Source: WeChat Official Account: Geek Park

ID: GeekPark

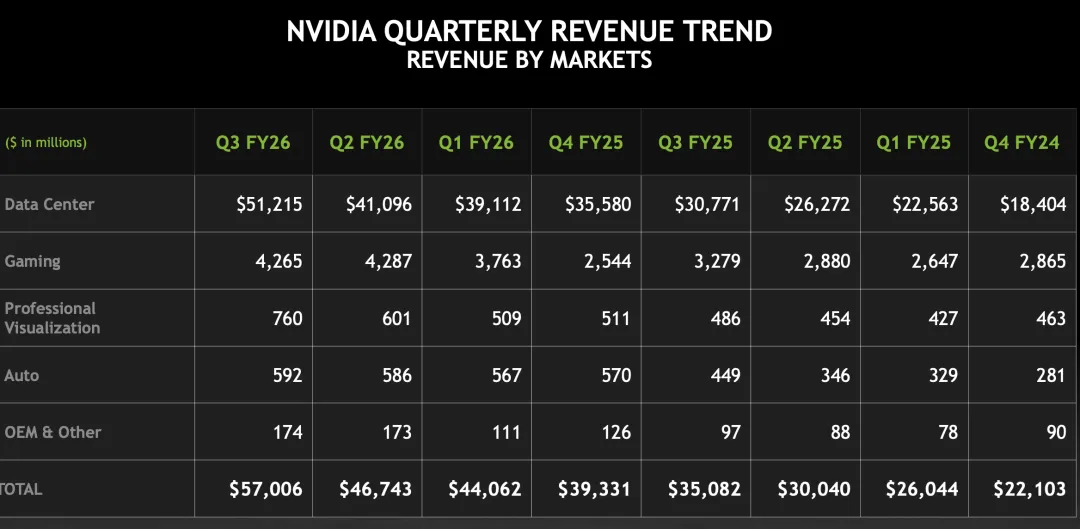

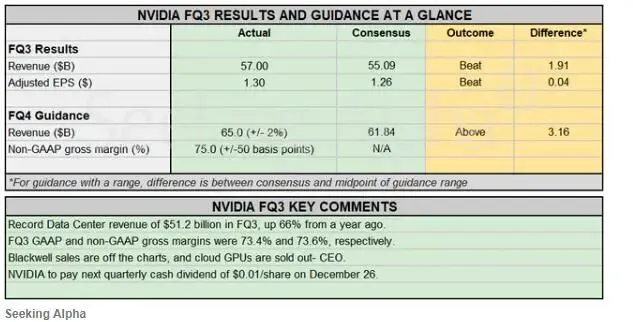

On November 20, 2025, NVIDIA announced its latest quarterly earnings report, with Q3 2025 revenue reaching $57.006 billion, a 62% increase from $35.082 billion in the same period last year; net profit was $31.910 billion, up 65% from $19.309 billion a year earlier. NVIDIA’s strong revenue generation ability once again exceeded everyone’s expectations, as its revenue three years ago was only one-tenth of what it is now.

NVIDIA Earnings Report Information | Source: NVIDIA

As the world’s most valuable technology company, NVIDIA’s every “surge” has surpassed many people’s imaginations. Rather than viewing this as a game between the company and investors, it is more accurate to say that NVIDIA, when everyone is fearful of investing heavily in AI, uses concrete earnings data to tell everyone to be bolder. “Be greedy when others are fearful” undoubtedly reflects NVIDIA’s current reality.

During the earnings call, NVIDIA CEO Jensen Huang directly responded to the market’s “AI bubble” rhetoric, stating that NVIDIA’s view on the AI bubble is “completely different” from the market’s perspective. He also elaborated that NVIDIA’s ability to reach a “higher” peak is due to AI currently promoting the transformation of three major platforms, which will lead to significant infrastructure investments, all of which are inseparable from NVIDIA.

What exactly has NVIDIA seen? Is the “AI bubble” really non-existent? What is the progress of Blackwell’s mass production? As NVIDIA raises its Q4 revenue forecast to $65 billion, it is clear that NVIDIA’s ambitions are no longer limited to expanding its commercial territory; it is transforming from a chip design giant into the “king of infrastructure” supporting the next AI revolution.

01

Blackwell Mass Production: AI Chips Made in America

NVIDIA’s ability to repeatedly break records is closely tied to the mass production and accelerated delivery of Blackwell architecture chips. The earnings report indicates that the GPU business contributed $43 billion in revenue, while the data center business soared to $51.2 billion, a year-on-year increase of 66%.

