In 1976, Yang Fu saved money for half a year and sought connections to buy a ticket, finally purchasing a Panda brand semiconductor radio. This small object, which has been discarded by many in memory, was a rare item over forty years ago.

One winter over forty years ago, Yang Fu visited a supply and marketing cooperative and saw a beautiful talking black box on the counter. The salesperson introduced it as a new type of radio, priced at 45 yuan.

Faced with this rare item, Yang Fu looked at it repeatedly and decided to buy the radio from that day on. To afford the radio, the family’s meals were downgraded, and everyone saved for half a year, finally gathering 45 yuan.

When the family excitedly ran to the cooperative, they found that the price of the radio had risen to over 50 yuan. After waiting for half a year, the family couldn’t wait any longer, so they borrowed seven or eight yuan from relatives and friends to make up the money for the radio. However, they still couldn’t bring the radio home because, at that time, purchases required ration tickets. The family sought connections everywhere to obtain tickets and finally brought the radio home.

At dinner time, the family would sit around the radio, listening to storytelling and broadcasts, feeling that life was more flavorful.

Yang Fu felt that saving and being frugal was worth it!

This was the first time the Chinese people became so obsessed with electronic products.

The radio served as a link between the Chinese people and semiconductors. After radios became popular in China, televisions, tape recorders, pagers, VCDs, PCs, and mobile phones gradually entered the homes of the Chinese people.

In this most populous country, the electronic product consumption of the Chinese people has, to some extent, influenced the global semiconductor industry. In fact, a massive electronic market has formed on this land.

The semiconductor industry chain is very long. From a grain of sand to a wafer, then to chips, and finally to electronic products distributed worldwide, the complexity of the process involves numerous personnel, technologies, and resources. Perhaps no other industry can compare. Just looking at components, a component often goes through six stages before reaching the consumer: component – module – OEM – brand – distributor – consumer.

Each stage in this process can affect another stage, and external environments can also impact this long chain, potentially altering the course of history.

History repeats itself, and so does the industry. Looking back at the semiconductor industry dynamics in 2008, we find that they are strikingly similar to the current situation.

After our comparison, we found that TI’s production halt during the Great Recession ten years ago is remarkably similar to Renesas’s recent production halt. We will review these two production halt events that are ten years apart along the timeline. The full text is divided into four parts:

1. The Great Recession of 2008

2. TI’s Production Halt

3. Familiar Production Halts and Recessions

4. Moving Forward in the Quagmire

1

The Great Recession of 2008

Let’s rewind to 2007, when 25 new high-capacity 12-inch wafer fabs joined production, doubling the global capacity of 12-inch wafer fabs by the end of 2008. By the end of 2008, 73 12-inch wafer fabs were producing over 6.2 million wafers per month.

Additionally, Taiwan and Japan ranked first and second in the global expansion of wafer fabs, accounting for 30% and 20% respectively, while mainland China ranked third with over 16%.

The following year, in 2008, the financial crisis spread to China and the semiconductor industry.

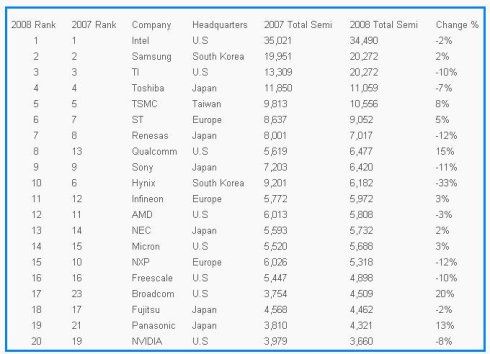

In 2008, the global semiconductor industry declined by 2% due to the financial crisis, totaling $266.61 billion. The revenue of the world’s top 20 semiconductor companies was $166.26 billion (accounting for 62% of the industry), which also decreased by 2.7% compared to the previous year, with six of the top ten companies experiencing revenue declines.

The memory industry was hit hardest that year, experiencing a comprehensive decline of 16.9%, with DRAM plummeting by 19.8%, NOR flash dropping by 16.2%, and NAND flash decreasing by 13.1%.

Among the 29 memory companies with revenues exceeding $100 million, only two were profitable, with the largest decline seen in South Korea’s Hynix, which plummeted by 29.1%, dropping from sixth to ninth place. Larger companies like Samsung and Toshiba also faced declines.

That year, Zhang Lan, who had just entered the chip distribution industry for two years, felt unprecedented pressure since graduation.

