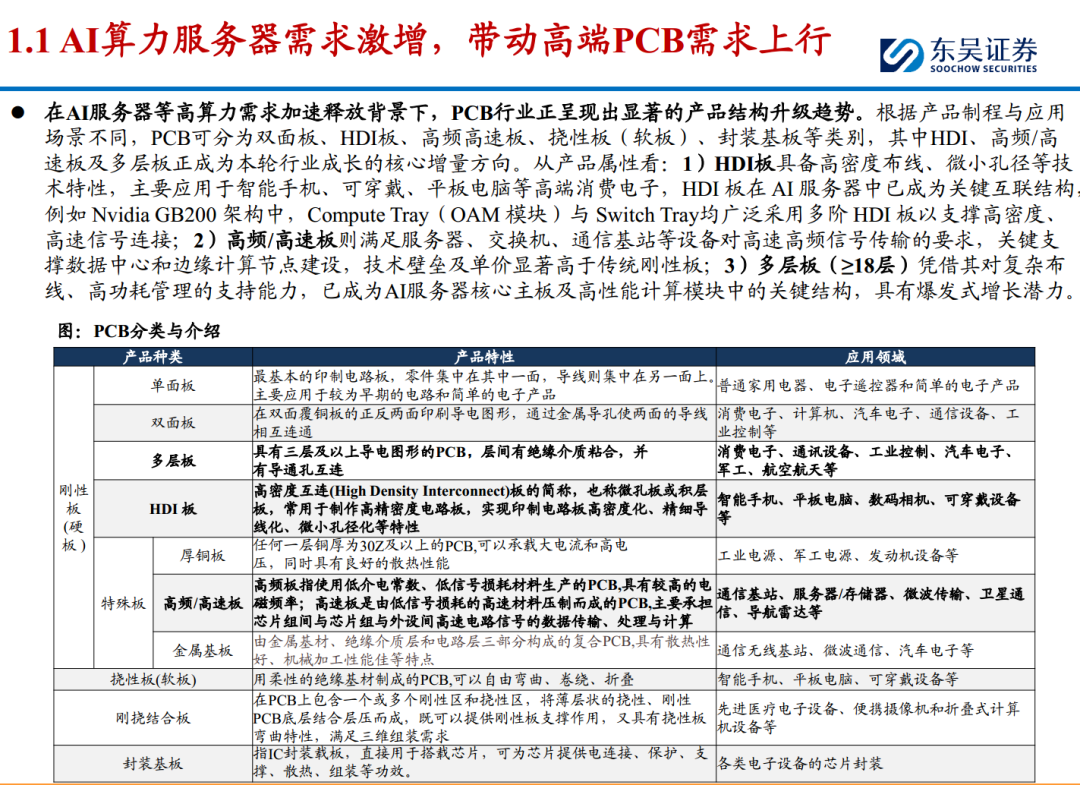

1. The surge in AI computing power demand drives the need for high-end PCBs, with domestic mainstream manufacturers actively expanding production.

1) Computing power demand: Against the backdrop of sustained high computing power demand from AIGC and others, the global server market is entering a new growth cycle starting in 2024. IDC predicts that from 2024 to 2029, the global server market will have an average annual compound growth rate (CAGR) of 18.8%, with accelerated server spending growing at over 20% annually, significantly higher than traditional non-accelerated products.

2) PCB demand: The PCB industry has experienced a phase adjustment from 2022 to 2023 due to weak downstream consumer electronics and inventory cycles. With emerging demands driven by AI servers and high-performance infrastructure, the industry is gradually recovering from 2024, showing a significant trend of product structure upgrades. 3) PCB manufacturers: As terminal demand transmits, domestic mainstream PCB manufacturers are actively expanding production, with capital expenditures accelerating upward, focusing on high-end directions such as HDI and multilayer boards.