The gross margin growth to 73.4% indicates that the mass production capability of the Blackwell architecture within the supply chain has matured, also showing that NVIDIA’s capacity expansion strategy has begun to translate into profit returns.

NVIDIA Earnings Report Information | Source: NVIDIA

The fervor on the demand side continues unabated. NVIDIA’s Chief Financial Officer Colette Kress revealed that the company announced a total of 5 million GPU AI factory and infrastructure projects last quarter, covering many cloud service providers and supercomputing centers worldwide. The Blackwell Ultra GPU, released in March this year, has quickly become the company’s best-selling chip, and even the previous generation of Blackwell sales continues to break records. NVIDIA CEO Jensen Huang candidly stated, “Cloud GPUs are already sold out, and computational demand is growing exponentially in training and inference.”

Notably, in October this year, NVIDIA and TSMC historically unveiled the first AI Blackwell chip wafer at their factory in Arizona, marking the first time the strongest AI chip has been manufactured “in the USA.” It is understood that the Grace Blackwell architecture AI system has also been fully mass-produced and rapidly deployed in the operations of many cloud service providers.

NVIDIA and TSMC Produce Blackwell in Arizona | Source: Reuters

However, the significance of Blackwell’s mass production goes far beyond this. Huang emphasized in the earnings report that the growth of the data center business is driven by the “transformation of three major platforms”: accelerated computing, powerful AI models, and intelligent agent applications. He explained that non-AI software is widely running on GPUs, and AI will give rise to new applications that will require higher computational power without user input. Huang firmly believes that people will soon realize the profound changes behind the AI boom, rather than just focusing on fluctuations in capital expenditure.

This statement has evidently injected a dose of “confidence” into the market, with many analysts believing it effectively alleviated investors’ concerns about the “AI bubble,” with some comments suggesting that “perhaps the AI trading frenzy is not over yet.” When asked about the biggest constraints on NVIDIA’s growth, Huang did not point to specific areas but emphasized the enormous scale, novelty, and complexity of the AI industry, as well as the importance of meticulous planning in supply chain, infrastructure, and financing.

Huang previously revealed that the company has secured $500 billion in AI chip orders for 2025 and 2026. Now, NVIDIA CFO Colette Kress boldly predicts that sales could exceed the originally projected targets within the next two years, by December 2026. Compared to its revenue of only $130 billion for the fiscal year ending January 2025, NVIDIA has been experiencing exponential growth over the past two years.

02

Chinese Orders Becoming “Insignificant”

Despite NVIDIA’s impressive performance in the global market, its performance in the Chinese market remains constrained. This summer, NVIDIA made significant efforts to secure export licenses for the H20 chip to China. Ultimately, after Huang personally communicated with the U.S. government and reached an agreement to pay 15% of sales in China to the U.S. government, NVIDIA obtained the relevant licenses. Some analysts had optimistically predicted that the Chinese business could contribute up to $50 billion in revenue annually.

However, actual sales data fell far short of expectations. Kress revealed during the earnings call that sales of the H20 chip in the last quarter were only $50 million, a stark contrast to previous market expectations, clearly reflecting the challenges in expanding its presence in the Chinese market.

Kress bluntly stated, “Due to geopolitical factors and increasingly fierce competition in the Chinese market, we were unable to secure large procurement orders this quarter. While we are disappointed with the current situation that hinders our ability to export more competitive data center computing products to China, we remain committed to continuing communication with both the U.S. and Chinese governments.”

Jensen Huang Dancing at the Celebration | Source: NVIDIA

However, it is evident from the earnings call that NVIDIA no longer holds high expectations for the Chinese market, and its market strategy is quietly shifting towards the Middle East.In this quarter, NVIDIA’s projects in the Middle East have accelerated. The U.S. Department of Commerce has approved the export of up to 35,000 NVIDIA Blackwell chips to two companies in Saudi Arabia and the UAE, with market estimates suggesting this order could be worth over $1 billion. This not only marks the first official approval for large-scale export of Blackwell architecture chips but also directly reflects the significant investment by Middle Eastern countries in high-end AI computing infrastructure and NVIDIA’s strong penetration in the region.

Now, NVIDIA’s cooperation with Saudi Arabia extends beyond hardware sales to include establishing large AI data centers, providing technical support, and talent training programs in deeper areas. These tangible investments and collaborations not only build NVIDIA’s strong presence in the Middle East market but also mitigate potential risks arising from limitations in the Chinese market, thereby ensuring the continued stability of its global AI leadership.

