PCBs are like the skeleton of electronic products, connecting electronic components and transmitting signals for devices such as mobile phones, computers, cars, and even rockets and satellites.

PCBs are like the skeleton of electronic products, connecting electronic components and transmitting signals for devices such as mobile phones, computers, cars, and even rockets and satellites.

The explosion of AI has brought unprecedented upgrade pressure to this skeleton: the number of layers is increasing, hole diameters are decreasing, and processes are becoming more complex.

This article interprets the overall picture of the PCB equipment industry from aspects such as industry overview, market, processes, industrial chain structure, and domestic progress.

Formore interpretations of industry reports and original documents, please join the Knowledge Planet

This article is a summary interpretation of the original report1. Overview of the PCB Industry

This article is a summary interpretation of the original report1. Overview of the PCB Industry

1. Industry Positioning

PCB stands for Printed Circuit Board, which is simply a bridge that carries electronic components and connects circuits.

From small devices like mobile phones and smartwatches to large systems like AI servers and electric control systems in new energy vehicles, almost all electronic products rely on it, earning it the title of “mother of electronic products”.

In terms of application scenarios, it mainly covers:

Communication equipment, 5G base stations, switches;

Automotive electronics, VCU and BMS systems in new energy vehicles;

Consumer electronics, mobile phones, PCs;

VR devices, server data storage, AI servers, etc.;

Medical devices, CT machines, ventilators, etc.

2. AI PCB

(1) Types

AI PCB specifically refers to PCB products used in the AI field, divided into cloud and terminal:

Cloud includes boards for AI servers, switches, optical modules, etc.;

Terminals cover AI smartphone motherboards, smart hardware connection boards, etc.

Among them, high-layer boards and HDI boards are the two core types of AI PCBs.

High-layer boards are used for GPU substrates in AI servers, while HDI boards support high-density signal connections in AI servers. The Compute Tray module in Nvidia’s GB200 architecture widely uses multi-stage HDI boards.

(2) High-layer Boards and HDI Boards

From global data in 2024, the output value of HDI boards is significantly higher than that of high-layer boards, but the growth rate of high-layer boards is faster.

The global output value of high-layer boards in 2024 is $2.421 billion, while the output value of HDI boards is $12.518 billion, making the output value of HDI 5.17 times that of high-layer boards;

In terms of growth rate, the output value of global high-layer boards is expected to grow by 40.2% year-on-year in 2024, while HDI boards are expected to grow by 18.8%, making the growth rate of high-layer boards 2.14 times that of HDI boards.

3. Cyclical Process

(1) Previous Cycle: 5G and New Energy

Since 2017, the PCB industry has entered an upward cycle, driven primarily by 5G communication base stations and new energy vehicles.

The popularity of 5G mobile phones and base stations has driven demand for mid-to-low-layer PCBs, while the electrification upgrades in new energy vehicles, such as motor control systems and battery management systems, have increased PCB usage.

The usage of FPC flexible circuit boards in new energy vehicles can reach up to 100 pieces per vehicle, several times that of traditional fuel vehicles.

In 2016, the global PCB output value was $54.2 billion, reaching a peak of $81.7 billion by 2022;

The revenue and capital expenditure of the top 40 global PCB companies peaked in 2021-2022, with revenue reaching $118.8 billion and capital expenditure reaching $13.2 billion in 2022.

(2) Current Cycle: AI

In the second half of 2023, the consumer electronics industry completed inventory clearance, and the explosion in demand for AI servers became a new growth driver for the PCB industry.

AI servers require high-layer boards, HDI boards, and other high-end PCBs, which have higher technical requirements, directly driving PCB manufacturers to expand production and increase capital expenditure.

The global PCB market size in the server/data storage field is expected to grow significantly year-on-year in 2024, with a projected CAGR of 11.6% from 2024 to 2029.

