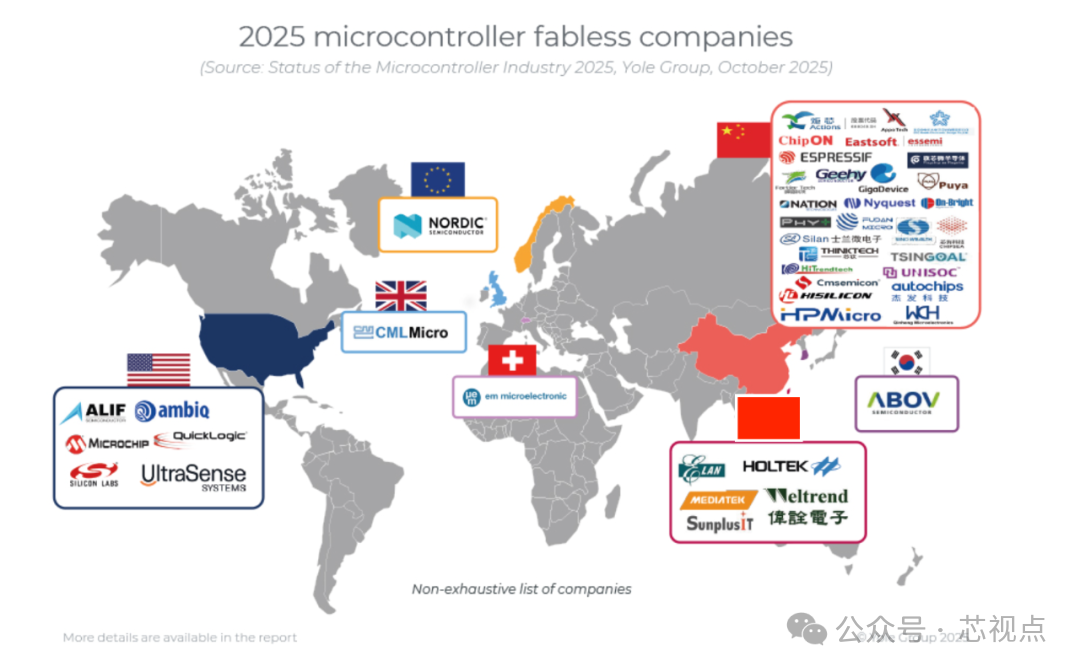

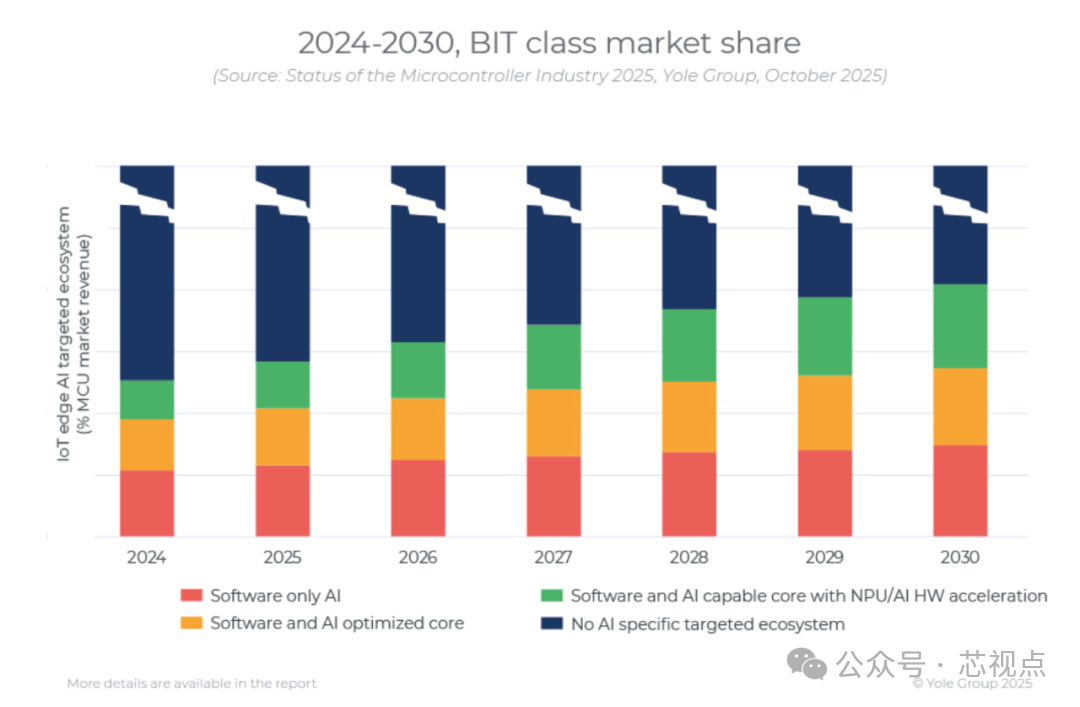

After the downturn in 2024, the MCU market seems to be making a strong comeback as we enter 2025.According to statistics from Yole, in the first quarter of 2025, although there are signs that production reduction strategies are still ongoing, the overall market has begun to recover demand through new orders. The MCU market has grown by approximately 9%; by the second quarter of 2025, all signs indicate a strong recovery momentum, with the overall market expected to grow an additional 16%.While these results are encouraging and allow us to breathe a sigh of relief, we must remain highly vigilant. This growth is still insufficient to compensate for the market losses in the fourth quarter of 2024. The fundamental factors that triggered this event still exist. Consumers remain skeptical. The geopolitical situation remains turbulent. Conflicts continue in various regions, and global tensions are escalating.On the other hand, new investments in areas such as wireless, security, automation, and IoT edge AI applications are being driven by various trends. The interaction of these forces seems to have converged into a potential market adjustment. The current double-digit growth rate may not be sustainable until the end of 2025, and the market will enter a new trajectory resembling a market adjustment, trending towards moderation and balance. This new trajectory will still maintain moderate growth, but the instability factors that led to the significant decline in the fourth quarter of 2024 remain. The risks are still high.Chinese MCU Manufacturers Chase the Five GiantsAmong the five major MCU design manufacturers, Infineon, NXP, and STMicroelectronics are integrated design manufacturers (IDM) headquartered in Europe. The other two are Renesas Electronics, headquartered in Japan, and Microchip, a fabless supplier based in the United States. These five suppliers account for about three-quarters of the microcontroller (MCU) market share (by revenue).However, at least 60 semiconductor companies are designing MCUs (it seems Yole is unaware of the Chinese MCU landscape).Despite Western countries attempting to hinder China’s production of cutting-edge semiconductor components critical to defense and many other markets through sanctions, tariffs, and other measures, China has shifted its focus to more common and less regulated semiconductor products, such as MCUs.MCUs are a vital component of the electronics industry. While processors like CPUs, GPUs, NPUs, FPGAs, and AI accelerators receive significant attention due to their applications in defense, aerospace, data centers, high-performance computing, and automotive ADAS technologies, the smaller, more common MCUs still account for over three-quarters of all processor sales. They are ubiquitous; without them, your car would not run, public transport would come to a halt, household appliances would not function, and many wireless devices would be unusable, among other issues.Therefore, although these tiny components are cheaper and technically less complex than other components, their importance to modern society is undiminished.While China may currently lack the cutting-edge technology to compete with Western manufacturers in CPU or GPU design, it has incentivized a large number of semiconductor suppliers to enter the MCU market. This has led to a surge of small and medium-sized design companies entering the market, launching competitively priced MCU products, with an increasing number of products based on RISC-V core technology to further reduce dependence on Western open architecture technologies (with low or no patent fees).As OEM manufacturers continue to seek low-cost semiconductor products from China, Chinese MCU suppliers will also continue to expand their business to capture a larger share of the global market.However, China cannot continue to subsidize