Use Hanghangcha for Industry Data

🕒 Welcome to explore the website: www.hanghangcha.com

Printed Circuit Boards (PCBs) are known as the “mother of electronic products” and serve as a bridge that connects electronic components and circuits. They are printed boards that form connections between points according to a predetermined design on a common substrate. Their main function is to connect various electronic components to form a predetermined circuit for transmission.Currently, the PCB industry is in its fifth growth cycle, primarily driven by 5G technology, cloud computing, and the Internet of Things, which support the growth of 5G base stations, communication devices, and new energy vehicles.According to Prismark’s forecast, the global PCB industry output value is expected to reach $101.6 billion by 2026, with a CAGR of 4.8% from 2021 to 2026, maintaining stable growth on a high base.

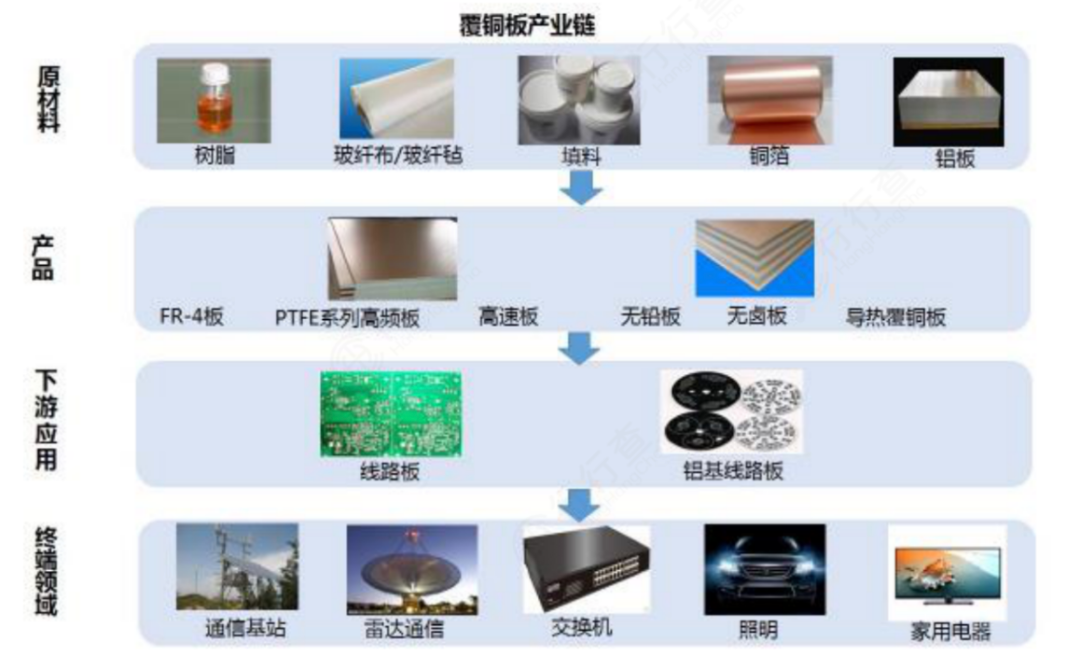

PCB Industry Chain

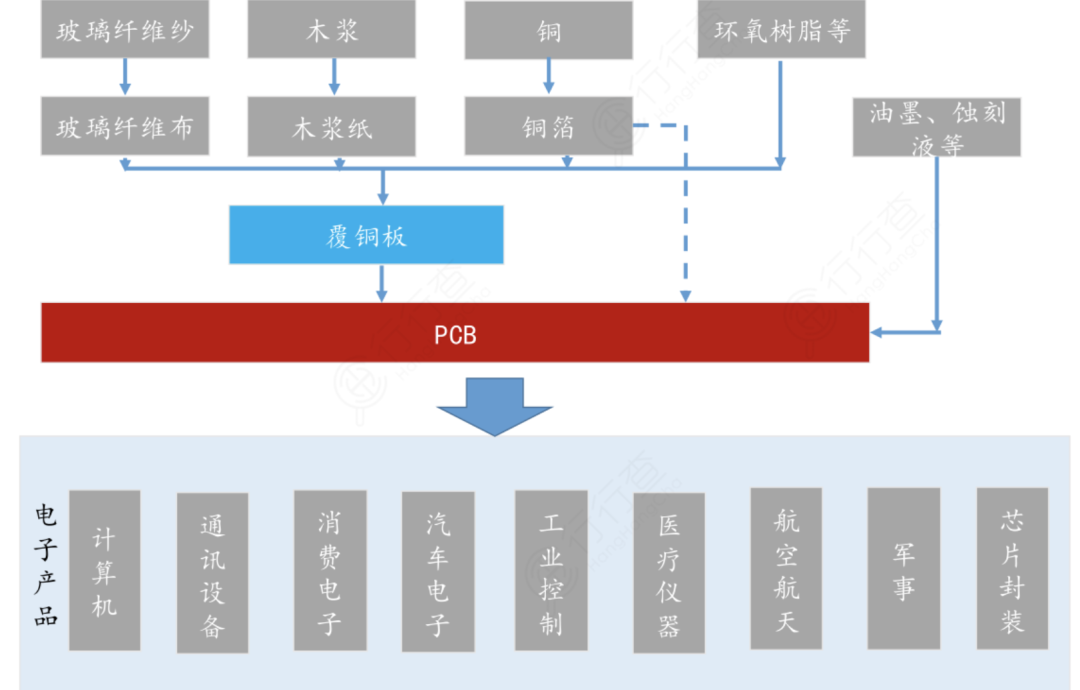

The upstream raw materials of the PCB industry chain primarily include copper-clad laminates and bonding sheets. The three main upstream materials for copper-clad laminates include copper foil, fiberglass cloth, and epoxy resin materials.The downstream communication and computer sectors remain the two main application areas, but in recent years, the trend of automotive electronics has become very clear (the electronic systems of new cars account for an average of over 40% of the total vehicle cost), leading to a significant increase in demand for automotive PCBs.