From the perspective of downstream application structure, servers/storage are currently the most elastic segments for growth in the PCB industry. During the period from 2020 to 2024, their market size CAGR is as high as 16.7%, far exceeding traditional applications such as automotive electronics (9.2%), mobile phones (-0.5%), and computers (-3.4%); from 2024 to 2029, it is expected to maintain a steady growth rate of 10.0%. With the accelerated construction of new infrastructures such as AI servers, intelligent computing centers, and data centers, the demand for server/storage PCBs is expected to remain strong.

In terms of corresponding PCB product structure, multilayer boards with more than 18 layers and HDI boards have become the core beneficiary categories. According to Prismark’s forecast, by 2025, the output value growth rate of multilayer boards with more than 18 layers will reach 41.7%, while HDI boards will be 10.4%; from 2024 to 2029, they are expected to maintain high growth rates of 15.7% and 6.4%, respectively. High-end HDI and ultra-high-layer rigid boards, due to their superior signal integrity, heat dissipation capabilities, and packaging density, have become indispensable PCB structures in modules such as AI server motherboards, AI accelerator cards (GPU cards), and switch cards.

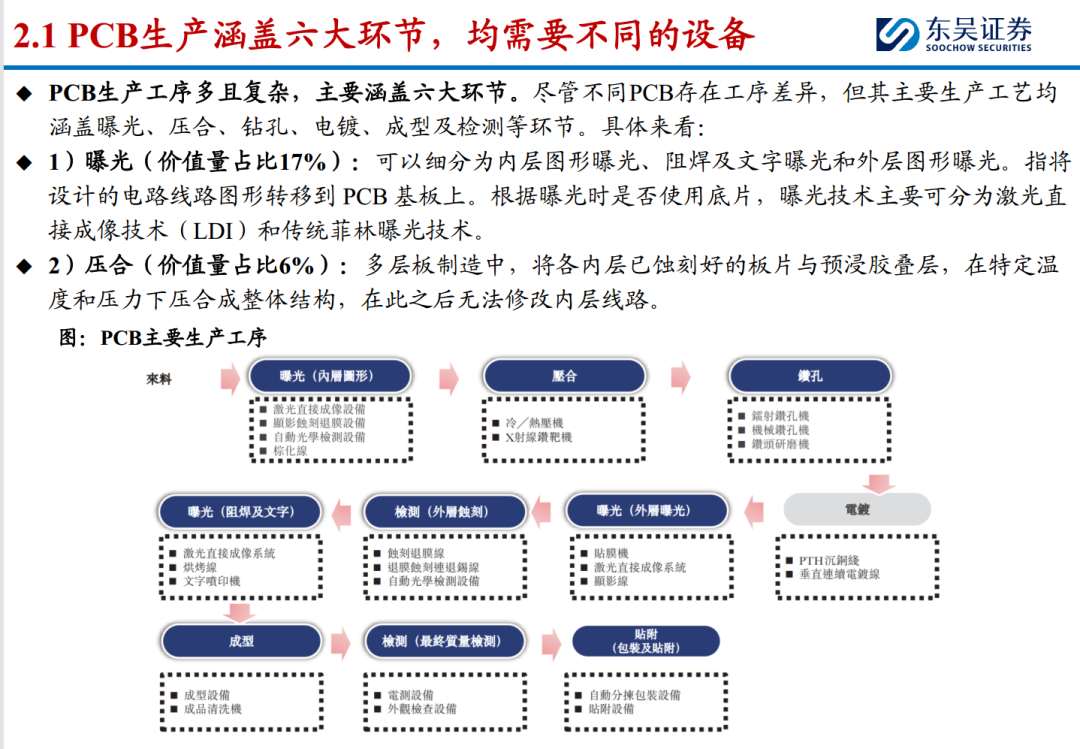

2. The variety of equipment required for PCB production is complex, with drilling/exposure/testing having the highest value.

