The content is sourced from the internet. If there are any issues with publication, please contact us for removal. The article is for research reference only and does not constitute any investment advice. Investment carries risks; please proceed with caution.

Weekend Update – New Materials in PCB Upstream: 1) Tongguan’s performance exceeds expectations, 2) Rubin’s progress is smooth, 3) Shengyi announces PCB expansion.

1) Tongguan Copper Foil Exceeds Expectations: In the second quarter, the market expected profits of over 10 million, but the actual profit approached 40 million, proving that the upstream of CCL, especially Taiguang Chain, has truly begun to release performance in the first quarter.

2) Rubin’s Progress is Smooth, Q布 + 4th Generation Copper Directly Related:

① Rubin completed its first tape-out in June 2025, with the first batch of wafers expected to be delivered by TSMC in October. Engineering samples are planned for release in Q4 2025, with chip and system design expected to be finalized by March 2026, and mass production in Q3 2026, with server racks starting to ramp up, currently showing no signs of delay.

② Taiguang will conduct a factory audit in July, with a framework agreement for Q布 gradually being established in August. It is expected that in H2 2026, the shipment volume of Q布 from Zhongcai Technology will reach 1-1.2 million meters per month, and Feilihua will reach 800,000 meters per month.

③ Tongguan’s mid-term report mentioned that “HVLP4 is undergoing full performance testing with downstream end customers,” with orders expected as early as Q4.

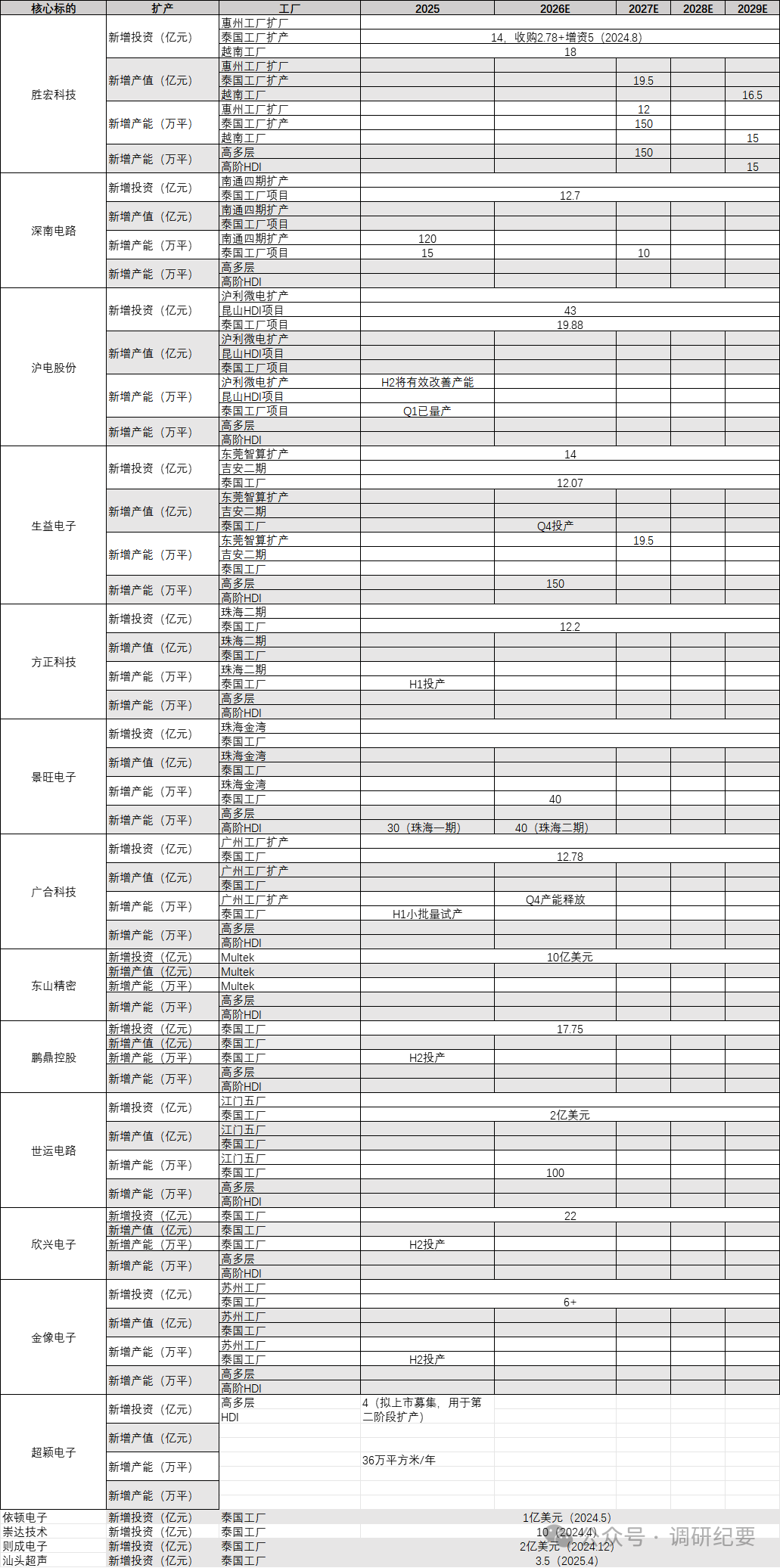

3) Shengyi’s PCB Expansion is Beneficial for Domestic Materials and Equipment: On Friday, Shengyi Electronics announced an investment of 1.9 billion yuan from its own funds to establish an annual production capacity of 700,000 square meters of PCBs, mainly focusing on new demands for high-layer AI servers.

