The latest Bernstein research report reveals that the spending on wafer fab equipment (WFE) in China shows strong resilience. The report indicates that China’s semiconductor equipment spending continues to exceed expectations, projected to reach $48 billion by 2025 (an increase of 7% compared to 2024), driven primarily by AI demand, accelerated domestic substitution, and an upturn in memory cycles. Key local equipment manufacturers such as North Huachuang, Zhongwei Company, and Tuojing Technology are expected to benefit from strong industry demand and domestic substitution.

Trend Reversal: Spending Forecasts Revised Upward

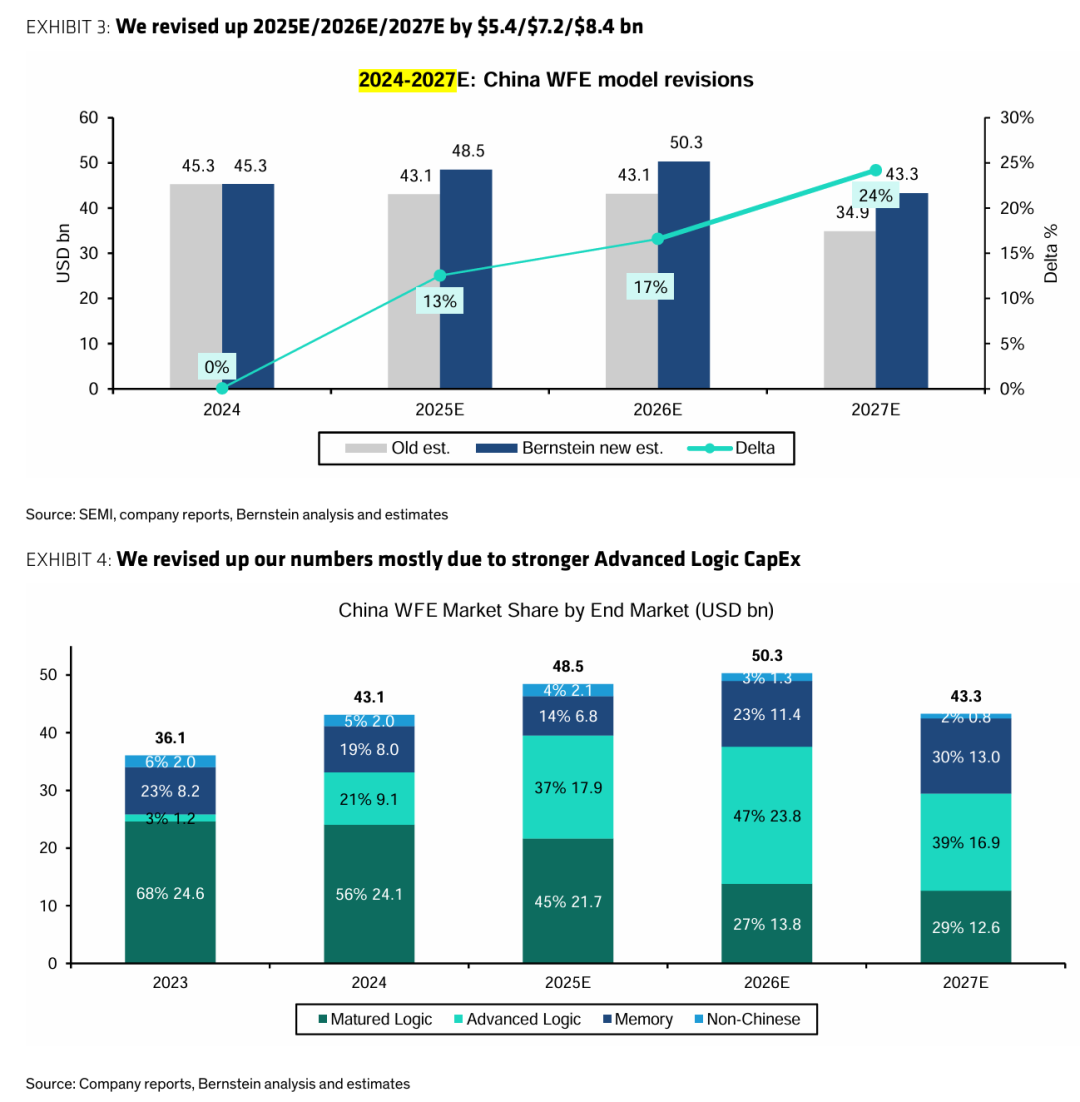

A year ago, the market generally expected China’s WFE spending to decline to $35 billion by 2025. However, actual developments have far exceeded expectations, with Bernstein significantly raising its 2025 forecast to $48 billion, and the 2026 forecast also increased from $43 billion to $50 billion. This indicates that since the export controls in 2022, China’s semiconductor equipment demand will achieve four consecutive years of strong growth.Import data confirms this trend: cumulative imports in October 2025 increased by 7% year-on-year, with a monthly increase of 11% in October alone. Notably, the growth rate of domestic equipment manufacturers exceeded 40%, becoming a significant force driving overall growth.

AI Becomes the Core Driving Force: Three Milestone Events Reshape the Landscape

In-depth analysis shows that artificial intelligence has become the core driving force behind China’s semiconductor equipment spending. Three key events in 2025 have completely transformed the industry ecosystem:DeepSeek Breakthroughdemonstrated that China can still develop excellent AI algorithms in a power-constrained environment, shifting the focus of demand from training to inference, creating an opportunity window for domestic AI chips.H20 Baneffectively excludes Nvidia from the Chinese inference market, opening up greater market space for domestic players.Huawei AI Roadmapshowcases that through innovative network technology, even with performance gaps in single chips, comparable or even superior computing power to international levels can be provided through large-scale cluster deployment, opening doors for domestic AI chips in training scenarios.These developments not only drive the expansion of advanced logic capacity but also stimulate demand for supporting technologies such as HBM and eSSD, further amplifying equipment spending.

Accelerated Domestic Substitution: Technological Breakthroughs and Ecological Synergy

