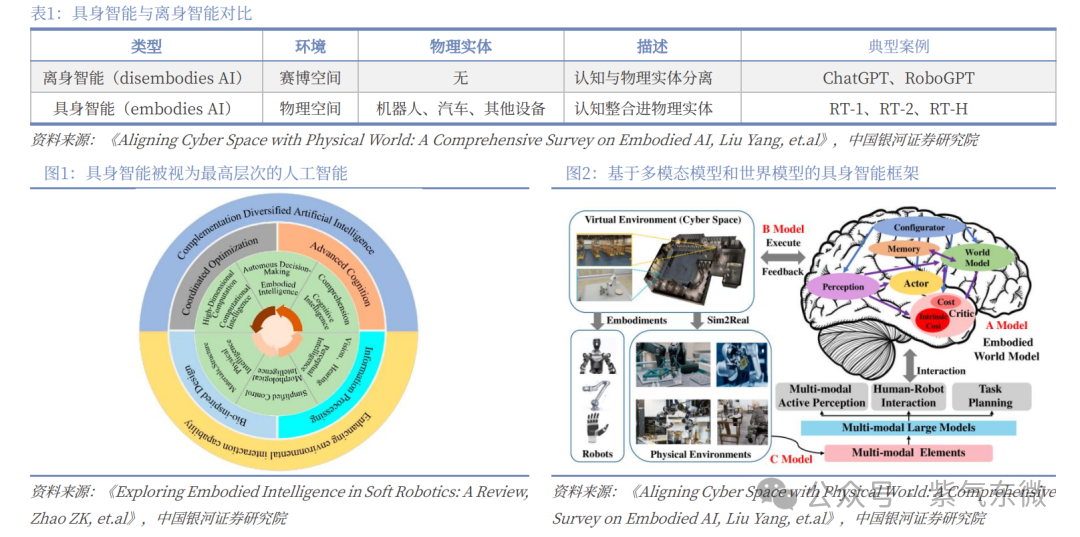

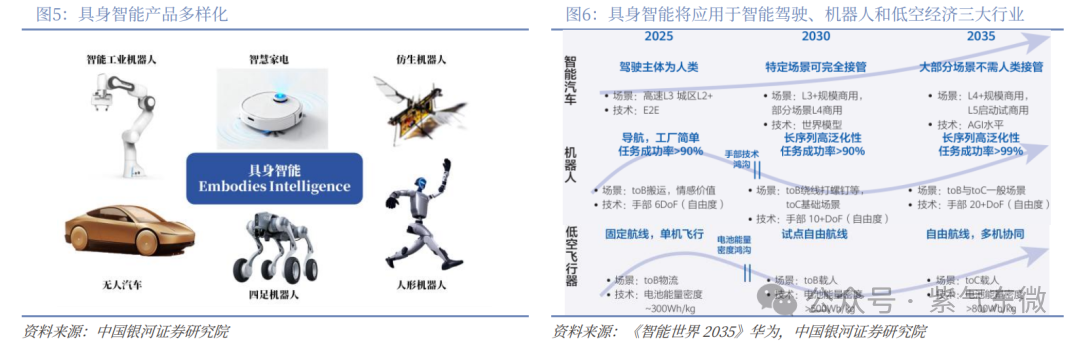

Embodied intelligence = a thinking brain + a perceiving and acting body, with its core value being the promotion of large-scale commercialization and industrialization of AI, driving efficiency and reconstructing models. The “14th Five-Year Plan” is expected to further elevate embodied intelligence as a core track supporting the strategy of a manufacturing powerhouse and digital China, achieving a strategic upgrade from “basic layout and ecological cultivation” to “core breakthroughs and integrated empowerment,” creating a “Embodied China” development model and reshaping the global competitive landscape of the intelligent industry. The market size of embodied intelligence is rapidly expanding, with a promising future, expected to exceed one trillion yuan by 2026. Humanoid robots, as representatives of embodied intelligence, are expected to first achieve applications in the industrial sector, gradually expanding to commercial services and household life, with the market size expected to reach nearly three trillion yuan by 2040.2025 is the year of mass production for humanoid robots, with technology and industrial development needs, as well as policy directions supporting the landing of application scenarios, accumulating data to feed back product iterations. Compared to other new productive forces, the current speed of promoting embodied intelligence and its long-term potential have advantages, with the industry possessing strong alpha attributes; among them, the humanoid robot direction is of utmost importance, with various technical routes yet to converge, and significant differentiated or marginal changes existing in each link. Recommended targets include: 1) Electric New Group: Wolong Electric Drive, Inovance Technology, Zhenyu Technology, Realtime Robotics, Mingzhi Electric, Fulim Precision, Xingyuan Materials, Jiechang Drive, Mingzhi Electric, etc. 2) Mechanical Group: Sanhua Intelligent Control, Green Harmonics, Fengli Intelligent, Zhongdali De, Wuzhou Xinchun, Hengli Hydraulic, Zhejiang Rongtai, Zhaowei Electromechanical, Dingzhi Technology, Hanwei Technology, Fulai New Materials; 3) Automotive Group: Sutech, Top Group, Bertley, Jingzhuan Technology, Xusheng Group, Junsheng Electronics, Horizon Robotics-W, Shuanglin Co., Zhongding Co., Lingyun Co., Best, Aikedi, Anpeilong.1. Embodied Intelligence – The Next Wave of Artificial IntelligenceEmbodied intelligence = a thinking brain + a perceiving and acting body. Embodied intelligence refers to intelligent agents with a physical carrier that can utilize their perception, decision-making, and interaction capabilities to perform tasks in the real world, continuously learning and evolving through interaction with the environment. This distinguishes it from traditional IoT, which emphasizes the application of AI in data linking, analysis, processing, and final decision-making between devices. The next wave of AI is physical AI. Embodied intelligence is regarded as the highest level of artificial intelligence. In July 2025, Huang Jenxun stated at the third Chain Expo’s advanced manufacturing chain theme event that “the next wave of AI is physical AI,” indicating that the technological trend of embodied intelligence has already formed. The core value of embodied intelligence is to promote the large-scale commercialization and industrialization of AI. Embodied intelligence is widely penetrating industries such as manufacturing, logistics, healthcare, transportation, and energy, driving efficiency and model reconstruction, bringing more opportunities for industrial landing. Its tangible products include but are not limited to various robots, smart cars, etc. Huawei predicts that embodied intelligence will be applied in three key industries: smart driving, smart robots, and low-altitude economy. IFR points out that AI and humanoid robots have become major trends in global robotics, with global professional service robot sales increasing by 30% in 2023, most of which possess varying degrees of intelligent features, and the commercialization potential is rapidly being released.

