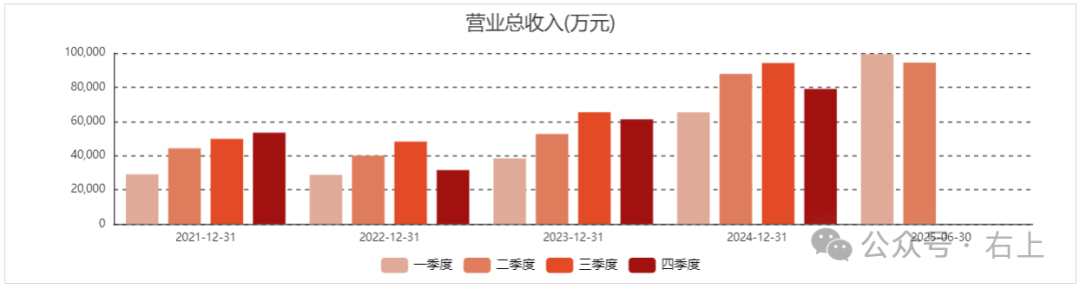

Disclaimer: This article serves solely as a personal investment record for individual learning and review, and under no circumstances constitutes investment advice for any individual. The author of this article bears no legal responsibility for any consequences arising from the use of its content. Readers are advised not to trade based on any varieties mentioned in this article. The varieties mentioned carry the risk of significant losses, which is not alarmist but a reality experienced by most of my investments during the current bear market from 2022 to 2024. The stock market carries risks; investment should be approached with caution!In 2016, Apple released the revolutionary AirPods,which led to rapid development in the Bluetooth TWS headphone industry. Many domestic chip design companies have entered this field, and previous articles have briefly introduced Hengxuan Technology, Rockchip Technology,and Zhongke Lanyun,three companies whose main products are low-power Bluetooth audio chips.Hengxuan Technology: Can Hengxuan Technology’s AI glasses become a new growth engine?Rockchip Technology: Another company designing low-power Bluetooth audio chips.Zhongke Lanyun: The Bluetooth audio chip design sector is indeed quite crowded.1. Comparison of Semi-Annual Report PerformanceNow that the semi-annual reports for 2025 have been released, let’s take a look at the performance of these three companies. Hengxuan has the largest revenue scale, more than double that of Zhongke Lanyun, which is nearly double that of Rockchip Technology. Both Hengxuan and Rockchip saw significant year-on-year growth in H1, but Hengxuan’s quarter-on-quarter growth in Q2 was negative due to supplier changes. Lanyun’s H1 performance was almost flat year-on-year, with no growth.1) Hengxuan TechnologyIn H1 2025, revenue grew by 26.58% year-on-year, and net profit attributable to the parent company grew by 106.45%. However, revenue in Q2 decreased quarter-on-quarter. This is partly due to a high base in Q1, and the company also mentioned in its performance forecast that “the adjustment of the supply chain in the first half of the year has negatively impacted the shipment pace in Q2.” We will continue to observe the situation in Q3. Hengxuan Technology’s H1 2025 performance report (from the company’s official account)

Hengxuan Technology’s H1 2025 performance report (from the company’s official account) Hengxuan Technology’s quarterly revenue situation (from Eastmoney website)2) Rockchip TechnologyIn H1 2025, revenue grew by 60.12% year-on-year, and net profit attributable to the parent company grew by 123.19%. Revenue in Q2 also saw significant quarter-on-quarter growth.

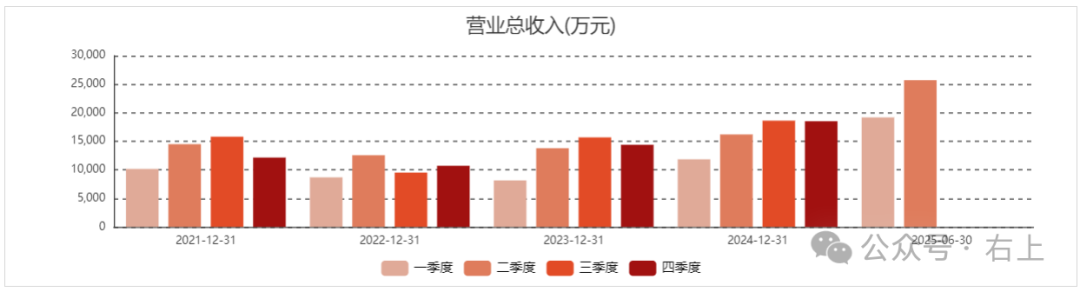

Hengxuan Technology’s quarterly revenue situation (from Eastmoney website)2) Rockchip TechnologyIn H1 2025, revenue grew by 60.12% year-on-year, and net profit attributable to the parent company grew by 123.19%. Revenue in Q2 also saw significant quarter-on-quarter growth. Rockchip Technology’s H1 2025 performance report (from the company’s official account)

