Follow our official account and reply with “Summary”

Get the collection of nearly 400 abstracts from the 2025 European Interventional Cardiology Conference immediately.

Note: This article has a total of 10,033 words, with an estimated reading time of 26 minutes.Medical robots, as high-end intelligent devices in the medical equipment field, deeply integrate technologies from multiple disciplines such as medicine, mechanical engineering, artificial intelligence, and materials science. They aim to assist or replace medical personnel in performing medical operations, thereby enhancing diagnostic accuracy, reducing surgical risks, optimizing medical resource allocation, and promoting innovation in medical service models. Driven by the dual forces of an aging population and breakthroughs in artificial intelligence technology, the demand for their application continues to grow, gradually becoming a core force in the intelligent upgrade of medical systems. According to international mainstream classification standards, medical robots mainly encompass four types: surgical robots, rehabilitation robots, assistive robots, and service robots. Currently, medical robots are deeply integrated into the entire medical process with their characteristics of precision and efficiency, promoting not only the standardization of surgeries and scientific rehabilitation but also contributing to the construction of a smart medical ecosystem.This article will systematically discuss the current development status, core value, and industry challenges of medical robots based on the NextDevice® medical device database and industry practices for readers’ reference.

1. Overview of Medical Robots

The NextDevice® database shows that as of July 31, 2025, the popular tag “medical robots” has recorded 467 approved market registration certificates. According to national classification, the largest number of registration certificates is for active surgical instruments, commonly known as “surgical robots”, followed by medical rehabilitation instruments, i.e., “rehabilitation robots”. Notably, with the continuous innovation of medical technology, the concept of medical robots has generalized, and their application scenarios have expanded from traditional surgical fields to emerging fields such as rehabilitation and traditional Chinese medicine, showing an increasingly diversified trend. For example, rehabilitation robots provide personalized rehabilitation training through bio-signal recognition and exoskeleton drive; traditional Chinese medicine therapy robots assist in acupuncture and massage operations, enhancing treatment efficiency; service robots undertake repetitive tasks such as dispensing medication, nursing, and disinfection, optimizing medical resource allocation. However, despite the expanding application scope, products with high technical barriers and core competitiveness are still concentrated in high-end categories such as laparoscopic surgical robots.

Table 1: Classification of Approved Medical Devices Related to Medical Robots (Data as of 2025.07.31)

2. Overview of Surgical Robots

Under the concept label of “medical robots”, further filtering the medical service projects “clinical surgery” and “medical devices” allows us to filter all surgical robot device products, totaling 217 registration certificates, of which 165 are domestic and 52 are imported. In terms of medical services, the largest number of registration certificates is for “orthopedic robot surgical assistance”, i.e., orthopedic surgical robots, with 86 registration certificates approved, the technical difficulty mainly lies in positioning accuracy. The second largest is “endoscopic robot surgical assistance”, which includes laparoscopic surgical robots and natural orifice transluminal endoscopic surgery robots, with 38 registration certificates approved, the technical difficulty mainly lies in the coordination of imaging modules and flexible robotic arms.

Table 2: Classification of Surgical Robot Device Products (Data as of 2025.07.31)

Figure 1: Huake Precision Q300 Series Neurosurgery Micro Robot[1]

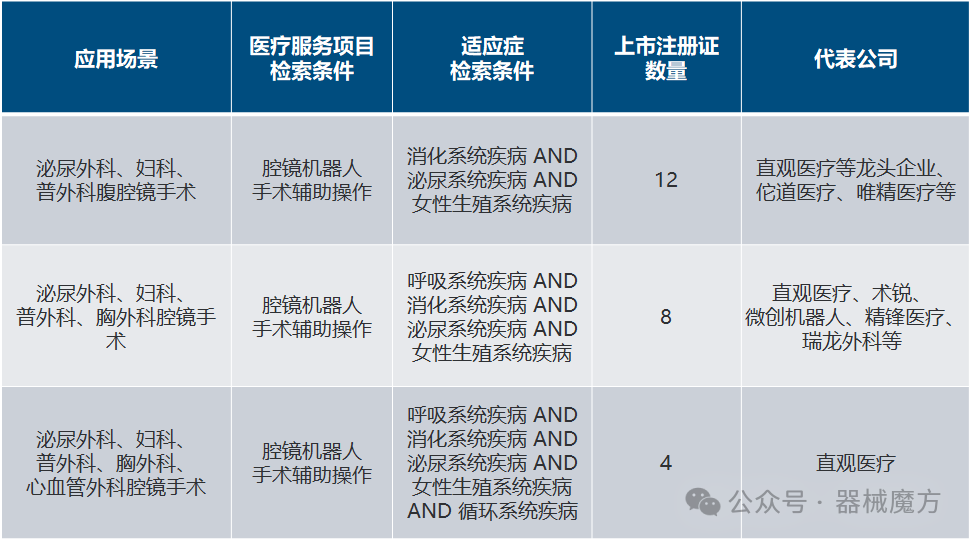

Using the “indications” field of NextDevice®, we can further filter the detailed application scenarios of surgical robots in various fields, as shown in Table 3. For example, orthopedic surgical robots can be filtered to include joint surgery robots, spinal surgery robots, trauma surgery robots, and ligament reconstruction surgical robots. Some surgical robot products have been approved for multiple fields of indications and can be used in multiple departments. For instance, in laparoscopic surgical robots, as shown in Table 4, a total of 12 products can be used simultaneously in urology, gynecology, and general surgery laparoscopic procedures, while Intuitive Surgical’s da Vinci surgical robot can be used in five departments: urology, gynecology, general surgery, thoracic surgery, and cardiovascular surgery, making it the laparoscopic surgical robot with the widest application range currently.

Table 3: Some Surgical Robot Device Detailed Application Scenarios (Data as of 2025.07.31)

Table 4: Some Laparoscopic Surgical Robot Devices Available for Multiple Departments (Data as of 2025.07.31)

In terms of the number of approved registration certificates, Medtronic Navigation Co., Ltd. has the most approvals, with a total of 7 registration certificates covering ENT surgical robots, neurosurgery surgical robots, and spinal surgery surgical robots. Following closely are Beijing Baihui Weikang Technology Co., Ltd. and Beijing Natong Medical Robot Technology Co., Ltd., each with 6 approved registration certificates. Notably, Beijing Tianzhihang Medical Technology Co., Ltd. successfully went public in 2020 on the Sci-Tech Innovation Board with its orthopedic robot products, becoming the “first stock of surgical robots” and currently the only surgical robot company listed on the Sci-Tech Innovation Board in China.

Table 5: Approval Status of Leading Domestic and Foreign Surgical Robot Companies (Based on the Number of Approved Registration Certificates, Data as of 2025.07.31)

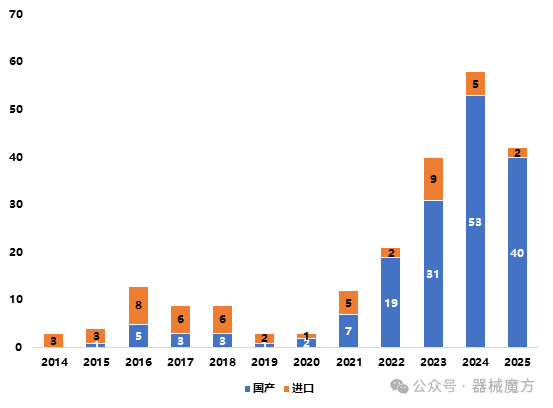

According to the first approval time field in the NextDevice® database, the data as of July 31, 2025, is shown in Figure 2. From the approval situation, early surgical robot devices in China were mainly dominated by imported products, but in recent years, the number of domestic products has exploded, increasing from only 7 domestic products approved in 2021 to 53 by 2024, and in the first seven months of 2025, the number of domestic approvals has reached 40. Analyzing solely from the number of approvals, domestic surgical robots have surpassed imported products in scale, showing a rapid catch-up trend.