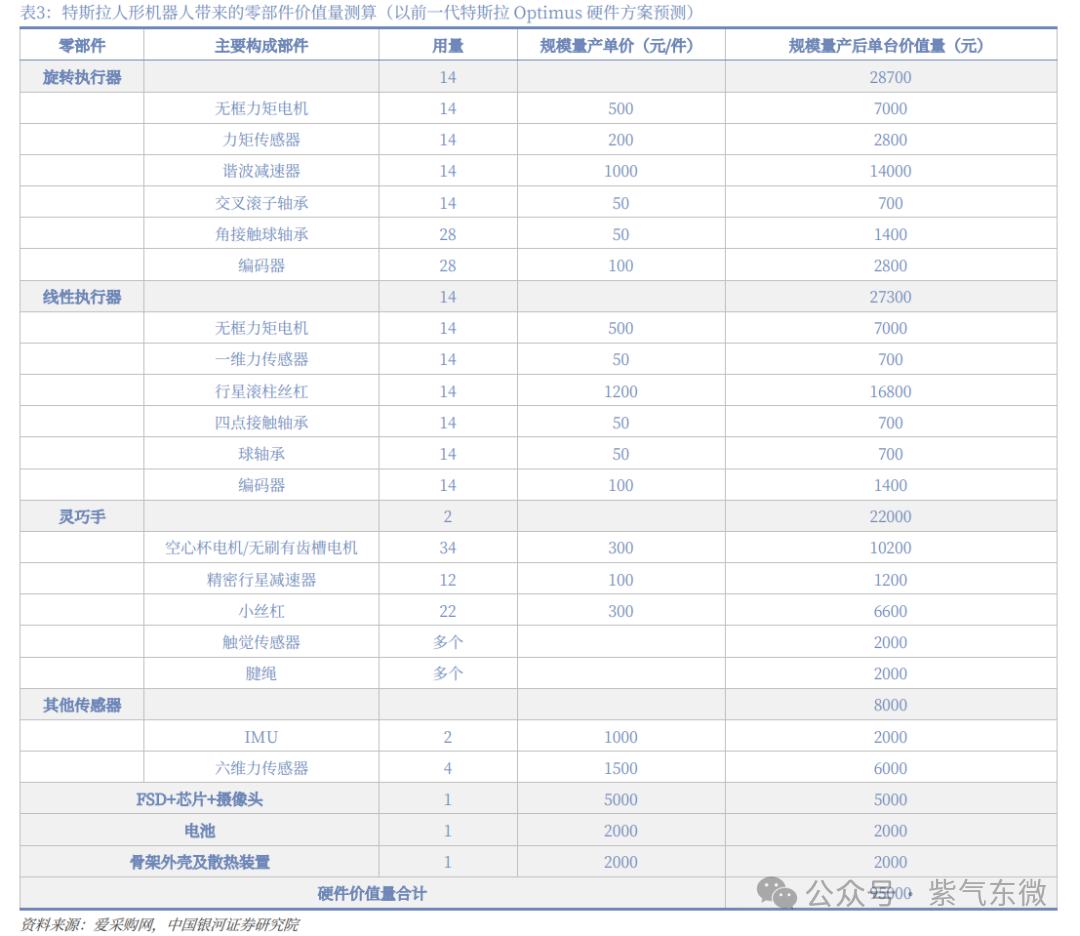

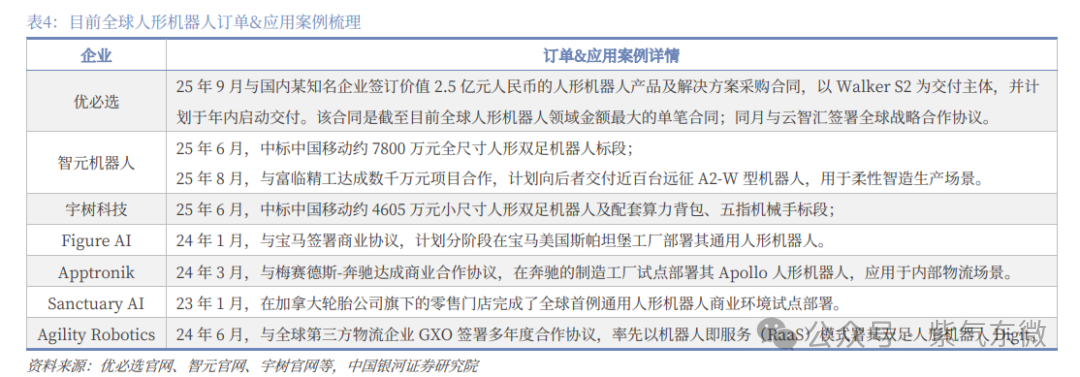

The core value of embodied intelligence is to promote the large-scale commercialization and industrialization of AI. Embodied intelligence is widely penetrating industries such as manufacturing, logistics, healthcare, transportation, and energy, driving efficiency and model reconstruction, bringing more opportunities for industrial landing. Its tangible products include but are not limited to various robots, smart cars, etc. Huawei predicts that embodied intelligence will be applied in three key industries: smart driving, smart robots, and low-altitude economy. IFR points out that AI and humanoid robots have become major trends in global robotics, with global professional service robot sales increasing by 30% in 2023, most of which possess varying degrees of intelligent features, and the commercialization potential is rapidly being released. Tesla’s Optimus leads the market, with orders supporting the expectation of a mass production year in 2025. Since the prototype was released in 2022, Tesla’s Optimus has undergone multiple iterations, and we expect to launch the V3 version by the end of 2025 and officially transition to mass production. Musk’s latest compensation plan indicates that Optimus aims for a shipment target of one million units in the next five years. Figure AI in the U.S. has reached trial agreements with BMW and others. Domestically, UBTECH has secured the world’s largest single order of 250 million yuan for the Walker S2 humanoid robot product and solution, with its Walker series contracts totaling nearly 400 million yuan; Yushu has partnered with Zhiyuan to win a 124 million yuan procurement project from a subsidiary of China Mobile. In the first half of 2025, over 83 humanoid robot projects have been publicly announced in China, with a total amount of nearly 330 million yuan. Driven by downstream orders, supply chain companies are rushing into core components such as precision reducers, servo motors, and sensors. In 2025, the global humanoid robot market is expected to officially reach a shipment volume of tens of thousands, with manufacturers racing to boost production capacity under the requirements of mass delivery, marking the industry’s entry into the mass production year.

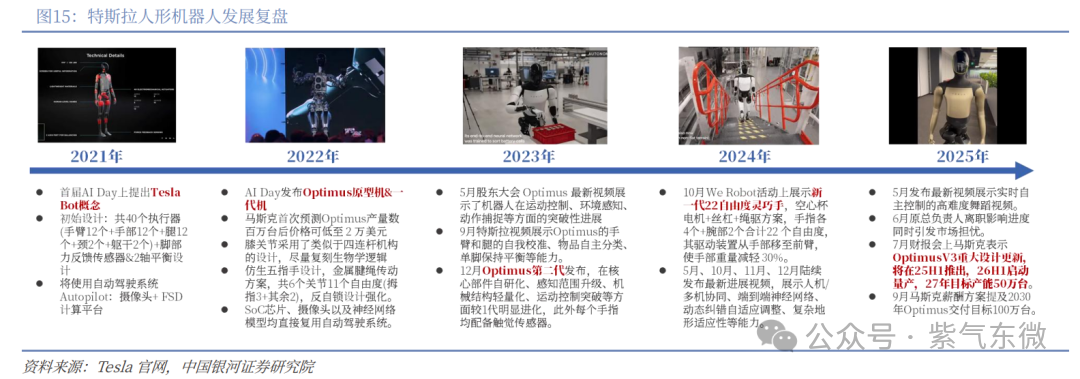

Tesla’s Optimus leads the market, with orders supporting the expectation of a mass production year in 2025. Since the prototype was released in 2022, Tesla’s Optimus has undergone multiple iterations, and we expect to launch the V3 version by the end of 2025 and officially transition to mass production. Musk’s latest compensation plan indicates that Optimus aims for a shipment target of one million units in the next five years. Figure AI in the U.S. has reached trial agreements with BMW and others. Domestically, UBTECH has secured the world’s largest single order of 250 million yuan for the Walker S2 humanoid robot product and solution, with its Walker series contracts totaling nearly 400 million yuan; Yushu has partnered with Zhiyuan to win a 124 million yuan procurement project from a subsidiary of China Mobile. In the first half of 2025, over 83 humanoid robot projects have been publicly announced in China, with a total amount of nearly 330 million yuan. Driven by downstream orders, supply chain companies are rushing into core components such as precision reducers, servo motors, and sensors. In 2025, the global humanoid robot market is expected to officially reach a shipment volume of tens of thousands, with manufacturers racing to boost production capacity under the requirements of mass delivery, marking the industry’s entry into the mass production year.

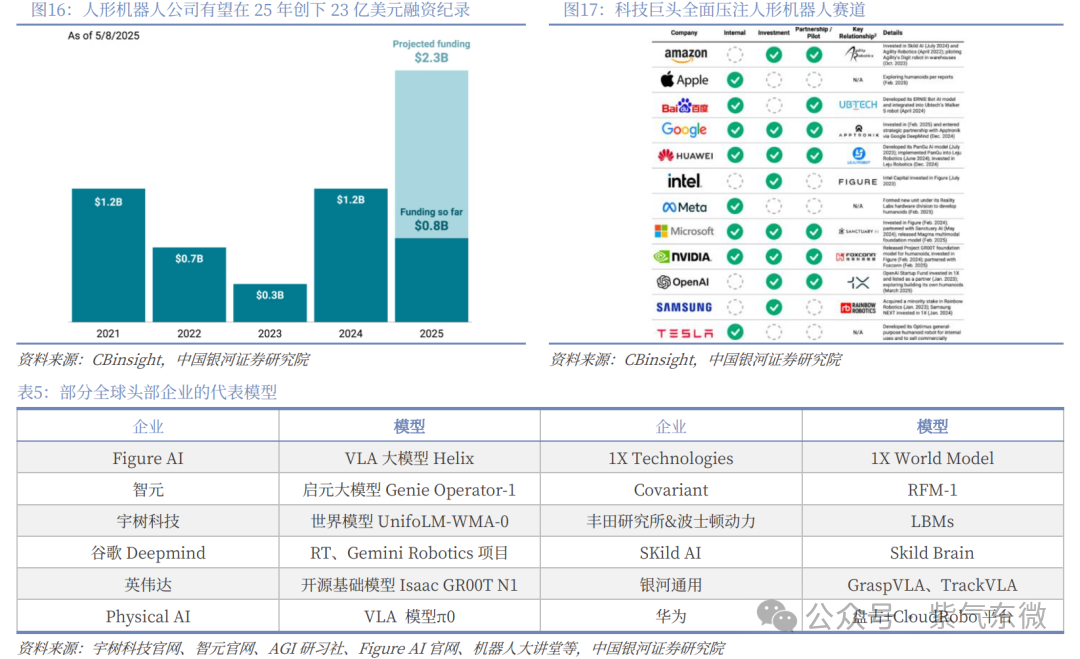

Algorithm models are breaking through, and capital is accelerating the process. Large language models represented by ChatGPT are the detonators of this round of AI revolution, and technology companies and startups are starting to fully exert their efforts on embodied intelligence models. As the new round of technological revolution begins, capital is quickly following up, such as Figure announcing over $1 billion in Series C financing in September 2025, with a valuation of approximately $39 billion after just three years. CBinsight predicts that global robotics company financing will reach $2.3 billion in 2025. From a directional perspective, we believe that the “brain” model capability is hotter than hardware solutions and will become the decisive factor in future competition. Technology companies have a certain first-mover advantage, and startups are also leveraging innovation under capital support to embark on a plan for a curve overtaking, entering the fast lane of overall development in embodied intelligence. Embodied intelligence is expected to reshape the landscape. Due to limitations such as market positioning, traditional robot companies, while experienced in high precision and efficient execution of repetitive tasks, lack accumulation in intelligent models and algorithms; in contrast, leading technology companies and startups can leverage mature supply chains to make up for hardware shortcomings and achieve a latecomer advantage, potentially reshaping the competitive landscape of embodied intelligence with a new logic.