Upstream Materials of PCB Industry Chain

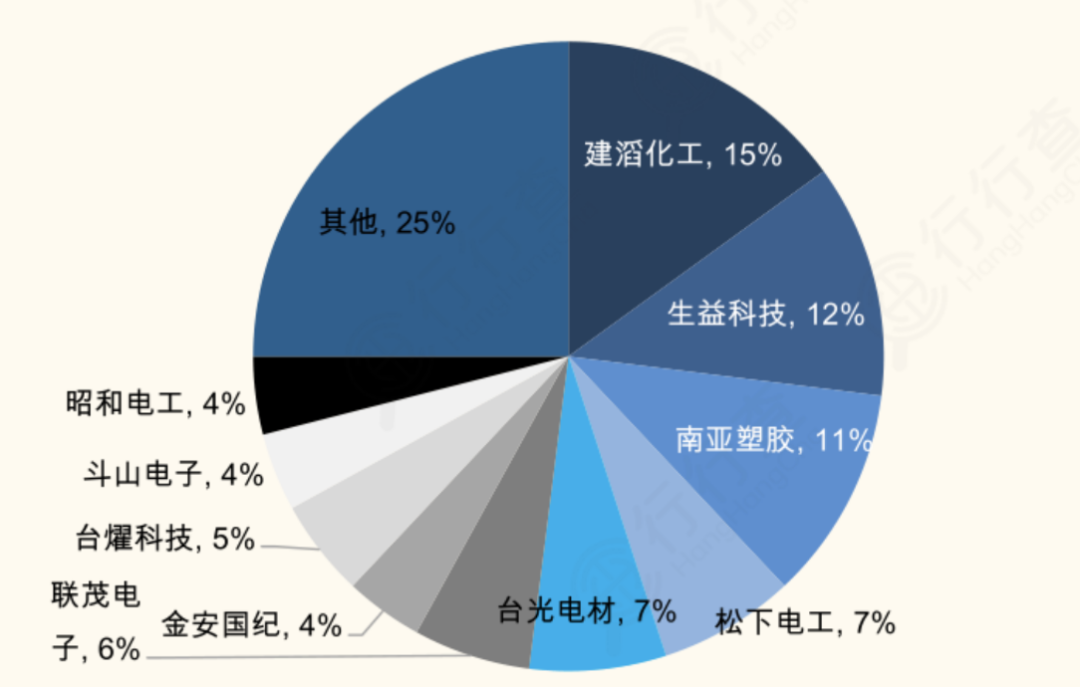

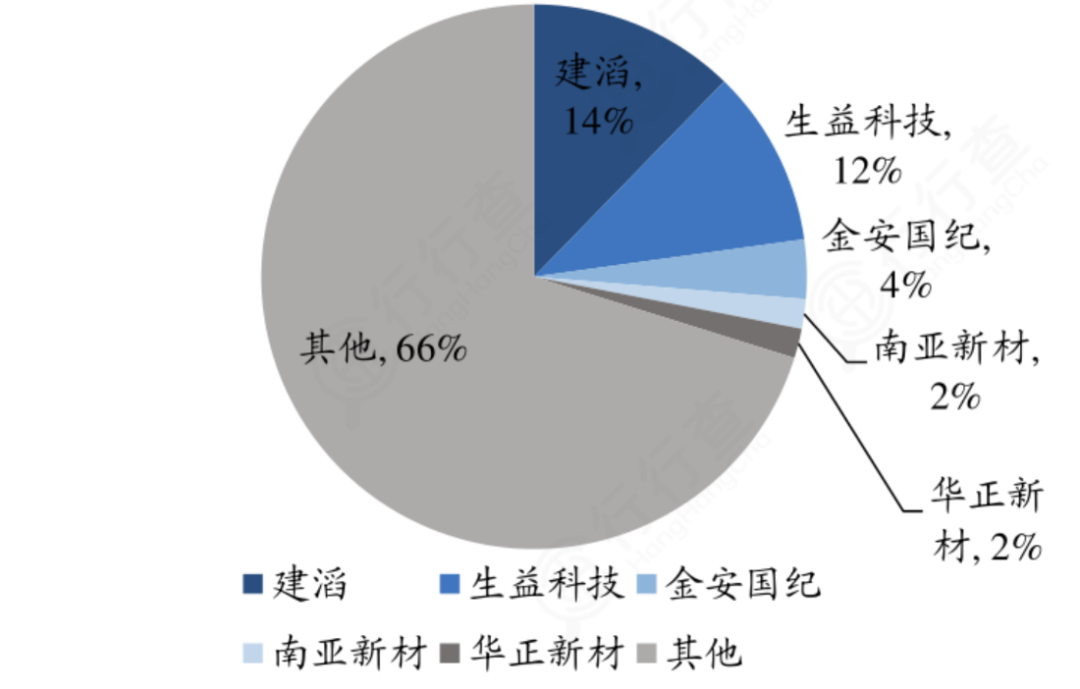

Copper-clad Laminate (CCL): Market Structure is Highly ConcentratedCopper-clad laminate is a product formed by pressing fiberglass cloth and copper foil together with epoxy resin and other bonding agents. It is a direct raw material for PCBs, which are manufactured through etching, electroplating, and multilayer board lamination.Due to the relatively favorable competitive structure of the copper-clad laminate industry compared to the downstream printed circuit board industry, copper-clad laminate companies can generally pass on costs to downstream customers. Leading companies can achieve higher profitability through scale advantages and self-manufacturing of upstream raw materials.The copper-clad laminate industry is capital-intensive and has a relatively high concentration. The global copper-clad laminate industry has a CR10 of 75% and a CR5 of 52%.The top three companies in the global copper-clad laminate market are: Kingboard Chemical with a market share of 15%, Shengyi Technology with a market share of 12%, and Nan Ya Plastics with a market share of 11%.Global Copper-clad Laminate Market Structure: Source: CCLAThere are five main copper-clad laminate manufacturers in mainland China: Kingboard Laminates, Shengyi Technology, Jin’an Guoji, Nan Ya New Materials, and Huazheng New Materials. These five manufacturers account for 34% of the global output value, while mainland China’s PCB output value exceeds 50%. Considering the supply chain support for upstream raw materials, domestic copper-clad laminate manufacturers are expected to fill the gap.