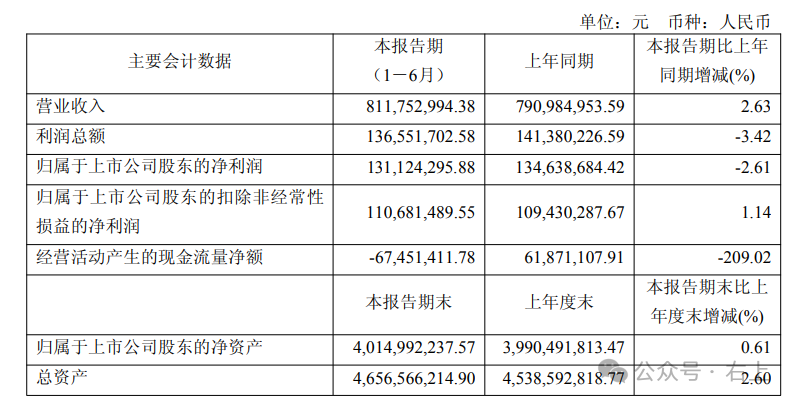

Rockchip Technology’s H1 2025 performance report (from the company’s official account) Rockchip Technology’s quarterly revenue situation (from Eastmoney website)3) Zhongke LanyunThe semi-annual report shows that both revenue and net profit year-on-year have seen almost no growth, which may be due to the company’s products primarily targeting low-end white-label markets, failing to benefit from the current wave of national subsidies.

Rockchip Technology’s quarterly revenue situation (from Eastmoney website)3) Zhongke LanyunThe semi-annual report shows that both revenue and net profit year-on-year have seen almost no growth, which may be due to the company’s products primarily targeting low-end white-label markets, failing to benefit from the current wave of national subsidies. Zhongke Lanyun’s semi-annual performance (from the company’s 2025 semi-annual report)

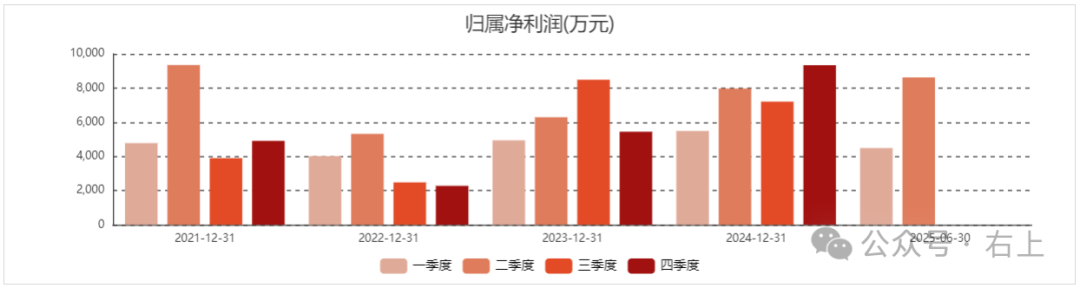

Zhongke Lanyun’s semi-annual performance (from the company’s 2025 semi-annual report) Zhongke Lanyun’s quarterly revenue situation (from Eastmoney website)