Algorithm models are breaking through, and capital is accelerating the process. Large language models represented by ChatGPT are the detonators of this round of AI revolution, and technology companies and startups are starting to fully exert their efforts on embodied intelligence models. As the new round of technological revolution begins, capital is quickly following up, such as Figure announcing over $1 billion in Series C financing in September 2025, with a valuation of approximately $39 billion after just three years. CBinsight predicts that global robotics company financing will reach $2.3 billion in 2025. From a directional perspective, we believe that the “brain” model capability is hotter than hardware solutions and will become the decisive factor in future competition. Technology companies have a certain first-mover advantage, and startups are also leveraging innovation under capital support to embark on a plan for a curve overtaking, entering the fast lane of overall development in embodied intelligence. Embodied intelligence is expected to reshape the landscape. Due to limitations such as market positioning, traditional robot companies, while experienced in high precision and efficient execution of repetitive tasks, lack accumulation in intelligent models and algorithms; in contrast, leading technology companies and startups can leverage mature supply chains to make up for hardware shortcomings and achieve a latecomer advantage, potentially reshaping the competitive landscape of embodied intelligence with a new logic. 2. Embodied China: Policies, Markets, and Supply Chains Working Together The “14th Five-Year Plan” period is a critical juncture under multiple historical intersections. In the historical context of “two changes and one leap,” the “14th Five-Year Plan” comprehensively promotes high-quality development to accelerate the process of Chinese-style modernization based on the organic unity of “new development stage, new development concept, and new development pattern.” At this opportune moment, embodied intelligence will also usher in a critical leap from the laboratory to mass production, from scientific research to practical production and life. China has formed certain leading advantages in policies, markets, and supply chains, but in some areas, especially in top models’ discourse power and core fields such as high-end chips, there is still a gap between us and global leading players. The “14th Five-Year Plan” will further elevate embodied intelligence as a core track supporting the strategy of a manufacturing powerhouse and digital China, achieving a strategic upgrade from “basic layout and ecological cultivation” to “core breakthroughs and integrated empowerment,” creating a “Embodied China” development model, injecting new productive forces into the high-quality development of the economy and society during the “14th Five-Year Plan” period, and reshaping the global competitive landscape of the intelligent industry. Under policy guidance, China has achieved remarkable results in developing emerging industries. China’s policies set direction, and the experience of “government-enterprise cooperation to accomplish major tasks” is rich. The policy determination, execution, and planning capabilities constitute the foundation of China’s national-level operating system. The top-level design of strategic emerging industries emphasizes clear goals, path decomposition, and responsibility implementation, with the ability to coordinate across departments and conduct pilot projects in different regions, transforming uncertain frontier technologies into feasible engineering routes. Based on the experiences of the “13th Five-Year Plan” and “14th Five-Year Plan,” China’s new energy vehicle industry, digital infrastructure construction, and “dual carbon” strategy have achieved significant results: by 2024, China’s new energy vehicle production and sales are expected to reach 12.89 million and 12.87 million units, with an electrification rate of 41%, maintaining the global first position for ten consecutive years; by the end of 2024, there will be 4.25 million 5G base stations, accounting for 34%, far ahead of the world; by the end of 2024, the cumulative installed capacity of photovoltaic power generation will reach 886GW, with a CAGR of 40% from the “13th Five-Year Plan” to now. Embodied intelligence will become a “must-answer question.” We are currently in the “fourth industrial revolution” led by artificial intelligence, which is an acceleration period of a new round of technological revolution and industrial transformation. Artificial intelligence is a key force shaping the competitiveness of major countries, and embodied intelligence, as the “pearl on the crown” of artificial intelligence, is expected to be a “must-answer question” for policy planning. Once the programmatic policies are established, the pace of industrial development will enter the fast lane, continuously releasing strong growth dividends, and related sectors are expected to become the core main line.

2. Embodied China: Policies, Markets, and Supply Chains Working Together The “14th Five-Year Plan” period is a critical juncture under multiple historical intersections. In the historical context of “two changes and one leap,” the “14th Five-Year Plan” comprehensively promotes high-quality development to accelerate the process of Chinese-style modernization based on the organic unity of “new development stage, new development concept, and new development pattern.” At this opportune moment, embodied intelligence will also usher in a critical leap from the laboratory to mass production, from scientific research to practical production and life. China has formed certain leading advantages in policies, markets, and supply chains, but in some areas, especially in top models’ discourse power and core fields such as high-end chips, there is still a gap between us and global leading players. The “14th Five-Year Plan” will further elevate embodied intelligence as a core track supporting the strategy of a manufacturing powerhouse and digital China, achieving a strategic upgrade from “basic layout and ecological cultivation” to “core breakthroughs and integrated empowerment,” creating a “Embodied China” development model, injecting new productive forces into the high-quality development of the economy and society during the “14th Five-Year Plan” period, and reshaping the global competitive landscape of the intelligent industry. Under policy guidance, China has achieved remarkable results in developing emerging industries. China’s policies set direction, and the experience of “government-enterprise cooperation to accomplish major tasks” is rich. The policy determination, execution, and planning capabilities constitute the foundation of China’s national-level operating system. The top-level design of strategic emerging industries emphasizes clear goals, path decomposition, and responsibility implementation, with the ability to coordinate across departments and conduct pilot projects in different regions, transforming uncertain frontier technologies into feasible engineering routes. Based on the experiences of the “13th Five-Year Plan” and “14th Five-Year Plan,” China’s new energy vehicle industry, digital infrastructure construction, and “dual carbon” strategy have achieved significant results: by 2024, China’s new energy vehicle production and sales are expected to reach 12.89 million and 12.87 million units, with an electrification rate of 41%, maintaining the global first position for ten consecutive years; by the end of 2024, there will be 4.25 million 5G base stations, accounting for 34%, far ahead of the world; by the end of 2024, the cumulative installed capacity of photovoltaic power generation will reach 886GW, with a CAGR of 40% from the “13th Five-Year Plan” to now. Embodied intelligence will become a “must-answer question.” We are currently in the “fourth industrial revolution” led by artificial intelligence, which is an acceleration period of a new round of technological revolution and industrial transformation. Artificial intelligence is a key force shaping the competitiveness of major countries, and embodied intelligence, as the “pearl on the crown” of artificial intelligence, is expected to be a “must-answer question” for policy planning. Once the programmatic policies are established, the pace of industrial development will enter the fast lane, continuously releasing strong growth dividends, and related sectors are expected to become the core main line.

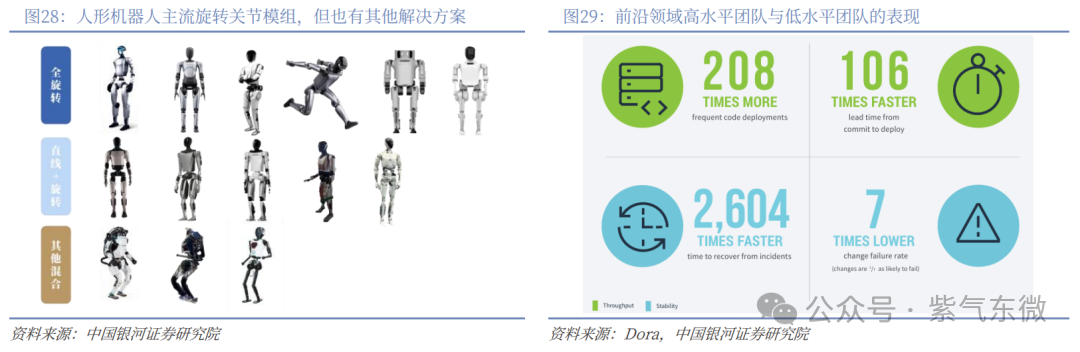

The demand for industrial and service robots is rapidly rising, and embodied intelligent robots have broad replacement and application scenario expansion space. According to data from the National Bureau of Statistics, from January to July 2025, China’s industrial robot output was 447,000 units, a year-on-year increase of 43.6%, and service robot output was 1.038 million units, a year-on-year increase of 80.4%. The market demand is rapidly rising, and the robot market is in a phase of rapid expansion. Compared to traditional robots, embodied intelligent robots have a higher level of intelligence, can undertake more complex work tasks, and have a wider range of application scenarios, not only capable of replacing traditional robots in industrial and service scenarios but also expected to expand application scenarios, with a broad market prospect. The mature development of embodied intelligence technology can enhance production efficiency, optimize life experiences, and reduce safety accidents, with ample market demand for improvement. In industrial scenarios, embodied intelligent robots have advantages over humans in terms of working hours and operational precision, which can improve production efficiency and reduce the threat of industrial accidents to personal safety; in service scenarios, the use of embodied intelligent robots can enhance the convenience of life and optimize life experiences; in transportation scenarios, taking intelligent assisted driving as an example, it can not only reduce driver fatigue but also enhance driving safety. According to Tesla’s vehicle safety report, the average mileage of collision accidents when using assisted driving features is over 500 miles, far higher than the non-assisted driving scenarios (around 100 miles), significantly improving vehicle driving safety. The products of embodied intelligence are diverse, and the difficulty of rapid iteration is high. Depending on the different downstream application industries and landing scenarios, as well as the divergence of technical routes, embodied intelligence has a very diverse product form, with differences in hardware performance, size, and cost. After scaling, it also requires that standardized key components be easily available, interchangeable, or even expandable. This diversified demand forces the supply chain to possess high flexibility, capable of providing customized core components in the early stage and achieving rapid mass production. Comprehensive development must rely on a mature industrial system to be realized. On the other hand, the design and development of high-end technology products often mean high frequency and efficient iteration. Dora’s research indicates that the iteration frequency of high-level technology service teams is 208 times that of low-level teams; currently, there is no unified technical route available for humanoid robots globally, and leading host companies often experience frequent trial and error and plan modifications during product development. In the future, during the iteration phase after finalization, there will also be high-frequency feedback of details and requirements to suppliers, which will pose significant challenges to the technical level and timely adjustment capabilities of the supply chain.