① Since July-August, both Dongshan and Shengyi have announced PCB expansion plans, accelerating downstream CAPEX and driving equipment demand.

② Shengyi Technology’s CCL has gained a certain market share in the NV-switch tray (M8), and the supply chain for electronic cloth/copper foil is expected to tilt towards domestic enterprises.

CCL Industry Chain Price Increase:

On Friday, Meizhou Weilibang Electronics, Guangdong Jiantao Laminates, and Ruixing Technology respectively issued price increase notices,marking the start of a cycle of rising volume and price.

1) High-end Copper Foil for AI: AI-driven penetration is accelerating, and domestic substitution is timely.

– AI drives the continuous increase in HVLP copper foil penetration;

– The global HVLP copper foil market is expected to achieve steady growth;

– Japanese and Korean companies have long dominated the market, and domestic substitution is accelerating.

2) Low Dielectric Electronic Cloth: Core substrate for high-frequency signals, domestic expansion welcomes market dividends.

– Low dielectric electronic cloth is a key high-performance material in the high-frequency electronics field;

– Domestic demand for low dielectric electronic cloth is rapidly increasing;

– Domestic manufacturers are accelerating expansion, and market share is expected to continue to rise.

3) Rise of High-Performance Resins: Hydrocarbon resins have the largest expected difference.

– Resin materials play multiple key roles as core adhesives for copper-clad laminates;

– The growing demand for high-performance resins is driving continuous industry expansion.

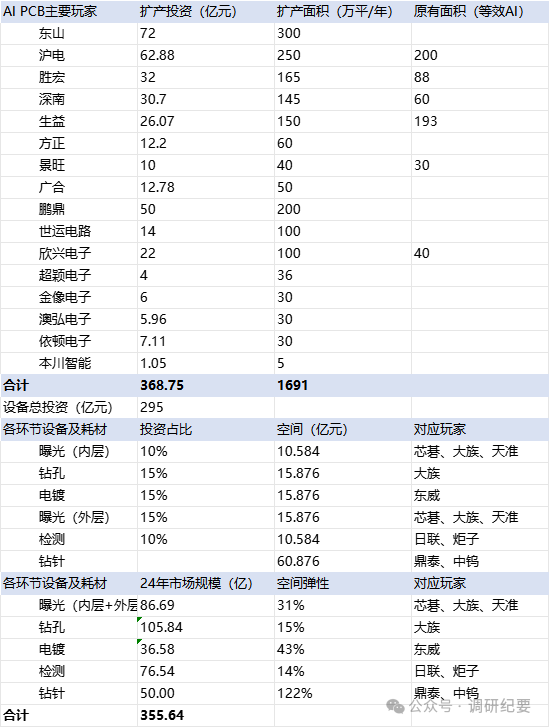

AIPCB Equipment: Flexibility Comes from Value Quantity Rather than Quantity

Since we recommended PCB equipment in July, many investors have been concerned about the incremental flexibility of PCB equipment brought by AI. We believe that the core of this round of AIPCB lies in value quantity rather than quantity. Essentially, it is the increase in equipment value brought about by process innovation and iteration, along with the logic of equipment inflation. We summarize as follows:

1. The value increment brought by the generational upgrade of PCB equipment is several times. Taking drilling equipment as an example, from traditional mechanical drills to CCD drills to CO2 laser drills to UV laser drills, the value changes from 700,000-1,000,000 to 1,000,000-2,000,000 to 2,000,000-3,000,000 to 4,000,000, with each generation bringing a doubling of value growth.

2. The increase in domestic production rate and market share breakthroughs open up flexibility space. Previously, domestic manufacturers mainly provided low-end mechanical drilling machines and CCD drills, while the AIPCB laser drilling machine market was basically monopolized by Mitsubishi. With Mitsubishi’s orders being fully booked, leading to supply shortages and extended schedules, domestic manufacturers are expected to break through in laser drilling machines for core customers. The increase in market share and the doubling of value quantity bring several times of growth in flexibility space.

3. Focus on breakthroughs and changes at the customer level. According to our understanding, recently, Shenghong has been in close contact with several leading domestic suppliers, and we understand that some have already formed intention orders. Subsequent breakthroughs and implementations at the customer level for high-end equipment may be catalyzing a new round of growth.