2. Market Status

1. Market Size

(1) Global PCB

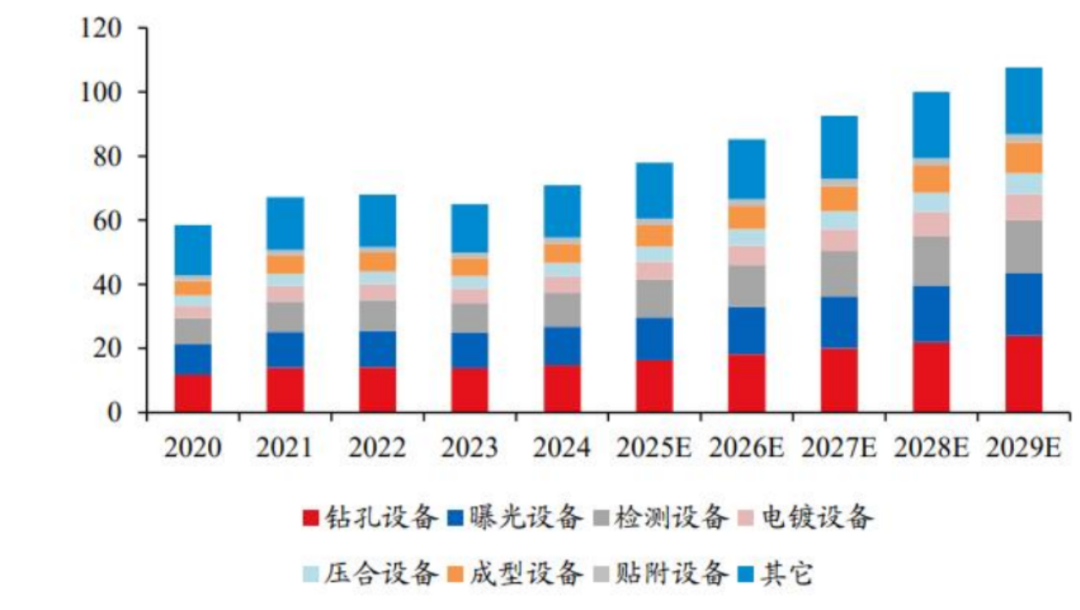

The global PCB dedicated equipment market size is expected to grow from $5.84 billion in 2020 to $7.085 billion in 2024.

With AI servers driving high-end PCB demand, the market is expected to maintain steady growth from 2024 to 2029, with growth rates for core equipment such as drilling, exposure, and plating expected to exceed the industry average.

(2) China PCB

China is the largest PCB equipment market globally, with the market size for dedicated PCB equipment expected to grow from $3.306 billion in 2020 to $4.111 billion in 2024, with a CAGR of 5.60%, outpacing the global growth rate.

By 2024, China’s share of the global PCB equipment market will exceed 58%, further consolidating its market dominance in drilling equipment, plating equipment, and other areas.

In 2024, the market size for drilling equipment in China is expected to reach $831 million, accounting for 56.5% of the global drilling equipment market.

Global PCB Dedicated Equipment Market Size (in billions)

2. Market Structure

(1) Market Share

In the PCB equipment market, drilling equipment has the highest value share, with drilling equipment accounting for 20.21% of the dedicated PCB equipment market in China in 2024;

Followed by exposure equipment at about 17%, testing equipment at about 14%, plating equipment at about 7%, laminating equipment at about 6%, forming equipment at about 9%, and other equipment such as attachment equipment at about 27%.

This structure stems from the core position of the drilling process in PCB production, as drilling is key to achieving multilayer board interconnections, and high-end PCBs have higher precision requirements for drilling, driving the growth of drilling equipment demand.

(2) Demand Distribution

From the downstream demand perspective, in 2024, the server/data storage sector will be the fastest-growing area for PCB equipment demand, accounting for 14%;

Followed by automotive electronics, consumer electronics, and communication equipment.

The acceleration of AI computing centers and data center construction will continue to expand the demand for PCB equipment in the server and data storage fields, becoming a growth point in the coming years.

