and considerate arrangement.It is somewhat lamentable that Furui Kun, established in 2014, has gone through eight rounds of financing, achieving revenue close to 100 million yuan, with losses only in the millions, and could have continued to survive on its own.However, under pressure from the exit of investment institution shareholders, they relinquished control of the company, with the founding team retaining shares and becoming employees.The excess equity returns that belong to entrepreneurs have turned into performance incentives for professional managers: good performance can earn rewards, while poor performance incurs penalties.The frenzy of capital has ended, and the founding team has given up on unrealistic overnight wealth, as the industry gradually returns to normal.Driving these two merger cases is the hot market in the RF SoC chip niche.As an important component of the IoT edge-side AI ecosystem, the market demand for RF SoC chips is indeed increasing, and the competitive landscape is relatively favorable. Tailin Micro’s performance growth as a leader in this niche is also evident.Therefore, this sector has recently attracted widespread attention from publicly listed chip design companies, with several listed companies expanding their RF SoC chip products through mergers or self-development.It can be seen that while demand is increasing, supply is also rapidly increasing.Whether this leads to flourishing growth or another chaotic situation depends on which grows faster: demand or supply.The frightening aspect of China’s speed is that the growth rate of supply exceeds that of any other country in the world.It often also exceeds any increase in global demand.