“At that time, I even considered changing careers,” Zhang Lan recalled vividly when discussing this experience.

2008 was an extraordinary year. The U.S. debt crisis struck, and the biggest impact on China was the sudden freeze of the external demand market, which was a huge shock for the world’s largest manufacturing country, which relied on export-driven economic growth.

Companies laid off workers and cut salaries, and everyone was called into the office for a “chat.” Zhang Lan also felt the crisis for the first time after graduation. After nervously sipping tea for half an hour, she was luckier than most of her colleagues and kept her job.

At that time, Zhang Lan didn’t even realize she was experiencing a financial crisis; her only feeling was that it was hard to get orders and earn money, while her colleagues discussed falling housing prices and occasionally heard news of someone committing suicide.

Thus, Zhang Lan endured the unforgettable year of 2008 while contemplating a career change and working cautiously.

In the first half of 2008, the global mobile phone market still appeared prosperous, but with the outbreak of the U.S. financial issues, a global economic crisis ensued, causing mobile phone sales to plummet in the second half. The third quarter saw a drastic change in the global market, akin to a blizzard, severely impacting the mobile phone industry. The downturn led to extreme pessimism, with Nokia, then the leading mobile phone manufacturer, issuing two warnings within half a month and lowering its sales forecast for the following year.

According to IDC reports, due to the global economic downturn, mobile phone shipments in the third quarter of 2008 fell sharply, reaching a six-year low of only 303 million units.

All five major mobile phone manufacturers underperformed in the third quarter, whether it was Motorola, which was already in the red, or Nokia, which was performing well at the time, both faced difficulties.

In the third quarter of 2008, Nokia’s gross margin increased in various departments, but net profit fell by 30% to €1.09 billion, and sales dropped by 5% to €12.2 billion. Nokia also restructured its sales and marketing operations and research centers, laying off 450 employees in the marketing department and 130 in the research center.

That year, the 3G version of the iPhone was released, and its market share rose from 11% to 17%, becoming a sensation. It was also in that year that Apple gradually replaced Nokia as the leading mobile phone manufacturer.

On January 7, 2009, China’s Ministry of Industry and Information Technology issued 3G licenses to China Mobile, China Telecom, and China Unicom for TD-SCDMA, CDMA2000, and WCDMA, marking China’s entry into the 3G era.

In the following years, under the leadership of Steve Jobs, Apple gradually ascended to prominence. In 2011, the People’s Daily published a sensational news story: a 17-year-old boy named Wang sold his kidney to buy an iPhone, resulting in severe injury after the removal of his right kidney at a hospital in Chenzhou, Hunan, and he only profited over 20,000 yuan. Many similar cases emerged, where young people sold their kidneys to buy iPhones.

When reporters interviewed these so-called “donors,” their most common response was: “I sold my kidney to buy an iPhone.” Some even expressed desires to buy a year of VIP membership for QQ or other services.

This was another instance of the Chinese people becoming obsessed with electronic products.

2

TI’s Production Halt

In March 2009, without any warning, TI suddenly announced a global production halt for three weeks.

According to TI, the halt was aimed at the global market and not just China;

Secondly, TI’s factories are flexible, and if urgent demand arises, they can adjust strategies and resume production early;

Thirdly, they had prepared adequately, and it would not affect normal deliveries to customers.

Of course, later facts proved that TI was just talking nonsense.

TI’s fourth-quarter financial report showed that revenue dropped from $3.56 billion in the same period of 2008 to $2.49 billion, with a net profit of $107 million, a staggering 85% drop compared to $756 million in the same period of 2007.

At that time, TI’s Vice President of Investor Relations, Ron Slaymaker, stated in an analyst conference call, “The current situation is not just a natural inventory adjustment issue that will improve in three quarters; it is a widespread economic slowdown that has significantly reduced consumption and may continue to decline.”

At that time, the mobile phone market was transitioning from 2G to 3G, and demand was slowing down. According to TI’s order situation, it had been on a downward trend. Customers also strengthened risk control to prevent excessive inventory.

TI’s largest customer, Nokia, also lowered its global mobile phone production forecast for 2009. According to Nokia’s fourth-quarter financial report for 2008, Nokia’s mobile terminal sales were 113.1 million units, a 15% decline compared to the same period in 2007, and a 4% decrease from the third quarter, which was greater than the industry average decline.

To cope with this “prolonged economic weakness“, TI announced a layoff plan of 3,400 employees before the halt.

