Today, humanoid robots have once again taken center stage, with multiple themes related to humanoid robots receiving significant funding boosts, such as PEEK materials rising nearly 6%; reducers increasing over 3%, and humanoid robots climbing over 2.6%. These three sectors ranked TOP1, TOP3, and TOP10 respectively among more than 260 concept sectors on that day.Short-term Rotation: Robotics in the “Value Gap” is Expected to Take Over from AI

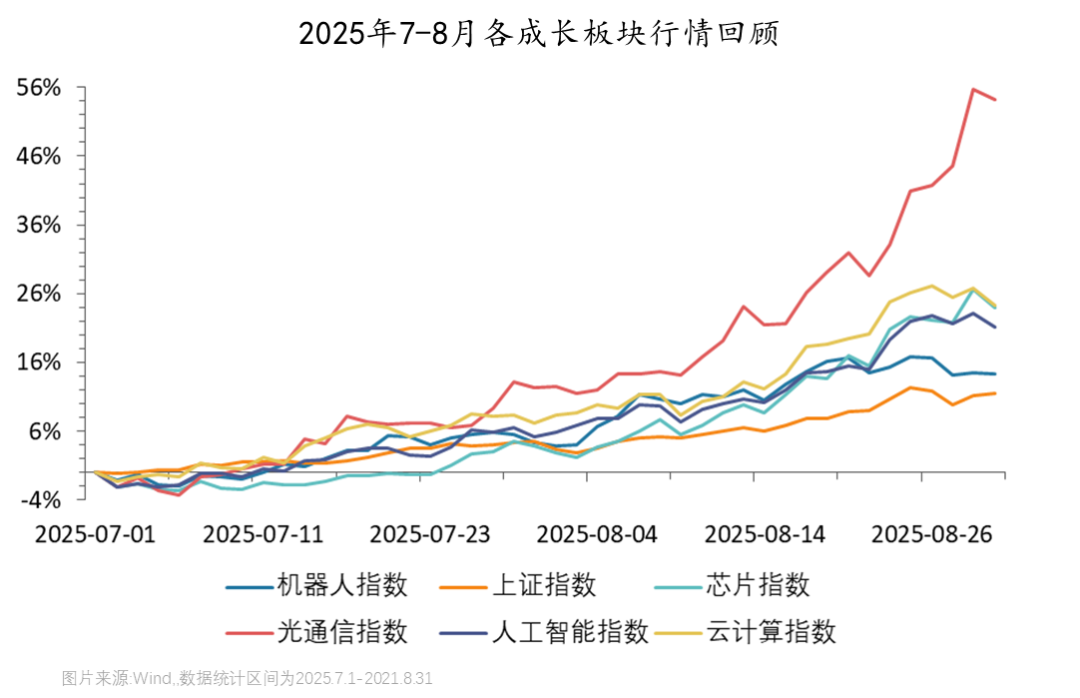

Looking back at the market uptrend in July and August, funds focused on chips and AI, with related ETFs reaching historical highs, while the robotics sector lagged behind, far from the gains of chips and AI.

Recently, with significant corrections in AI and chips, whether the robotics sector can develop an independent market trend requires us to clarify the connection between AI and robotics, and grasp the context of sector rotation, which may allow for a more composed approach.

Chips, AI, and robotics can be viewed as a closely connected industrial development line:

Chips are the foundational base:Chips provide the computational power support for AI, serving as the physical basis for AI model training, data processing, and algorithm optimization. The development of high-performance chips drives breakthroughs in AI technology, such as NVIDIA’s GPUs being widely used in deep learning; at the same time, the miniaturization and low-power design of chips also promote the lightweight and intelligent design of robots.

AI is the core engine:AI technology endows robots with perception, learning, and decision-making capabilities, determining the “intellectual ceiling” of robots. Through computer vision, natural language processing, and other AI algorithms, robots can recognize their environment, understand instructions, and act autonomously. For example, Tesla’s Optimus robot achieves visual navigation and complex task execution through AI algorithms.

Robots are the application interface:As devices with a physical form, robots provide a tangible medium for AI technology to interact directly with the real world, transforming virtual intelligence into actual physical actions, such as the precise operations of industrial robots on production lines and the interactions of service robots with humans, making robots the concrete “interface” for AI technology to penetrate various industries.

In this industrial growth line, whether it is technological breakthroughs, favorable policies, capacity releases, or high performance growth, various positive factors upstream will transmit and interact with downstream. Specifically, AI is the core driving force, and after computational power, there will inevitably be robots. Currently, the investment logic in the computational power sector has significantly improved, and the optimization of large model capabilities is gradually accumulating from quantitative changes to qualitative changes. As the explosion of AI applications approaches dawn, humanoid robots, as core AI applications, will also benefit. Therefore, in the prosperous cycle led by AI technology, robots may arrive late, but they will not be absent.

Unlike the “blooming flowers” style speculation in the robotics sector at the beginning of the year,the robotics sector is currently at a critical “turning point” for mass production release and commercialization. In the future, market funds will focus more on companies with actual revenue.Just as the chip industry benefits from the explosion of computational power demand, with clear performance in sub-sectors like optical modules, AI large model companies are rapidly advancing application landing under policy support, which can quickly reflect in financial reports. Thus, the “smart money” in a bull market prioritizes investments in computational power construction and model development that yield faster results; while most companies in the robotics industry have yet to form scaled revenue, so stock price reactions may lag.

Currently, with significant pullbacks in growth sectors like AI and chips, a “value gap” is needed to absorb the heat and overflow of funds from AI, and at this time, the robotics sector may be worth paying attention to.Especially recently, Yushu Technology announced that it will submit an IPO application in the fourth quarter, and UBTECH also announced that it has obtained a 250 million yuan robot contract.

Every round of structural bull market in the A-share market is deeply engraved with the imprint of the era’s development: 2014-2015 was the Internet+, 2017 was the sharing economy, 2019-2020 was 5G communication and domestic substitution, and 2021 was electric equipment and new energy vehicles. History does not repeat itself, but it progresses with similar rhythms. As the baton of the era passes to the present, the AI and robotics industries are at a critical moment of transitioning from 0-1 to 1-10, and the commercialization landing will open up a prosperous mainline market, thus driving a leap in penetration rates.

Source: Huaxia Fund Note: The above content is for reference only and does not constitute specific investment advice. The stock market has risks, and investment should be cautious.Wealth and Friends Studio

Host: Hangban Danyang Lin Shuo Lu YiOrganizer: Zhang Yumei Review: Ruo Wen Final Review: Lai Ting

Host: Hangban Danyang Lin Shuo Lu YiOrganizer: Zhang Yumei Review: Ruo Wen Final Review: Lai Ting