3. Processes

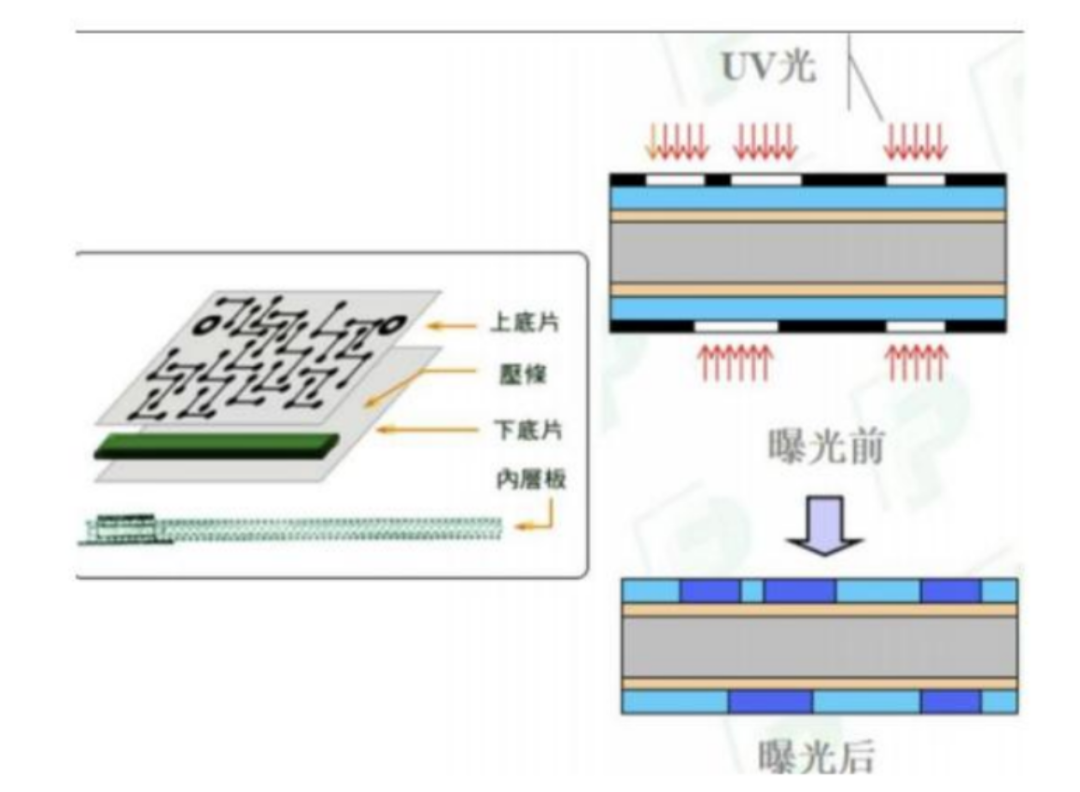

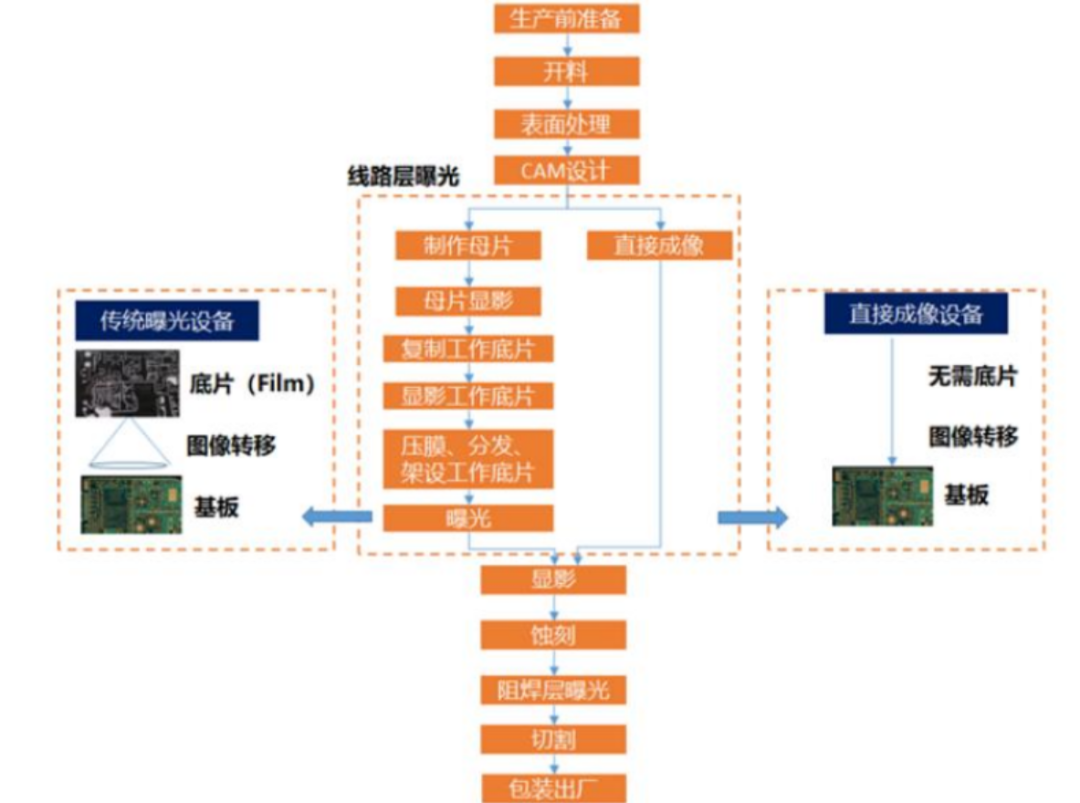

(1) Exposure Process and Equipment

This is the process of transferring circuit patterns onto the PCB substrate, accounting for 17% of the value share, mainly divided into three categories: inner layer pattern exposure, solder mask and text exposure, and outer layer pattern exposure.

The corresponding equipment includes laser direct imaging (LDI) equipment and traditional film exposure equipment:

LDI does not require film and directly projects patterns onto the substrate using lasers, achieving higher precision;

Traditional film exposure requires the production of film negatives first and is suitable for mid-to-low-end PCBs.

Currently, high-end PCB production has widely adopted LDI, with almost all exposure processes for HDI boards and high-layer boards using LDI.

Film Exposure Principle

(2) Laminating Process and Equipment

The laminating process is used for multilayer board manufacturing, accounting for 6% of the value share. It is the process of stacking inner layers with prepreg and pressing them into a whole under specific temperature and pressure.

The corresponding equipment is the laminating machine, with core requirements for uniformity and stability of temperature and pressure. Uneven lamination can lead to poor interlayer bonding in multilayer boards, affecting circuit conductivity.

High-end laminating equipment can achieve precise temperature and pressure adjustments to meet the production needs of high-layer boards.

(3) Drilling Process and Equipment

Drilling is the process of machining conductive holes on the PCB, accounting for 21% of the value share, and is key to achieving multilayer board interconnections. The corresponding equipment includes mechanical drilling machines and laser drilling machines:

Mechanical drilling machines are suitable for through holes with a diameter of ≥0.15mm, used with drill bits;

Laser drilling machines are suitable for blind holes and buried holes with a diameter of <0.15mm, divided into CO2 laser drilling machines, UV laser drilling machines, etc.

PCBs for AI servers require a large number of small holes, thus the demand for laser drilling machines is rapidly increasing. The UV laser drilling machine from Dazhu CNC can achieve processing of holes with a diameter of 0.05mm.

