Comprehensive Overview of Domestic Computing Power Chip Core Tracks

1. AI Computing Power Chips

GPU: is the preferred acceleration chip in AI servers, with major participants in the GPU market including overseas manufacturers such as NVIDIA, AMD, Intel, Qualcomm, and ARM.

Domestic high-end AI chip manufacturers such as Cambricon, HW, Jingjia Micro, Haiguang Information, and Loongson Technology are accelerating their development.

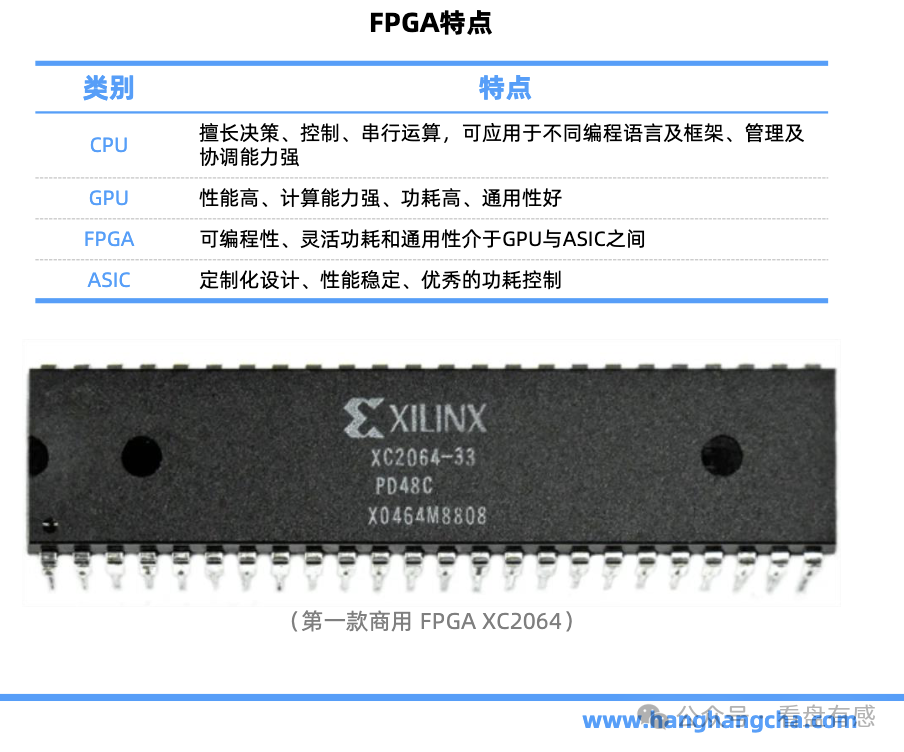

FPGA: is a type of semi-custom chip that can be flexibly programmed, allowing for pre-fabrication and programming in the lab or on-site, with advantages such as short development time and no need for tape-out.

The global FPGA market is dominated by Xilinx (now under AMD) and Altera (now under Intel). Domestic alternatives are still in the early stages, with clear differentiation among high, medium, and low-end products.

Domestic manufacturers Fudan Microelectronics, Anlogic, and Unisoc (a subsidiary of Unisoc) lead the domestic FPGA replacement, with other relevant companies including Jingwei Qili, Chengdu Huayi Electronics, Zhiduojing, and Gaoyun Semiconductor.

ASIC Chips: are mainly used for deep learning acceleration, showing significant advantages in efficiency and speed compared to other AI chips on the large model inference side.

Typical domestic ASIC chips include: Alibaba’s PingTouGe with the 含光800 AI chip; Baidu’s Kunlun series AI chips; Tencent’s self-developed dedicated chips for AI inference, video transcoding, and smart network cards, among others. Other relevant companies include Lanqi Technology, Allwinner Technology, Guokewai, Chunzhong Technology, and Shanshi Network Technology.

2. Raw Materials for Computing Power Chips

Silicon Wafers: are the basic material for computing power chips, accounting for about 35% of the market share, with purity and quality directly affecting chip performance.

Main manufacturers include Shanghai Silicon Industry, China Silicon Corporation, Liang Micro, China Crystal Technology, Zhizhong Technology, Yangjie Technology, Yuyuan Semiconductor, Shanghai Hejing, Jinrui Hong, and Nanjing Guosheng.

Electronic Specialty Gases: are the “blood” of the electronics industry, directly affecting chip performance, yield, and reliability, mainly used in etching and deposition processes.

The domestic electronic specialty gas replacement process is accelerating, with companies such as Huate Gas, Jinhong Gas, Yake Technology, China Shipbuilding Gas, Haohua Technology, Heyuan Gas, and Nanjing University of Posts and Telecommunications making breakthroughs in various types of specialty gases.

Photoresist: is a core material in the photolithography process.

Main manufacturers in the domestic photoresist market include Nanjing University of Posts and Telecommunications, Tongcheng New Materials (Beijing Kehua), Huamao Technology (Xuzhou Bokan), Jingrui Electric Materials (Suzhou Ruihong), Shanghai Xinyang, Rongda Photonics, Dinglong Co., Ltd., Guangxin Materials, Feikai Materials, and Yake Technology.

There are many companies involved in various stages of the industrial chain, including Chip Source Micro (coating and developing), Qicai Chemical (photoresist intermediates), Foster (photosensitive dry film), Maolai Optical (optical systems), Jushi Chemical, Baihehua, Shengjian Environment, Tongyi Co., Ltd., and Songjing Co., Ltd..