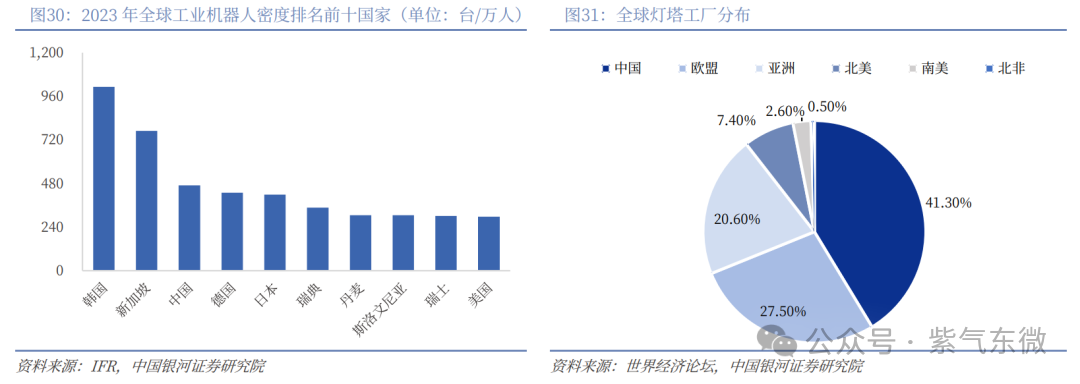

The demand for industrial and service robots is rapidly rising, and embodied intelligent robots have broad replacement and application scenario expansion space. According to data from the National Bureau of Statistics, from January to July 2025, China’s industrial robot output was 447,000 units, a year-on-year increase of 43.6%, and service robot output was 1.038 million units, a year-on-year increase of 80.4%. The market demand is rapidly rising, and the robot market is in a phase of rapid expansion. Compared to traditional robots, embodied intelligent robots have a higher level of intelligence, can undertake more complex work tasks, and have a wider range of application scenarios, not only capable of replacing traditional robots in industrial and service scenarios but also expected to expand application scenarios, with a broad market prospect. The mature development of embodied intelligence technology can enhance production efficiency, optimize life experiences, and reduce safety accidents, with ample market demand for improvement. In industrial scenarios, embodied intelligent robots have advantages over humans in terms of working hours and operational precision, which can improve production efficiency and reduce the threat of industrial accidents to personal safety; in service scenarios, the use of embodied intelligent robots can enhance the convenience of life and optimize life experiences; in transportation scenarios, taking intelligent assisted driving as an example, it can not only reduce driver fatigue but also enhance driving safety. According to Tesla’s vehicle safety report, the average mileage of collision accidents when using assisted driving features is over 500 miles, far higher than the non-assisted driving scenarios (around 100 miles), significantly improving vehicle driving safety. The products of embodied intelligence are diverse, and the difficulty of rapid iteration is high. Depending on the different downstream application industries and landing scenarios, as well as the divergence of technical routes, embodied intelligence has a very diverse product form, with differences in hardware performance, size, and cost. After scaling, it also requires that standardized key components be easily available, interchangeable, or even expandable. This diversified demand forces the supply chain to possess high flexibility, capable of providing customized core components in the early stage and achieving rapid mass production. Comprehensive development must rely on a mature industrial system to be realized. On the other hand, the design and development of high-end technology products often mean high frequency and efficient iteration. Dora’s research indicates that the iteration frequency of high-level technology service teams is 208 times that of low-level teams; currently, there is no unified technical route available for humanoid robots globally, and leading host companies often experience frequent trial and error and plan modifications during product development. In the future, during the iteration phase after finalization, there will also be high-frequency feedback of details and requirements to suppliers, which will pose significant challenges to the technical level and timely adjustment capabilities of the supply chain. China’s high-end manufacturing, strong industrial strength, and complete supply chain safeguard the development of embodied intelligence. China is the only country in the world that has all industrial categories listed by the United Nations ISIC, allowing complete machine manufacturers to achieve closed-loop collaboration from materials, components to system integration in the same domestic market. In addition, after digital and automated upgrades, Chinese manufacturing has represented the leading level of global high-end manufacturing, with a manufacturing robot density of 470 units per 10,000 people in 2023, ranking third globally; 41% of the 201 global lighthouse factories are located in China, ranking first; and in 2023, China ranked second in the UNIDO’s CIP index, being at the forefront of the world in terms of technological complexity and global manufacturing influence.

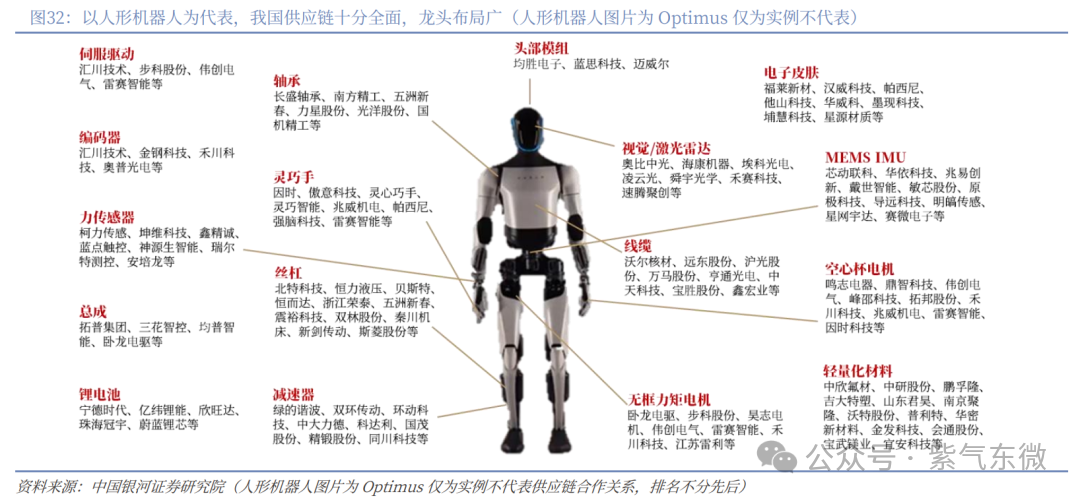

China’s high-end manufacturing, strong industrial strength, and complete supply chain safeguard the development of embodied intelligence. China is the only country in the world that has all industrial categories listed by the United Nations ISIC, allowing complete machine manufacturers to achieve closed-loop collaboration from materials, components to system integration in the same domestic market. In addition, after digital and automated upgrades, Chinese manufacturing has represented the leading level of global high-end manufacturing, with a manufacturing robot density of 470 units per 10,000 people in 2023, ranking third globally; 41% of the 201 global lighthouse factories are located in China, ranking first; and in 2023, China ranked second in the UNIDO’s CIP index, being at the forefront of the world in terms of technological complexity and global manufacturing influence. In the field of humanoid robots, we believe that China’s supply chain has obvious leading capabilities: 1) In the upstream raw material sector, high-performance motors rely on resources such as rare earth permanent magnets, with China holding 40% of global resource reserves and 92% of smelting and separation capacity; 2) In the midstream component manufacturing sector, benefiting from the development achievements of other mature industries with strong technological homogeneity (the automotive industry being the most typical), the domestic supply chain layout is very comprehensive, with leading suppliers for high power density motors, harmonic/planetary reducers, modules, six-dimensional torque and IMU/depth cameras, and high specific energy batteries, all having high localization rates, enabling rapid prototyping of products; in addition, large-scale mass production has accumulated rich engineering and production management experience, laying a foundation for subsequent cost reduction and forming a significant cost-performance advantage, thus accelerating application expansion. Looking ahead, close cooperation with host manufacturers, strong technical strength, and rich experience in mass production are the three core basic elements for component companies to compete.

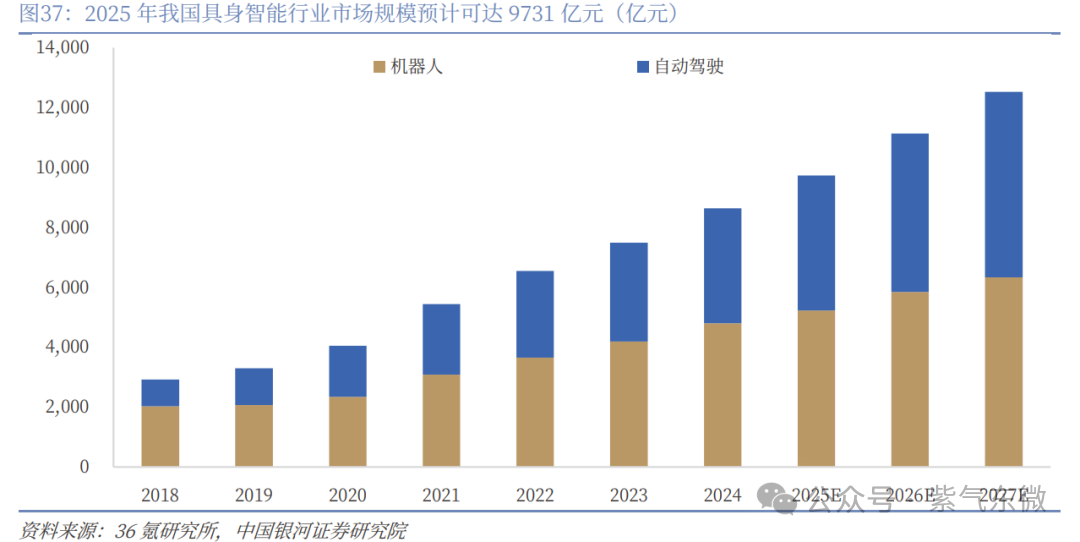

In the field of humanoid robots, we believe that China’s supply chain has obvious leading capabilities: 1) In the upstream raw material sector, high-performance motors rely on resources such as rare earth permanent magnets, with China holding 40% of global resource reserves and 92% of smelting and separation capacity; 2) In the midstream component manufacturing sector, benefiting from the development achievements of other mature industries with strong technological homogeneity (the automotive industry being the most typical), the domestic supply chain layout is very comprehensive, with leading suppliers for high power density motors, harmonic/planetary reducers, modules, six-dimensional torque and IMU/depth cameras, and high specific energy batteries, all having high localization rates, enabling rapid prototyping of products; in addition, large-scale mass production has accumulated rich engineering and production management experience, laying a foundation for subsequent cost reduction and forming a significant cost-performance advantage, thus accelerating application expansion. Looking ahead, close cooperation with host manufacturers, strong technical strength, and rich experience in mass production are the three core basic elements for component companies to compete.  3. Rapid Growth of Market Size, Continuous Expansion of Application Scenarios The market size of embodied intelligence is rapidly expanding, with a promising future, expected to exceed one trillion yuan by 2026. Since 2025, the market size of embodied intelligence has rapidly expanded. Wang Xingxing, founder of Yushu Technology, stated at the 2025 World Artificial Intelligence Conference that “the average growth rate of the national intelligent robot industry in the first half of this year can reach 50% to 100%.” According to 36Kr Research Institute, the market size of China’s embodied intelligence industry is expected to reach 973.1 billion yuan by 2025, with the robot market size expected to reach 522.9 billion yuan, a year-on-year increase of 8.9%, and the autonomous driving market size expected to reach 450.2 billion yuan, a year-on-year increase of 17.5%. By 2026, the market size of China’s embodied intelligence industry is expected to exceed one trillion yuan.