this market indefinitely; eventually, there will be winners, and companies that cannot compete will be eliminated. At that point, market dynamics beyond costs, such as quality, relationships, and business and trade policies, will become increasingly important. At least for now. The following image illustrates the significant disparity in the number of fabless designers currently in mainland China. The New Frontier of AI ScalingArtificial intelligence is now recognized as a powerful driver of the scaling of computing devices, networking equipment, and data centers. This has led to a tremendous demand for next-generation GPUs, NPUs, ASIC AI accelerators, and FPGAs for AI computing performance. However, as this industry flourishes, there are numerous challenges in scaling to meet the computational time demands of AI applications on server clusters. These challenges include the power consumption of servers, the required cooling, the generated network traffic, security, privacy, and latency issues, among others.What is less known is that AI scaling has another frontier, which is the downward expansion—IoT edge computing. With this trend of downward expansion, a new type of microcontroller (MCU) has emerged to meet this demand. Many core IP designers and MCU suppliers are turning their attention to how to help customers leverage AI in this new domain to address the challenges of AI in networks.There is a misconception that AI requires large processors with trillions of operations per second (TOPS) performance to fully realize its application performance. While there is some truth to this, it is actually misleading. The higher the processing performance (usually measured in TOPS), the faster AI operations are typically completed. Given the enormous scale of operations executed in today’s cloud data centers, it is easy to believe this. However, not all AI applications have the same performance requirements. Currently, some AI frameworks are optimized for very resource-constrained situations (e.g., IoT AI Edge). This includes platforms based on the TinyML framework, such as Edge Impulse or TensorFlow Lite.First, many traditional MCUs can integrate third-party AI algorithms, although the efficiency is often not high. MCU suppliers and third-party vendors provide tools that can enhance the operational efficiency of AI algorithms. Without hardware acceleration, these tools are referred to as pure software solutions, but they almost always utilize some form of compact, resource-constrained AI framework, such as TinyML. Additionally, these tools can also convert traditional applications to run within AI frameworks, thereby improving efficiency.Second, one strategy MCU suppliers are adopting for edge AI is to use enhanced core architectures to accelerate typical AI algorithms. The core complexes are often multi-core. A typical core architecture may include Arm Cortex M55 or M85, or the recently launched M52, all of which include features for AI.The third strategy is to integrate additional dedicated neural network processing units (NPUs) or AI hardware accelerators to accelerate more complex matrix multiplication operations, thereby meeting the demands of more demanding AI applications while maintaining the power efficiency or cost-effectiveness of microcontrollers.These solutions aim to address significant challenges that cloud or network edge-based solutions may not be able to handle. They can reduce network traffic, lower energy consumption and cooling requirements, decrease latency, and enhance privacy and security. When application scenarios are more limited, such as listening for specific sounds, perceiving events, determining whether operations exceed standards, and using data to identify issues, or various other edge applications, these solutions can be effective. The following image illustrates how this emerging field is rapidly addressing the challenges posed by IoT edge AI.