TI is considered one of the world’s top companies in terms of scale and technology. Although TI’s revenue is not the largest, it has consistently ranked third to fifth globally. TI’s greatest feature is its exceptionally wide product line. If categorized by complete product models, it has tens of thousands, more than the total of companies ranked second to tenth combined.

Because of this characteristic, TI’s products are applied in a very wide range of fields. Basically, anywhere there is electricity, TI’s products may be used (though this is a possibility, not a certainty, as TI faces many competitors), and even the phone in front of you may already be using TI’s products.

Base stations, servers, mobile phones, computers, televisions, medical devices, automobiles, high-speed trains, high-voltage transmission, smart wearables, cash counting machines, servos, PLCs, air conditioners, robots, industrial control, inverters, movies, lighting, new energy, drones, elevators, refrigerators, washing machines, audio equipment, toys, water, electricity, and gas meters… basically, any application you can think of can more or less use TI’s products.

Any company that ranks among the top in China is definitely a key customer of TI. Outsiders may find it unbelievable, but that is the kind of company TI is.

Since China is a major consumer of chips, TI’s sales in China can largely reflect the state of the Chinese economy.

The faster the technological progress, the more pronounced the reflection; the slower the technological progress, the more sensitive the response.

3

Familiar Production Halts and Recessions

Hegel said that major events in history occur twice.

On the eve of International Women’s Day, also known as the day of the artificial goddess, Renesas suddenly announced its impending production halt.

According to Japanese media reports, Renesas Electronics issued a notice at the end of February 2019 announcing that all domestic and foreign factories would intermittently halt operations from April to September 2019 to cope with demand slowdown.

The factories involved in this halt include front-end and back-end factories. According to insiders, Renesas Electronics has a total of 14 factories worldwide, of which 6 front-end factories in Japan will halt for one month at the end of April and another month at the end of August, while three back-end factories will halt for several weeks from April to September.

Additionally, factories in China and Malaysia will also halt for several weeks from April to September. In total, Renesas Electronics will halt 13 of its 14 factories.

Comparing this Renesas production halt with TI’s earlier halt reveals many similarities.

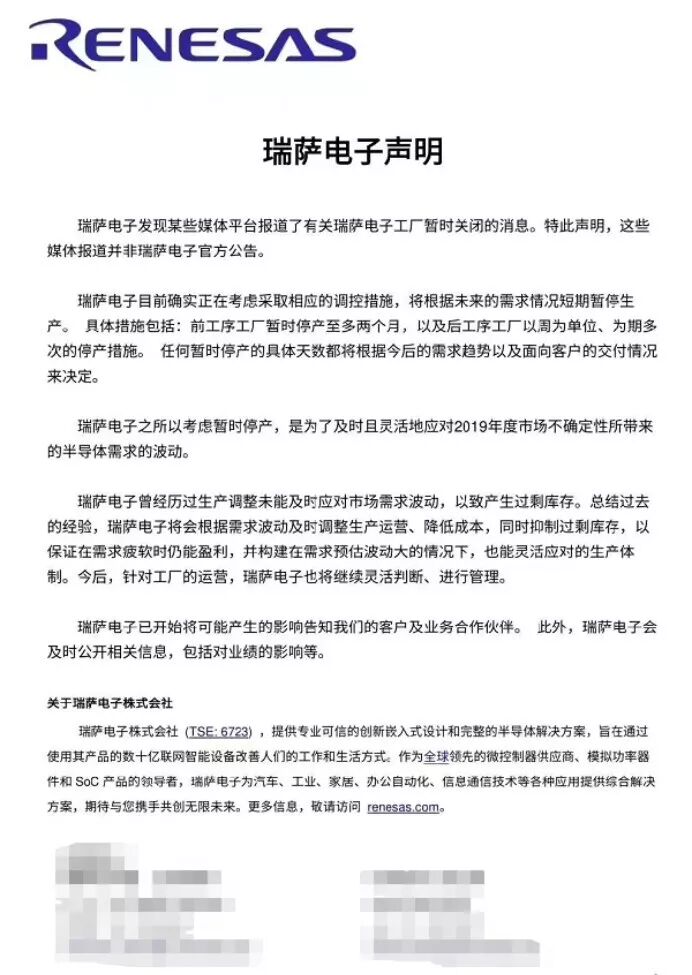

On the evening of March 7, Renesas Electronics issued a statement regarding reports from certain media platforms about the temporary closure of its factories, stating:

From this statement, it can be seen that:

-

Renesas stated that some media reports were unofficial.