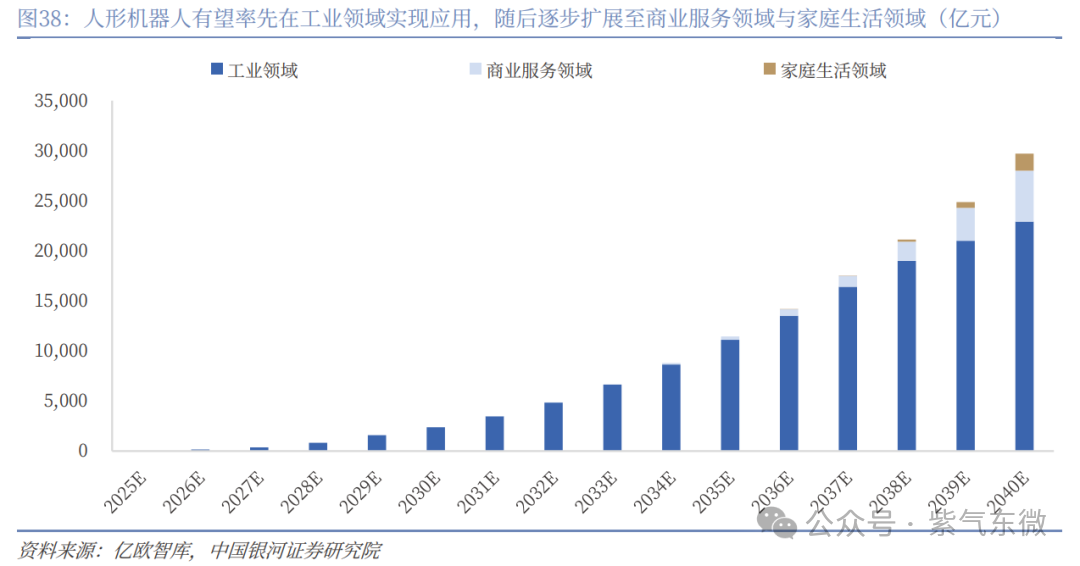

3. Rapid Growth of Market Size, Continuous Expansion of Application Scenarios The market size of embodied intelligence is rapidly expanding, with a promising future, expected to exceed one trillion yuan by 2026. Since 2025, the market size of embodied intelligence has rapidly expanded. Wang Xingxing, founder of Yushu Technology, stated at the 2025 World Artificial Intelligence Conference that “the average growth rate of the national intelligent robot industry in the first half of this year can reach 50% to 100%.” According to 36Kr Research Institute, the market size of China’s embodied intelligence industry is expected to reach 973.1 billion yuan by 2025, with the robot market size expected to reach 522.9 billion yuan, a year-on-year increase of 8.9%, and the autonomous driving market size expected to reach 450.2 billion yuan, a year-on-year increase of 17.5%. By 2026, the market size of China’s embodied intelligence industry is expected to exceed one trillion yuan. Humanoid robots are expected to first achieve applications in the industrial field, gradually expanding to commercial service and household life fields. Industrial scenarios have a high degree of standardization and repetition in work steps, and the relatively closed nature of the scenarios helps humanoid robot products to land in early applications. According to EEO Intelligence, from 2025 to 2030, humanoid robots are expected to first be applied in the industrial field, and after 2030, humanoid robots will gradually be applied in commercial service fields, and after 2035, humanoid robots will gradually be applied in household life fields, with the market size of humanoid robots expected to reach nearly three trillion yuan by 2040.

Humanoid robots are expected to first achieve applications in the industrial field, gradually expanding to commercial service and household life fields. Industrial scenarios have a high degree of standardization and repetition in work steps, and the relatively closed nature of the scenarios helps humanoid robot products to land in early applications. According to EEO Intelligence, from 2025 to 2030, humanoid robots are expected to first be applied in the industrial field, and after 2030, humanoid robots will gradually be applied in commercial service fields, and after 2035, humanoid robots will gradually be applied in household life fields, with the market size of humanoid robots expected to reach nearly three trillion yuan by 2040. The application prospects of humanoid robots in industrial scenarios are broad. The demand for automation and intelligence in the industrial sector is high, with complex production processes and high requirements for efficiency, precision, and flexibility, as well as many dangerous scenarios. The application of humanoid robots can achieve efficiency improvements and reduce safety accidents, thus there is a high demand for humanoid robots. Humanoid robots can be applied in multiple production links across various industries such as automotive, electronics, chemicals, machinery manufacturing, textiles, and food and beverage, possessing broad application prospects.

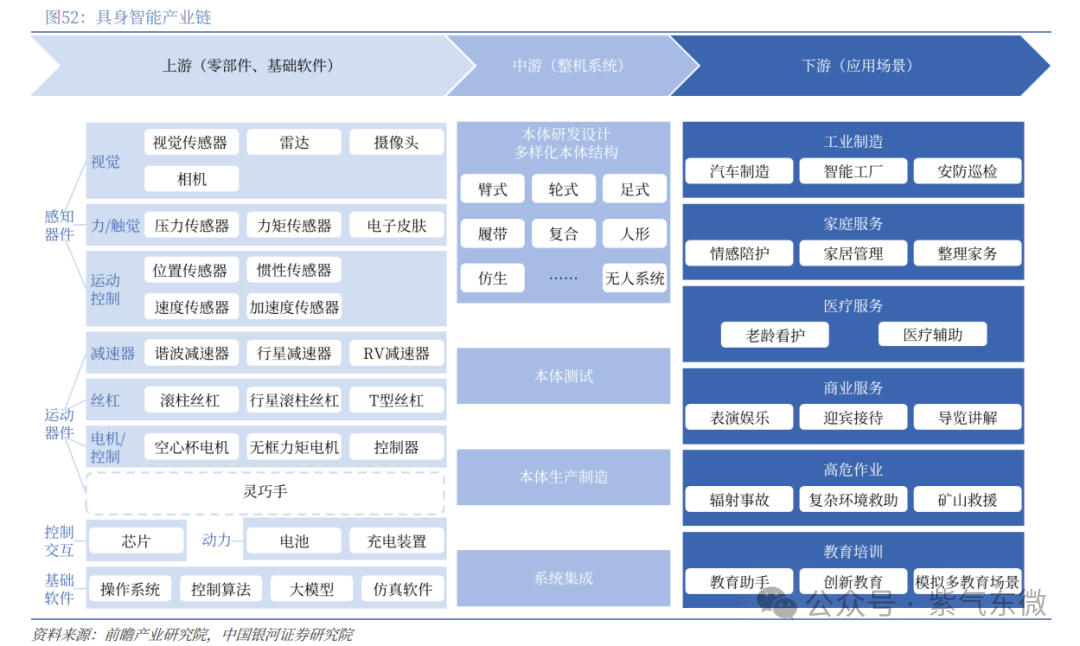

The application prospects of humanoid robots in industrial scenarios are broad. The demand for automation and intelligence in the industrial sector is high, with complex production processes and high requirements for efficiency, precision, and flexibility, as well as many dangerous scenarios. The application of humanoid robots can achieve efficiency improvements and reduce safety accidents, thus there is a high demand for humanoid robots. Humanoid robots can be applied in multiple production links across various industries such as automotive, electronics, chemicals, machinery manufacturing, textiles, and food and beverage, possessing broad application prospects. Many leading companies have deployed humanoid robot products in automotive factories, accelerating the practical application of humanoid robots in industrial scenarios. Currently, several companies have deployed humanoid robot products in industrial scenarios represented by automotive factories, promoting the acceleration of practical applications of humanoid robots, such as Tesla’s Optimus entering its own factory to perform battery unit disassembly work; Figure 02 has increased speed by 400% and success rate by seven times after practicing on BMW’s production line; UBTECH has collaborated with well-known companies such as Dongfeng Liuzhou Automobile, Geely, FAW-Volkswagen Qingdao Branch, Audi FAW, BYD, BAIC New Energy, Foxconn, and Shunfeng to promote its industrial humanoid robot Walker S series into factory “training” and has deployed dozens of Walker S1 in the Zeekr 5G smart factory, attempting to undertake collaborative work such as sorting, transporting, and assembling under the command of the same unified “brain.” Humanoid robots are expected to be applied in last-mile delivery scenarios in logistics, solving the “last 10 meters” problem. Unmanned transport logistics vehicles can complete the task of transporting goods from the distribution point to the outlet, while the delivery task from the outlet to the end consumer is still mainly completed by delivery personnel. The industry is actively exploring the use of humanoid robot products to solve the “last 10 meters” problem, such as the industry’s first 5G-A embodied intelligent robot “Kua Fu” jointly released by Leju, Huawei, and China Mobile, which can cooperate with drones to receive items delivered by drones and complete ground transfer. Once the technology matures, it is expected to replace some delivery personnel’s work. 4. Collaborative Development of Upstream and Downstream, Promoting Progress in the Embodied Intelligence Industry The embodied intelligence industry chain covers multiple links, with upstream including components and basic software, midstream including whole machine system research and design, body testing, production, and system integration, and downstream covering research and education, commercial services, industrial manufacturing, high-risk operations, healthcare, and household services. Among them, upstream components can be divided into perception devices (such as vision, force/torque, tactile and other sensors), motion devices (such as motors/controllers, reducers, screws, etc.), and control interaction (such as chips, power systems, etc.); basic software includes operating systems, control algorithms, large models, and simulation software, etc. Midstream embodied intelligent robots have diverse body structures, including arm-type/wheeled/footed/tracked/composite/humanoid/bionic and other unmanned systems, among which humanoids, with their higher anthropomorphism, stronger interactivity, and adaptability to the environment, have become the most focused form.