Source: CCLAThere are five main copper-clad laminate manufacturers in mainland China: Kingboard Laminates, Shengyi Technology, Jin’an Guoji, Nan Ya New Materials, and Huazheng New Materials. These five manufacturers account for 34% of the global output value, while mainland China’s PCB output value exceeds 50%. Considering the supply chain support for upstream raw materials, domestic copper-clad laminate manufacturers are expected to fill the gap. Source: Prismark

Source: Prismark

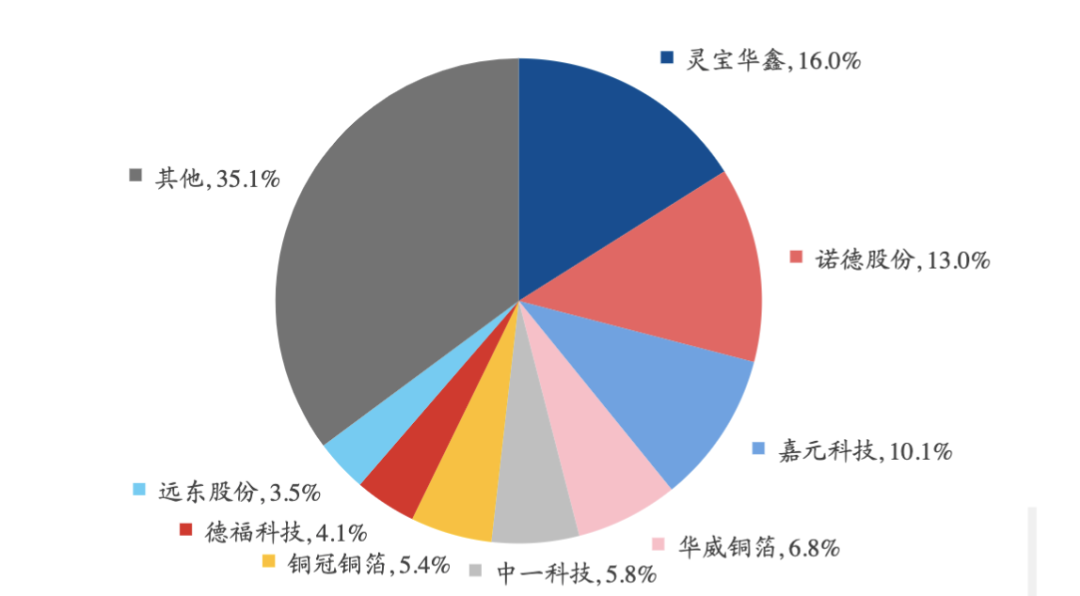

Copper Foil

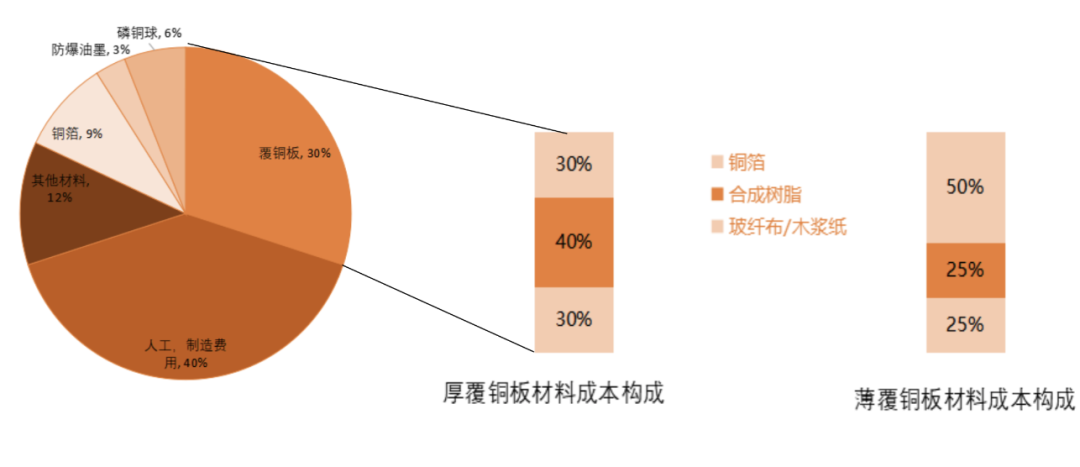

In terms of cost, copper-clad laminates account for about 30%-40% of the entire PCB manufacturing cost, and copper foil is the primary raw material for producing copper-clad laminates, accounting for 30% (thin foil) and 50% (thick foil) of the cost of copper-clad laminates.PCB Cost Distribution: Source: Tianfeng SecuritiesDepending on the application field, copper foil can be divided into lithium battery copper foil and standard copper foil.Standard copper foil is a thin layer of copper foil deposited on the substrate of the circuit board. It is one of the important base materials for copper-clad laminates and printed circuit boards, serving as a conductor. It is generally thicker than lithium battery copper foil, mostly ranging from 12-70μm, with one rough side and one smooth side. The smooth side is used for circuit printing, while the rough side combines with the substrate.From the perspective of the global copper foil market structure, the production technology and market share of high-performance PCB copper foil are still dominated by Japanese manufacturers. Domestic production capacity for high-frequency and high-speed substrate copper foil has not yet formed.The top five companies in the global high-end copper foil market are: Furukawa Electric Co., Ltd., Mitsui Mining & Smelting Co., Ltd., Fukuda Metal Foil & Powder Co., Ltd., Nippon Electrolytic Co., and Nippon Energy Company, all of which are Japanese companies.Standard copper foil is less profitable than lithium battery copper foil. The competitive landscape for lithium battery copper foil is relatively fragmented, while the