1. Overview of Industry Concepts

RTP crystals specifically refer to the key components used in the rapid thermal annealing process—heaters/thermal field core materials. They do not refer to a single type of crystal material (such as quartz crystals), but rather a functional term that typically denotes ceramic or crystal materials capable of withstanding extremely high temperatures (over 1000°C) while maintaining excellent thermal stability, uniformity, and longevity, such as silicon carbide, aluminum oxide, and yttrium-stabilized zirconia.

Industry Chain Positioning: RTP crystals are located upstream in the semiconductor industry chain—within the materials and equipment segment. Their downstream applications are directly in rapid thermal annealing equipment used in semiconductor manufacturing, which is an indispensable part of the front-end processes (such as post-ion implantation annealing and thin film densification) in chip manufacturing. Therefore, the performance of RTP crystals directly determines the uniformity, efficiency, and yield of thermal processing, making them the “unsung heroes” of high-end semiconductor manufacturing.

2. Market Characteristics

-

High Technical Barriers: The manufacturing of RTP crystals involves complex processes such as the formulation of high-performance ceramic materials, precision molding, high-temperature sintering, and precision machining, resulting in a very high technical threshold that requires long-term R&D and experience accumulation.

-

Strong Customer Binding and Long Certification Cycles: Once certified by semiconductor equipment manufacturers (such as Applied Materials, Axcelis) or end chip manufacturers (such as SMIC, Yangtze Memory Technologies), a stable supply chain relationship is formed. The costs and risks of changing suppliers are extremely high, leading to certification cycles typically lasting 1-2 years.

-

Relatively Niche but Crucial Market Size: Compared to bulk semiconductor materials like photoresists and silicon wafers, RTP crystals represent a typical “small but refined” market. However, their performance has a decisive impact on the electrical parameters, reliability, and yield of chips, making their strategic value far greater than their market size.

-

High Gross Margin and High Added Value: Due to technical barriers and customer stickiness, qualified RTP crystal products have very high gross margins, making it a typical capital and technology-intensive industry.

3. Current Industry Status

-

Global Landscape: The global RTP crystal market has long been dominated by a few companies from the United States, Japan, and other countries (such as Momentive Performance Materials in the U.S. and Covalent Materials in Japan). They occupy a significant portion of the global market share due to their first-mover technological advantages and extensive patent portfolios.

-

Current Situation in China: Import Dependence and Emergence of Domestic Substitution

-

High Dependence on Imports: The RTP crystals used in China’s high-end semiconductor production lines are almost entirely reliant on imports, creating a potential “bottleneck” in the supply chain.

-

Strong Policy Drive: Under the national “14th Five-Year Plan,” “Made in China 2025,” and the backdrop of “semiconductor localization,” RTP crystals, as key semiconductor components, have received unprecedented policy and capital attention.

-

Emergence of Local Enterprises: A number of leading domestic advanced ceramic material companies (such as China Steel Luoyang Institute, Shanghai Institute of Silicate, and their industrialization companies) are actively investing in R&D, achieving breakthroughs in laboratory stages and some mature processes, and beginning to send samples for verification to domestic equipment manufacturers and wafer fabs, marking the initiation of domestic substitution from “0 to 1.”

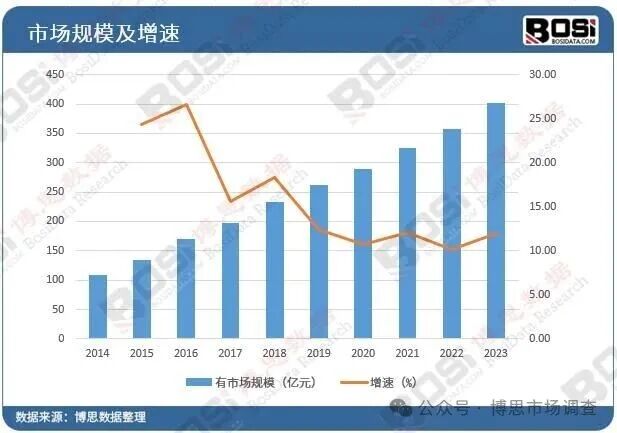

Strong Market Demand: With the continuous expansion of wafer production capacity in China (such as new production lines from SMIC, Huahong Semiconductor) and the rapid development of third-generation semiconductors (SiC, GaN), the demand for RTP processes has surged, directly driving the demand for high-performance RTP crystals.