The New Frontier of AI ScalingArtificial intelligence is now recognized as a powerful driver of the scaling of computing devices, networking equipment, and data centers. This has led to a tremendous demand for next-generation GPUs, NPUs, ASIC AI accelerators, and FPGAs for AI computing performance. However, as this industry flourishes, there are numerous challenges in scaling to meet the computational time demands of AI applications on server clusters. These challenges include the power consumption of servers, the required cooling, the generated network traffic, security, privacy, and latency issues, among others.What is less known is that AI scaling has another frontier, which is the downward expansion—IoT edge computing. With this trend of downward expansion, a new type of microcontroller (MCU) has emerged to meet this demand. Many core IP designers and MCU suppliers are turning their attention to how to help customers leverage AI in this new domain to address the challenges of AI in networks.There is a misconception that AI requires large processors with trillions of operations per second (TOPS) performance to fully realize its application performance. While there is some truth to this, it is actually misleading. The higher the processing performance (usually measured in TOPS), the faster AI operations are typically completed. Given the enormous scale of operations executed in today’s cloud data centers, it is easy to believe this. However, not all AI applications have the same performance requirements. Currently, some AI frameworks are optimized for very resource-constrained situations (e.g., IoT AI Edge). This includes platforms based on the TinyML framework, such as Edge Impulse or TensorFlow Lite.First, many traditional MCUs can integrate third-party AI algorithms, although the efficiency is often not high. MCU suppliers and third-party vendors provide tools that can enhance the operational efficiency of AI algorithms. Without hardware acceleration, these tools are referred to as pure software solutions, but they almost always utilize some form of compact, resource-constrained AI framework, such as TinyML. Additionally, these tools can also convert traditional applications to run within AI frameworks, thereby improving efficiency.Second, one strategy MCU suppliers are adopting for edge AI is to use enhanced core architectures to accelerate typical AI algorithms. The core complexes are often multi-core. A typical core architecture may include Arm Cortex M55 or M85, or the recently launched M52, all of which include features for AI.The third strategy is to integrate additional dedicated neural network processing units (NPUs) or AI hardware accelerators to accelerate more complex matrix multiplication operations, thereby meeting the demands of more demanding AI applications while maintaining the power efficiency or cost-effectiveness of microcontrollers.These solutions aim to address significant challenges that cloud or network edge-based solutions may not be able to handle. They can reduce network traffic, lower energy consumption and cooling requirements, decrease latency, and enhance privacy and security. When application scenarios are more limited, such as listening for specific sounds, perceiving events, determining whether operations exceed standards, and using data to identify issues, or various other edge applications, these solutions can be effective. The following image illustrates how this emerging field is rapidly addressing the challenges posed by IoT edge AI. Yole emphasizes that AI capabilities are gradually becoming a key differentiating advantage. As the TinyML framework enables resource-constrained processors and architectures (such as Arm’s M55/M85 or AI-accelerated RISC-V cores) to support machine learning, and these architectures are increasingly being adopted by mainstream suppliers, it is expected that by 2028, AI at the MCU level will cover at least 10% of MCUs. Meanwhile, the automotive industry continues to see a growing demand for high-reliability MCUs to meet safety requirements across various systems, including steering, braking, propulsion, communication, and energy management systems, in compliance with ISO 26262 and AEC-Q100 standards.Electrification is further accelerating the proliferation of MCUs (smart control units), especially in hybrid platforms that require coordination between internal combustion engines and electric power systems. Beyond power systems, consumers also expect full vehicle electrification—from digital lighting to smart seating and cockpit experiences—which will further drive the widespread application of MCUs.

Yole emphasizes that AI capabilities are gradually becoming a key differentiating advantage. As the TinyML framework enables resource-constrained processors and architectures (such as Arm’s M55/M85 or AI-accelerated RISC-V cores) to support machine learning, and these architectures are increasingly being adopted by mainstream suppliers, it is expected that by 2028, AI at the MCU level will cover at least 10% of MCUs. Meanwhile, the automotive industry continues to see a growing demand for high-reliability MCUs to meet safety requirements across various systems, including steering, braking, propulsion, communication, and energy management systems, in compliance with ISO 26262 and AEC-Q100 standards.Electrification is further accelerating the proliferation of MCUs (smart control units), especially in hybrid platforms that require coordination between internal combustion engines and electric power systems. Beyond power systems, consumers also expect full vehicle electrification—from digital lighting to smart seating and cockpit experiences—which will further drive the widespread application of MCUs.