(4) Plating Process and Equipment

The plating process is used to form a copper layer on the hole walls and circuit surfaces, accounting for 7% of the value share, divided into chemical plating and electroplating steps.

The corresponding equipment includes vertical continuous plating equipment, vertical lift plating equipment, and horizontal continuous plating equipment:

VCP has the highest degree of automation, capable of continuously completing feeding, plating, drying, and other processes with good uniformity, making it the mainstream choice for high-end PCBs;

Horizontal continuous plating equipment is suitable for electroplating ultra-thin PCBs or flexible PCBs.

(5) Forming and Testing Process and Equipment

The forming process is the process of machining the PCB to specified dimensions, accounting for 9% of the value share. The corresponding equipment includes mechanical forming machines and laser forming machines:

Laser forming machines have higher precision and are suitable for small sizes or complex shapes of PCBs, such as small accelerator module PCBs in AI servers.

The testing process runs through the entire PCB production, with core equipment including flying probe testers and AOI testing equipment:

Flying probe testers are used to test circuit conductivity, while AOI is used to detect pattern defects.

Process Flow Chart for PCB Manufacturing Using Traditional Exposure Equipment and Direct Imaging Equipment

4. PCB Equipment Industry Links

1. Drilling Equipment and Consumables

(1) Drilling Equipment

The global drilling equipment market is expected to grow from $1.174 billion in 2020 to $1.47 billion in 2024, with a growth rate of 6.5% in 2024;

It is expected to accelerate growth from 2024 to 2029, reaching $2.399 billion.

The Chinese drilling equipment market is synchronized with the global market, with a scale of $831 million in 2024, expected to reach $1.358 billion by 2029, maintaining a share of over 56% in the global market, highlighting China’s dominant position in the drilling equipment market.

(2) Drill Bits

Drill bits are the core consumables of mechanical drilling machines, made of tungsten-cobalt alloy, characterized by high hardness but poor toughness.