-

It acknowledged that Renesas Electronics has a production halt plan, specifically that front-end factories would halt for up to two months, and back-end factories would halt for several weeks at a time.

-

Renesas Electronics’ production halt is due to fluctuations in semiconductor demand caused by market uncertainties in 2019.

-

Renesas Electronics’ production adjustments failed to respond timely to market demand fluctuations, resulting in excess inventory.

-

Renesas Electronics will promptly disclose relevant information, including the impact on performance.

In July 2018, Renesas Electronics saw a significant decrease in purchases from some customers. To alleviate inventory pressure, Renesas Electronics significantly reduced wafer input in August 2018 to adapt to demand changes. However, this also had negative effects on Renesas Electronics. According to the company’s financial report, Renesas Electronics’ revenue at the end of December 2018 was 118 billion yen, a decrease of 23.5 billion yen compared to the end of September.

In fact, Renesas Electronics’ operational difficulties had already shown signs.

In February, Renesas Electronics announced its 2018 financial report. Demand for automotive and factory automation (FA) semiconductor chips softened, dragging down consolidated revenue by 2.9% to 757.4 billion yen, showing a 14.8% decline in operating profit and a 29.3% drop in net profit to 54.6 billion yen.

Specifically, Renesas’ semiconductor business revenue decreased by 3.1% to 740.5 billion yen in the previous year. Automotive business revenue fell by 3.4% to 398.5 billion yen; industrial business revenue decreased by 4.7% to 187.2 billion yen; and general-purpose semiconductor business revenue increased by 0.6% to 151.3 billion yen.

Regarding the decline in performance, Renesas Electronics attributed it to the economic downturn in China, which led to a significant decline in sales of semiconductors used in the automotive market, home appliances, and factory production equipment.

To cope with the difficulties, Japanese media reported that Renesas President Watanabe announced a layoff plan. The number of layoffs is approximately 1,000, scheduled for June 2019.

Renesas Electronics’ main product is the MCU semiconductor, which serves as the control center for automobiles, home appliances, and industrial equipment.

Let’s take a look at recent domestic automobile sales:

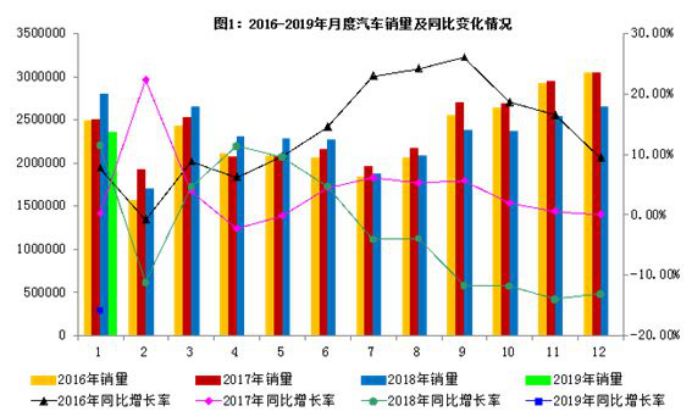

In January, domestic passenger car production and sales reached 1.995 million and 2.021 million units, respectively, down 14.4% and 17.7% year-on-year. Among them, sedan production and sales were 941,000 and 986,000 units, down 14.2% and 14.9% year-on-year; SUV production and sales were 874,000 and 879,000 units, down 15.1% and 18.9% year-on-year; MPV production and sales were 146,000 and 130,000 units, down 17% and 27.4% year-on-year.

After steadily growing for over twenty years, China’s wholesale automobile sales fell by 2.8% for the first time in 2018. In the fourth quarter of 2018, passenger car wholesale volume saw a significant year-on-year decline of 15%, the first decline since the 1990s.