downstream customers in the lithium battery sector are more concentrated, making it difficult for companies to have strong negotiating power.However, copper foil technology is still continuously iterating, so having an advantage in R&D capabilities can help companies gain a competitive edge in technology iterations, thus achieving temporary profitability is the best way to lead.Dispersed Landscape of Copper Foil Sector:

Source: Tianfeng SecuritiesDepending on the application field, copper foil can be divided into lithium battery copper foil and standard copper foil.Standard copper foil is a thin layer of copper foil deposited on the substrate of the circuit board. It is one of the important base materials for copper-clad laminates and printed circuit boards, serving as a conductor. It is generally thicker than lithium battery copper foil, mostly ranging from 12-70μm, with one rough side and one smooth side. The smooth side is used for circuit printing, while the rough side combines with the substrate.From the perspective of the global copper foil market structure, the production technology and market share of high-performance PCB copper foil are still dominated by Japanese manufacturers. Domestic production capacity for high-frequency and high-speed substrate copper foil has not yet formed.The top five companies in the global high-end copper foil market are: Furukawa Electric Co., Ltd., Mitsui Mining & Smelting Co., Ltd., Fukuda Metal Foil & Powder Co., Ltd., Nippon Electrolytic Co., and Nippon Energy Company, all of which are Japanese companies.Standard copper foil is less profitable than lithium battery copper foil. The competitive landscape for lithium battery copper foil is relatively fragmented, while the downstream customers in the lithium battery sector are more concentrated, making it difficult for companies to have strong negotiating power.However, copper foil technology is still continuously iterating, so having an advantage in R&D capabilities can help companies gain a competitive edge in technology iterations, thus achieving temporary profitability is the best way to lead.Dispersed Landscape of Copper Foil Sector: Source: GGII, Industrial Securities