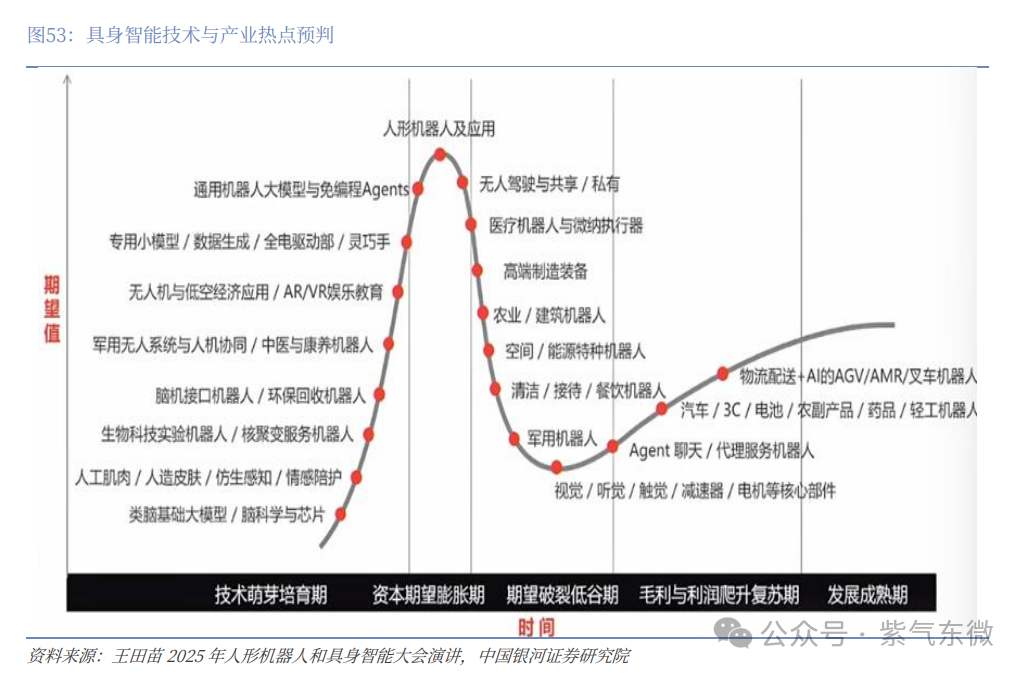

Many leading companies have deployed humanoid robot products in automotive factories, accelerating the practical application of humanoid robots in industrial scenarios. Currently, several companies have deployed humanoid robot products in industrial scenarios represented by automotive factories, promoting the acceleration of practical applications of humanoid robots, such as Tesla’s Optimus entering its own factory to perform battery unit disassembly work; Figure 02 has increased speed by 400% and success rate by seven times after practicing on BMW’s production line; UBTECH has collaborated with well-known companies such as Dongfeng Liuzhou Automobile, Geely, FAW-Volkswagen Qingdao Branch, Audi FAW, BYD, BAIC New Energy, Foxconn, and Shunfeng to promote its industrial humanoid robot Walker S series into factory “training” and has deployed dozens of Walker S1 in the Zeekr 5G smart factory, attempting to undertake collaborative work such as sorting, transporting, and assembling under the command of the same unified “brain.” Humanoid robots are expected to be applied in last-mile delivery scenarios in logistics, solving the “last 10 meters” problem. Unmanned transport logistics vehicles can complete the task of transporting goods from the distribution point to the outlet, while the delivery task from the outlet to the end consumer is still mainly completed by delivery personnel. The industry is actively exploring the use of humanoid robot products to solve the “last 10 meters” problem, such as the industry’s first 5G-A embodied intelligent robot “Kua Fu” jointly released by Leju, Huawei, and China Mobile, which can cooperate with drones to receive items delivered by drones and complete ground transfer. Once the technology matures, it is expected to replace some delivery personnel’s work. 4. Collaborative Development of Upstream and Downstream, Promoting Progress in the Embodied Intelligence Industry The embodied intelligence industry chain covers multiple links, with upstream including components and basic software, midstream including whole machine system research and design, body testing, production, and system integration, and downstream covering research and education, commercial services, industrial manufacturing, high-risk operations, healthcare, and household services. Among them, upstream components can be divided into perception devices (such as vision, force/torque, tactile and other sensors), motion devices (such as motors/controllers, reducers, screws, etc.), and control interaction (such as chips, power systems, etc.); basic software includes operating systems, control algorithms, large models, and simulation software, etc. Midstream embodied intelligent robots have diverse body structures, including arm-type/wheeled/footed/tracked/composite/humanoid/bionic and other unmanned systems, among which humanoids, with their higher anthropomorphism, stronger interactivity, and adaptability to the environment, have become the most focused form. From the perspective of technology and industry hotspots, the application of humanoid robots is currently in a period of capital expectation expansion, while components are waiting to rebound from a low expectation valley. 2025 is the year of mass production for humanoid robots, with technology and industrial development needs, as well as policy directions supporting the landing of application scenarios, accumulating data to feed back product iterations. The current core bottleneck in industrial development lies in the embodied large model, with key issues in data bottlenecks and model architecture exploration. Unlike products such as smart cars, AGV/AMR, and quadruped robots, the operational importance of humanoid robots has significantly increased, with multi-finger dexterous hand design (including tactile sensor research), dexterous operation datasets, and operational large models becoming key to enhancing functionality. The small shipment volume currently limits the scale effect of component production, requiring significant financial strength from component companies due to high R&D investment and low current revenue, while the rapid increase in participants has intensified industry competition. However, as mass production approaches, component manufacturers with quality large customer resources and strong mass production capabilities, or OEMs with outstanding manufacturing capabilities and comprehensive professional support for startups are expected to stand out.