The market share of domestic equipment manufacturers continues to rise, with the self-sufficiency rate expected to increase from 22% in 2025 to 29% in 2026. This trend is particularly evident in the DRAM and mature process logic fields, whereas localization previously focused mainly on advanced logic and NAND fields.Three major factors are driving the acceleration of domestic substitution:Forced Collaborative Developmenthas become a turning point. After the export controls, support for domestic equipment manufacturers shifted from “assistance” to “self-interest driven,” with wafer fabs opening more process interfaces to equipment manufacturers and significantly increasing R&D support budgets.Joint Development Accelerates Technological Improvement. Domestic equipment manufacturers conduct testing and verification on wafer fab production lines, rapidly iterating and optimizing, quickly narrowing the performance gap with global leaders.Government Policy Guidanceencourages increasing the localization rate of equipment through subsidies and fund support. The third phase of the major fund has established a fund of 34.4 billion yuan, focusing on supporting the R&D of bottleneck equipment.

Investment Insights: Focus on Technologically Advanced Domestic Equipment Manufacturers

Analysis shows that against the backdrop of overall WFE spending growth, domestic equipment manufacturers will grow significantly faster than their global peers. Key companies to watch include:Zhongwei Company, a leader in the dry etching field, has its technological strength recognized globally and continues to benefit from the trend of domestic substitution.North Huachuang, with a product line covering deposition, etching, thermal treatment, and more, has a diverse customer base and, as a domestic WFE leader, will benefit maximally from the localization process.Tuojing Technology, focusing on deposition equipment, is strategically positioned in advanced packaging and has an excellent record of product innovation.Among global equipment manufacturers, companies like Tokyo Electron and KLA Corporation still hold competitive advantages in specific technology areas, but overall market share in China is under pressure.

Future Outlook: 2027 May See Normalization Adjustments

Although the growth trend for 2026 is clear, 2027 may become a digestion period. Current forecasts suggest a 14% decline in spending in 2027, but this judgment still carries uncertainties. Continuous observation of the progress in advanced logic production line construction and the localization process in the memory sector is needed.Final analysis indicates that the Chinese semiconductor equipment market has entered a new phase driven by AI demand and domestic substitution, a trend that is expected to continue in the short to medium term.