Source: GGII, Industrial Securities

Fiberglass Yarn: Oligopoly Structure Formation

Fiberglass yarn can be made into fiberglass cloth, which is used in the production of the core substrate of printed circuit boards (PCBs) – copper-clad laminates.Electronic fiberglass yarn accounts for about 25%-40% of the cost of copper-clad laminates and is a crucial material in PCB preparation, with high demand.From the perspective of global fiberglass production capacity, by the end of 2019, CR6 (China Jushi, US OC, Japan NEG, Taishan Fiberglass, Chongqing International, US JM) accounted for over 70% of the total global fiberglass production capacity. The CR3 in China (China Jushi, Taishan Fiberglass, Chongqing International) accounted for over 60% of the total domestic production capacity, while CR6 (CR3 and Shandong Fiberglass, Sichuan Weibao, Changhai Co.) accounted for about 80% of the total domestic production capacity. The oligopoly structure of fiberglass supply has basically formed globally and domestically. Source: Huazheng New Materials IPO Prospectus

Source: Huazheng New Materials IPO Prospectus

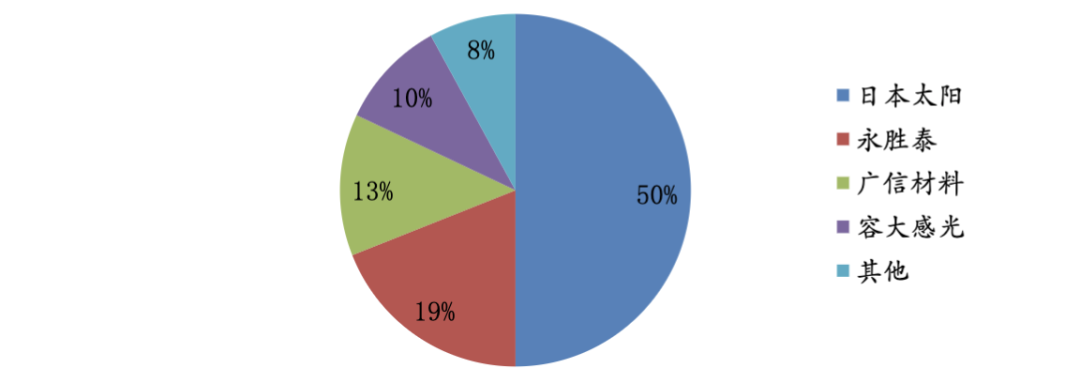

PCB Ink: Domestic Brand Advantages Stand Out

According to the prospectus of Rongda Photoelectric, although the differences in PCB types and layers can lead to variations in the proportion of PCB ink to PCB output value, on the whole, PCB ink accounts for an average of about 3% of the PCB output value. Therefore, the market size of PCB ink tends to fluctuate in line with that of PCBs.From a market perspective, the high-end market for domestic PCB-specific inks is still mainly occupied by foreign companies like Japan’s Sun Chemical.As the global manufacturing industry accelerates its shift to China, some domestic suppliers have gradually mastered the synthesis technology of key raw materials for PCB inks, changing the previous reliance on imported synthetic resins. At the same time, foreign suppliers are gradually losing market share due to disadvantages such as transportation distance and high production costs, while domestic brands’ cost-performance advantages are becoming increasingly prominent.Domestic PCB ink suppliers such as Guangxin Materials and Rongda Photoelectric have gradually grown, and their related products have started to enter large PCB manufacturers like Foxconn, Shenzhen South Circuit, and Jinko Electronics.Currently, Guangxin Materials’ solder mask ink products rank first among domestic brands in market share. Source: Jinko Electronics IPO Prospectus