As PCBs develop towards higher layers and micro-holes, the demand for drill bits has shown a simultaneous increase in both quantity and price:

In terms of quantity, the number of holes drilled in 18-layer PCBs is 1.5 times that of 12-layer PCBs, and the lifespan of drill bits has decreased from 500 holes per bit to 300 holes per bit, significantly increasing usage;

In terms of price, micro drill bits with a diameter of less than 0.2mm are 2-3 times the price of ordinary drill bits, and coated drill bits are even more expensive.

In 2024, the global drill bit market size is expected to be around $1.2 billion, with Chinese manufacturer Dingtai Gaoke holding a 26.5% market share, ranking first globally.

2. Exposure Equipment

(1) Exposure Equipment Market

The global exposure equipment market is expected to reach approximately $1.204 billion in 2024, with China accounting for about 55% of the market.

With the growing demand for HDI boards and high-layer boards, the penetration rate of LDI is expected to increase from 40% in 2020 to 65% in 2024, and is projected to exceed 80% by 2029.

The unit price of LDI is 3-5 times that of traditional film exposure equipment, so the growth of the exposure equipment market size is mainly driven by LDI, with the global LDI market size expected to reach approximately $850 million in 2024, a year-on-year increase of 12%.

(2) Technical Focus

The focus of exposure equipment is on high precision and high speed:

In terms of high precision, overseas manufacturers can achieve a line width of 20μm, while domestic manufacturers have caught up to 25μm, gradually narrowing the gap;

In terms of high speed, overseas LDI can achieve a processing efficiency of 150 pieces/hour, while domestic equipment is about 120 pieces/hour, with the main gap in multi-laser head collaborative control technology.

In the future, as the demand for IC substrates grows, exposure equipment will also need to upgrade to higher resolutions.

3. Plating Equipment

(1) Plating Equipment Market

The global plating equipment market is expected to reach approximately $508 million in 2024, with China accounting for about 70% of the market.

Among them, vertical continuous plating equipment is the mainstream, with the Chinese VCP market size expected to reach approximately $210 million in 2024, accounting for 59% of the domestic plating equipment market;

It is expected that by 2026, the Chinese VCP market size will reach 2.4 billion yuan, with a CAGR of 10%.

The growth of VCP is mainly driven by the expansion of high-end PCB production, such as Dongwei Technology’s VCP equipment, which has entered the production lines of leading PCB manufacturers like Shennan Circuit and Huidian Co.

(2) Horizontal Plating Equipment

High-end HDI boards and IC substrates require horizontal plating equipment, especially three-in-one horizontal plating equipment, which integrates functions of glue residue removal, chemical copper deposition, and copper plating, a field previously dominated by foreign capital.

In 2024, Dongwei Technology’s three-in-one horizontal plating equipment passed customer acceptance, filling a domestic gap, with a unit price only 70% of foreign equipment.

It has already received bulk orders, and it is expected that the domestic replacement rate of horizontal plating equipment will increase from 10% to 30% in the next three years.

4. Testing Equipment

(1) Market

The global testing equipment market is expected to grow from $818 million in 2020 to $1.063 billion in 2024, with a growth rate of 15% in 2024, making it one of the fastest-growing categories in PCB equipment;

The Chinese testing equipment market is expected to reach $489 million in 2024, with a year-on-year growth of 17%, higher than the global average.

The core reason for the growth in testing equipment demand is the higher quality requirements for high-end PCBs, with the qualification rate for PCBs used in AI servers needing to reach 99.9%, far exceeding the 95% for ordinary PCBs, thus requiring more testing equipment for full-process monitoring.

(2) Technology

Testing equipment is transitioning from manual-assisted testing to fully automated testing:

The recognition accuracy of AOI testing equipment has improved from 50μm to 20μm, capable of detecting small defects such as circuit gaps and hole position deviations;

The testing speed of flying probe testers has increased from 100 points/second to 300 points/second, while also supporting parallel testing of multiple boards.

Domestic manufacturers like Dazhu CNC’s AOI equipment can now compete with Japan’s SCREEN products, with market share increasing from 15% in 2020 to 25% in 2024.