03

Concerns Hidden Behind the Earnings Report

Is the AI Bubble Real or Not?

Currently, no one doubts NVIDIA’s prospects.

Ranked first globally, with a market capitalization exceeding $5 trillion and a price-to-earnings ratio as high as 30 times, rapid growth continues.

As NVIDIA reaches such heights, the market generally expects its strong growth to continue in the coming years, with many believing that during an economic downturn, the company’s price-to-earnings ratio will remain around 26 times by 2028. Although a 3.8% annualized earnings yield may seem less attractive in the short term, especially since it may take years to realize, it is important to note that we are discussing a company that may still achieve 50% year-on-year growth next year.

In this context, simplifying NVIDIA investors’ concerns to mere market fears of the “AI bubble” may be misleading. A deeper analysis of the earnings data reveals that NVIDIA still faces some challenges that have not been fully disclosed.

First, there are hidden capital expenditures. While global tech giants need to explain their massive investments in AI infrastructure to investors, NVIDIA’s own capital expenditures are rarely disclosed. NVIDIA recently revealed that it has reached agreements with cloud service providers to lease servers worth up to $26 billion over the next six years, a figure that is double what was promised three months ago, and NVIDIA itself is becoming one of the largest cloud spenders and GPU users globally.

More concerning is that NVIDIA indicated it may not fully utilize all server capacity, and some leasing commitments “may be reduced, terminated, or sold to others by the cloud service providers leasing the servers.”

Additionally, NVIDIA is also supporting its ecosystem by leasing AI chips from cloud startups like Lambda. This indicates that as an “AI shovel seller,” NVIDIA sometimes needs to invest heavily to maintain the vitality and competitiveness of its business ecosystem, which undoubtedly adds complexity to its business model.

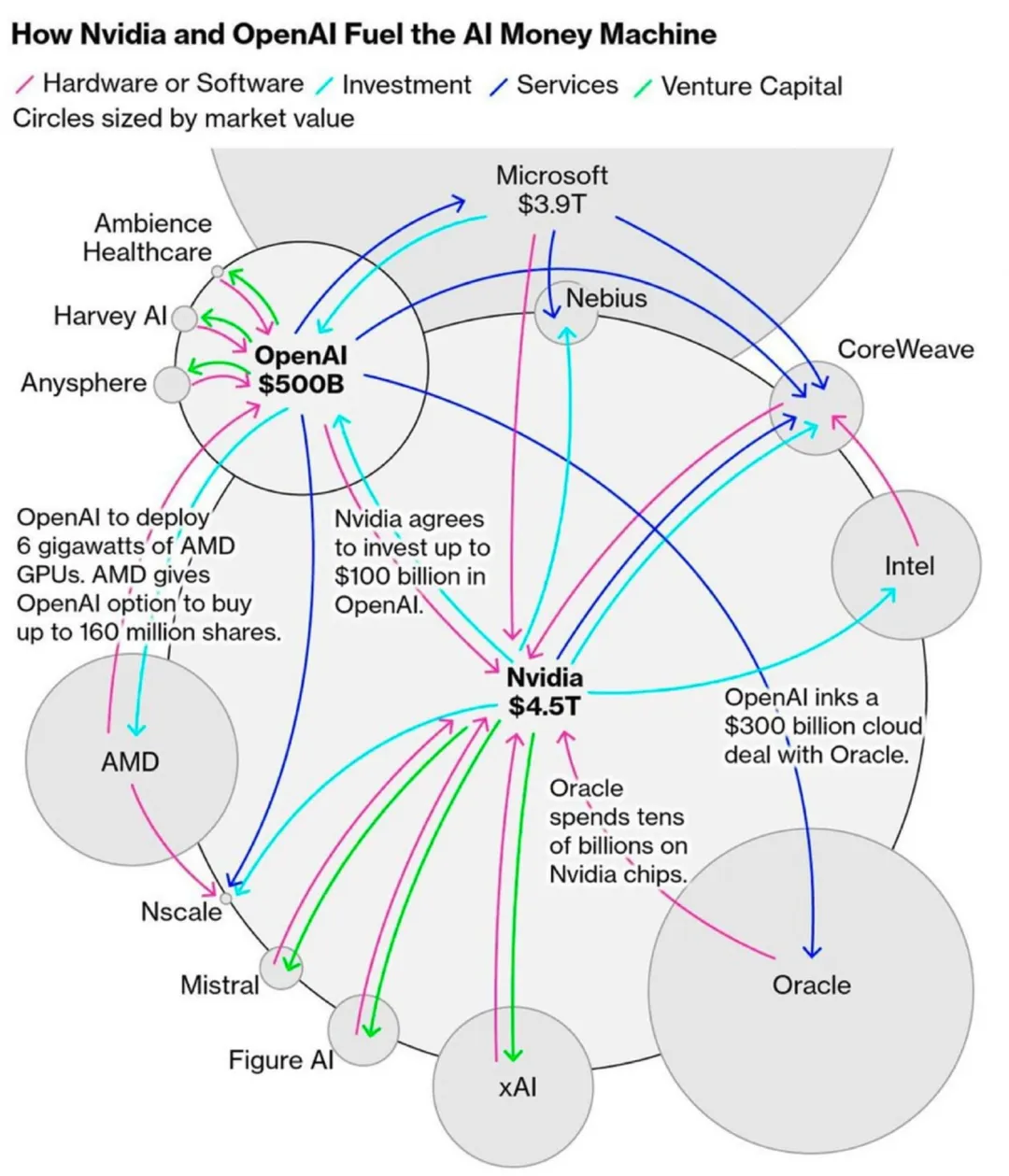

Secondly, NVIDIA’s major customers may also become its potential competitors. A regulatory filing disclosed that 61% of NVIDIA’s revenue in the third quarter came from four unnamed customers, which are speculated to include Microsoft, Meta, and Oracle. However, these tech giants are clearly unwilling to remain permanently dependent on NVIDIA’s supply chain and are actively seeking alternatives such as self-developed AI chips to break free from NVIDIA’s control. For instance, Google’s TPU chips have been gaining more customer favor, and traditional competitors like AMD are also making continuous efforts, while OpenAI and Meta have initiated plans to develop their own AI chips.

NVIDIA and OpenAI’s Joint AI Ecosystem | Source: Bloomberg

Moreover, NVIDIA’s business growth is not solely driven by pure market demand but is partially fueled by its “financial superpower.” Huang directly pointed out that “NVIDIA is using cash to drive growth.” For example, last quarter, the company invested as much as $100 billion in its two major customers, OpenAI and $10 billion in Anthropic. Notably, Anthropic previously primarily used Amazon and Google’s chips, but after receiving NVIDIA’s investment, this AI company will use NVIDIA chips for model training for the first time. This highlights NVIDIA’s high dependence on a few closely related customers and the cyclical nature of certain transactions.

Furthermore, the massive data center construction required to achieve AGI will face significant constraints in land and power. Huang addressed these concerns during the earnings call, stating that NVIDIA is actively working to ensure that factors outside the chip supply chain do not hinder its development. “We have now established partnerships with many companies in the fields of land, power, and data center construction, including financing for these projects. These matters are not easy, but they are solvable.” This indicates that NVIDIA recognizes the bottlenecks to future growth and is taking steps to build a broader ecosystem to address the complex systemic challenges posed by AI infrastructure construction.

More importantly, the sustainability of the AI business model remains in question. While NVIDIA and TSMC are profiting immensely from AI, other manufacturers have not seen significant improvements in production efficiency. If AI fails to continue generating substantial profits, customers may reduce their investments at any time, which would slow NVIDIA’s growth. Statistics show that while AI infrastructure investment is expected to reach about $4 trillion over the next five years, the currently observable productivity improvement forecasts range from an annualized 0.1% to 2.9%, indicating significant uncertainty. Especially since the release of ChatGPT, the global stock market’s value has increased by over $17 trillion, a substantial portion of which has been driven by the AI narrative. However, investors are now beginning to reassess whether this round of massive investment can yield sustainable and measurable returns, rather than just a one-time valuation boost.

Undoubtedly, NVIDIA’s strong order performance is predictable now, but the real key lies in the management’s judgment on future demand, supply chain resilience, and customer investment pace. Analyst Murphy warned that if NVIDIA signals any slowdown in AI procurement pace, the impact will not be limited to the chip sector but will also affect the data center, server supply chain, and even the entire related software ecosystem.

“Rather than fearing an AI bubble, it seems everyone wants to escape just before NVIDIA’s stock price crashes,” a Twitter user remarked.

*Header image source: Reuters

Reprinted with permission from Cool Play Lab

For reprints, please contact the original author

NVIDIA’s Earnings Report Insights

NVIDIA’s Earnings Report Insights