Source: Jinko Electronics IPO Prospectus

Midstream Manufacturing of PCB Industry Chain

Midstream Manufacturing of PCB Industry Chain

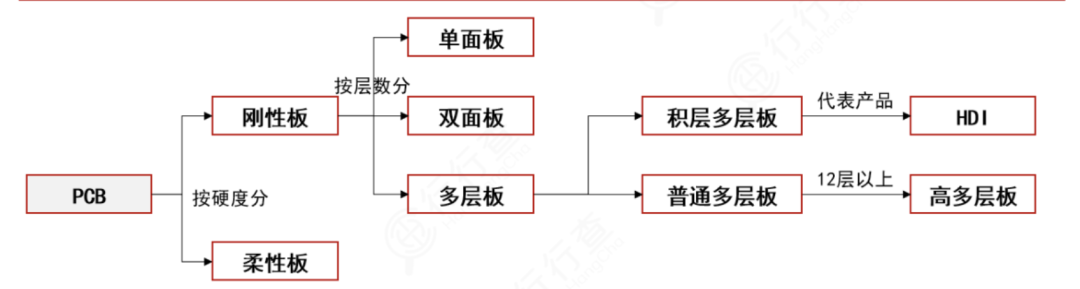

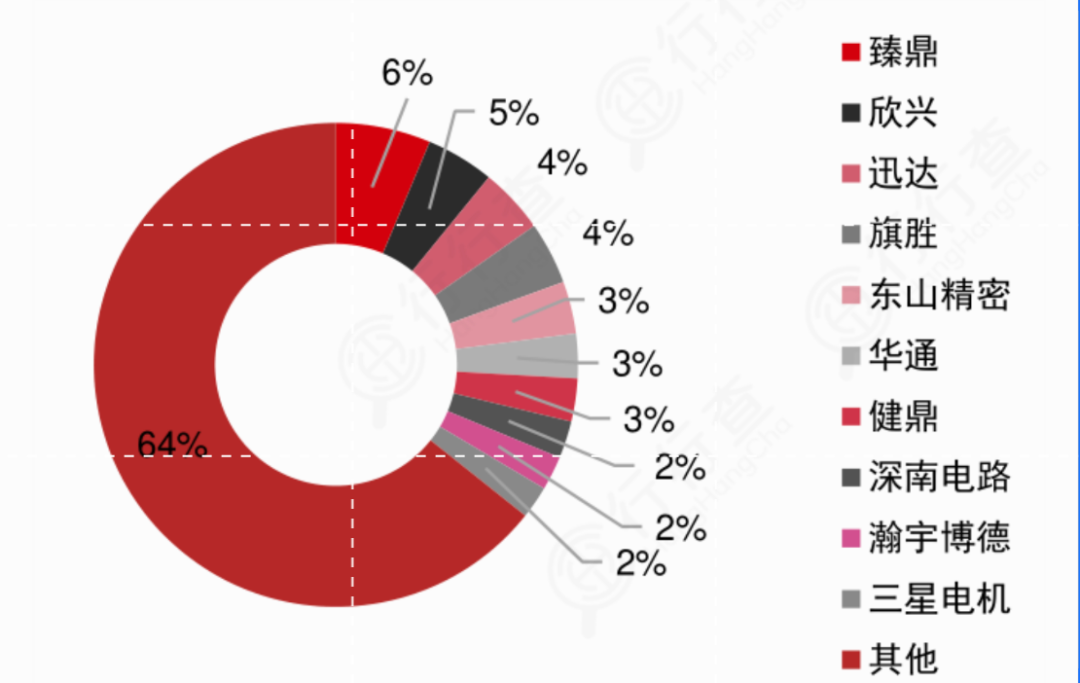

The PCB industry is capital-intensive and has high technical requirements for manufacturers.According to the prospectus of Pegatron, establishing a production line with an annual capacity of over one million square meters requires an investment of hundreds of millions of yuan. PCB manufacturers also need to maintain continuous high investment in raw materials, R&D, etc., to meet downstream customers’ requirements for customized production, product upgrades, and rapid delivery.There are numerous types of PCBs. Generally, they can be divided into rigid circuit boards, flexible boards, and rigid-flex boards based on hardness. Based on the number of conductive layers, they can be categorized into single-sided boards, double-sided boards, and multilayer boards.Multilayer boards can be divided into ordinary multilayer boards and stacked multilayer boards based on the number of lamination cycles. In ordinary multilayer boards, those with more than 12 layers are generally referred to as high multilayer boards.Stacked multilayer boards are represented by HDI (High-Density Interconnect) boards, which are widely used in portable consumer electronics due to their high wiring density. High-end smartphones mainly use 10-layer or more 3-stage HDI boards.In automotive circuit boards, traditional single-layer PCBs, double-layer PCBs, and multilayer PCBs are widely used, and in recent years, the extensive application of HDI has also become the first choice for automotive electronic products. From the perspective of the competitive landscape on the PCB manufacturing side, the global market share is relatively fragmented.High-end PCB manufacturers are further expanding their market share and improving profitability under the support of technological dividends, while mid-to-low-end manufacturers are gradually exiting due to slow technological upgrades and compressed profit margins.According to Pegatron’s prospectus, although the global PCB market structure is still relatively fragmented (with over 2000 manufacturers globally), factors such as capital, technology, supply chain, and environmental management capabilities have created a high barrier to entry in the PCB industry, and the industry barriers continue to rise with the iteration and upgrade of downstream customer products.The top companies in the PCB industry are: Zhen Ding with a market share of 6%, Xinxing Technology with a market share of 5%, and Xunda with a market share of 4%.

