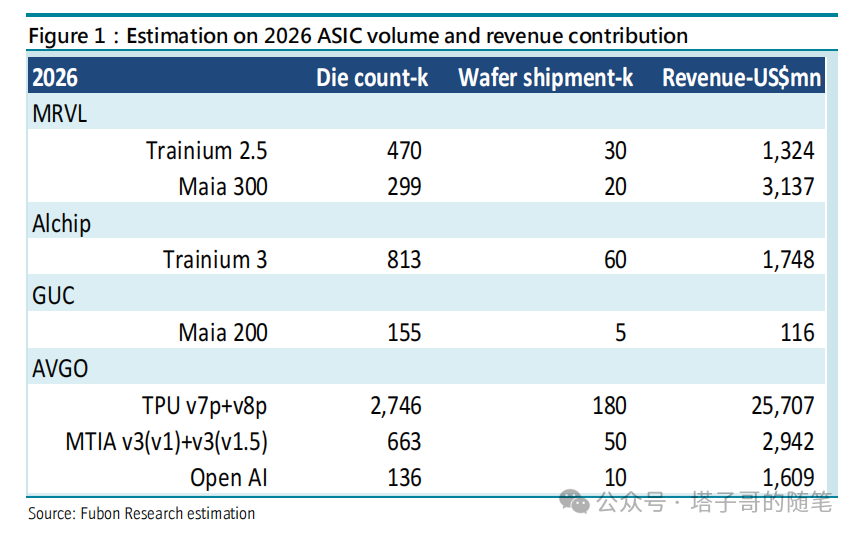

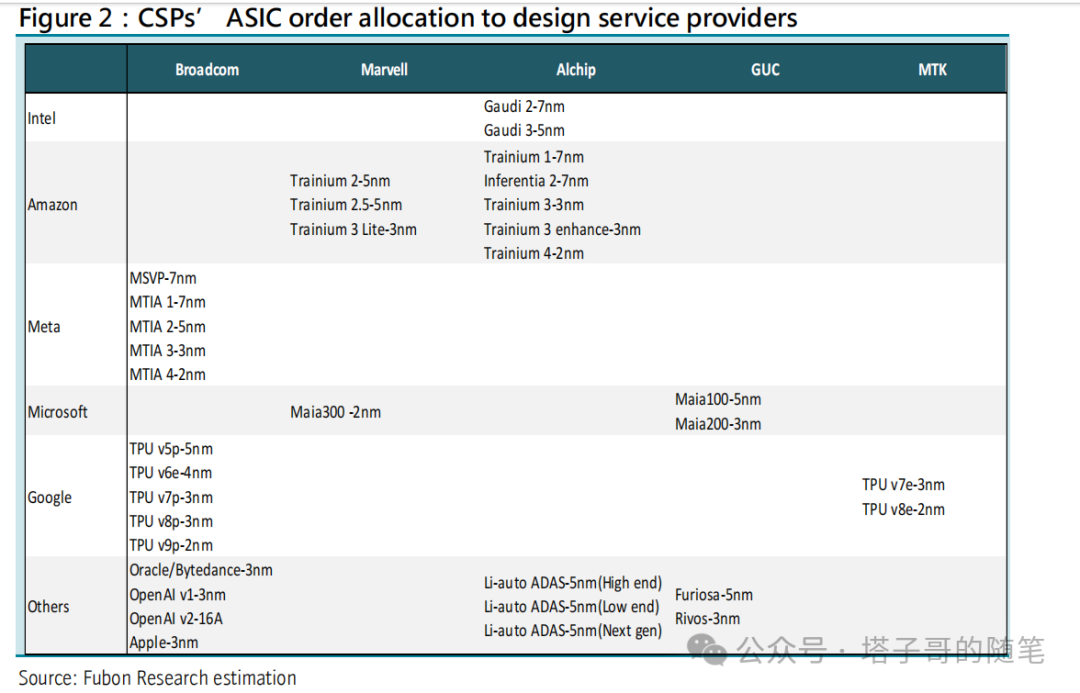

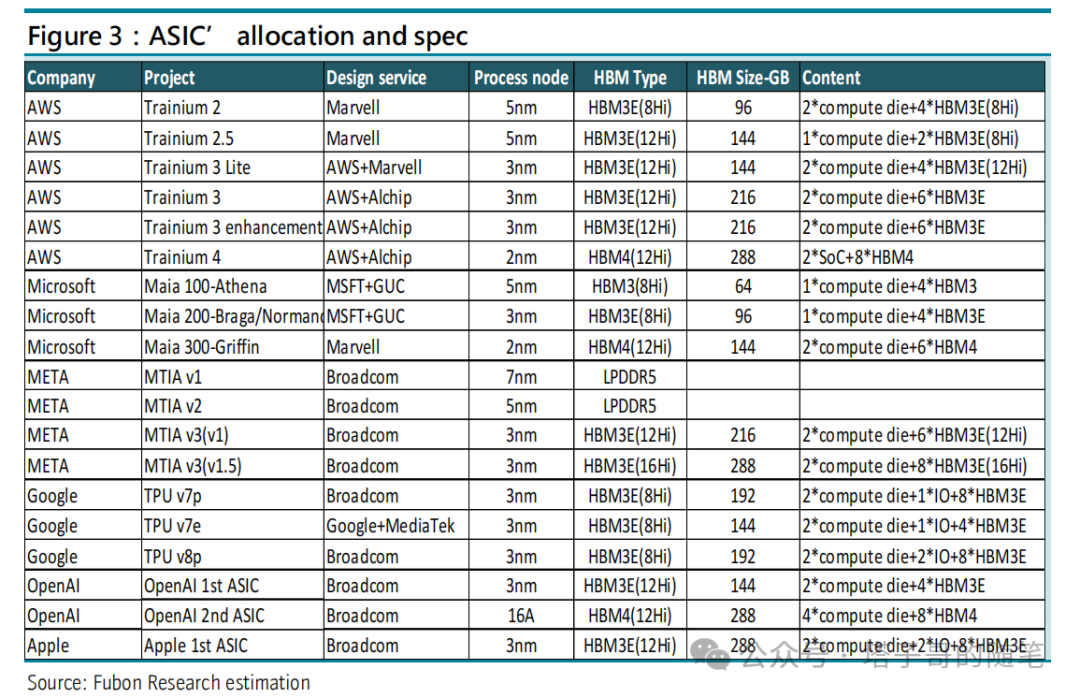

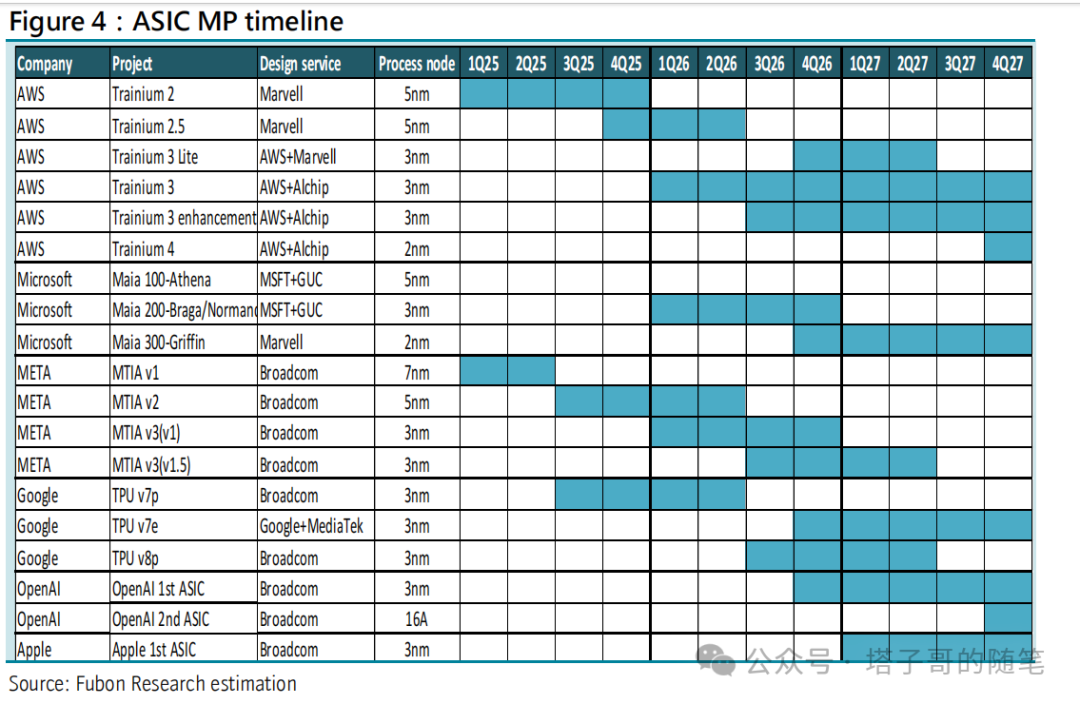

Recently, there has been extensive discussion regarding Google’s new technology, the upward revision of TPU demand, and the requirement to establish servers. Many institutions have revised their forecasts for related custom chips and servers, along with connectivity calculations. Jefferies pointed out in its latest report that the custom chips from Google, Meta, and other tech giants are thriving, which is beneficial for companies like Broadcom and Marvell. Google’s TPU forecast continues to be revised upward: Google has achieved significant success in AI development, and the TPU is undoubtedly a key factor supporting its growth. Previously, we believed that Google’s ASIC development had matured, and there should not be any unexpected changes in quantity. However, in this quarter’s update, we have significantly raised our 2026 TPU quantity forecast from 1.8 million to 2.7 million. Over the past few months, we have observed a continuous monthly upward adjustment in the TPU quantity forecast. The capacity quotas secured by upstream wafer fabs have gradually increased from 1.2 million, 1.5 million, 1.8 million to the current level of 2 million, and this growth trend has not stopped. According to our research, Google/Broadcom currently requires capacity to reach 2.7-2.8 million units. We believe this target is highly likely to be achieved for the following reasons: (1) Google has always been a primary ASIC customer in CoWoS packaging technology, and recent development progress has been smooth. Capacity allocation will be gradually