1) PCB equipment: The PCB production process is complex and includes exposure, lamination, drilling, electroplating, forming, and testing. In 2024, the global PCB equipment market size is expected to reach 51 billion yuan, a year-on-year increase of 9.0%, with a CAGR of 4.9% from 2020 to 2024. The current wave of AI computing construction has increased the demand for PCB equipment, with the market expected to reach 77.5 billion yuan by 2029, and a CAGR of 8.7% from 2024 to 2029, significantly higher than previous levels. Specifically, drilling/exposure/testing equipment accounts for the highest value, with 20.75%, 16.99%, and 15.00% respectively in 2024.

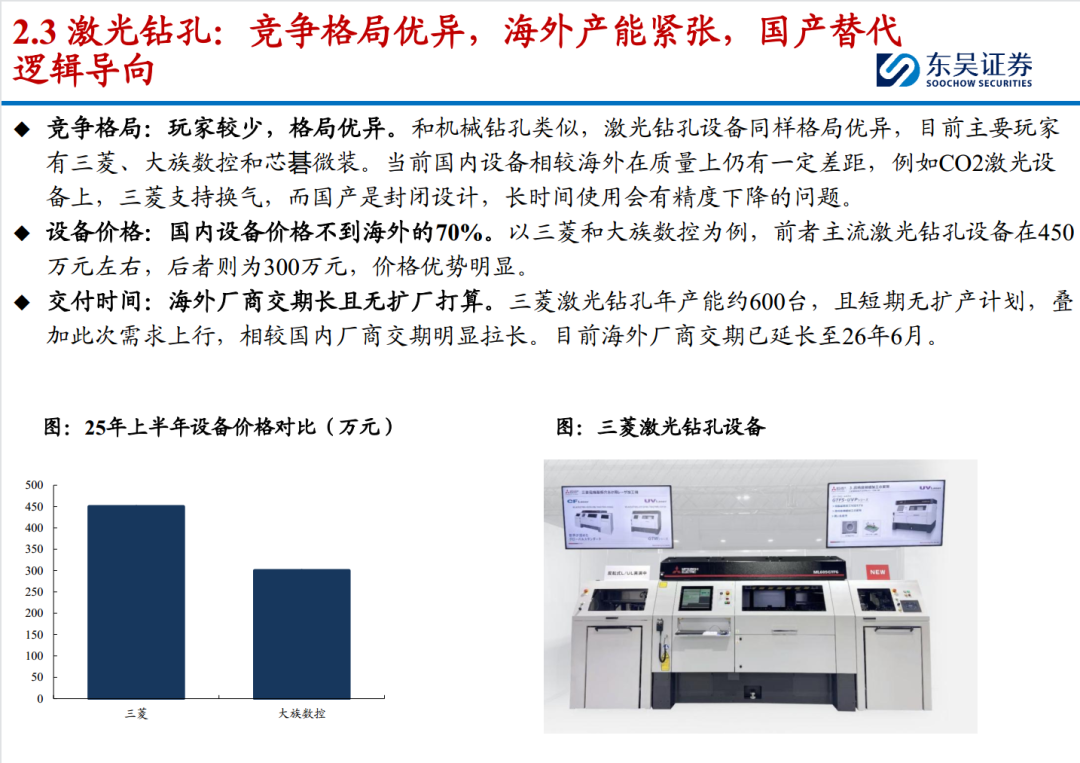

2) Drilling equipment: This can be divided into mechanical drilling and laser drilling. The current surge in computing power demand has catalyzed the need for high-end HDI, which in turn drives demand for drilling equipment, benefiting both mechanical and laser drilling. Additionally, due to the significant increase in the number of buried holes/blind holes/micro-holes in high-end HDI, the demand for laser drilling equipment is expected to double. There are few players in the industry, and the competitive landscape is favorable, with domestic manufacturers having a clear price advantage, ample production capacity, and short delivery times, which is expected to accelerate the process of domestic substitution.