From the perspective of technology and industry hotspots, the application of humanoid robots is currently in a period of capital expectation expansion, while components are waiting to rebound from a low expectation valley. 2025 is the year of mass production for humanoid robots, with technology and industrial development needs, as well as policy directions supporting the landing of application scenarios, accumulating data to feed back product iterations. The current core bottleneck in industrial development lies in the embodied large model, with key issues in data bottlenecks and model architecture exploration. Unlike products such as smart cars, AGV/AMR, and quadruped robots, the operational importance of humanoid robots has significantly increased, with multi-finger dexterous hand design (including tactile sensor research), dexterous operation datasets, and operational large models becoming key to enhancing functionality. The small shipment volume currently limits the scale effect of component production, requiring significant financial strength from component companies due to high R&D investment and low current revenue, while the rapid increase in participants has intensified industry competition. However, as mass production approaches, component manufacturers with quality large customer resources and strong mass production capabilities, or OEMs with outstanding manufacturing capabilities and comprehensive professional support for startups are expected to stand out. Currently, humanoid robot manufacturers are flourishing, and we roughly categorize the main participants into five categories: 1) Startups: Fast product iteration speed. This category can be further subdivided: the first type, robot companies, based on humanoid robots and other robotic products with technological homogeneity, have advantages in mechanical structure design and control. For example, Fourier Intelligence, Yushu Technology. The second type, founders or key executives with backgrounds in the internet/intelligent driving, have a certain sensitivity in using model algorithms, such as overseas Figure AI, 1X Technologies, and domestic Zhiyuan Robotics. The third type, other startups, such as UBTECH, Kepler Robotics, Leju Robotics, etc. 2) Automotive manufacturers: Have advantages in technology, scenarios, and supply chains. Technical advantages are reflected in algorithms and precision manufacturing, scenario advantages are reflected in B2B factory training and data collection, and supply advantages are reflected in the overlap of humanoid robots and electric vehicle components, making it more efficient for car manufacturers to choose familiar integrators and component suppliers. For example, Tesla, Xiaopeng, GAC Group, Seres. 3) Consumer electronics companies: 3C supply chain companies have strong capabilities in large-scale mass production quality and cost control, with accumulated experience in assembly and OEM, such as Lens Technology, Lingyi Technology, etc. 3C brand manufacturers have better product promotion capabilities in B2C scenarios, especially in household service scenarios, such as Xiaomi, APPLE, etc. 4) Research institutions/innovation centers: Have R&D experience and financial support. For example, Galaxy General Robotics, Star Motion Era, etc. 5) Other technology/internet giants: Currently, humanoid robots have become one of the consensus directions for technology/internet giants at home and abroad. With strong technology, capital, and talent strength, Tencent has previously attempted to launch a humanoid robot “Xiao Wu,” and ByteDance is also accelerating its layout, becoming a strong potential competitor. Beyond the body, technology/internet giants are currently more involved in the humanoid robot industry through investment + self-research large models, such as Alibaba & Ant investing in Yushu, Xinghai Map, Zhujidongli, etc.; Tencent investing in Yushu and Zhiyuan; Meituan investing in Yushu, Galaxy General, Xinghai Map, etc., laying out in fields such as medical delivery, unmanned retail, and low-altitude; JD investing in Qianxun Intelligent, Zhongqing Robotics, Zhujidongli, etc., in conjunction with its JoyAI large model and JoyScale AI computing power platform, serving the company’s logistics, warehousing, and other supply chain scenarios. 5. Companies Actively Layout, Market Competition Gradually Intensifies Dexterous hands: Currently, the technology in the dexterous hand field has not yet converged, with both self-research and third-party suppliers developing simultaneously, leading to increasing competition. The former includes Zhiyuan Robotics, Yushu Technology, Star Motion Era, Magic Atom, and Zhongke Huiling (Lingbao CASBOT), while the latter has also differentiated into different characteristics, such as Qiangna Intelligent and Aoyi Technology entering the robot dexterous hand from brain-machine interfaces, while Shiji, Pashini, Daming, Realtime Robotics, and Zhaowei Electromechanical provide not only complete hands but also internal components. Pashini and Dexterous Intelligence provide not only hardware hands but also launch data collection factories and operational datasets, while Lingchu Intelligent and Zhongke Silicon Technology combine AI operational algorithms with hardware dexterous hands. Motors: Frameless torque motors have an overseas first-mover advantage. The top three in the domestic market are Hota Technology (18%), Dazhuo Motors (15%), and Boke Co. (8%), with Hota and Dazhuo being mainstream collaborative robot suppliers in China. Hollow cup motors have a global CR3 > 50%, mainly foreign, such as Swiss MAXON, German FAULHABER, and Swiss PORTESCAP, with advantages in winding design and winding process accumulation, and advanced winding equipment self-researched and manufactured. Domestic Mingzhi Electric, Dingzhi Technology, Tuobang Co., Weichuang Electric, and Zhaowei Electromechanical are also committed to domestic substitution, among which Mingzhi Electric has independent patents for hollow cup windings, a complete product line, and product performance close to foreign levels, making it one of the leading domestic hollow cup motor manufacturers. Axial flux motors have a global CR3 of about 84%, with domestic manufacturers Hub Power being one of the leaders. According to QY research, the core manufacturers of axial flux motors YASA, Hub Power, and Naxatra Labs account for about 84% of the global market share. Regionally, Europe/Asia-Pacific/North America account for about 48%/32%/15% respectively. Screws: High-end ball screws are mainly overseas, while the mid-end market is dominated by Taiwanese and mainland companies, and the low-end market is mainly by mainland manufacturers. According to Huajing Industry Research Institute, German Rexroth, Japanese THK, and NSK occupy 90%/30% of China’s high-end/mid-end ball screw market, with mainland Chinese manufacturers only accounting for 5%/30% of high-end/mid-end. Planetary roller screws are dominated by overseas manufacturers, with domestic manufacturers’ market share in 2022 totaling less than 20%. According to Wang Youxue’s research on the marketing strategy of E company’s roller screws, in the Chinese market in 2022, overseas leaders Rollvis, GSA, and Ewellix accounted for 26%, 26%, and 14% respectively, while domestic manufacturers accounted for 19% (of which Nanjing Technology accounted for 8%, and Bote Precision accounted for 8%). Participants in the humanoid robot screw market, in addition to traditional screw manufacturers such as Xinjian Transmission and Nanjing Technology, new entrants are mostly automotive parts manufacturers, as well as other mechanical equipment and industrial component suppliers (such as leading hydraulic parts manufacturers Hengli Hydraulic and bearing manufacturers Wuzhou Xinchun). The former has a relatively high homogeneity in production processes between automotive parts and screws, possessing low-cost industrialization production experience and automotive customer resources. The latter is based on precision processing technology accumulation and mass production capabilities. Looking ahead, close cooperation with host manufacturers, strong technical strength, and rich experience in mass production are the three core basic elements for component companies to compete. Reducers: Harmonic reducers are mainly Japanese, with Harmonic Drive’s global and Chinese market shares in 2023 at 85% and 40%, respectively. According to the research report from Guanyan, in 2023, Harmonic Drive’s global market share is 85%, while Green Harmonics accounts for 8%; in 2023, the CR3 and CR5 market shares of China’s harmonic reducer industry are 68% and 81%, respectively, with Harmonic Drive accounting for 40%, Green Harmonics for 18%, and Laifu Harmonics for 10%. Precision planetary reducers are mainly dominated by Japanese and German manufacturers, with domestic market shares of local manufacturers Kefeng Intelligent and Niusidate at 12% and 9% in 2022, respectively. According to QY research, the top three Japanese and German manufacturers, including Shinbo and German Weitenshtein and Nucat, accounted for 35% of the global market share in 2022. In the Chinese market in 2022, the top three were Japan’s Shinbo at 20%, Kefeng Intelligent at 12%, and Niusidate (Shandong) at 9%. Cycloidal reducers are dominated by Japanese manufacturers, but the pattern is not yet solidified, with some domestic gear manufacturers and RV reducer manufacturers attempting to develop cycloidal needle wheel reducer products suitable for humanoid robots. Six-dimensional force sensors: The global market is highly concentrated, with the top three being overseas leaders, accounting for over 50% of the market share in 2023. According to QY Research, in 2023, the top five manufacturers, ATI, Schunk, AMTI, Yuli Instruments, and Kistler, accounted for 36.2%, 8.2%, 8.0%, 4.3%, and 4.3% of the market share, respectively, with a CR5 of 61%; by category, strain gauge type accounts for 76.2%, with the rest mainly being piezoelectric/capacitive types. In 2023, the domestic market’s localization rate is about 30%. According to the China Business Industry Research Institute, in the domestic market in 2023, the CR5 is 50.5%, with the top three being ATI/Yuli Instruments/Epson, accounting for 22.4%, 12.2%, and 6.4%, respectively, while Landot Touch/Kunwei Technology/Xin Jingcheng accounted for 4.8%, 4.7%, and 2.2%. In 2024, in the Chinese humanoid robot six-dimensional force sensor market, Landot/Kunwei/Yuli/Xin Jingcheng/ATI are expected to account for 62%, 26%, 7%, 4%, and 1%, respectively (MIR). Flexible tactile sensors: The global market is dominated by North America and Europe. According to QY Research, in 2022, all of the top five manufacturers in the global market are overseas companies (Novasentis, Tekscan, Japan Display Inc., Baumer, Fraba), with a combined market share of about 57.1%. The domestic market is relatively fragmented, with different technology routes, such as resistive – Fulai New Materials/Huawei Technology, capacitive – Tashan Technology, visual tactile – Daming/Witai Robotics, electromagnetic Hall effect – Pashini, etc. Hanwei Technology has launched products in resistive/piezoelectric/capacitive/flexible sweat routes. Currently, most dexterous hands are equipped with resistive/capacitive sensors, with optional visual tactile/electromagnetic sensors. AI Chips: Nvidia holds an absolute dominance, with the localization rate continuously improving. In 2024, Nvidia’s global market share in AI chips is as high as 90% (Gartner), with advantages in process technology, architecture design, and software ecosystem. At the same time, the penetration rate of domestic AI chip brands is about 30%, doubling from last year (IDC), with companies like Horizon and Black Sesame Intelligence effectively reusing high-performance, high-reliability, automotive-grade chip technology from the intelligent automotive field in robotics, while Cambricon provides the cloud/edge computing power needed for training AI models and complex reasoning in robots. Embodied intelligence is the next wave of artificial intelligence development and will be one of the most important sectors under the “14th Five-Year Plan.” Among the representative industries of embodied intelligence, we particularly look forward to the alpha opportunities brought by the humanoid robot industry. The “14th Five-Year Plan” will be a critical period for humanoid robots to move towards mass production, and we recommend early in-depth layout around the entire industry chain: 1) Hosts: Several domestic host manufacturers have achieved remarkable results in mass production, forming clear main lines around key players such as T chain, F chain, Yushu chain, and Zhiyuan chain, while there are many potential players waiting to be explored. The form of robot bodies has not yet converged, and domestic host manufacturers are increasingly focusing on linear joints. We recommend layout directions such as ① leading enterprises with deep technical accumulation and good product ecological patterns; ② OEMs with outstanding manufacturing capabilities and specialized comprehensive support for startups. 2) Application scenarios: We believe this link is one of the biggest breakthrough points for the industrialization of embodied intelligence. The differentiation of application scenarios will also affect the technical route direction of various upstream players. Enterprises with strong landing capabilities are expected to dominate the industry chain and enjoy greater flexibility. Currently, scenarios are mainly concentrated in data collection, automotive industry, etc. In the short term, we are optimistic about the acceleration opportunities brought by special and hazardous fields, while in the long term, we are optimistic about the general fields such as large models that connect commercial and life services, while also paying attention to the premium space brought by some large-scale markets with strong qualification barriers. 3) Dexterous hands: This link accounts for a high cost of the host and directly affects the actual working ability of robots, making it a key link in the industrialization of embodied intelligence, with high attention in investment and financing. However, due to high technical bottlenecks in both hardware and software, as well as low return-cost ratios, there are also relatively large divergences, and the trend of routes has not yet converged, possessing both high growth potential and uncertainty. We believe that the current layout of dexterous hands should start from the core of downstream applications, with structural opportunities in various sub-materials, sensors, etc., and technological advantages being the biggest catalyst for company growth, focusing on areas with significant marginal changes such as electronic skin. 4) Components: Core components such as screws, reducers, motors, etc., have achieved breakthroughs in domestic production, but many new entrants have increased the competition intensity in the field, posing a risk of rapid intensification of competition. We believe that the current layout direction mainly focuses on leading enterprises, especially those at the head of the automotive industry chain, which have excellent large-scale product mass production and quality control capabilities. A mature supply chain system is conducive to rapid cost reduction and landing, while already having good relationships with host manufacturers, will continue to benefit from industrial development opportunities, becoming core participants in the embodied intelligence industry. The hardware OEM model is gradually emerging, and the division of research, production, and sales is beginning to explore. In the 1-100 mass production stage, the requirements for consistency and cost control of components will be enhanced, and the adoption of hardware OEM and host assembly models is expected to increase. 5) “Big and Small Brains”: Currently, the hardware barriers in the industry are decreasing, and the big and small brains are important shortcomings. The current technical routes for large models are still diverging, with VLA currently receiving high attention, and dual-system architectures such as Figure AI helix and Nvidia GR00T N1 are thriving. In terms of operational control, multiple solutions are merging and gradually converging. In addition, data is one of the core bottlenecks for achieving general embodied intelligence. Currently, robot experiential data can be directly used for strategy learning but is relatively scarce, while human data is abundant but requires repositioning or non-physical motion data, and the data quality may not be high. We believe that data training grounds and simulation solutions may become key development directions. On the one hand, local governments are leading the “industry-university-research” cooperation to build collection and training centers, while on the other hand, simulation and synthetic data are also being continuously attempted. Note: This report is excerpted from the Galaxy Securities Research Report for reference only and should not be used as an investment basis.