Figure 2: Approval Status of Surgical Robots from 2014 to 2025

On the policy front, on March 13, 2024, the State Council issued the “Notice on Printing and Distributing the Action Plan for Promoting Large-scale Equipment Updates and Consumer Goods Replacement”[2], which mentioned, “Encourage qualified medical institutions to accelerate the update and transformation of medical equipment such as medical imaging, radiation therapy, telemedicine, and surgical robots.” This indicates that China is vigorously supporting the update and localization of surgical robots. However, in contrast, the journey of related surgical robot companies in China to go public has been fraught with difficulties. As shown in Table 6, currently, apart from Tianzhihang and MicroPort Robotics being listed on the A-share and Hong Kong stock markets respectively, Runmed is listed on the Hong Kong stock market but has no approved surgical robot products. Other surgical robot companies have not yet gone public, among which Jianjia Medical, Sizhe Rui, and Jingfeng Medical have submitted prospectuses, while Shurui Robotics once had plans to go public.

On the policy front, on March 13, 2024, the State Council issued the “Notice on Printing and Distributing the Action Plan for Promoting Large-scale Equipment Updates and Consumer Goods Replacement”[2], which mentioned, “Encourage qualified medical institutions to accelerate the update and transformation of medical equipment such as medical imaging, radiation therapy, telemedicine, and surgical robots.” This indicates that China is vigorously supporting the update and localization of surgical robots. However, in contrast, the journey of related surgical robot companies in China to go public has been fraught with difficulties. As shown in Table 6, currently, apart from Tianzhihang and MicroPort Robotics being listed on the A-share and Hong Kong stock markets respectively, Runmed is listed on the Hong Kong stock market but has no approved surgical robot products. Other surgical robot companies have not yet gone public, among which Jianjia Medical, Sizhe Rui, and Jingfeng Medical have submitted prospectuses, while Shurui Robotics once had plans to go public.

Table 6: Status of Surgical Robot Companies in China that Have IPOed or Plan to IPO

According to the NextDevice® database, Jianjia Medical’s joint replacement surgical navigation system (National Medical Device Approval No. 20223010462) has been approved as an innovative medical device, while Jingfeng Medical’s laparoscopic single-port surgical system (National Medical Device Approval No. 20233011753) and thoracoabdominal laparoscopic surgical system (National Medical Device Approval No. 20233011623) have also been approved as innovative medical devices. Shurui Robotics’ thoracoabdominal laparoscopic single-port surgical system (National Medical Device Approval No. 20233010833) has also been approved as an innovative medical device. Despite a considerable number of products recognized as innovative medical devices being approved, the aforementioned three companies (Jianjia, Jingfeng, Shurui) have not yet been able to go public as planned, and the reasons behind this may vary. However, it is undeniable that the commercialization of surgical robots has been relatively slow, and whether they can achieve profitability and expand commercialization is one of the key concerns for regulatory authorities. According to Tianzhihang’s 2024 annual report[3], the company has been in a state of loss for three consecutive years from 2022 to 2024, with losses exceeding 100 million RMB each year, reflecting the common difficulties in the industry. Under the current strong expectations for policy support and market growth, will the surgical robot industry have a promising future or face severe challenges?

According to the NextDevice® database, Jianjia Medical’s joint replacement surgical navigation system (National Medical Device Approval No. 20223010462) has been approved as an innovative medical device, while Jingfeng Medical’s laparoscopic single-port surgical system (National Medical Device Approval No. 20233011753) and thoracoabdominal laparoscopic surgical system (National Medical Device Approval No. 20233011623) have also been approved as innovative medical devices. Shurui Robotics’ thoracoabdominal laparoscopic single-port surgical system (National Medical Device Approval No. 20233010833) has also been approved as an innovative medical device. Despite a considerable number of products recognized as innovative medical devices being approved, the aforementioned three companies (Jianjia, Jingfeng, Shurui) have not yet been able to go public as planned, and the reasons behind this may vary. However, it is undeniable that the commercialization of surgical robots has been relatively slow, and whether they can achieve profitability and expand commercialization is one of the key concerns for regulatory authorities. According to Tianzhihang’s 2024 annual report[3], the company has been in a state of loss for three consecutive years from 2022 to 2024, with losses exceeding 100 million RMB each year, reflecting the common difficulties in the industry. Under the current strong expectations for policy support and market growth, will the surgical robot industry have a promising future or face severe challenges?

Figure 3: Shurui Snake Arm Surgical Robot

Source: Shurui Official Website[4]