3) Drill bits: The current AI computing power demands higher requirements for drill bits, mainly reflected in the increased aspect ratio of drill bits. However, compared to the challenges in technology, current production capacity is the main bottleneck. Domestic players dominate the industry and are still accelerating production expansion, with expectations of further increasing market share in the future.

4) Exposure equipment: This is divided into traditional film exposure and LDI, with the latter being more suitable for HDI exposure needs. In terms of market structure, it is currently dominated by foreign brands, with a low domestic production rate.

5) Electroplating equipment: High-end HDI has led to a significant increase in the number of electroplating cycles, coupled with pressure on yield rates, driving an increase in demand for electroplating equipment.

3. Mainstream equipment manufacturers show a clear upward trend, expecting accelerated performance release in the future.

1) DAHUA CNC: A global leader in PCB equipment, covering almost all processes.

2) XINQI Microelectronics: A global leader in laser direct writing lithography, covering the high-end PCB market.

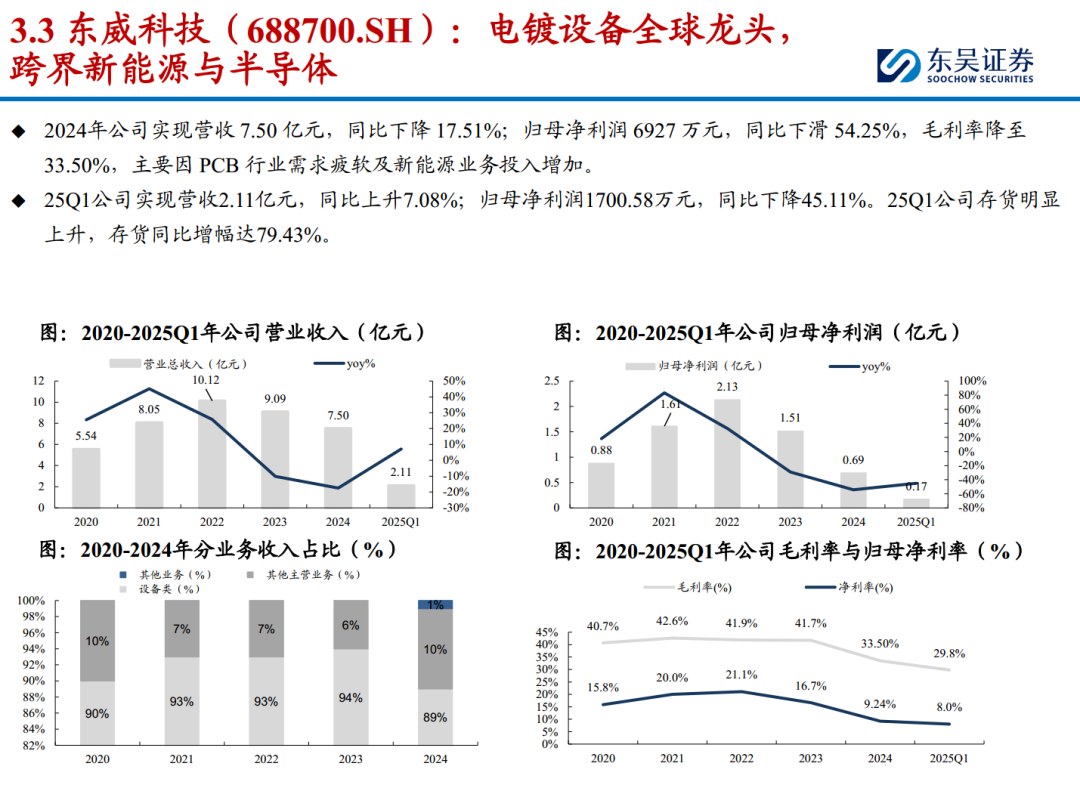

3) DONGWEI Technology: A global leader in electroplating equipment, crossing into new energy and semiconductors.

4) DINGTAI High-Tech: A global leader in PCB tooling, with strong development in drill bit business.