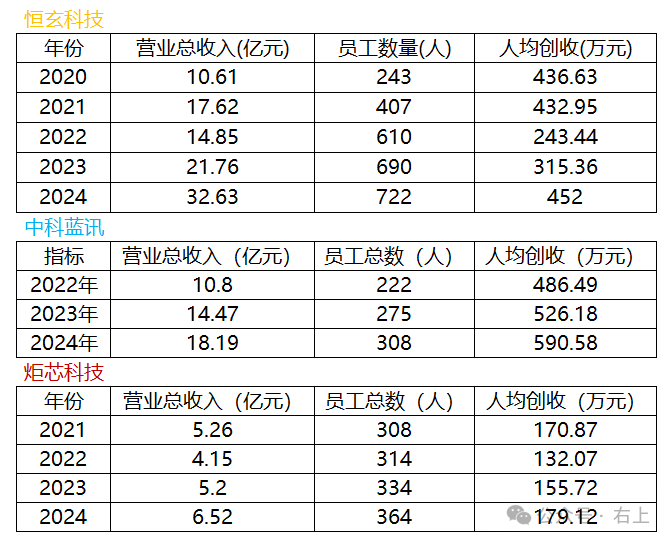

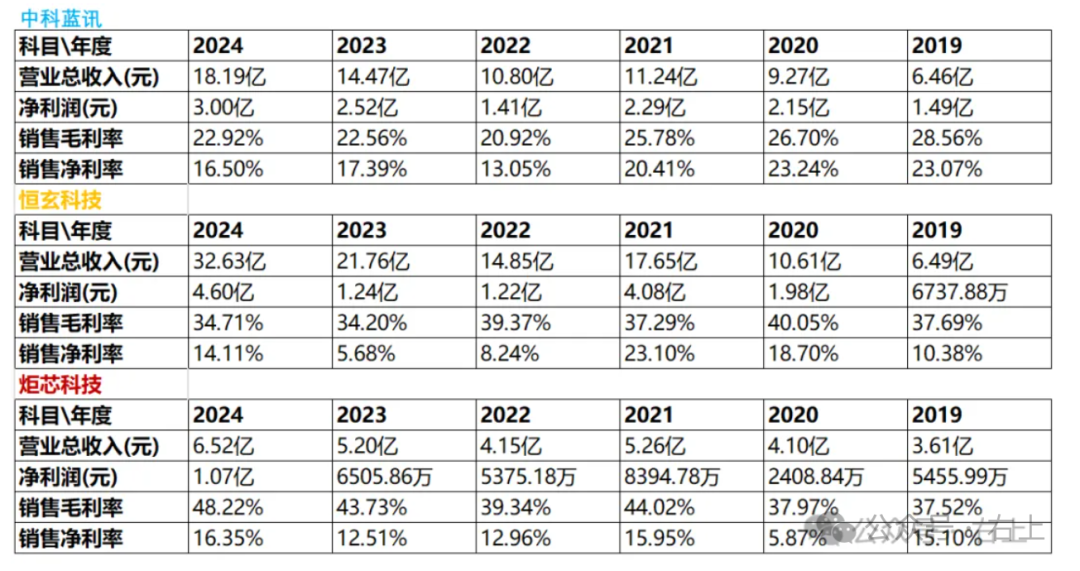

Zhongke Lanyun’s quarterly revenue situation (from Eastmoney website) Zhongke Lanyun’s quarterly net profit situation (from Eastmoney website)2. Comparison of Company OperationsIn previous articles, we listed the operational conditions of the three companies. From the perspective of gross margin and net margin, Hengxuan and Rockchip are relatively close. Lanyun’s gross margin is significantly lower than the other two, but its net margin is similar, even slightly higher. From the latest Q2 situation, Hengxuan has a gross margin of 40% and a net margin of 12%; Rockchip has a gross margin of 51% and a net margin of 19%; Lanyun has a gross margin of 23% and a net margin of 19%.Hengxuan has the most R&D personnel, indicating a greater potential for future growth. Moreover, the 6nm BES2800 has already been introduced to clients and is ramping up production quickly, which is very helpful in consolidating the company’s high-end market share. There are also more advanced process chips under development.

