If past AI was helping humans “write emails,” the future AI is learning to help humans “do business.”

UBS released a recent research report, using a baseball term to describe the current AI transformation—”Top of the third inning.” This means the game has just begun, and we are far from the decisive moment.

According to McKinsey data, in the past five years, insurance companies that have taken the lead in AI have achieved a total shareholder return (TSR) that is 6.1 times greater than that of laggards.

This is not merely a technology show, but a war about survival efficiency.

Today, we combine UBS’s in-depth research to dissect the evolution from Generative AI (Gen AI) to Agentic AI, and see who the real winners are in this transformation.

1. Current Situation: From “Testing the Waters” to “Monetization”

In the past two years, most insurance companies were still conducting AI “pilot projects.” However, in the last 12-18 months, the situation has changed. UBS points out that the industry has seen measurable profit and loss (P&L) and balance sheet benefits.

This benefit no longer comes solely from layoffs, but more from the “brute force cracking” of unstructured data.

💡 Terminology Explanation: Unstructured Data

Previously, computers could only understand numbers in Excel. However, the insurance industry is filled with PDF documents, handwritten claims forms, doctor notes, and on-site photos, which are all examples of “unstructured data.” The breakthrough of Generative AI is that it can understand this chaotic information and convert it into decision-making basis.

In the next 5-10 years, the key transformation will shift from “predictive analytics” to “Generative AI and Agentic AI.”

2. Property and Casualty (P&C): Taming Chaotic Data

For Property and Casualty (P&C) insurance, AI is reshaping three core pillars: underwriting, claims, and distribution.

1. Underwriting

Traditional underwriters spend a lot of time reading thick submission materials. Now, AI can not only extract data but also perform catastrophe modeling. Applicable scenarios: AI can comprehensively analyze geographic information, historical weather data, and building structure data to calculate potential losses from hurricanes or floods more accurately than humans.

2. Claims

AI is simplifying end-to-end submission management and accelerating the processing of complex claims. By automating manual processes, administrative overhead that previously took weeks has been significantly reduced.

3. Brokers

The current AI adoption rate among brokers is still in its early stages, mainly focused on productivity tools. Although large brokerage firms have made many announcements, most are still in the “experimental phase.”

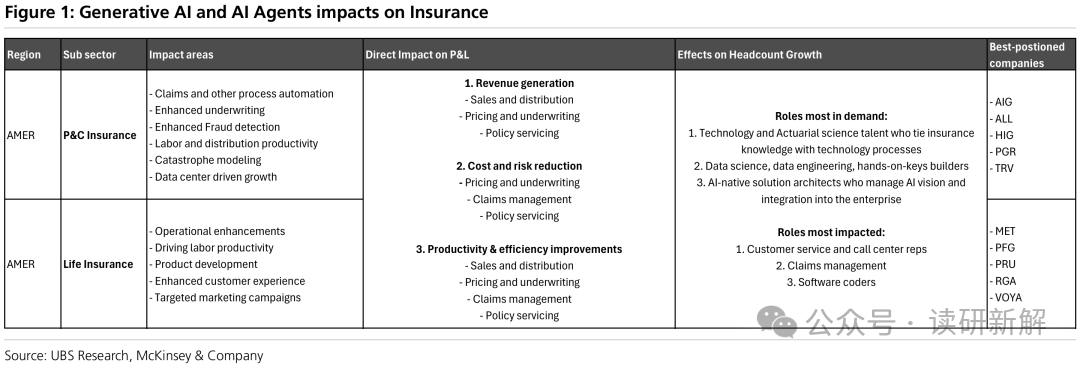

👇 The following image shows the specific impact of AI on different insurance sectors and the required talent structure:

The chart illustrates the specific impact areas of AI in the property and casualty and life insurance sectors in the Americas. On the left, P&C focuses on fraud detection and catastrophe modeling; life insurance emphasizes product development and customer experience. On the right, the most in-demand talent is highlighted: hybrid talents who understand both insurance and technology.

We can see a key trend: the demand for talent is undergoing a dramatic change. The most sought-after are no longer pure coders, but “AI-native solution architects” and actuarial technology talents who can combine insurance knowledge with technical processes.

3. Life Insurance: The Rise of Agentic AI

If AI is an assistant in the P&C field, then in life insurance, AI is evolving into an “agent.” The report highlights a cutting-edge concept—Agentic AI.

💡 Terminology Explanation: Agentic AI

Traditional ChatGPT answers your questions. In contrast, Agentic AI possesses “agency.” It can autonomously plan and execute multi-step tasks. For example, it not only tells you that a customer needs a physical examination but also automatically schedules the appointment, tracks the examination report, analyzes the results, and finally provides a “recommendation for underwriting.”

Group insurance business: UBS believes that group benefits underwriters may be the biggest long-term beneficiaries of the AI wave. These companies have billions of historical claims records. In the past, this data was difficult to utilize due to its complexity and outdated systems. With Agentic AI, this vast data is activated for highly accurate pricing and profitability analysis. Unfortunately, many companies have yet to fully tap into this gold mine.