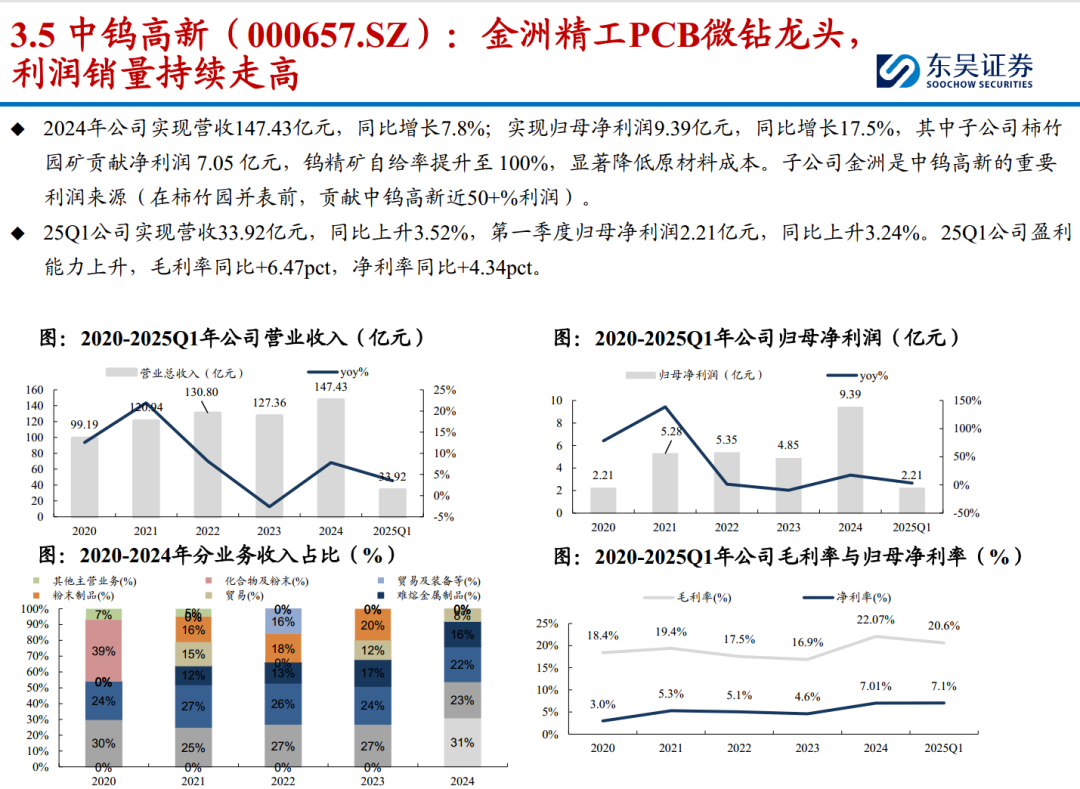

5) ZHONGTUNG High-Tech: A leading manufacturer of PCB micro-drills, with profits and sales continuing to rise.

6) KAIKE Precision Machinery: A core supplier for high-end electronic manufacturing, deeply bound to leading customers.

4. Investment Recommendations

In the drilling segment, it is recommended to focus on equipment side [DAHUA CNC] and consumables side [DINGTAI High-Tech], [ZHONGTUNG High-Tech]; for exposure, focus on [XINQI Microelectronics], [TIANZUN Technology]; for electroplating, focus on [DONGWEI Technology]; for solder paste printing, focus on [KAIKE Precision Machinery].

This is an excerpt from the report; the original report is:

《Mechanical Equipment – In-Depth Report on PCB Equipment: Benefiting from High Downstream Prosperity + Supply-Demand Gap + Import Substitution, Equipment Manufacturers are the Gold Diggers – Dongwu Securities [Zhou Ershuang, Qian Yaotian, Tao Zetian] – 20250822【40 pages】》

Please click the “Read Original” link below to jump to the [Value Directory] computer site for download and reading.