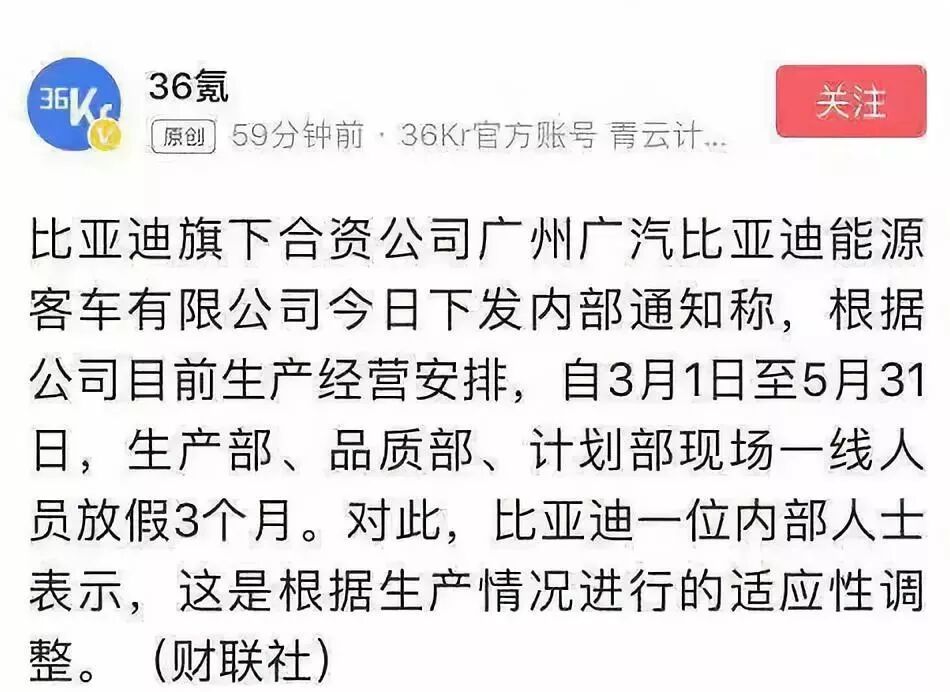

On the evening of March 11, reports emerged that Guangzhou BYD Energy Bus Co., Ltd., a joint venture under BYD, had frontline personnel in production, quality, and planning departments take a three-month leave.

On the same day that women across the country celebrated their holiday, China’s General Administration of Customs released some not-so-optimistic data, stating that in February, China’s total import and export value was $266.36 billion, a decrease of 13.8%.

Among them, exports were $135.24 billion, down 20.7%; imports were $131.12 billion, down 5.2%; and the trade surplus narrowed by 87.2%. Excluding the Spring Festival factor, in February, China’s imports and exports, exports, and imports grew by 3.9%, 1.5%, and 6.5%, respectively.

In the first two months, the import of electromechanical products was 883.91 billion yuan, a decrease of 3.1%. Among them, integrated circuits numbered 54.93 billion, a decrease of 10.8%; and automobiles numbered 150,000, a decrease of 13.5%.

Comparing TI’s production halt with Renesas’s, the reasons for the halt are almost identical: on one hand, the poor economic environment, and on the other, excess inventory. If we compare the situation before the halt, many similarities can be found. It even gives one the illusion of returning to ten years ago.

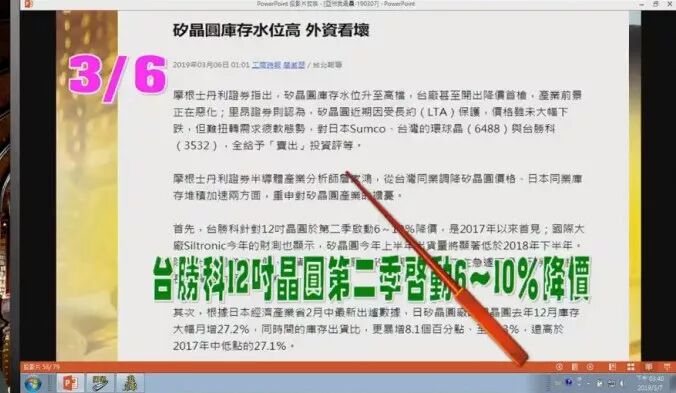

According to SEMI statistics, the total area of silicon wafer shipments in 2018 was 12,732 million square inches (MSI), surpassing the previous market high of 11,810 million square inches in 2017, with an 8% increase from the previous year.

Globally, it was expected that wafer shortages would continue at least until 2020. At the end of February, Taiwan’s major silicon wafer manufacturer, TSMC, decided to lower the prices of some 12-inch silicon wafers by 6% to 10% for the next season, and various wafer fabs were negotiating price reductions with major Japanese manufacturers.

In contrast, by the end of 2018, China’s 12-inch wafer manufacturing plants had an installed capacity of about 600,000 wafers; 8-inch wafer manufacturing plants had an installed capacity of about 900,000 wafers; 6-inch wafer manufacturing plants had an installed capacity of about 2 million wafers; 5-inch wafer manufacturing plants had an installed capacity of about 900,000 wafers; 4-inch wafer manufacturing plants had an installed capacity of about 2 million wafers; and 3-inch wafer manufacturing plants had an installed capacity of about 500,000 wafers.