Wet Electronic Chemicals: also known as ultra-pure reagents or process chemicals, refer to chemical reagents with a main component purity greater than 99.99%, with impurity ions and particle counts meeting strict requirements.

Domestic manufacturers:

Jianghua Micro’s wet electronic chemicals have been successfully introduced to multiple 12-inch semiconductor wafer factories;

Jingrui Electric Materials’ hydrogen peroxide and sulfuric acid meet SEMI G5 standards (metal impurities < 0.1 ppb) and have been supplied to some domestic wafer manufacturers.

Main manufacturers also include Shanghai Xinyang, Xingfu Electronics, Glinda, Juhua Co., Ltd., Guanghua Technology, Xinzoubang, Xingfa Group, Duofuduo, Anji Technology, Yake Technology, Feikai Materials, Zhujuxin, Huarong Chemical, Duofuduo, Guanghua Technology, and Tiancheng Technology.

Advanced Packaging Materials: Advanced packaging enhances information transmission speed, reduces unit packaging costs, and minimizes packaging area, with epoxy molding compounds occupying over 95% of the electronic packaging market share.

The global market is mainly dominated by foreign manufacturers such as Shin-Etsu Chemical, Sumitomo Bakelite, and Henkel (formerly Hitachi Chemical).

Domestic manufacturers’ market share is mainly held by Huahai Chengke, Hengsu Huawai, Changchun Molding Materials, Beijing Kehua, and Changxing Electronics.

3. EDA Software & IP Cores

EDA software, short for Electronic Design Automation software, is a software tool that uses computer-aided design technology to complete the design process of ultra-large-scale integrated circuit chips.

Among global EDA tools, Synopsys, Cadence, and Siemens EDA account for nearly 80% of the market share.

Domestic EDA manufacturer Huada Jiutian ranks fourth globally, with Gailun Electronics and Guangli Micro also being two major domestic participants.

Huada Jiutian has achieved full-process capabilities in analog/panel/storage/RF design, with AI empowerment added to the design platform, RF design accelerated based on GPU computing power, and new OPC functions for high-end applications;

Guangli Micro has formed a soft and hard collaborative product matrix around semiconductor electrical testing;

Gailun Electronics has formed a general analog design platform.

IP cores play an important role in chip design.

Semiconductor IP, short for semiconductor intellectual property cores, refers to functional modules that are pre-designed, verified, and reusable in IC chip design.

The IP industry shows a clear oligopoly pattern, with urgent demand for domestic alternatives.

Xinyuan Co., Ltd. is currently the only Chinese mainland IP company in the top ten and is the number one semiconductor IP supplier in China;

Canxin Co., Ltd. is also accelerating the layout of self-developed high-speed interface IP and high-performance analog IP;

Huada Jiutian, Xinlai Technology, and Huaxia Core also have corresponding layouts in semiconductor IP.

4. Chip Design

Also known as integrated circuit design, it is the process of integrating electronic components, circuits, and functions into a single chip.

The market is mainly dominated by a few manufacturers including Broadcom, Qualcomm, MediaTek, Intel, NVIDIA, Samsung, Marvell, and Chipone.

Domestic core participants in the chip design field include HW, Unisoc, Cambricon, Weir Shares, Goodix Technology, GigaDevice, and Lanqi Technology.

5. Packaging & Advanced Packaging

Packaging is located in the mid-to-late end of the semiconductor industry chain. In the global OSAT ranking, ASE and Amkor rank first and second, respectively.

Domestic independent packaging and testing first-tier representative companies include Changdian Technology, Tongfu Microelectronics, and Huatian Technology, which occupy the third, fourth, and sixth positions in the global top ten OSAT (packaging and testing companies) ranking in 2024. Additionally, many companies such as Shenghe Jingwei, Jingfang Technology, Yongxi Electronics, Qizhong Technology, and Huicheng Shares are also actively laying out.

Advanced Packaging: Chip packaging is a key step in chip manufacturing.

Electroplating Liquids: Major domestic manufacturers include Qiangli New Materials, Aisen Shares, Tiancheng Technology, and Shanghai Xinyang.

Temporary Bonding Adhesives: Domestic manufacturer Feikai Materials has broken the 3M monopoly, and Dinglong Co., Ltd. has overcome key technologies such as high-temperature resistance and low volatility in temporary bonding adhesives.

PSPI Photoresist: Qiangli New Materials, Bomi Technology, Aisen Shares, and Feikai Materials have made layouts in this field.

Epoxy Molding Compounds: are the most widely used encapsulation materials, providing core functions such as protection, thermal conductivity, and support for chips. Huahai Chengke is involved in epoxy molding compounds and underfill adhesives, Lianrui New Materials has broken the monopoly on electronic-grade spherical silicon micropowder technology, and Yishitong has made layouts in the Low-α spherical silicon and spherical aluminum fields.

Advanced Packaging Equipment:Domestic manufacturers in this field include Huahai Qingke (CMP equipment), Shengmei Shanghai (electroplating), Chip Source Micro (coating and developing, temporary bonding and debonding), Zhongsilicon (TSV deep silicon etching), Tuojing Technology (hybrid bonding equipment), Shanghai Microelectronics (optical K equipment), and Chip Micro Packaging (direct-write lithography equipment) as major players in the equipment field.

Post-processing layout manufacturers include Wenyi Technology, Naike Equipment, Xinyi Chang (die bonding machines), Guangli Technology (thinning machines), Delong Laser (SIP packaging), Aotwei (semi-automatic dicing machines), Changchuan Technology, Huafeng Measurement and Control, and San Chao New Materials.