implemented based on customer priority and end-market demand, and Google has fully met the standards in all aspects; (2) The monthly rolling forecast mechanism allows for timely adjustments to capacity planning, which is precisely why we continue to see upward revisions in forecasts. As visibility improves, wafer fabs will secure more capacity quotas. According to our research, the current supply chain can fully meet the demand of Google/Broadcom for 2.7-2.8 million units. Meta launches 2nm ASIC side projects: As mentioned in our previous report, Meta has consistently adopted an aggressive strategy in ASIC development. From its 5nm to 3nm process ASIC products, the average selling price has increased fivefold, and shipments have nearly doubled. Meta’s initiative to start side projects at the 2nm process node exceeds our expectations once again. According to our research, its 2nm generation will initiate two ASIC projects, both expected to begin mass production in the second half of 2027. The high-end project Olympus will continue to be outsourced to Broadcom, as Meta aims to create the most powerful ASIC chips—each chip will feature 2 compute dies and 12 HBM3E high-bandwidth memory (12-layer stacking). Currently, few cloud service providers have attempted to configure 12 HBM, and Meta is expected to be the first company to adopt this configuration. On the other hand, for the low-end project, Meta is exploring the possibility of using a customer-owned technology model, where its internal team will handle front-end design, while back-end design will be outsourced to third parties. Supplier selection is currently underway, with bidders including Marvell Technology, MediaTek, Alchip, and GUC. We refer to