3. Da Vinci Surgical Robot

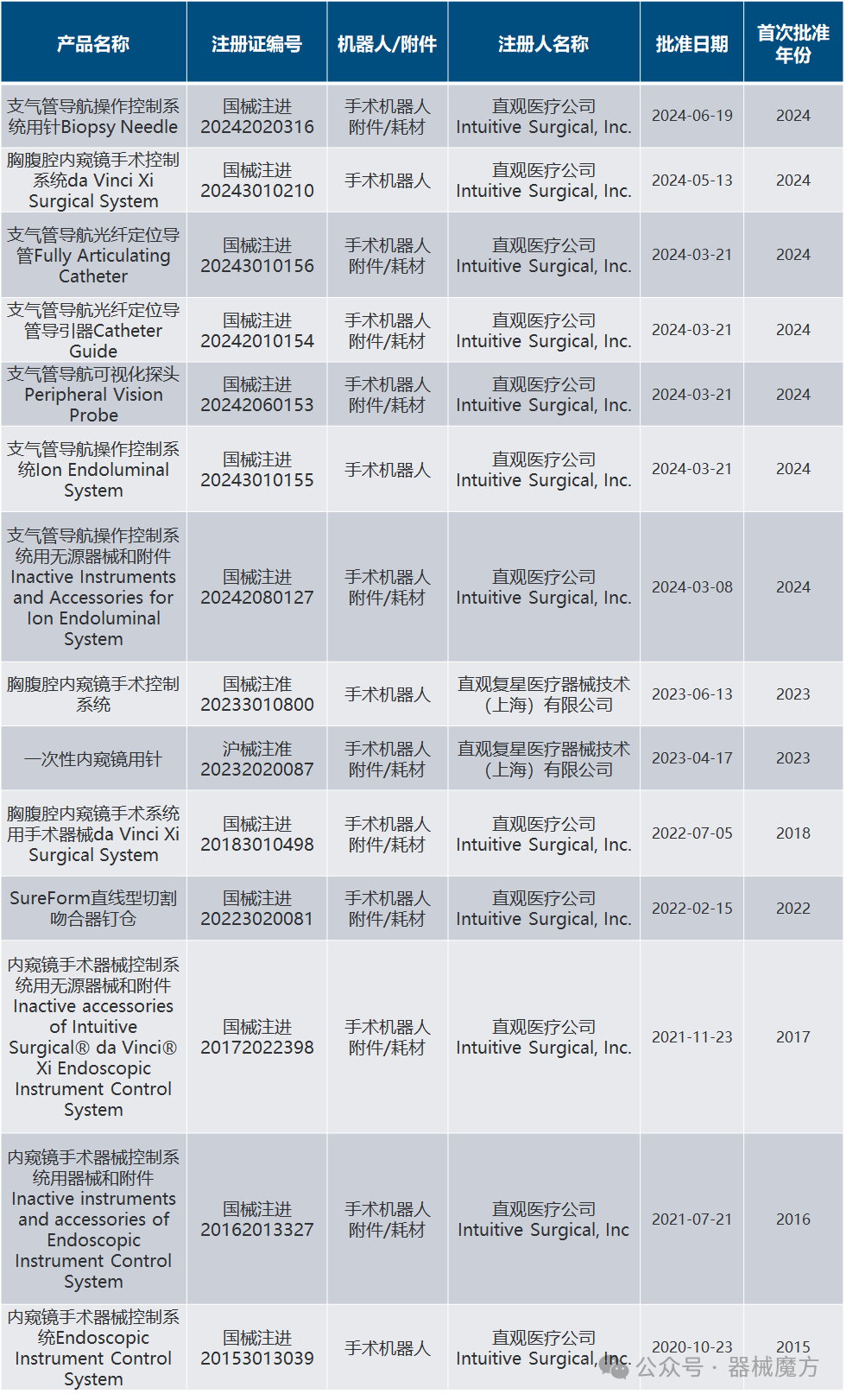

In fact, despite over a hundred domestic surgical robot products being approved, China’s surgical robot market has long presented a pattern of “one dominant player and many strong competitors”. The “one dominant player” refers to the Da Vinci robot, which holds an absolute dominant position in terms of market access time, brand influence, total installed volume, and surgical volume. The “many strong competitors” refer to domestic manufacturers that occupy relatively leading positions in their respective niche markets, such as Tianzhihang in orthopedic trauma and spinal fields, Jianjia Medical in joint replacement, Huake Precision in neurosurgery, and Sizhe Rui in laparoscopic robots. According to the NextDevice® database, as of July 31, 2025, Intuitive Surgical and Intuitive Fosun have a total of 14 surgical robot-related registration certificates approved and valid, of which 4 are surgical robots and 10 are surgical robot accessories/consumables.

Table 7: Approved and Valid Surgical Robot-Related Products from Intuitive Surgical and Intuitive Fosun

According to Intuitive Surgical’s company announcement[5] and the Chinese government announcement, on July 31, 2020, the National Health Commission of China issued the “Notice on Adjusting the Planning for Large Medical Equipment Configuration from 2018 to 2020”[6], which planned a total of 268 endoscopic surgical instrument control systems (surgical robots), of which 225 were planned for 2018-2020. Intuitive Surgical’s 2020 annual report shows that by the end of 2020, 111 Da Vinci robots had been sold in the Chinese market, almost monopolizing the domestic market. According to the National Health Commission’s announcement on June 21, 2023, the “Notice on the Release of the 14th Five-Year Plan for Large Medical Equipment Configuration”[7] states that during the 14th Five-Year Plan period, the planned number of laparoscopic surgical systems is 559 units. Intuitive Surgical’s 2024 annual report shows that under this quota, 121 Da Vinci robots have been sold in China.In terms of domestic surgical robots, according to MicroPort Robotics’ 2024 annual report[8], by the end of 2024, the Tumai laparoscopic robot had a cumulative global order of 60 units, with 39 new global orders signed in 2024, and over 30 units installed commercially, with 11 units installed in overseas markets. This suggests that the installation volume of Tumai in the domestic market in 2024 is approximately 20 units. From the above data, it can be seen that the Da Vinci robot still firmly occupies the domestic market.

According to Intuitive Surgical’s company announcement[5] and the Chinese government announcement, on July 31, 2020, the National Health Commission of China issued the “Notice on Adjusting the Planning for Large Medical Equipment Configuration from 2018 to 2020”[6], which planned a total of 268 endoscopic surgical instrument control systems (surgical robots), of which 225 were planned for 2018-2020. Intuitive Surgical’s 2020 annual report shows that by the end of 2020, 111 Da Vinci robots had been sold in the Chinese market, almost monopolizing the domestic market. According to the National Health Commission’s announcement on June 21, 2023, the “Notice on the Release of the 14th Five-Year Plan for Large Medical Equipment Configuration”[7] states that during the 14th Five-Year Plan period, the planned number of laparoscopic surgical systems is 559 units. Intuitive Surgical’s 2024 annual report shows that under this quota, 121 Da Vinci robots have been sold in China.In terms of domestic surgical robots, according to MicroPort Robotics’ 2024 annual report[8], by the end of 2024, the Tumai laparoscopic robot had a cumulative global order of 60 units, with 39 new global orders signed in 2024, and over 30 units installed commercially, with 11 units installed in overseas markets. This suggests that the installation volume of Tumai in the domestic market in 2024 is approximately 20 units. From the above data, it can be seen that the Da Vinci robot still firmly occupies the domestic market.

Figure 4: Da Vinci Surgical Robot

Source: Intuitive Surgical Official Website[9]