Currently, humanoid robot manufacturers are flourishing, and we roughly categorize the main participants into five categories: 1) Startups: Fast product iteration speed. This category can be further subdivided: the first type, robot companies, based on humanoid robots and other robotic products with technological homogeneity, have advantages in mechanical structure design and control. For example, Fourier Intelligence, Yushu Technology. The second type, founders or key executives with backgrounds in the internet/intelligent driving, have a certain sensitivity in using model algorithms, such as overseas Figure AI, 1X Technologies, and domestic Zhiyuan Robotics. The third type, other startups, such as UBTECH, Kepler Robotics, Leju Robotics, etc. 2) Automotive manufacturers: Have advantages in technology, scenarios, and supply chains. Technical advantages are reflected in algorithms and precision manufacturing, scenario advantages are reflected in B2B factory training and data collection, and supply advantages are reflected in the overlap of humanoid robots and electric vehicle components, making it more efficient for car manufacturers to choose familiar integrators and component suppliers. For example, Tesla, Xiaopeng, GAC Group, Seres. 3) Consumer electronics companies: 3C supply chain companies have strong capabilities in large-scale mass production quality and cost control, with accumulated experience in assembly and OEM, such as Lens Technology, Lingyi Technology, etc. 3C brand manufacturers have better product promotion capabilities in B2C scenarios, especially in household service scenarios, such as Xiaomi, APPLE, etc. 4) Research institutions/innovation centers: Have R&D experience and financial support. For example, Galaxy General Robotics, Star Motion Era, etc. 5) Other technology/internet giants: Currently, humanoid robots have become one of the consensus directions for technology/internet giants at home and abroad. With strong technology, capital, and talent strength, Tencent has previously attempted to launch a humanoid robot “Xiao Wu,” and ByteDance is also accelerating its layout, becoming a strong potential competitor. Beyond the body, technology/internet giants are currently more involved in the humanoid robot industry through investment + self-research large models, such as Alibaba & Ant investing in Yushu, Xinghai Map, Zhujidongli, etc.; Tencent investing in Yushu and Zhiyuan; Meituan investing in Yushu, Galaxy General, Xinghai Map, etc., laying out in fields such as medical delivery, unmanned retail, and low-altitude; JD investing in Qianxun Intelligent, Zhongqing Robotics, Zhujidongli, etc., in conjunction with its JoyAI large model and JoyScale AI computing power platform, serving the company’s logistics, warehousing, and other supply chain scenarios. 5. Companies Actively Layout, Market Competition Gradually Intensifies Dexterous hands: Currently, the technology in the dexterous hand field has not yet converged, with both self-research and third-party suppliers developing simultaneously, leading to increasing competition. The former includes Zhiyuan Robotics, Yushu Technology, Star Motion Era, Magic Atom, and Zhongke Huiling (Lingbao CASBOT), while the latter has also differentiated into different characteristics, such as Qiangna Intelligent and Aoyi Technology entering the robot dexterous hand from brain-machine interfaces, while Shiji, Pashini, Daming, Realtime Robotics, and Zhaowei Electromechanical provide not only complete hands but also internal components. Pashini and Dexterous Intelligence provide not only hardware hands but also launch data collection factories and operational datasets, while Lingchu Intelligent and Zhongke Silicon Technology combine AI operational algorithms with hardware dexterous hands. Motors: Frameless torque motors have an overseas first-mover advantage. The top three in the domestic market are Hota Technology (18%), Dazhuo Motors (15%), and Boke Co. (8%), with Hota and Dazhuo being mainstream collaborative robot suppliers in China. Hollow cup motors have a global CR3 > 50%, mainly foreign, such as Swiss MAXON, German FAULHABER, and Swiss PORTESCAP, with advantages in winding design and winding process accumulation, and advanced winding equipment self-researched and manufactured. Domestic Mingzhi Electric, Dingzhi Technology, Tuobang Co., Weichuang Electric, and Zhaowei Electromechanical are also committed to domestic substitution, among which Mingzhi Electric has independent patents for hollow cup windings, a complete product line, and product performance close to foreign levels, making it one of the leading domestic hollow cup motor manufacturers. Axial flux motors have a global CR3 of about 84%, with domestic manufacturers Hub Power being one of the leaders. According to QY research, the core manufacturers of axial flux motors YASA, Hub Power, and Naxatra Labs account for about 84% of the global market share. Regionally, Europe/Asia-Pacific/North America account for about 48%/32%/15% respectively. Screws: High-end ball screws are mainly overseas, while the mid-end market is dominated by Taiwanese and mainland companies, and the low-end market is mainly by mainland manufacturers. According to Huajing Industry Research Institute, German Rexroth, Japanese THK, and NSK occupy 90%/30% of China’s high-end/mid-end ball screw market, with mainland Chinese manufacturers only accounting for 5%/30% of high-end/mid-end. Planetary roller screws are dominated by overseas manufacturers, with domestic manufacturers’ market share in 2022 totaling less than 20%. According to Wang Youxue’s research on the marketing strategy of E company’s roller screws, in the Chinese market in 2022, overseas leaders Rollvis, GSA, and Ewellix accounted for 26%, 26%, and 14% respectively, while domestic manufacturers accounted for 19% (of which Nanjing Technology accounted for 8%, and Bote Precision accounted for 8%). Participants in the humanoid robot screw market, in addition to traditional screw manufacturers such as Xinjian Transmission and Nanjing Technology, new entrants are mostly automotive parts manufacturers, as well as other mechanical equipment and industrial component suppliers (such as leading hydraulic parts manufacturers Hengli Hydraulic and bearing manufacturers Wuzhou Xinchun). The former has a relatively high homogeneity in production processes between automotive parts and screws, possessing low-cost industrialization production experience and automotive customer resources. The latter is based on precision processing technology accumulation and mass production capabilities. Looking ahead, close cooperation with host manufacturers, strong technical strength, and rich experience in mass production are the three core basic elements for component companies to compete. Reducers: Harmonic reducers are mainly Japanese, with Harmonic Drive’s global and Chinese market shares in 2023 at 85% and 40%, respectively. According to the research report from Guanyan, in 2023, Harmonic Drive’s global market share is 85%, while Green Harmonics accounts for 8%; in 2023, the CR3 and CR5 market shares of China’s harmonic reducer industry are 68% and 81%, respectively, with Harmonic Drive accounting for 40%, Green Harmonics for 18%, and Laifu Harmonics for 10%. Precision planetary reducers are mainly dominated by Japanese and German manufacturers, with domestic market shares of local manufacturers Kefeng Intelligent and Niusidate at 12% and 9% in 2022, respectively. According to QY research, the top three Japanese and German manufacturers, including Shinbo and German Weitenshtein and Nucat, accounted for 35% of the global market share in 2022. In the Chinese market in 2022, the top three were Japan’s Shinbo at 20%, Kefeng Intelligent at 12%, and Niusidate (Shandong) at 9%. Cycloidal reducers are dominated by Japanese manufacturers, but the pattern is not yet solidified, with some domestic gear manufacturers and RV reducer manufacturers attempting to develop cycloidal needle wheel reducer products suitable for humanoid robots. Six-dimensional force sensors: The global market is highly concentrated, with the top three being overseas leaders, accounting for over 50% of the market share in 2023. According to QY Research, in 2023, the top five manufacturers, ATI, Schunk, AMTI, Yuli Instruments, and Kistler, accounted for 36.2%, 8.2%, 8.0%, 4.3%, and 4.3% of the market share, respectively, with a CR5 of 61%; by category, strain gauge type accounts for 76.2%, with the rest mainly being piezoelectric/capacitive types. In 2023, the domestic market’s localization rate is about 30%. According to the China Business Industry Research Institute, in the domestic market in 2023, the CR5 is 50.5%, with the top three being ATI/Yuli Instruments/Epson, accounting for 22.4%, 12.2%, and 6.4%, respectively, while Landot Touch/Kunwei Technology/Xin Jingcheng accounted for 4.8%, 4.7%, and 2.2%. In 2024, in the Chinese humanoid robot six-dimensional force sensor market, Landot/Kunwei/Yuli/Xin Jingcheng/ATI are expected to account for 62%, 26%, 7%, 4%, and 1%, respectively (MIR). Flexible tactile sensors: The global market is dominated by North America and Europe. According to QY Research, in 2022, all of the top five manufacturers in the global market are overseas companies (Novasentis, Tekscan, Japan Display Inc., Baumer, Fraba), with a combined market share of about 57.1%. The domestic market is relatively fragmented, with different technology routes, such as resistive – Fulai New Materials/Huawei Technology, capacitive – Tashan Technology, visual tactile – Daming/Witai Robotics, electromagnetic Hall effect – Pashini, etc. Hanwei Technology has launched products in resistive/piezoelectric/capacitive/flexible sweat routes. Currently, most dexterous hands are equipped with resistive/capacitive sensors, with optional visual tactile/electromagnetic sensors. AI Chips: Nvidia holds an absolute dominance, with the localization rate continuously improving. In 2024, Nvidia’s global market share in AI chips is as high as 90% (Gartner), with advantages in process technology, architecture design, and software ecosystem. At the same time, the penetration rate of domestic AI chip brands is about 30%, doubling from last year (IDC), with companies like Horizon and Black Sesame Intelligence effectively reusing high-performance, high-reliability, automotive-grade chip technology from the intelligent automotive field in robotics, while Cambricon provides the cloud/edge computing power needed for training AI models and complex reasoning in robots. Embodied intelligence is the next wave of artificial intelligence development and will be one of the most important sectors under the “14th Five-Year Plan.” Among the representative industries of embodied intelligence, we particularly look forward to the alpha opportunities brought by the humanoid robot industry. The “14th Five-Year Plan” will be a critical period for humanoid robots to move towards mass production, and we recommend early in-depth layout around the entire industry chain: 1) Hosts: Several domestic host manufacturers have achieved remarkable results in mass production, forming clear main lines around key players such as T chain, F chain, Yushu chain, and Zhiyuan chain, while there are many potential players waiting to be explored. The form of robot bodies has not yet converged, and domestic host manufacturers are increasingly focusing on linear joints. We recommend layout directions such as ① leading enterprises with deep technical accumulation and good product ecological patterns; ② OEMs with outstanding manufacturing capabilities and specialized comprehensive support for startups. 2) Application scenarios: We believe this link is one of the biggest breakthrough points for the industrialization of embodied intelligence. The differentiation of application scenarios will also affect the technical route direction of various upstream players. Enterprises with strong landing capabilities are expected to dominate the industry chain and enjoy greater flexibility. Currently, scenarios are mainly concentrated in data collection, automotive industry, etc. In the short term, we are optimistic about the acceleration opportunities brought by special and hazardous fields, while in the long term, we are optimistic about the general fields such as large models that connect commercial and life services, while also paying attention to the premium space brought by some large-scale markets with strong qualification barriers. 3) Dexterous hands: This link accounts for a high cost of the host and directly affects the actual working ability of robots, making it a key link in the industrialization of embodied intelligence, with high attention in investment and financing. However, due to high technical bottlenecks in both hardware and software, as well as low return-cost ratios, there are also relatively large divergences, and the trend of routes has not yet converged, possessing both high growth potential and uncertainty. We believe that the current layout of dexterous hands should start from the core of downstream applications, with structural opportunities in various sub-materials, sensors, etc., and technological advantages being the biggest catalyst for company growth, focusing on areas with significant marginal changes such as electronic skin. 4) Components: Core components such as screws, reducers, motors, etc., have achieved breakthroughs in domestic production, but many new entrants have increased the competition intensity in the field, posing a risk of rapid intensification of competition. We believe that the current layout direction mainly focuses on leading enterprises, especially those at the head of the automotive industry chain, which have excellent large-scale product mass production and quality control capabilities. A mature supply chain system is conducive to rapid cost reduction and landing, while already having good relationships with host manufacturers, will continue to benefit from industrial development opportunities, becoming core participants in the embodied intelligence industry. The hardware OEM model is gradually emerging, and the division of research, production, and sales is beginning to explore. In the 1-100 mass production stage, the requirements for consistency and cost control of components will be enhanced, and the adoption of hardware OEM and host assembly models is expected to increase. 5) “Big and Small Brains”: Currently, the hardware barriers in the industry are decreasing, and the big and small brains are important shortcomings. The current technical routes for large models are still diverging, with VLA currently receiving high attention, and dual-system architectures such as Figure AI helix and Nvidia GR00T N1 are thriving. In terms of operational control, multiple solutions are merging and gradually converging. In addition, data is one of the core bottlenecks for achieving general embodied intelligence. Currently, robot experiential data can be directly used for strategy learning but is relatively scarce, while human data is abundant but requires repositioning or non-physical motion data, and the data quality may not be high. We believe that data training grounds and simulation solutions may become key development directions. On the one hand, local governments are leading the “industry-university-research” cooperation to build collection and training centers, while on the other hand, simulation and synthetic data are also being continuously attempted. Note: This report is excerpted from the Galaxy Securities Research Report for reference only and should not be used as an investment basis.