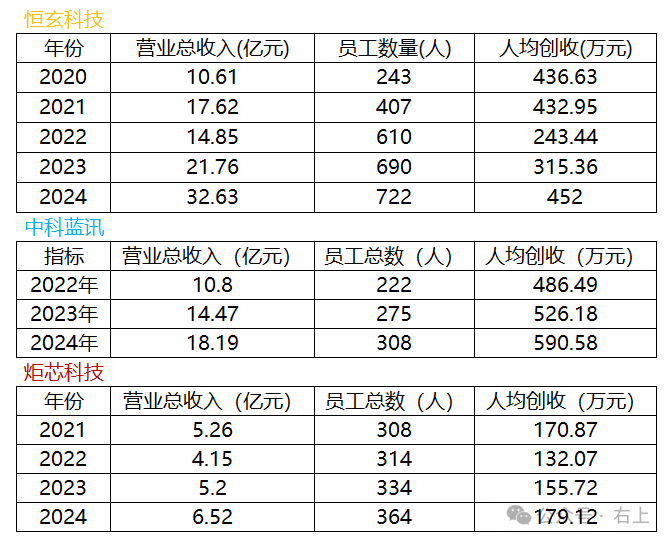

Zhongke Lanyun’s quarterly net profit situation (from Eastmoney website)2. Comparison of Company OperationsIn previous articles, we listed the operational conditions of the three companies. From the perspective of gross margin and net margin, Hengxuan and Rockchip are relatively close. Lanyun’s gross margin is significantly lower than the other two, but its net margin is similar, even slightly higher. From the latest Q2 situation, Hengxuan has a gross margin of 40% and a net margin of 12%; Rockchip has a gross margin of 51% and a net margin of 19%; Lanyun has a gross margin of 23% and a net margin of 19%.Hengxuan has the most R&D personnel, indicating a greater potential for future growth. Moreover, the 6nm BES2800 has already been introduced to clients and is ramping up production quickly, which is very helpful in consolidating the company’s high-end market share. There are also more advanced process chips under development. Why does Lanyun have a gross margin significantly lower than the other two yet manage to achieve a slightly higher net margin? By examining the number of employees and revenue per capita for the three companies, the answer becomes clear. Lanyun has fewer employees than Rockchip, yet its revenue in 2024 is nearly three times that of Rockchip. Its revenue per capita is the highest among the three. Therefore, Lanyun’s strategy is to gain market share through low gross margins and low costs (using lower-end processes and RISC V), while controlling R&D scale to manage expense ratios, thus achieving a higher net margin.

Why does Lanyun have a gross margin significantly lower than the other two yet manage to achieve a slightly higher net margin? By examining the number of employees and revenue per capita for the three companies, the answer becomes clear. Lanyun has fewer employees than Rockchip, yet its revenue in 2024 is nearly three times that of Rockchip. Its revenue per capita is the highest among the three. Therefore, Lanyun’s strategy is to gain market share through low gross margins and low costs (using lower-end processes and RISC V), while controlling R&D scale to manage expense ratios, thus achieving a higher net margin. 3. Initial Company AssessmentNote: The initial company assessment refers to Warren Buffett’s three dimensions for evaluating a company: 1) Does it have a good business model? 2) Does it have a good management team? 3) Is it in a good price range? This assessment qualitatively analyzes and evaluates a company based on these three dimensions rather than quantitatively. Please note that this evaluation is merely my personal understanding, and due to insufficient research on the company, it may differ significantly from the actual situation. Please do not make trading decisions based on this.Initial assessment of the business model (ranked from high to low: high, above average, average, below average, low)This sector is highly competitive. In addition to the three companies mentioned in the article, there are other companies as well. Additionally, companies like Qualcomm and MTK also have corresponding products in this field. Therefore, the current business model is rated as average. Among the three companies, Hengxuan is the most promising, as it currently leads in both revenue scale and R&D strength, focusing on the high-end market, which deserves a higher valuation.Initial assessment of the management team (ranked from high to low: excellent, good, average, poor)All three companies were founded around the same time, around 2016. Based on the historical performance of the three companies, it is evident that Hengxuan’s management team is superior. Hengxuan’s management team is rated as good, while the other two are rated as average.Current stock price assessment (very high, high, reasonable, low, very low)Based on the latest four quarters of performance, Hengxuan’s revenue is approximately 3.67 billion, with a net profit of about 620 million; Lanyun’s revenue is approximately 1.84 billion, with a net profit of about 300 million; Rockchip’s revenue is approximately 820 million, with a net profit of about 160 million.As of the closing price on September 5, 2025, Hengxuan’s market value is 42 billion, with a PS ratio of about 11.4 times and a dynamic PE ratio of about 67.7 times; Lanyun’s market value is 13.3 billion, with a PS ratio of about 7.2 times and a dynamic PE ratio of about 44.3 times; Rockchip’s market value is 9.57 billion, with a PS ratio of about 11.7 times and a dynamic PE ratio of about 59.8 times. Currently, Hengxuan and Rockchip’s valuations are very close, while Lanyun’s market value is lower due to its growth potential. At present, all three companies are considered overvalued. Unfortunately, the current market and the semiconductor industry as a whole are generally overvalued, and it is unlikely to see a more reasonable valuation in the short term.Among the three companies, Hengxuan is undoubtedly the most promising. However, the company’s market share in the headphone and smartwatch sectors is already quite high. Although AI glasses are experiencing strong growth, the market is still relatively small, and there is currently no new growth curve in sight. Furthermore, as processes become more advanced, costs are also rising, and it remains to be seen whether the current gross margin levels can be maintained.