4. Competitive Landscape: Elephants Dancing vs. Ants Moving

In this AI race, will the century-old traditional giants (Incumbents) win, or will the agile tech newcomers (New Entrants) prevail?

UBS experts provide a clear judgment: traditional giants have structural advantages, but they must overcome the “big company disease.”

| Type | Advantages | Disadvantages | Core Challenges |

| Traditional Giants | Data Scale: Have decades of accumulated historical data | Data is scattered across outdated systems, and decision-making processes are slow. | How to break down data silos and improve decision-making speed |

| Tech Newcomers | No historical baggage, can quickly implement AI solutions | Lack of Data: Insufficient data volume to train robust models | How to establish model barriers without historical data |

Conclusion: The winners will be those companies that can adopt a “pragmatic strategy”—that is:

Build: Develop internally for core differentiated areas (such as proprietary underwriting models).

Buy: Directly purchase ready-made solutions for common functions like document extraction and basic analysis.

5. Risks and Challenges: Not Just a Technical Issue

The industry currently lacks data scientists, but it needs “translators.” These are bridge-type talents who can connect business needs (like actuaries) with technical implementation (like programmers).

The focus of regulatory scrutiny is changing:

In the past: Focused on the input side (What data did you use?).

Now: Focused on the output side (Are the decisions made by AI fair? Is there algorithmic bias?).

Over-reliance on external AI giants may lead to core operational capabilities being compromised.

6. Investment Trends

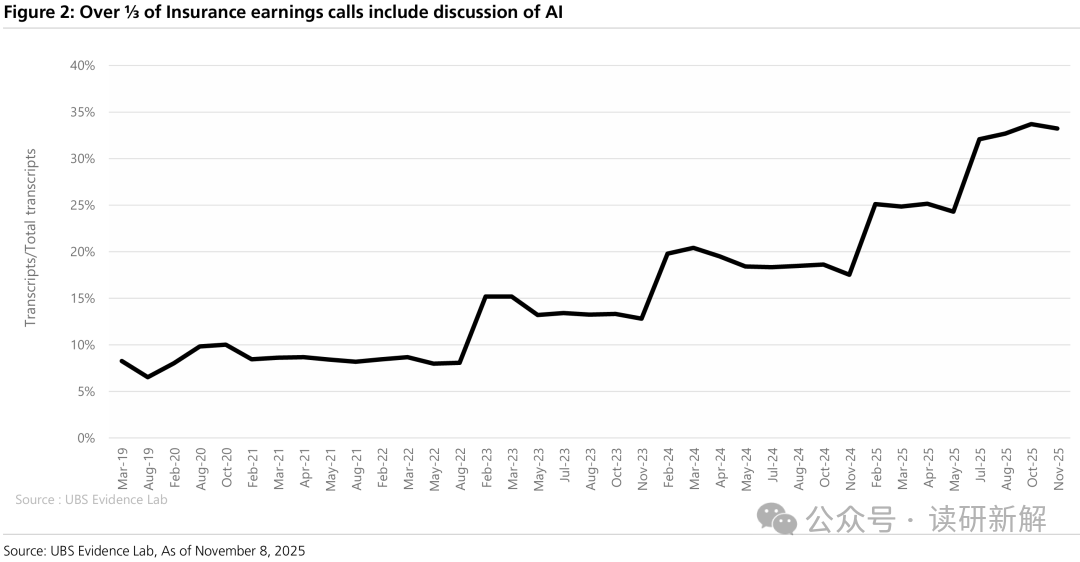

Almost every insurance company’s earnings call is now discussing AI. As shown in the following image, over one-third of earnings calls include discussions about AI.

👇 The proportion of AI mentions in insurance earnings calls has skyrocketed:

Since 2023, the proportion of AI mentions has risen exponentially, indicating high management attention. However, investors should be wary of companies that only have slogans without implementation.

UBS advises investors: Look at KPIs, not PPTs; truly successful AI applications should be reflected in improvements in the following financial metrics: Loss Ratios: Accurate pricing leads to fewer claims; Expense Ratios: High automation reduces administrative costs; Business Growth Rate: Faster underwriting leads to more new policies.

Key targets to focus on:

Most favored P&C vision: Allstate (ALL), AIG, The Hartford (HIG), Progressive (PGR), Travelers (TRV).

Most favored Life vision: MetLife (MET), Principal Financial (PFG), Prudential (PRU), RGA, Voya (VOYA).

Conclusion

The AI transformation in the U.S. insurance industry is not about creating a fully automated future, but about using Agentic AI to eliminate tedious low-value labor, allowing professionals to return to the essence of risk management.

For investors, this is also a signal: seeking those giants who hold vast amounts of data and have the ability to “unlock” data value through AI may be the source of excess returns in the next decade.