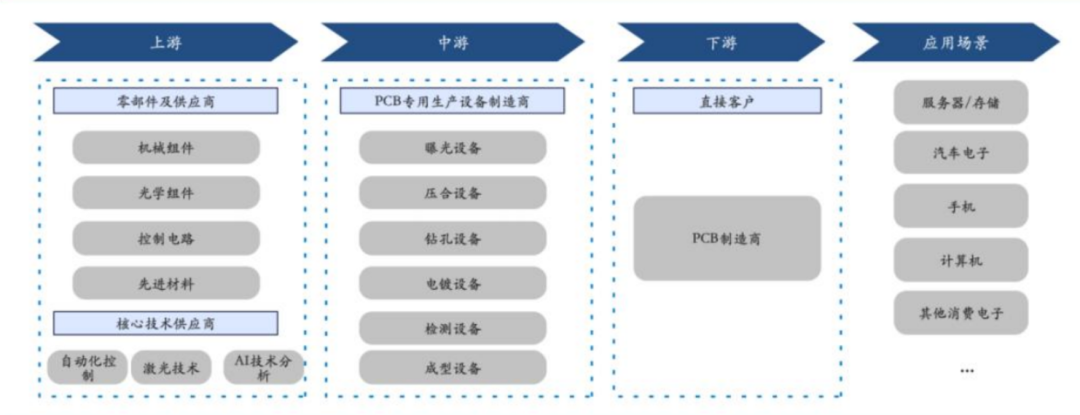

5. Industry Supply Chain

1. Upstream of the Supply Chain

(1) Supply Structure

The upstream components of PCB equipment are mainly divided into three categories:

Mechanical components, spindles, guide rails, ball screws;

Optical components, lasers, lenses, CCD cameras;

Control circuits, servo motors, PLCs, motion controllers.

High-end components still rely on imports:

Spindles mainly come from Germany’s Schaeffler and Japan’s NSK; lasers mainly come from the US’s Coherent and Germany’s Trumpf; motion controllers mainly come from Japan’s Fanuc and Germany’s Siemens.

Domestic manufacturers have achieved independent supply in the mid-to-low-end component field, with guide rails in mechanical components and PLCs in control circuits having a domestic rate of over 60%, but the domestic rate for high-end components is still less than 20%.

(2) Cooperation Models

The core technologies of PCB equipment include laser technology, automation control technology, and AI detection technology:

Laser technology is mainly achieved through cooperation with specialized laser companies, such as Dazhu CNC sharing laser technology with Dazhu Laser.

Automation control technology often adopts a combination of independent research and external cooperation;

AI detection technology is developed through cooperation with universities and AI companies.

Currently, the proportion of R&D investment by domestic equipment manufacturers is generally between 8%-12%, higher than the 5%-8% in traditional machinery industries.

PCB Dedicated Equipment Supply Chain

2. Midstream of the Supply Chain

(1) Manufacturers

The top five PCB equipment manufacturers globally are expected to hold a combined market share of 20.9% in 2024, including China’s Dazhu CNC, Japan’s Mitsubishi Electric, the US’s MKS, the US’s KLA, and Germany’s Schmoll.

Dazhu CNC is the only Chinese company to enter the global top five, covering drilling, exposure, forming, testing, and other core processes, with a market share of over 30% in the mid-to-low-end equipment market.

(2) Competitive Hierarchy

Domestic PCB equipment manufacturers can be divided into three tiers:

The first tier includes Dazhu CNC and Dongwei Technology, whose products cover core processes and possess global competitiveness;

The second tier includes Xinqi Microelectronics and Haozhi Electromechanical, focusing on a single field and leading in market share in niche markets;

The third tier includes small and medium-sized manufacturers, mainly focusing on mid-to-low-end equipment, with severe product homogeneity.

In 2024, the revenue of first-tier manufacturers is expected to account for 45% of the domestic PCB equipment market, the second tier 30%, and the third tier 25%.

3. Downstream of the Supply Chain

(1) Distribution

Global PCB manufacturers are mainly concentrated in China (56%), Taiwan (20%), Japan (10%), and South Korea (8%).

Leading domestic PCB manufacturers include Pengding Holdings, Shennan Circuit, Huidian Co., and Dongshan Precision, whose equipment procurement demands are large and requirements are high:

Pengding Holdings’ HDI board production line can purchase over 50 LDI machines in a single order, requiring equipment processing efficiency of ≥100 pieces/hour;

Overseas PCB manufacturers tend to primarily import equipment, supplemented by domestic equipment, but the proportion of domestic equipment procurement has been gradually increasing in recent years.