3. Initial Company AssessmentNote: The initial company assessment refers to Warren Buffett’s three dimensions for evaluating a company: 1) Does it have a good business model? 2) Does it have a good management team? 3) Is it in a good price range? This assessment qualitatively analyzes and evaluates a company based on these three dimensions rather than quantitatively. Please note that this evaluation is merely my personal understanding, and due to insufficient research on the company, it may differ significantly from the actual situation. Please do not make trading decisions based on this.Initial assessment of the business model (ranked from high to low: high, above average, average, below average, low)This sector is highly competitive. In addition to the three companies mentioned in the article, there are other companies as well. Additionally, companies like Qualcomm and MTK also have corresponding products in this field. Therefore, the current business model is rated as average. Among the three companies, Hengxuan is the most promising, as it currently leads in both revenue scale and R&D strength, focusing on the high-end market, which deserves a higher valuation.Initial assessment of the management team (ranked from high to low: excellent, good, average, poor)All three companies were founded around the same time, around 2016. Based on the historical performance of the three companies, it is evident that Hengxuan’s management team is superior. Hengxuan’s management team is rated as good, while the other two are rated as average.Current stock price assessment (very high, high, reasonable, low, very low)Based on the latest four quarters of performance, Hengxuan’s revenue is approximately 3.67 billion, with a net profit of about 620 million; Lanyun’s revenue is approximately 1.84 billion, with a net profit of about 300 million; Rockchip’s revenue is approximately 820 million, with a net profit of about 160 million.As of the closing price on September 5, 2025, Hengxuan’s market value is 42 billion, with a PS ratio of about 11.4 times and a dynamic PE ratio of about 67.7 times; Lanyun’s market value is 13.3 billion, with a PS ratio of about 7.2 times and a dynamic PE ratio of about 44.3 times; Rockchip’s market value is 9.57 billion, with a PS ratio of about 11.7 times and a dynamic PE ratio of about 59.8 times. Currently, Hengxuan and Rockchip’s valuations are very close, while Lanyun’s market value is lower due to its growth potential. At present, all three companies are considered overvalued. Unfortunately, the current market and the semiconductor industry as a whole are generally overvalued, and it is unlikely to see a more reasonable valuation in the short term.Among the three companies, Hengxuan is undoubtedly the most promising. However, the company’s market share in the headphone and smartwatch sectors is already quite high. Although AI glasses are experiencing strong growth, the market is still relatively small, and there is currently no new growth curve in sight. Furthermore, as processes become more advanced, costs are also rising, and it remains to be seen whether the current gross margin levels can be maintained.

—————————————————————-

This public account mainly focuses on researching companies in the semiconductor electronics industry. Below are links to historical articles; feel free to click to read if interested. This article is quite long, and I appreciate you reading to the end. If you enjoy the author’s articles, please give a thumbs up and a heart. If you are interested in discussing the content, feel free to leave a message in the comments!

Learning from OmniVision’s semi-annual report

Initial impressions of OmniVision

Wentai Technology is about to become a pure semiconductor company

Wentai Technology – Transitioning from Addition to Subtraction

Initial impressions of Lattice Semiconductor

Initial impressions of Sunlord Electronics

Initial impressions of GigaDevice

Initial impressions of Espressif Technology

The Bluetooth audio chip design sector is indeed quite crowded

Another company designing low-power Bluetooth audio chips

Rockchip, a chip design company that always captures popular sectors

This company dominates 40% of the mobile phone market in Africa but is relatively unknown domestically

Hengxuan Technology: Can AI glasses become a new growth engine?

Applauding Huaqin Technology’s pioneering efforts

Reading notes on Huaqin Technology’s 2024 financial report

Initial impressions of Kingdee International

Xiaomi’s automotive business continues to drive group growth

If smoothly acquired, Focus Media’s acquisition of New Wave will bring certain performance growth