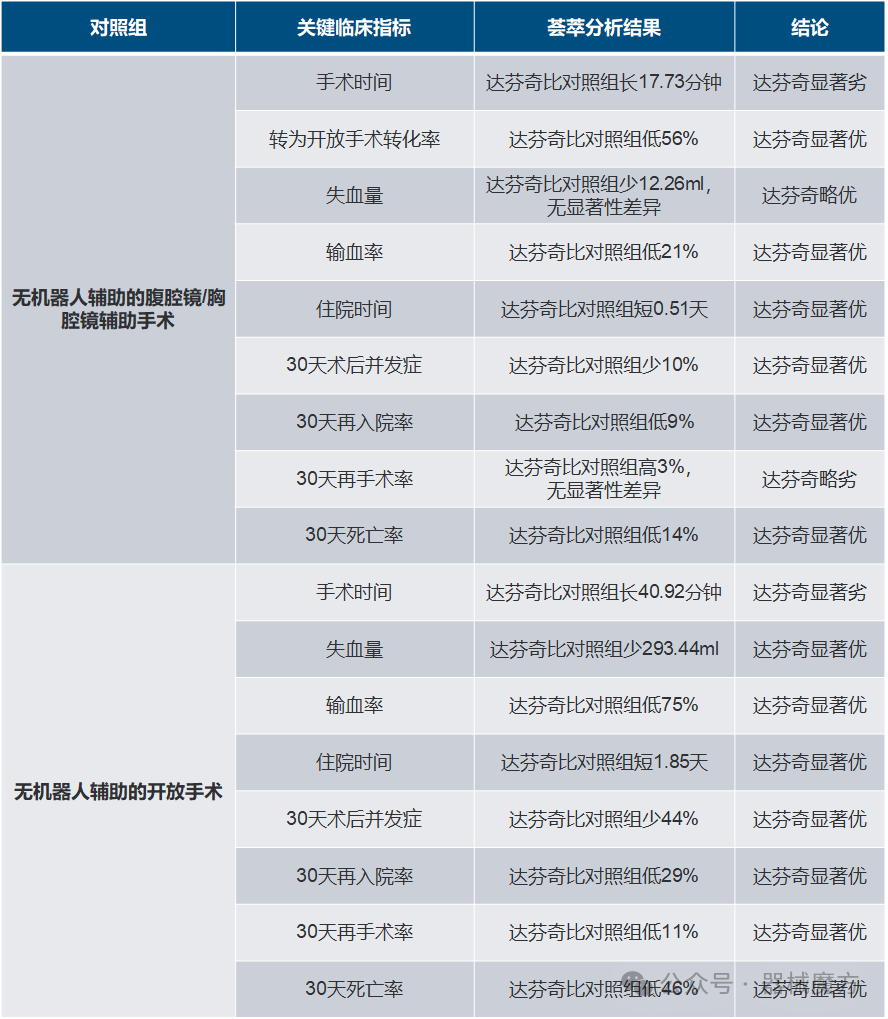

The long-term “occupation” of the domestic and international markets by the Da Vinci surgical robot is due to multiple factors. According to announcements from Intuitive Surgical and information disclosed by the FDA[5], in March 1997, surgeons successfully performed surgery on a human using an early prototype of Intuitive Surgical, and in July 1997, the early prototype received FDA 510(k) clearance (Approval No.: K965001), allowing the surgical control console and patient cart to be used with specific rigid endoscopes and simple instruments (such as blunt dissection instruments, retractors, and stabilizers). By June 2000, the early Da Vinci system had completed over 600 surgeries, including more than 200 general and vascular surgeries, over 10 gynecological surgeries, and over 400 thoracic surgeries. Based on successful clinical applications, in July 2000, the first-generation Da Vinci surgical robot received FDA 510(k) clearance (Approval No.: K990144), with the approved product name being “Intuitive Surgical Endoscopic Instruments, Intuitive Surgical Endoscopic Instrument Control System”, used to assist in controlling various endoscopic instruments during laparoscopic surgeries (such as cholecystectomy or fundoplication). In March 2001, the Da Vinci system expanded its applicability to non-cardiac thoracoscopic surgeries (Approval No.: K002489), and the name “Da Vinci” first appeared in the product name.On September 7, 2001, surgeon Jacques Marescaux successfully performed a cholecystectomy on a 68-year-old female patient via remote control of the Zeus surgical robot located in Strasbourg, France. This surgery was named the “Lindbergh Operation” in honor of the first pilot to fly solo across the Atlantic, Charles Lindbergh, and the results were published in the journal Nature[11]. This surgery showcased the potential of surgical robots to the world, and the Zeus surgical robot used in this surgery was developed by Computer Motion, which posed a significant challenge to the Da Vinci robot in its early days. However, Computer Motion was acquired by Intuitive Surgical in 2003, and the Da Vinci robot thus “inherited” the reputation of the Zeus robot. A multicenter prospective trial published in June 2005[12] showed that using the Da Vinci surgical robot for mitral valve repair in 112 patients with moderate to severe mitral regurgitation across 10 medical centers resulted in an average robotic system operation time of 77.9 minutes and an overall surgical time of 266.4 minutes. Although the surgical time was longer than traditional open-heart mitral valve repair surgery, there were no deaths, strokes, or device-related complications, and the average hospital stay was 4.7 days, which was better than traditional surgery. From the above information, it can be seen that the Da Vinci surgical robot accumulated rich clinical success experience, clinical data, and academic reputation shortly after its approval.In 2025, an important meta-analysis published by institutions such as Massachusetts General Hospital affiliated with Harvard University (“The COMPARE Study: Comparing Perioperative Outcomes of Oncologic Minimally Invasive Laparoscopic, da Vinci Robotic, and Open Procedures: A Systematic Review and Meta-analysis of the Evidence”)[13] comprehensively assessed the clinical effects of Da Vinci robot-assisted surgery compared to laparoscopic/thoracoscopic and open surgeries in the field of oncological surgery. This study integrated 230 clinical studies from 2010 to 2022, and the results showed that although the surgical time was relatively longer, the Da Vinci robot demonstrated significant advantages in various oncological surgeries, including lower conversion rates to open surgery, less intraoperative blood loss and transfusion requirements, shorter postoperative hospital stays, and lower postoperative complications, readmission rates, and mortality rates.

Table 8: Results of RCT Clinical Trials of Da Vinci Surgical Robot Meta-analysis[13]

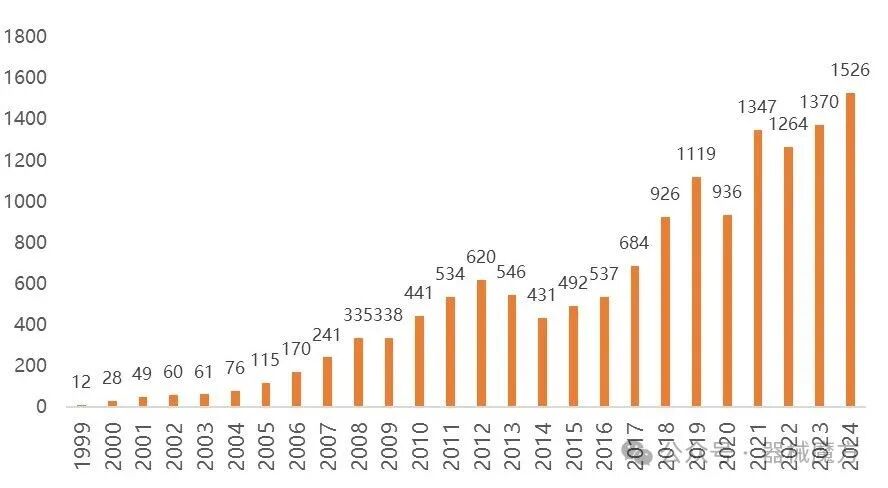

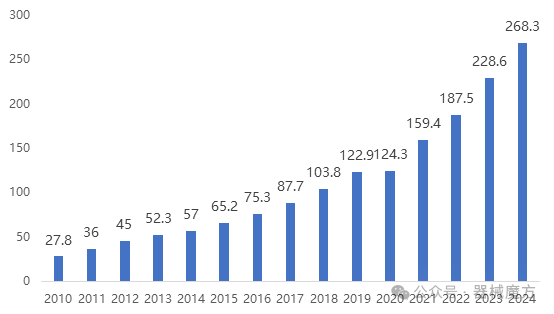

With strong clinical evidence and patent layout, the sales volume of the Da Vinci surgical robot has been rising year after year, forming a de facto monopoly in the surgical robot industry. According to the annual report disclosed by Intuitive Surgical[5], as shown in Figure 5, the sales volume of the Da Vinci surgical robot has rapidly increased from 12 units in 1999 to 1,526 units in 2024, and is expected to continue to rise. By the end of 2024, over 14,000 Da Vinci robots had been sold globally, completing 9,902 installations. In terms of surgical volume, as shown in Figure 6, in 2024, the Da Vinci surgical robot completed approximately 2.68 million surgeries, and by the end of 2024, the total number of surgeries completed exceeded 16 million.

With strong clinical evidence and patent layout, the sales volume of the Da Vinci surgical robot has been rising year after year, forming a de facto monopoly in the surgical robot industry. According to the annual report disclosed by Intuitive Surgical[5], as shown in Figure 5, the sales volume of the Da Vinci surgical robot has rapidly increased from 12 units in 1999 to 1,526 units in 2024, and is expected to continue to rise. By the end of 2024, over 14,000 Da Vinci robots had been sold globally, completing 9,902 installations. In terms of surgical volume, as shown in Figure 6, in 2024, the Da Vinci surgical robot completed approximately 2.68 million surgeries, and by the end of 2024, the total number of surgeries completed exceeded 16 million.