(2) End Applications

The demand in end application fields is transmitted through terminal equipment manufacturers, PCB manufacturers, and PCB equipment manufacturers:

For example, in the case of AI servers, terminal manufacturers like Nvidia and Dell increase orders for AI servers, leading PCB manufacturers like Shennan Circuit and Huidian Co. to expand production of PCBs for AI servers, and then procure drilling and exposure equipment from Dazhu CNC and Xinqi Microelectronics.

This transmission cycle typically lasts 6-12 months, meaning that after the explosion of terminal demand, PCB manufacturers will initiate expansion within 6 months, and PCB equipment manufacturers will fulfill orders within 12 months.

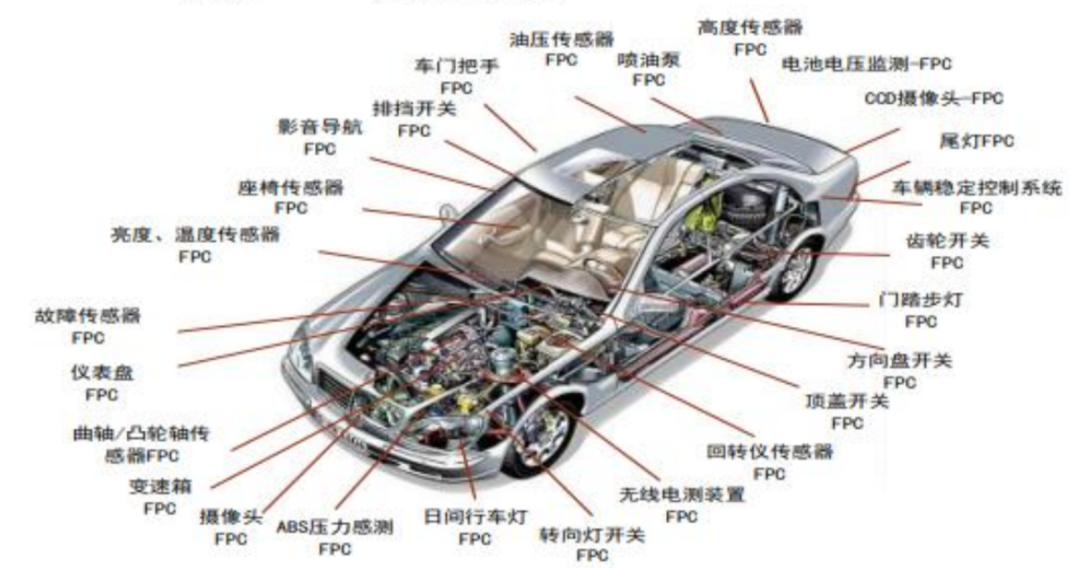

Vehicle FPC Usage

6. Related Companies

1. Dazhu CNC

(1) Products

Dazhu CNC’s products cover drilling, exposure, forming, testing, laminating, and other full-process equipment, with advantages in drilling and exposure equipment:

In terms of drilling equipment, its 3D back drilling function CCD six-axis mechanical drilling machine can achieve ultra-short stub processing, leading to bulk purchases from Shennan Circuit and Huidian Co.;

In terms of exposure equipment, its LDI equipment achieves a processing efficiency of 120 pieces/hour with a line width precision of 25μm, already applied in the production line of HDI boards for AI servers.

Dazhu CNC has also developed integrated drilling and testing equipment, combining drilling and testing processes, reducing production line footprint by 30%.

(2) Market Layout

In the domestic market, Dazhu CNC’s customers cover over 90% of leading PCB manufacturers, with domestic revenue accounting for 75% in 2024;

In the overseas market, it has entered the supply chains of overseas PCB manufacturers such as Thailand’s Zhendin and Vietnam’s Yifei Electric, with overseas revenue accounting for 25% in 2024, a year-on-year growth of 40%.

In 2024, Dazhu CNC’s PCB equipment revenue is expected to reach 3.3 billion yuan, with drilling equipment revenue accounting for 45%, exposure equipment 25%, and other equipment 30%.

2. Xinqi Microelectronics

(1) Products

Xinqi focuses on exposure equipment, with its core products being LDI equipment, divided into line layer LDI and solder mask layer LDI:

The MAS series of line layer LDI equipment achieves a minimum line width of 3-4μm, suitable for IC substrates and high-end HDI boards;

The NEX series of solder mask layer LDI equipment achieves a processing efficiency of 150 pieces/hour and has entered the production lines of Pengding Holdings and Dongshan Precision.