this as a “side project.” Although its scale may not match Olympus, it is expected to bring high unit price returns for the competing design service suppliers, making it worth pursuing vigorously. Updates on other key ASIC projects: Our forecast for AWS’s 2026 ASIC remains largely unchanged. Since AWS is a secondary ASIC customer, its ability to secure more CoWoS capacity depends on other customers releasing allocation quotas or AWS adjusting its product mix. According to our research, AWS is considering upgrading the Trainium chip directly from the 2.5 generation to the 3rd generation architecture. OpenAI’s ASIC forecast remains unchanged, with mass production expected to begin in the fourth quarter of 2026, reaching a scale of 136,000 units.xAI’s ASIC project has extremely low visibility, making it impossible to make reliable predictions at this time. The most significant changes are in Apple’s ASIC project. According to our research, this project has been delayed due to internal strategic disagreements—some teams believe that self-developed ASICs are crucial, while another faction insists that the purchased NVIDIA GPUs are sufficient to meet demand. Given the current progress, the likelihood of Apple achieving mass production of ASICs in 2026 is extremely low. Among emerging ASIC projects, Oracle’s ASIC is worth noting. According to our research, its mass production time may fall between 2027-2028, with the end customer likely being a certain Chinese hyperscale enterprise. Relevant charts are as follows:

Complete reports, other foreign research reports, the latest research minutes, macro data interpretation, and trading opportunities have been updated. We welcome everyone to join the discussion: