A Customs Declaration That Triggered Global Shockwaves

On the morning of April 13, 2025, at 10 AM, merchants in the Huaqiangbei electronics market in Shenzhen discovered that the spot price of Texas Instruments’ TPS61093 power management chip had surged by 23% compared to the previous week. At the same time, the stock price of Sanan Optoelectronics hit the daily limit within 15 minutes of opening—this chain reaction was ignited by the announcement made three days earlier by the China Semiconductor Industry Association regarding the ‘Origin Certification Rules for Semiconductor Products.’

This seemingly technical rule adjustment is, in fact, China’s ‘asymmetric counterattack’ in the global semiconductor war. While the United States is obsessed with using the Entity List to block technology, China is reconstructing the industrial chain ecosystem with market rules. This article will delve into the three strategic logics of this game and the trillion-level investment opportunities behind it.

1. Policy Deconstruction: Why is ‘Wafer Origin’ a Fatal Blow?

1. Striking at the ‘Achilles’ Heel’ of American Manufacturing

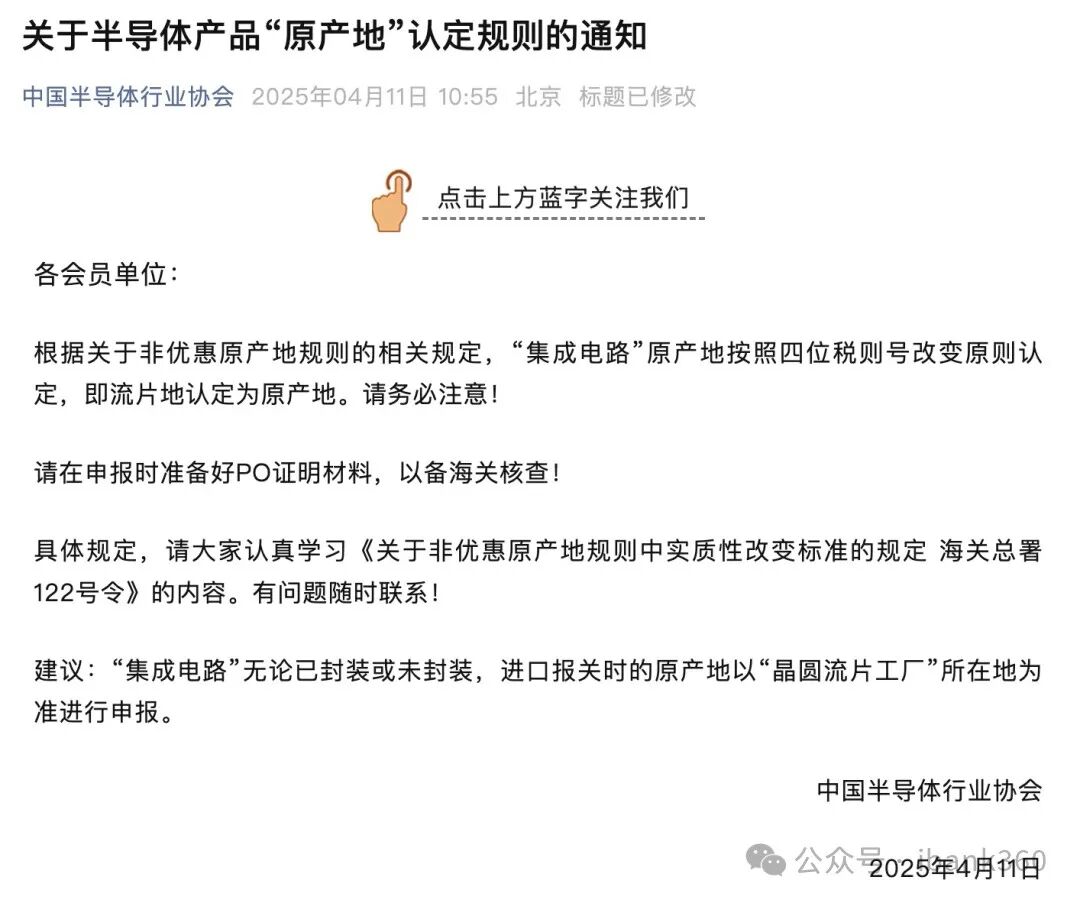

Cost Leverage: The new regulation requires the origin of chips to be determined by the wafer origin, meaning that chips manufactured in the U.S. (such as those from TI’s Texas factory) will incur additional tariffs upon import. For example, the comprehensive tax rate for TI’s general-purpose analog chips may rise from 6% to 21% (according to data from the General Administration of Customs), directly eroding 15%-20% of American companies’ profit margins.

Capacity Dilemma: The average production cycle for new wafer fabs in the U.S. is 4.3 years (SEMI 2024 Annual Report), while China’s mature process (28nm and above) capacity already accounts for 32% of the global total (according to data from IC Insights), creating a ‘time difference’ advantage.

2. Precisely Cutting the Industrial Chain with ‘Four Two Pulling a Thousand Pounds’

Exempting High-End Chips: AI chips like Nvidia’s H20 and AMD’s MI350 are primarily produced at TSMC and are not affected by the new regulations, ensuring China’s computing power needs while avoiding provoking a full-scale countermeasure from the U.S.

Targeting Low-End Capacity: Analog chips, RF components, and other mature process products are the main targets, as these chips account for 68% of China’s total imports (according to the General Administration of Customs 2024 Annual Report), but the domestic substitution rate is less than 20%, leaving significant room for replacement.

Strategic Implications: During the critical period of the U.S. CHIPS Act subsidizing domestic manufacturing, China is accelerating the ‘de-Americanization’ of global capacity with tariff leverage, as TSMC founder Morris Chang stated: ‘This could turn the Arizona wafer fab into a political specimen.’

2. Industrial Changes: The ‘Three-Stage Rocket’ of Domestic Substitution

1. First Stage: Analog Chips’ ‘Rural Encircling the City’

Price War Terminator: TI’s annual revenue in China exceeds $12 billion, and its gross margin for general-purpose power chips may plummet from 68% to below 50% (according to estimates from CITIC Securities), providing domestic manufacturers with a breathing window.

Technological Singularity Explosion: Chipone’s GaN fast-charging chips have entered the Huawei Mate 70 supply chain, and Naxin Micro’s automotive-grade isolation chips have passed ASIL-D certification, marking the dawn of high-end substitution for domestic analog chips.

2. Second Stage: RF and Specialty Processes’ Shortcut

5G Base Station Competition: Weijie Chuangxin’s 5G PA module has captured over 40% of the Huawei base station market and is challenging Skyworks’ filter market.

IDM Model Rising: Silan Micro’s 12-inch IGBT production line has achieved a yield of 94%, and Huahong’s 90nm BCD process has secured a 12 billion yuan order from BYD, with specialty processes becoming the key to breakthroughs.

3. Third Stage: The Dimensionality Reduction Strike of Third-Generation Semiconductors

Silicon Carbide Revolution: Tianyue Advanced’s 8-inch substrate has reached a global market share of 21%, forcing Wolfspeed to announce a 30% layoff at its Texas factory.

GaN Ecosystem Closed Loop: Innoscience’s GaN chips are deeply integrated with Xiaomi’s 120W fast charging, with a year-on-year shipment increase of 300% in 2024.

3. Global Supply Chain Restructuring: Who is Profiting in the Underflow?

1. Southeast Asia as a ‘Tax Haven’

UMC’s Singapore plant’s capacity scheduling has reached Q3 2026, and GlobalFoundries’ Malaysia plant has received orders transferred from American companies, with local semiconductor investments surging by 47% (McKinsey 2025 Report).

2. Accelerated Localization of Equipment and Materials

SMIC’s 5nm etching machine has entered Yangtze Memory’s mass production line, with a year-on-year revenue increase of 82% in 2024.

Shanghai Silicon Industry’s 12-inch silicon wafer yield has surpassed 90%, competing for orders from TSMC’s Nanjing plant.

3. Taiwanese and Korean Foundries’ ‘Dual Benefits’

As TSMC’s U.S. factory faces production delays, its Nanjing plant has received a large order for 28nm CIS chips transferred from SMIC, while Samsung’s Xi’an plant has secured 70% of Qualcomm’s 5G RF chip foundry orders.

4. Investment Insights: Capturing Explosive Points in Certainty

1. Short-Cycle Opportunities

Analog Chip Substitution: Focus on companies with gross margin increases exceeding 5% (such as Sanan Optoelectronics and Aiwai Electronics).

RF Front-End Breakthrough: With the acceleration of 5G base station construction, Weijie Chuangxin and Zhaoshengwei may replicate the 10-fold stock miracle of Zhaoshengwei in 2019.

2. Long-Cycle Layout

Automotive-Grade Chips: By 2025, the market size of China’s new energy vehicle chip market is expected to reach 180 billion yuan (according to the China Association of Automobile Manufacturers), with Silan Micro and Huahong Semiconductor as core targets.

Storage-Compute Integrated AI Chips: Avoiding advanced process restrictions, Cambrian’s Siyuan 590 achieves 85% of Nvidia’s H20 performance and has secured an order of 500,000 pieces from ByteDance.

3. Risk Warnings

U.S. Technological Countermeasures: May restrict exports of equipment below 14nm to China, requiring North Huachuang and Tuojing Technology to accelerate validation.

Concerns of Overcapacity: There are currently 142 wafer fabs under construction globally (according to SEMI data), which may trigger a price war by 2026.

Conclusion: The ‘Chinese Equation’ of the Semiconductor War

While the Biden administration is still debating whether to expand sanctions against SMIC, China has already leveraged a customs rule to disrupt the global semiconductor order. From tariff leverage to capacity substitution, from equipment breakthroughs to ecosystem feedback, this combination is rewriting the rules of industrial competition. As ASML CEO Peter Wennink warned: ‘By 2030, the world may witness two independent semiconductor supply chain systems.’ And China is becoming the core variable of the new system.#ChipWar #DomesticSubstitution #TechnologicalSelf-Reliance

What do you think will be the next breakthrough area for domestic chips?

Three readers will be randomly selected from the comments section to receive an electronic version of the ‘2025 Semiconductor Investment Map.’