4. Future Trends

-

Acceleration of Domestic Substitution as the Main Theme: Under considerations of geopolitical and supply chain security, domestic wafer fabs have a strong motivation to cultivate local supply chains. The next 3-5 years will be a critical window for the domestic substitution of RTP crystals, and local companies with technical strength will face explosive growth opportunities.

-

Technological Evolution Towards More Advanced Nodes: As logic chips advance to 3nm/2nm and memory chips develop towards higher stacking layers, the thermal budget control and temperature uniformity requirements for RTP processes have become almost stringent. This drives RTP crystal materials to develop towards higher purity, better thermal performance, and longer lifespan.

-

Third-Generation Semiconductors Bring New Growth: The manufacturing of silicon carbide (SiC) power devices requires extremely high annealing temperatures (>1500°C), which poses new challenges and demands for RTP crystals, also opening new avenues for companies with technological reserves in ultra-high temperature materials.

-

Collaborative Innovation in the Industry Chain: In the future, the collaborative R&D between RTP crystal material suppliers, equipment manufacturers, and wafer fabs will become closer to jointly define product specifications and solve cutting-edge process challenges.

5. Challenges and Opportunities

Challenges:

-

Technical Gap: There is still a gap between domestic products and international top levels in terms of material consistency, reliability, and lifespan.

-

Talent Shortage: There is a severe shortage of top R&D and engineering talent with interdisciplinary knowledge (materials science, semiconductor physics, thermodynamics).

-

High Capital Investment: The investment in R&D and production lines is substantial, and the return cycle is long, posing a severe test for the financial strength of enterprises.

-

Customer Trust: Breaking the brand barriers of international giants and gaining the trust of downstream customers requires time and the accumulation of successful cases.

Opportunities:

-

Huge Domestic Market Space for Localization: Even replacing just 10% of the import market represents a multi-billion-level blue ocean market for local enterprises.

-

Dual Support from Policies and Capital: National big funds, local industrial funds, and an active capital market are actively laying out the semiconductor materials field, providing ample “ammunition” for outstanding enterprises.

-

Possibility of Technological Leapfrogging: In emerging fields such as third-generation semiconductors, the gap between domestic and international starts is relatively small, providing strategic opportunities for Chinese enterprises to leapfrog.

-

Complete Local Industry Chain Ecosystem: China is building a complete semiconductor industry chain from design, manufacturing to packaging and testing, providing an unparalleled testing ground and application ecosystem for upstream material companies.

In this process, Bosi Data will continue to pay attention to industry dynamics, providing accurate and timely market analysis and advice for related enterprises and investors.

Chapter 1Overview of the RTP Crystal Industry

Chapter 2Analysis of the Development Environment of the RTP Crystal Industry

Chapter 3Analysis of Supply and Demand in China’s RTP Crystal Industry

Chapter 4Current Status and Trend Forecast of RTP Crystal Industry Technology Development (2024-2025)

Chapter 5Analysis of Overall Development of China’s RTP Crystal Industry (2019-2024)

Chapter 6Research on Key Regional Markets of China’s RTP Crystal Industry (2019-2024)

Chapter 7Analysis of Price Trends and Influencing Factors of Domestic RTP Crystal Products

Chapter 8Analysis of Related Industry Development of China’s RTP Crystal Industry (2025)

Chapter 9Research on Key Enterprises in the RTP Crystal Industry

Chapter 10Recommendations for Competitive Strategies of Enterprises in China’s RTP Crystal Industry

Chapter 11Investment Barriers and Risks in China’s RTP Crystal Industry (2025-2031)

Chapter 12Development Trends and Project Investment Recommendations in the RTP Crystal Industry

For the complete report directory, please click on “Read the original text” below.