4. How to view the market value height of this round of PCB equipment? Domestic manufacturers still have significant potential marginal changes. Currently, PCB equipment manufacturers correspond to a PE of about 20-25x for next year. We believe that this valuation level only reflects the recent high growth in orders and shipments. The subsequent investment logic for the sector revolves around: 1) the gradual clarification and upward revision of total spending next year. 2) Order structure: progress in order volume for high-end equipment such as laser drilling machines; 3) Customer structure: expansion of market share among core customers such as Shenghong. There is still considerable room for valuation improvement.

5. Investment opportunities from PCB to PCBA equipment. The demand for AI computing power drives the technological upgrade of PCBs. As the later stage of the PCB process, the prosperity and importance of PCBA equipment are continuously increasing. Its essence remains the increase in equipment value brought about by process innovation and iteration, along with the logic of equipment inflation. Recently, Shengyi Electronics has expanded production, and Kaige Precision Machinery has issued equity incentives. We continue to strengthen investment opportunities in PCBA equipment. PCBA is the “assembled circuit board” or “circuit assembly board,” which is a finished product that installs and solders various electronic components onto the PCB through surface mount technology (SMT), plug-in technology, etc., and belongs to the later stage of PCB processing. The core processes of PCBA include solder paste printing, chip placement, reflow soldering, and the associated inspection processes, focusing on key companies such as Kaige Precision Machinery, Jintuo Co., and Sitake.

(The table from July has not yet been updated for this expansion)

Comprehensive Overview of the PCB Equipment Industry

Comprehensive Overview of the PCB Equipment Industry

1. Demand Side: Two Layers of Logic Overlap

1) Technological Upgrade: Boards are becoming more refined. Ordinary high-layer → HDI → substrate-like → narrow boards, with hole diameters shrinking from 50 μm to 20 μm and then to a few microns, while line width and spacing are also being tightened.

2) Accelerated Expansion: Leading manufacturers such as Shenghong, Shennan, Shengyi, and Jingwang are all expanding production, focusing on high-end HDI/substrate-like boards, which have a value that is 20-50% higher than ordinary boards.

Result: Equipment demand has both “quantity” and “price,” a double boost.

2. Core Equipment Links

(Sorted by value from high to low)

1) Drilling

– Mechanical Drilling: Dazhu CNC leads, achieving precision of 30-40 μm, with rapid improvement in domestic production rate.

– Laser Drilling: Japanese company Mitsubishi still dominates the high-end market, but the window for domestic substitution has opened—new machine precision requirements have leveled the playing field.

2) Electroplating

– Vertical Continuous Electroplating (VCP): Dongwei Technology is the leader, with the highest market share.

– New Demand: Pulse electroplating, three-in-one equipment, MSAP level, with unit prices and gross margins 10-20% higher than traditional models.

3) Exposure

– Inner Layer + Outer Layer: Xinqi Microelectronics and Tianzhun Technology are both involved. As line widths become finer, the demand for LDI (Laser Direct Imaging) increases, raising the value of each machine.

4) Inspection / Lamination / Reflow Soldering

– Reflow Soldering: As boards become larger and layers increase, high-temperature reflow at 288 °C + low-CTE materials are needed to prevent warping. Jinlu Electronics has already laid out low-stress soldering solutions.

– Inspection Equipment: AOI and AVI increase linearly with the number of layers.

– Lamination: After more than 20 layers, the number of laminations increases, and equipment demand amplifies accordingly.

3. Value Quantity and Delivery Time

– High-end equipment of the same type is generally 20-50% more expensive than traditional models, with some high-end models being 80% more expensive.

– Equipment delivery time: 6-9 months from order to shipment, faster than previous semiconductor equipment, but this round of expansion is expected to last at least 2 years, possibly extending to 3 years.

4. Pace of Domestic Production

– Drilling: Dazhu CNC has entered Shenghong and Shennan’s supply chains, rapidly increasing market share.

– Electroplating: Dongwei Technology is the absolute leader in the domestic market, continuously iterating pulse and three-in-one models.

– Exposure: Xinqi Microelectronics and Tianzhun Technology are first to capture the incremental market.

– Others: There is still significant substitution space in soldering, lamination, and inspection links.

5. Consumables Benefit Simultaneously

– Drill bits, electroplating solutions, dry films, solder, etc., will expand in volume alongside capacity expansion, with higher gross margins for high-end formulations.

– Representative companies: Shanghai Xinyang (electroplating solutions), Jinlu Electronics (solder), Tiancheng Technology (PCB specialty chemicals), etc.

—END— If any students are interested and would like to see more materials, such as investment records, popular companies, and industry summaries, as well as stock recommendations, you can join the Knowledge Planet.The current free features of the planet are not open yet. Scan the code to receive a coupon. After joining, you can contact the assistant for a refund (the platform will charge a 20% handling fee).

If any students are interested and would like to see more materials, such as investment records, popular companies, and industry summaries, as well as stock recommendations, you can join the Knowledge Planet.The current free features of the planet are not open yet. Scan the code to receive a coupon. After joining, you can contact the assistant for a refund (the platform will charge a 20% handling fee).