This is strikingly similar to 2008, when the global sentiment was that wafers would continue to be in short supply, and domestic wafer fabs were expanding significantly, only to suddenly hit the brakes.

Due to persistent oversupply, most transactions for DRAM memory chips have shifted to monthly pricing, and in February, there was a significant price drop, with quarterly declines adjusted from the originally estimated 25% to nearly 30%.

In the first quarter of 2019, NAND contract prices fell by 10% month-on-month, and the downward trend in memory prices is expected to continue. In response to the sluggish market, memory manufacturers have generally stopped increasing production or even reduced output to mitigate the negative impact of insufficient demand.

Both DRAM and NAND environments are almost identical to those in 2008.

After leaving her former employer, Zhang Lan, who now runs her own company, told me: “Many distributors’ warehouses are already filled with goods, and there is significant inventory pressure, and I am also worried about how to sell the stock I accumulated last year.”

It is rumored that various chip manufacturers’ distributors are dumping inventory, and distributors have been given strict orders: whoever has high inventory and cannot manage customers may very well be eliminated. TI’s Q1 performance fell by 10%, NXP’s performance was also dismal, ST’s performance was terrible, and other major manufacturers are not doing much better. Some even say that people from France came to the company, urging their bosses to place orders and pick up goods, but there is simply no demand from customers.

Distributors are filled with goods, traders are filled with goods, and customers are also filled with goods; there is an abundance of goods everywhere!

Not only Zhang Lan, who has been in the industry for over a decade, feels the downturn in the chip market. Recently, in various groups, there are messages about dumping inventory everywhere. Some experienced individuals even told me: “This quarter, clear the inventory; next quarter, basically don’t work. Distributors are filled with goods from the original manufacturers, and distributors are also worried about the stock in their warehouses.”

4

Moving Forward in the Quagmire

Let’s take a look at that glorious Apple from 2008, for which someone even sold a kidney to buy a phone.

On January 3, Apple CEO Tim Cook published an open letter, which was dubbed the most expensive letter in history.

Because on the day this letter was released, Apple’s stock price plummeted by 10%, resulting in a loss of $75 billion in market value in one day, equivalent to 1.33 Baidu (as of January 4, Baidu’s total market value was $56.1 billion).

In this open letter, Cook lowered the revenue forecast for Q1 of fiscal year 2019 (the fourth quarter of calendar year 2018) from the original $89-93 billion to $84 billion, a decline of over 7%.

This was unprecedented since the birth of the iPhone.

As a result, the once arrogant Apple has been bowing to Chinese consumers, lowering prices three times in the past two months for various reasons.

In this journey, Apple, which has gradually replaced Nokia since 2008, seems to reflect a bit of Nokia’s shadow.

As Liang Ning said: Everyone’s presentation is a combination of all their past experiences. In fact, the occurrence of every historical event is also a combination of many environmental factors from the past.

If we take TI and Renesas as the protagonists of this article, before the production halts, wafer expansion, price reductions, declining mobile phone sales, and factory layoffs, both cases are surprisingly similar.

Looking at the timelines of TI’s production halt in 2009 and Renesas’s production halt in 2019, they are ten years apart, both revealing news in March.

Another coincidence is that in 2009, the three major domestic operators welcomed the arrival of 3G, while in 2019, 5G is also on the horizon, with products waiting in incubators for mass production, uncertain of which will be the lucky one.

History repeats itself, but not exactly the same. In 2008, after the 4 trillion yuan stimulus, product demand exploded; what about in 2018? In 2009, Moore’s Law still had room to grow; what about in 2019? In 2008…

Just like ten years ago, no one knows what the future holds; everyone is moving forward blindly. However, the only difference is that ten years ago, there were still glimmers of light, while ten years later, it is pitch black, with nothing.

In 2019, cash is king. We are all moving forward in the quagmire, hoping to become the lucky ones chosen by history, but there are only a few spots for the lucky ones. Only by shedding the burdens we carry can we more easily escape this dark quagmire. For example, the stagnant materials lying in factories and warehouses may very well become a pile of garbage as time passes.

Because no one knows the future direction.

Written by: Shy, Typeset by: Zhang Wei

WeChat Official Account: Chip World (ID: xinpianlaosiji)