Figure 5: Annual Global Sales Volume of Da Vinci Surgical Robot (Units)

Source: Company Announcement[5]

Figure 6: Annual Global Surgical Volume of Da Vinci Surgical Robot (10,000 Cases)

4. The Path of Domestic Surgical Robot Localization and Replacement

4.1 Improvement and Breakthrough of the Upstream Supply Chain of Surgical Robots

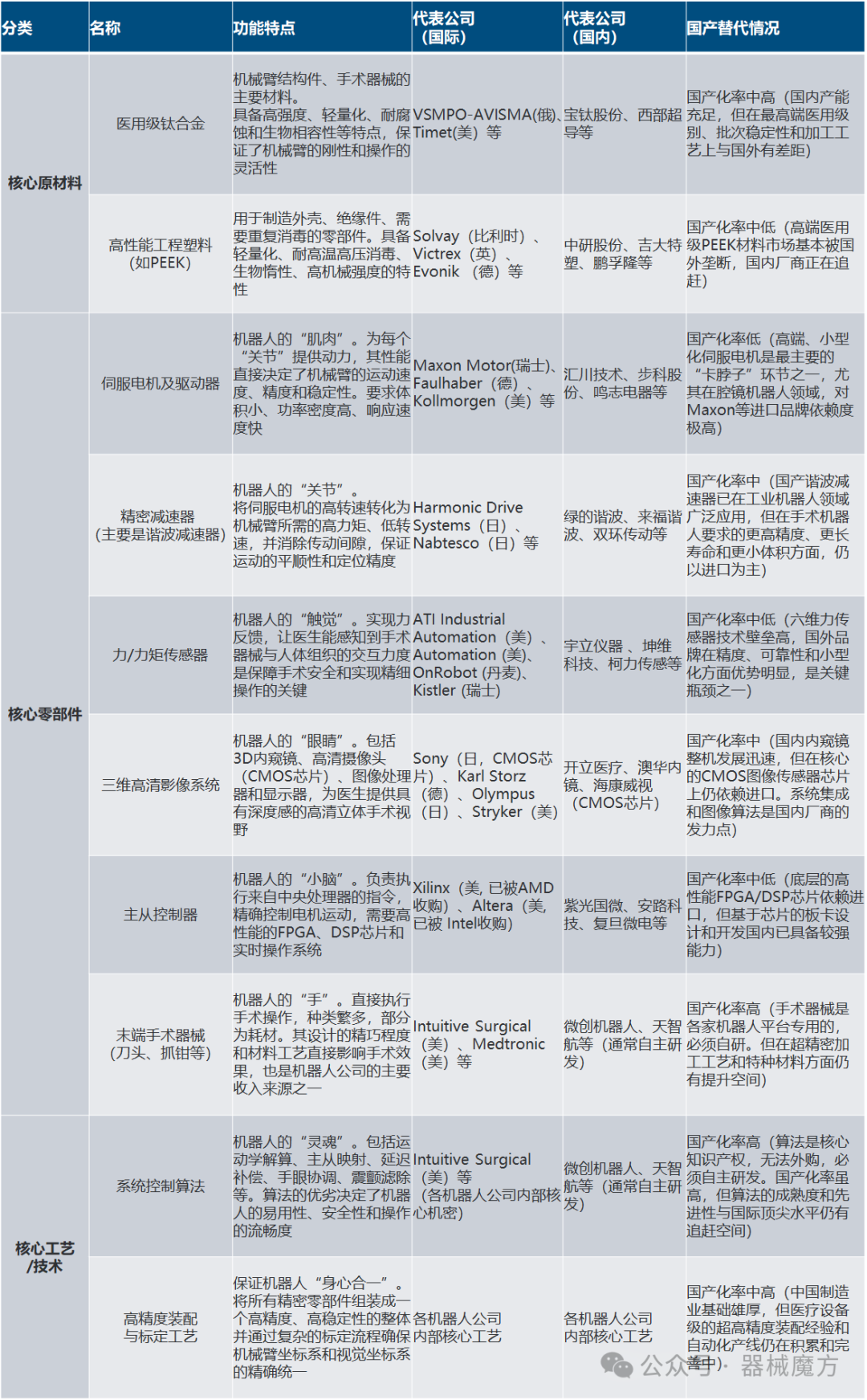

Overall, the upstream industrial chain of surgical robots in China shows a characteristic of “strong software and weak hardware”, meaning that in areas related to software, algorithms, and system integration, such as control algorithms and surgical instrument design, domestic companies are relatively mature in technology. However, in core hardware, especially components such as servo motors, precision reducers, force sensors, and high-end chips that require long-term precision manufacturing processes, the level of localization is low, which is a major bottleneck for industrial development. As new surgical robot products continue to be approved and launched in China, the enormous market demand is forcing upstream component suppliers to tackle technical challenges and achieve localization. Therefore, the sustainable and healthy development of China’s surgical robot industry in the future will not only depend on the technological innovation and market promotion of downstream manufacturers but also fundamentally rely on the maturity and breakthroughs of the upstream core component industrial chain.