In 2024, Xinqi Microelectronics also expanded its laser drilling equipment business, with its CO2 laser drilling equipment passing mass production verification from leading customers, with expected order volume exceeding 200 million yuan in 2025.

(2) Capacity and Market

In 2024, Xinqi Microelectronics’ LDI equipment capacity is expected to reach 300 units/year, and after the second-phase base is put into production in 2025, capacity will increase to 500 units/year.

In the overseas market, its Thai subsidiary serves as a hub for Southeast Asia, contributing 120 million yuan in revenue in 2024, accounting for 15%;

At the same time, it is expanding into the Vietnamese and Malaysian markets, with new overseas orders exceeding 150 million yuan in 2024.

In 2024, Xinqi Microelectronics’ revenue is expected to reach 782 million yuan, a year-on-year growth of 35%, with LDI equipment revenue accounting for 90%.

3. Dongwei Technology

(1) Products

Dongwei Technology’s products include vertical continuous plating equipment, with the latest generation of VCP equipment achieving a plating uniformity error of ≤5%, meeting the production needs of high-layer boards above 18 layers;

It has also developed three-in-one horizontal plating equipment, integrating glue residue removal, chemical copper deposition, and copper plating functions, filling a domestic gap, with bulk orders of 50 million yuan received in 2024.

Dongwei Technology is also laying out new energy plating equipment, but PCB plating equipment remains the main source of revenue.

(2) Performance and Customers

In the first half of 2025, Dongwei Technology is expected to achieve revenue of 443 million yuan, a year-on-year growth of 13.1%, with PCB plating equipment revenue of 354 million yuan, a year-on-year growth of 18%; net profit attributable to the parent company is expected to be 43 million yuan, a year-on-year decrease of 23.7%.

In terms of customers, procurement from leading domestic PCB manufacturers accounts for over 60%, with overseas customer procurement accounting for 15% in 2024.

4. Dingtai Gaoke

(1) Products

Dingtai Gaoke’s core products are PCB drill bits, including ordinary drill bits, micro drill bits, and coated drill bits, with micro drill bits accounting for 28.09% of sales in 2024 and coated drill bits accounting for 36.18%.

In terms of capacity, Dingtai Gaoke’s drill bit monthly capacity is expected to exceed 100 million units in 2024, with a global market share of 26.5%, ranking first.

Additionally, Dingtai Gaoke has expanded into grinding and polishing materials and automation equipment businesses, but drill bit business still accounts for over 85% of revenue.

(2) Technical Advantages

In the overseas market, Dingtai Gaoke has achieved localized supply through its production base in Thailand, with overseas revenue expected to reach 79 million yuan in 2024, a year-on-year growth of 124.09%;

It has also acquired Germany’s MPK Kemmer GmbH, gaining access to European customer resources.

In terms of technology, Dingtai Gaoke’s high aspect ratio drill bits can meet the needs of high-layer boards for AI servers, with a breakage rate 20% lower than imported drill bits.

5. Zhongtung High-tech

(1) Products

Zhongtung High-tech’s subsidiary, Jinzhu Precision, is a global supplier of high-end drill bits, with its core products being PCB micro drill bits, covering standard sizes from 0.01mm to 6.50mm, capable of mass production of 0.01mm ultra-micro drill bits, with leading technology globally.

In 2024, Jinzhu Precision’s micro drill capacity is expected to reach 680 million units, accounting for 25% of Zhongtung High-tech’s revenue.

Additionally, Zhongtung High-tech has a complete tungsten industry chain, providing cost advantages in drill bit raw material supply.

(2) Market Position

From 2018 to 2024, Zhongtung High-tech’s operating income is expected to grow from 8.177 billion yuan to 14.743 billion yuan, with a CAGR of 10.32%;

Net profit attributable to the parent company is expected to grow from 136 million yuan to 939 million yuan, with a CAGR of 37.99%.

Among them, Jinzhu Precision’s drill bit products have a market share of 18% in the high-end market, with customers including Nvidia’s PCB suppliers Yifei Electric and Zhendin.

Formore interpretations of industry reports and original documents, please join the Knowledge Planet