From the perspective of the competitive landscape on the PCB manufacturing side, the global market share is relatively fragmented.High-end PCB manufacturers are further expanding their market share and improving profitability under the support of technological dividends, while mid-to-low-end manufacturers are gradually exiting due to slow technological upgrades and compressed profit margins.According to Pegatron’s prospectus, although the global PCB market structure is still relatively fragmented (with over 2000 manufacturers globally), factors such as capital, technology, supply chain, and environmental management capabilities have created a high barrier to entry in the PCB industry, and the industry barriers continue to rise with the iteration and upgrade of downstream customer products.The top companies in the PCB industry are: Zhen Ding with a market share of 6%, Xinxing Technology with a market share of 5%, and Xunda with a market share of 4%. Source: CITIC SecuritiesPrismark predicts that the advancement of server/data storage and wired/wireless infrastructure construction will drive rapid growth in PCB demand. With the innovative applications of automotive and other consumer electronics gradually becoming widespread, the output value of PCBs in related fields is also expected to increase.After 2000, there has been a noticeable trend of the PCB industry shifting to mainland China. This trend is expected to continue in the future, with Prismark forecasting that the output value of PCBs in mainland China will reach $41.77 billion by 2024, accounting for 55.1%, leading to rapid development in the industry.

Source: CITIC SecuritiesPrismark predicts that the advancement of server/data storage and wired/wireless infrastructure construction will drive rapid growth in PCB demand. With the innovative applications of automotive and other consumer electronics gradually becoming widespread, the output value of PCBs in related fields is also expected to increase.After 2000, there has been a noticeable trend of the PCB industry shifting to mainland China. This trend is expected to continue in the future, with Prismark forecasting that the output value of PCBs in mainland China will reach $41.77 billion by 2024, accounting for 55.1%, leading to rapid development in the industry.

Click here to quickly view recent hot industries

👉🏻 Silicon Carbide Industry Chain Map👉🏻 Perovskite Battery Industry Chain Analysis👉🏻 IGBT Industry Chain Investment Map👉🏻 Carbon Fiber Industry Chain Overview👉🏻 Military Equipment Investment Map👉🏻 Power Battery Recycling Overview👉🏻 Automotive Thermal Management: High-Value Segmented Track

Exchange for Learning | Business Cooperation | Article ReprintPlease leave a message in the background or add the assistant WeChat: lqzk999👇Give a “Share, Like, and Watch” triple click!