Table 9: Main Technologies and Upstream Industrial Chain of Surgical Robots

4.2 Deepening Clinical Value and Data Accumulation

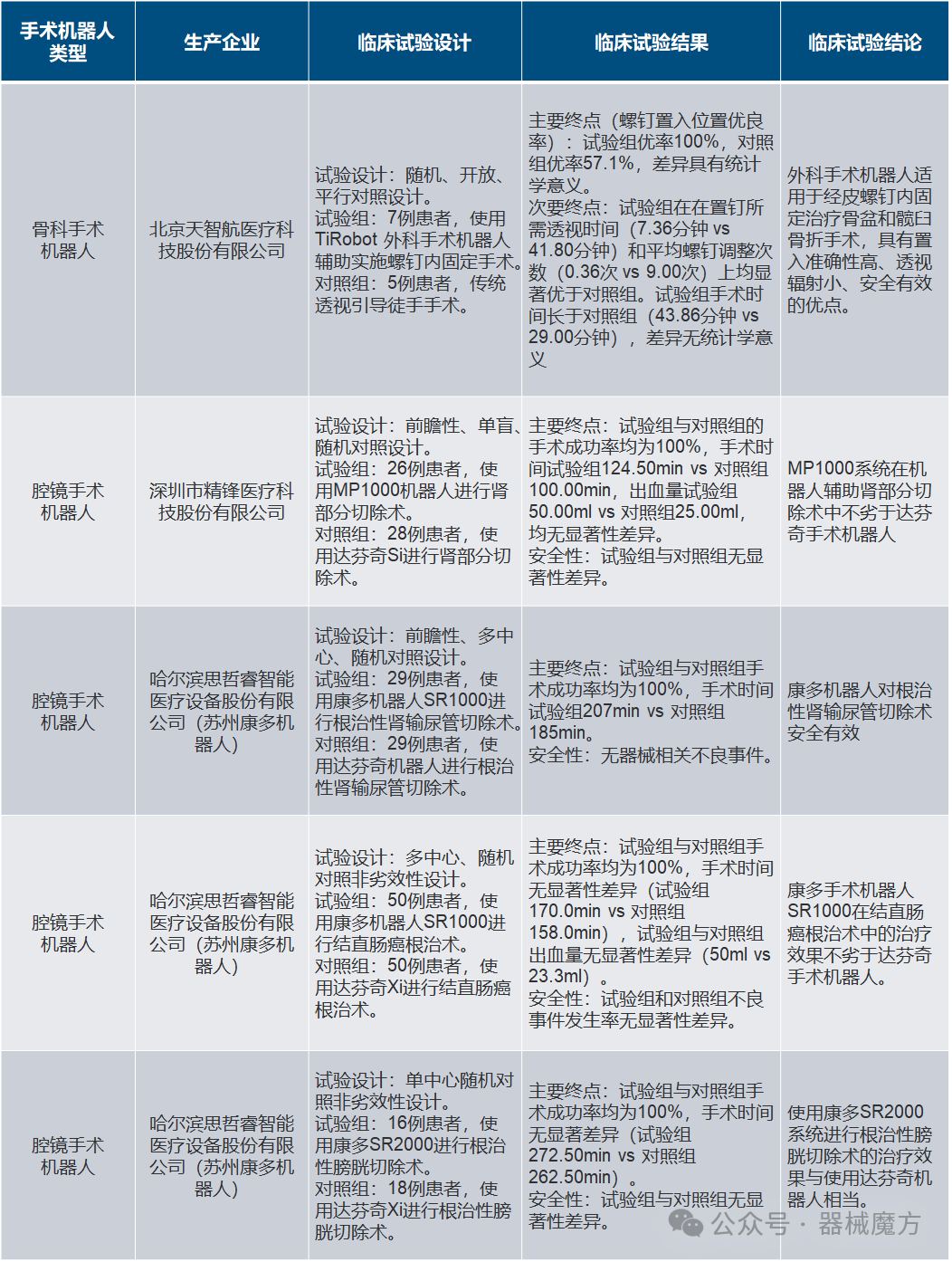

The successful path of the Da Vinci surgical robot may not be fully replicable today, but domestic manufacturers can still focus on accumulating strong clinical evidence to accelerate the replacement of hospital scenarios. Taking Tianzhihang as an example, according to the company’s announcement[3], in July 2016, Beijing Jishuitan Hospital, the PLA General Hospital, and Tianjin Tianjin Hospital issued the “Clinical Trial Report of the TiRobot Surgical Robot Positioning System”, which is the core basis for the approval of its Tianji orthopedic surgical robot by the NMPA. In this clinical trial, the robot guided 55 operations, while 55 operations were performed manually by doctors using traditional methods. The trial results showed that the surgeries using the Tianji orthopedic surgical navigation robot had an average cumulative fluoroscopy time of 7.41 seconds, while the surgeries performed manually by doctors had an average cumulative fluoroscopy time of 44.65 seconds. Other literature indicates[14] that using fluoroscopy assistance for percutaneous placement of a single anterior column screw requires 62 fluoroscopy sessions, while the Tianji orthopedic surgical robot averaged no more than 8 fluoroscopy sessions during surgery, fully demonstrating that the Tianji orthopedic surgical robot has higher positioning accuracy compared to traditional surgery. In addition to Tianzhihang, Table 10 lists the current clinical trial results of surgical robots disclosed by regulatory reviews in China.

Table 10: Clinical Trial Status of Surgical Robots in China (Regulatory Review Disclosure Standard)

Data Source: Review Reports[15], Company Announcements[3,8,16,17]

Table 11: Summary of Clinical Trials of Some Surgical Robots in China (Literature Disclosure Standard)

Data Source: Academic Literature[18,19,20,21,22]

From Tables 10 and 11, it can be seen that clinical trials of surgical robots in China are flourishing, with many domestic manufacturers such as MicroPort, Weigao, Jingfeng, and Tianzhihang completing clinical trials of products in various fields such as laparoscopic, orthopedic, neurosurgery, and vascular intervention, achieving positive results. A significant commonality of these trials is that, except for orthopedic surgical robots, which can outperform traditional manual surgeries in terms of positioning accuracy and precision, most designs adopted a “non-inferiority study” approach. This means that the main goal of the trials is to prove that domestic robots are not inferior to traditional surgeries or already marketed similar products in terms of technical success rate, clinical effectiveness, and safety. From the results, almost all approved domestic robots successfully reached the preset endpoints, verifying their safety and effectiveness in clinical applications, paving the way for obtaining approval from the National Medical Products Administration (NMPA). However, while “non-inferiority” clinical trial results are a stepping stone to market entry, in market competition, this merely means “equally good” and is not sufficient to provide a compelling reason for hospitals to replace existing expensive equipment or traditional surgical processes. Therefore, for domestic surgical robots to truly break into the market, merely achieving “non-inferiority” is far from enough. Currently, Da Vinci occupies a dominant position due to its technological stability and first-mover advantage, while domestic products still have shortcomings in core components and clinical data accumulation, limiting cost control and high-end development. Therefore, in addition to ensuring the stability and reliability of the upstream supply chain, domestic surgical robot manufacturers must deepen clinical trial data to establish differentiated advantages. By providing richer clinical data to demonstrate the superiority of specific surgical types and collecting real-world data to optimize products, they can strengthen clinically driven innovation. Only by deeply engaging in clinical practice can they transition from “running alongside” to “leading” and capture market share.

4.3 Deep Differentiation Competitive Route

The rise of domestic surgical robots hinges on avoiding traditional strongholds of international giants and instead achieving differentiated technological breakthroughs in niche areas, thus avoiding direct competition with “Da Vinci” in traditional multi-port laparoscopic fields through technological innovation and scene adaptation to achieve “overtaking on a bend”.

- Single-port laparoscope: “Replacing imports before they arrive”, single-port laparoscopic robots have become a breakthrough for domestic companies due to their advantages of minimal trauma, quick recovery, and low cost. Currently, domestic companies such as Shurui and Jingfeng Medical have already made layouts;

- Flexible robotic arms: Breaking through the operational bottleneck in narrow spaces, driven by the operational needs in narrow anatomical spaces (such as the digestive tract and urethra), flexible robotic arm technology can overcome the limitations of Da Vinci’s rigid instrument arms, becoming a direction for differentiation competition;

- Force feedback technology: Simulating real tactile sensations, force feedback technology enhances operational precision through tactile simulation, for example, achieving precise control of end-effectors in laparoscopic surgeries. Combined with AI-assisted decision-making systems, it can further lower operational thresholds;

- AI + 5G: Reshaping the grassroots medical ecosystem, China’s medical resource allocation is imbalanced, making it very difficult for grassroots hospitals to perform surgeries. Therefore, domestic robots can respond to the national policy of sinking medical resources, solving the surgical implementation difficulties in grassroots hospitals and constructing a localized model of “equipment + service”.

- Specialized innovation: Opening up differentiated tracks, focusing on specialized fields such as hepatobiliary and urology, developing customized technologies to address clinical pain points, which can avoid homogenization competition while effectively solving the core needs of specialized surgeries.

In summary, domestic surgical robots need to focus on new-generation technologies and specialized approaches to avoid traditional patent barriers, using clinical value as a foundation, leveraging policy dividends and cost advantages, ultimately achieving a reversal in the high-end medical equipment field with “Made in China”.

4.4 Building an Independent Ecosystem

The high learning cost and steep learning curve of the Da Vinci surgical robot make it difficult for doctors who have become accustomed to using the Da Vinci robot for surgeries to change their habits and switch to another “non-inferior” surgical robot. Therefore, even if domestic manufacturers obtain innovative medical device registration certificates through innovative registration processes, it is challenging to replicate the Da Vinci model and rapidly expand the market. In this case, domestic manufacturers must invest resources to establish a training and certification system for doctors that rivals or even surpasses that of Da Vinci. For example, by collaborating with top hospitals and medical schools, they can incorporate the operation of domestic robots into standardized training for resident physicians, cultivating habits from the source. Furthermore, they can leverage cost advantages to actively explore the vast market of county-level hospitals, achieving rapid market penetration and thus building a comprehensive ecosystem for surgical robots.

5. Research and Development Status of Surgical Robots

As one of the key directions for breaking through domestic surgical robots, flexible robotic arms, with their bendable and winding characteristics, can overcome operational bottlenecks in narrow spaces, effectively addressing the limitations of traditional rigid robotic arms. This characteristic allows for precise operations in convoluted areas that traditional instruments find difficult to reach, aligning closely with the needs of minimally invasive and endoscopic surgeries. Among the companies developing flexible arm surgical robots, Robor Medical is one of the fastest progressors. According to the NextDevice® database, Robor Medical’s gastrointestinal endoscopic surgical instrument control device (National Medical Device Approval No. 20253010539) and the accompanying tissue forceps (National Medical Device Approval No. 20253011149) were approved for market launch on March 11, 2025, and June 20, 2025, respectively, both as innovative medical devices suitable for endoscopic submucosal dissection (ESD) of the esophagus and stomach, allowing for clamping and lifting of diseased tissues. According to the company’s official website[23], Robor Medical’s EndoFaster gastrointestinal endoscopic surgical robot system is one of the world’s leading natural orifice surgical robots and the first gastrointestinal endoscopic surgical assistance system to complete human clinical trials. Its flexible arm diameter can be controlled to about 3mm, achieving precise master-slave control with 4 degrees of freedom in the limited space of the gastrointestinal tract, significantly enhancing the safety of ESD. Currently, Robor Medical is working on developing a multi-channel gastrointestinal endoscopic surgical robot system to address the complexity of single-arm surgical robot procedures, which still require the operation of endoscopes and are physically demanding.

Figure 7: Robor Medical Gastrointestinal Endoscopic Surgical Robot (Approved for Market Launch, Multi-Channel Robot System Under Development)[23]

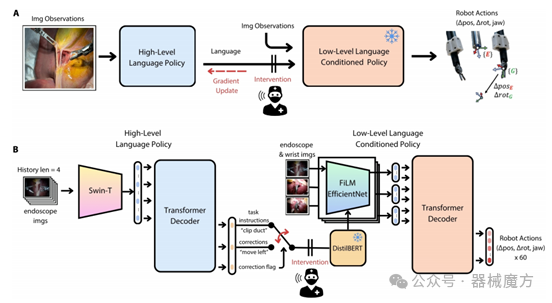

Robor Medical has established core advantages in flexible arm design and ESD specialty through differentiated technological paths. Its products are compatible with traditional endoscopic systems, retaining doctors’ operational habits while building technological barriers through over 80 core patents. Early deep clinical cooperation with Qilu Hospital of Shandong University provided a solid verification foundation for product implementation. With the approval of innovative devices, the company is accelerating the development of the second-generation dual-channel system EndoDreams to further address surgical efficiency and operational burden issues. In the future, Robor Medical is expected to leverage its flexible arm platform advantages to expand into more fields and penetrate the grassroots medical market with its low-cost and high compatibility features.Force feedback technology is another core direction for the evolution of surgical robots. Traditional laparoscopic surgical robot systems lack a force feedback mechanism, leading to a loss of “tactile sensation”, making it difficult for doctors to perform precise surgical operations based on sensitive touch, which somewhat reduces the safety of surgical robots and increases learning costs. The fifth-generation Da Vinci surgical robot introduced a force feedback mechanism, allowing doctors to perceive tissues through touch, enhancing operational precision. In a preclinical study published in 2025[24], 29 novice surgeons were divided into a force feedback group (15) and a no force feedback group (14), performing robot-assisted suturing surgeries on ex vivo pig bladders and aortas. The study results showed that force feedback significantly reduced the average applied force (bladder: 1.71 N vs 2.40 N; aorta: 1.80 N vs 2.53 N), average error counts (bladder: 0.59 vs 1.76; aorta: 0.38 vs 1.14), and task completion times (bladder: 659 seconds vs 781 seconds; aorta: 460 seconds vs 570 seconds), demonstrating the enormous potential of force feedback technology in improving surgical safety, efficiency, and teaching quality. Domestically, according to news released on March 1, 2025, on the official website of Tuodao Medical[25], Tuodao Medical is conducting a national key research and development project on “Surgical Robot Force Sensing and Force Feedback Technology”, aiming to break the monopoly of the Da Vinci surgical robot in the field of force feedback.Currently, while the flexible robotic arms and force feedback technology of surgical robots continue to optimize the doctor’s operational experience, achieving fully autonomous surgery remains a common vision for the industry. In July 2025, a cover study in Science Robotics[26] proposed the SRT-H (Hierarchical Surgical Robot Transformer) framework, which demonstrated the feasibility of this vision in ex vivo experiments for the first time. This system employs a unique “language planning + action imitation” dual-level architecture: the high-level strategy generates task instructions through natural language, while the low-level strategy translates them into precise instrument trajectories. In 8 fresh pig gallbladder experiments, SRT-H independently completed the critical steps of “clamping and cutting the gallbladder duct and gallbladder artery” during cholecystectomy, achieving a success rate of 100% with an average time of 317 seconds, and autonomously corrected 6 operational deviations on average for each surgery. Notably, this system maintained stable performance under non-standard conditions such as anatomical structure variations and simulated blood interference, demonstrating environmental adaptability that surpasses traditional preset path robots. Although there is still a gap between ex vivo experiments and clinical live applications, and the operational efficiency is currently lower than that of human physicians, the demonstrated step-level autonomy has laid the foundation for truly unmanned surgery.

Robor Medical has established core advantages in flexible arm design and ESD specialty through differentiated technological paths. Its products are compatible with traditional endoscopic systems, retaining doctors’ operational habits while building technological barriers through over 80 core patents. Early deep clinical cooperation with Qilu Hospital of Shandong University provided a solid verification foundation for product implementation. With the approval of innovative devices, the company is accelerating the development of the second-generation dual-channel system EndoDreams to further address surgical efficiency and operational burden issues. In the future, Robor Medical is expected to leverage its flexible arm platform advantages to expand into more fields and penetrate the grassroots medical market with its low-cost and high compatibility features.Force feedback technology is another core direction for the evolution of surgical robots. Traditional laparoscopic surgical robot systems lack a force feedback mechanism, leading to a loss of “tactile sensation”, making it difficult for doctors to perform precise surgical operations based on sensitive touch, which somewhat reduces the safety of surgical robots and increases learning costs. The fifth-generation Da Vinci surgical robot introduced a force feedback mechanism, allowing doctors to perceive tissues through touch, enhancing operational precision. In a preclinical study published in 2025[24], 29 novice surgeons were divided into a force feedback group (15) and a no force feedback group (14), performing robot-assisted suturing surgeries on ex vivo pig bladders and aortas. The study results showed that force feedback significantly reduced the average applied force (bladder: 1.71 N vs 2.40 N; aorta: 1.80 N vs 2.53 N), average error counts (bladder: 0.59 vs 1.76; aorta: 0.38 vs 1.14), and task completion times (bladder: 659 seconds vs 781 seconds; aorta: 460 seconds vs 570 seconds), demonstrating the enormous potential of force feedback technology in improving surgical safety, efficiency, and teaching quality. Domestically, according to news released on March 1, 2025, on the official website of Tuodao Medical[25], Tuodao Medical is conducting a national key research and development project on “Surgical Robot Force Sensing and Force Feedback Technology”, aiming to break the monopoly of the Da Vinci surgical robot in the field of force feedback.Currently, while the flexible robotic arms and force feedback technology of surgical robots continue to optimize the doctor’s operational experience, achieving fully autonomous surgery remains a common vision for the industry. In July 2025, a cover study in Science Robotics[26] proposed the SRT-H (Hierarchical Surgical Robot Transformer) framework, which demonstrated the feasibility of this vision in ex vivo experiments for the first time. This system employs a unique “language planning + action imitation” dual-level architecture: the high-level strategy generates task instructions through natural language, while the low-level strategy translates them into precise instrument trajectories. In 8 fresh pig gallbladder experiments, SRT-H independently completed the critical steps of “clamping and cutting the gallbladder duct and gallbladder artery” during cholecystectomy, achieving a success rate of 100% with an average time of 317 seconds, and autonomously corrected 6 operational deviations on average for each surgery. Notably, this system maintained stable performance under non-standard conditions such as anatomical structure variations and simulated blood interference, demonstrating environmental adaptability that surpasses traditional preset path robots. Although there is still a gap between ex vivo experiments and clinical live applications, and the operational efficiency is currently lower than that of human physicians, the demonstrated step-level autonomy has laid the foundation for truly unmanned surgery.

Figure 8: SRT-H Process for Fully Autonomous Robotic Surgery[26]

6. Investment and Financing Situation in the Surgical Robot Industry

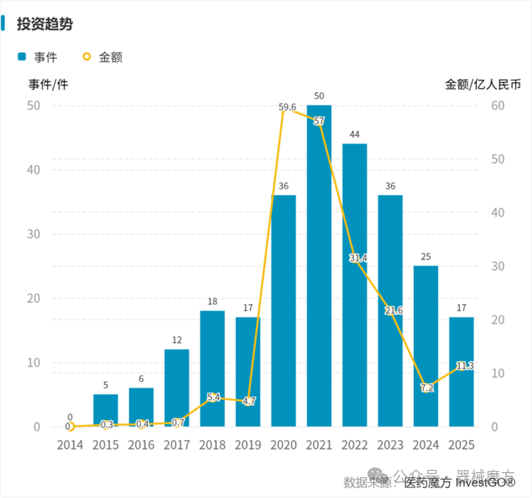

In terms of investment and financing, according to the InvestGO® database, the investment and financing heat in the “surgical robot” sector peaked between 2020 and 2021, with the highest financing amount in 2020, when MicroPort Robotics received a large strategic investment of 3 billion RMB. The number of financing events was highest in 2021, with Jingfeng Medical completing nearly 600 million RMB in Series B financing and over 200 million USD in Series C financing, while Shurui Robotics completed 300 million RMB in Series B financing in 2021. From 2022 to 2024, the financing heat gradually declined, but there has been a certain recovery trend in 2025 (as of July 31). In the long term, China’s enormous surgical volume and the evolution of automation technology are expected to enhance the global competitiveness of domestic surgical robots.

Figure 9: Investment Trend in the “Surgical Robot” Sector

7. Conclusion

Intuitive Surgical has not only brought surgical robots, which integrate various cutting-edge technologies, into the public eye but has also maintained a long-term monopoly in the market with the Da Vinci system. Today, over a hundred domestic surgical robot products have been approved for market launch, continuously challenging the throne of Da Vinci, the “number one”. However, Da Vinci has built a strong competitive moat with its deep patent barriers, vast clinical data accumulation, and the operational habits formed by doctors over time, coupled with the national restrictions on the number of large medical devices configured, making the market expansion path for domestic surgical robots full of challenges. To break through, these “new players” must rely on solid clinical evidence, build a complete ecosystem, and ensure the stability and reliability of the upstream supply chain to gradually capture market share. We look forward to the surgical robot industry accelerating the realization of domestic substitution under the promotion of collaborative innovation along the industrial chain, ultimately breaking the monopoly pattern of Da Vinci. At the same time, with continuous technological iterations and breakthroughs, we hope that surgical robots can evolve beyond the boundaries of “assisted operations” towards the goal of independently completing surgeries.

NextDevice Medical Device Database

NextDevice® is a medical device lifecycle database created by Medical Cube, covering four core scenarios in the device field: products, sales, R&D, and investment. The Cube has built a high-precision structured data system through “AI big data monitoring collection + professional data analyst review and cleaning”, deeply cleaning and standardizing information on device product classification, technology generations, medical service projects, indications, popular tracks, performance characteristics, and listing/bidding, etc.; at the same time, it further integrates and connects the global device labeling system, synchronizing information on devices under research and investment dynamics, achieving multi-dimensional competitive landscape analysis and decision support throughout the medical device lifecycle.

References:[1] Huake Precision Official Website[2] Chinese Government Website. Notice of the State Council on Printing and Distributing the Action Plan for Promoting Large-scale Equipment Updates and Consumer Goods Replacement.https://www.gov.cn/zhengce/content/202403/content_6939232.htm[3] Tianzhihang Company Announcement[4] Beijing Shurui Robotics Co., Ltd. Official Website[5] Intuitive Surgical, Inc. Company Announcement[6] Chinese Government Website. Notice of the National Health Commission on Adjusting the Planning for Large Medical Equipment Configuration from 2018 to 2020.https://www.gov.cn/zhengce/zhengceku/2020-08/01/content_5531860.htm[7] Chinese Government Website. Notice of the National Health Commission on the Release of the 14th Five-Year Plan for Large Medical Equipment Configuration.https://www.gov.cn/zhengce/zhengceku/202307/content_6889445.htm[8] MicroPort Robotics Company Announcement[9] Intuitive Surgical, Inc. Official Website[10] FDA.510(k) Premarket Notification[11] DOI: 10.1038/35096636.[12] DOI: 10.1016/j.jtcvs.2004.07.050.[13] DOI: 10.1097/SLA.0000000000006572.[14] DOI: 10.3969/j.issn.1671-167X.2017.02.017.[15] National Medical Products Administration Medical Device Technical Review Center. Medical Device Product Registration Technical Review Report[16] Sizhe Rui Company Announcement[17] Jianjia Medical Company Announcement[18] DOI: 10.3969/j.issn.1671-167X.2017.02.017.[19] DOI: 10.1097/JS9.0000000000001166.[20] DOI: 10.1590/S1677-5538.IBJU.2024.0230.[21] DOI: 10.1007/s00464-024-10682-5.[22] DOI: 10.1038/s41598-025-95382-3.[23] Robor Medical Official Website[24] DOI: 10.1007/s00464-024-11472-9.[25] Tuodao Medical. Tuodao Medical Takes on National Responsibilities, “Surgical Robot Force Sensing and Force Feedback Technology” National Key R&D Plan Project Officially Launched. https://www.tuodaomedical.com/uncategorized/356[26] DOI: 10.1126/scirobotics.adt5254.

References:[1] Huake Precision Official Website[2] Chinese Government Website. Notice of the State Council on Printing and Distributing the Action Plan for Promoting Large-scale Equipment Updates and Consumer Goods Replacement.https://www.gov.cn/zhengce/content/202403/content_6939232.htm[3] Tianzhihang Company Announcement[4] Beijing Shurui Robotics Co., Ltd. Official Website[5] Intuitive Surgical, Inc. Company Announcement[6] Chinese Government Website. Notice of the National Health Commission on Adjusting the Planning for Large Medical Equipment Configuration from 2018 to 2020.https://www.gov.cn/zhengce/zhengceku/2020-08/01/content_5531860.htm[7] Chinese Government Website. Notice of the National Health Commission on the Release of the 14th Five-Year Plan for Large Medical Equipment Configuration.https://www.gov.cn/zhengce/zhengceku/202307/content_6889445.htm[8] MicroPort Robotics Company Announcement[9] Intuitive Surgical, Inc. Official Website[10] FDA.510(k) Premarket Notification[11] DOI: 10.1038/35096636.[12] DOI: 10.1016/j.jtcvs.2004.07.050.[13] DOI: 10.1097/SLA.0000000000006572.[14] DOI: 10.3969/j.issn.1671-167X.2017.02.017.[15] National Medical Products Administration Medical Device Technical Review Center. Medical Device Product Registration Technical Review Report[16] Sizhe Rui Company Announcement[17] Jianjia Medical Company Announcement[18] DOI: 10.3969/j.issn.1671-167X.2017.02.017.[19] DOI: 10.1097/JS9.0000000000001166.[20] DOI: 10.1590/S1677-5538.IBJU.2024.0230.[21] DOI: 10.1007/s00464-024-10682-5.[22] DOI: 10.1038/s41598-025-95382-3.[23] Robor Medical Official Website[24] DOI: 10.1007/s00464-024-11472-9.[25] Tuodao Medical. Tuodao Medical Takes on National Responsibilities, “Surgical Robot Force Sensing and Force Feedback Technology” National Key R&D Plan Project Officially Launched. https://www.tuodaomedical.com/uncategorized/356[26] DOI: 10.1126/scirobotics.adt5254.