Authors: Qin Han, Wang Yuchen

Authors: Qin Han, Wang Yuchen

Core Viewpoints:

The recent issue of credit asset scarcity has significantly eased, and the liquidity environment is likely to remain loose, favoring short-duration leveraged strategies in credit bonds. First, the leverage spread is gradually widening. Second, monetary policy is unlikely to tighten in the short term, and liquidity will continue to be loose. Third, the leveraged strategy for short-duration (around 1.5 years) credit bonds combines both yield and certainty.

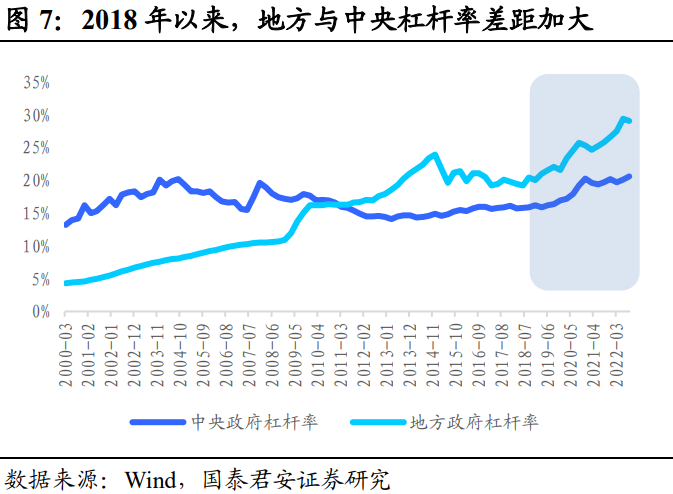

Urban investment bonds benefit from multiple positive factors, and concerns about credit risk are diminishing. (1) The government is increasing leverage, and government bonds and broad fiscal tools may be further enhanced. (2) The optimization of epidemic prevention policies continues, reducing the fiscal burden on local governments. (3) Real estate policies are being strengthened, improving expectations for land finance. (4) In the second half of 2023, the economy is expected to shift from recovery to prosperity, with increased on-balance-sheet income for local governments alleviating their fiscal burdens.

The essence of real estate is the credit cycle. Before housing prices return to a price that reflects their true commodity nature, more attention should be paid to the expansion and contraction of the credit cycle. Under the collateral guarantee model, some real estate companies still face pressure to shrink their balance sheets, while weaker state-owned enterprises exhibit strong resilience and some yield space, making them suitable for investment.

Overall, financial bonds are primarily passively allocated: under the new regulatory rules, the structure of subordinated debt holdings is facing adjustments. Coupled with the increased risk of a bond market correction in 2023, banks’ subordinated capital bonds and perpetual bonds will primarily be passively allocated to avoid tail risks.

Risk Warning: Unexpected tightening of monetary policy, economic recovery exceeding expectations.

Body

1. The overall cost-effectiveness of credit bonds has improved, recommending short-duration leveraged strategies under loose liquidity

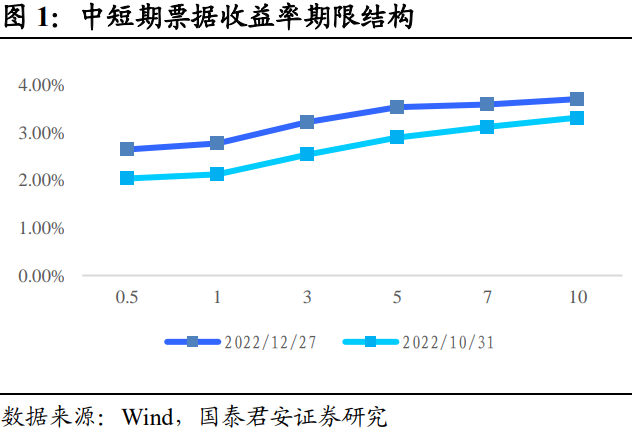

Recently, due to the optimization of epidemic prevention policies and the strengthening of real estate policies, the bond market has experienced adjustments. Coupled with negative feedback from financial product redemptions, some liquid credit bond varieties have seen larger adjustment amplitudes. After a prolonged increase of one and a half months, the average interest rate adjustment amplitude reached around 100 basis points, significantly alleviating the previous scarcity of credit bond assets.

The overall spread of medium and short-duration credit bonds favored by institutional investors has increased significantly. After the new asset management regulations, institutions prefer medium and short-duration credit bonds, making the interest rate curve more likely to exhibit “bull steep” and “bear flat” shapes. Since the second quarter of 2022, influenced by liquidity easing, short-end yields and spreads have generally declined, leading to a phenomenon of credit asset scarcity. Since November, the bond market adjustments combined with financial product redemptions have led to larger adjustment amplitudes for liquid medium and short-end varieties.

After the new asset management regulations, the large asset management industry has returned to the same starting line, and institutional behavior has become more homogeneous, with a rising preference for medium and short-duration credit bonds. Therefore, during periods of liquidity easing, the short end is more likely to see collective buying, and the primary market may experience oversubscription, with some subscription multiples exceeding 5 or even 10 times; conversely, during marginal liquidity tightening, the impact of institutional behavior may lead to a significant increase in short and medium-end yields.

The issue of credit asset scarcity has significantly eased, and the overall cost-effectiveness of credit bonds has improved. With the recent overall adjustment of credit bond yields, the selection of bonds with yields above 3.5% for one-year terms is gradually increasing, whereas in the second and third quarters of 2022, credit bonds with 3% yields were hard to find, indicating that the issue of credit asset scarcity is gradually alleviating.

Bond issuance is unlikely to increase significantly in the short term, and supply and demand will remain tightly balanced. For insurance funds and other allocation-type funds, the absolute yield levels are already attractive. High-quality credit bonds remain important core assets, and due to interest rate adjustments, the balance of corporate financing costs may tilt from bond financing to bank loans, making it difficult for bond issuance to increase significantly in the short term, and supply and demand will remain tightly balanced. For insurance funds and other allocation-type funds, the current absolute yield levels of credit bonds are attractive, and during this period, insurance companies are actively selling their New Year products, alleviating the pressure on the asset-liability matching of incremental funds.

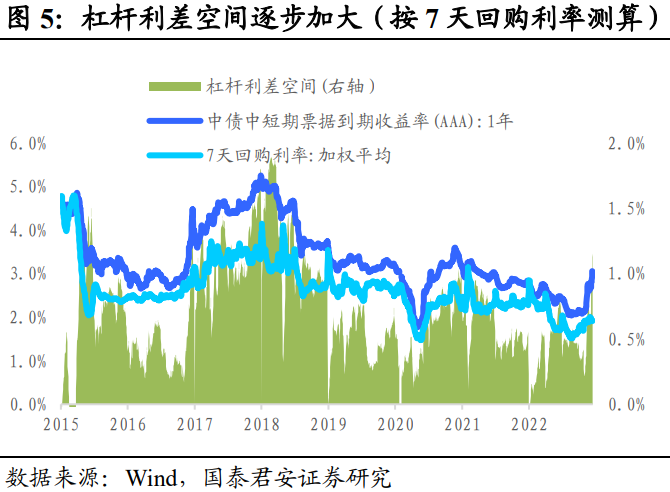

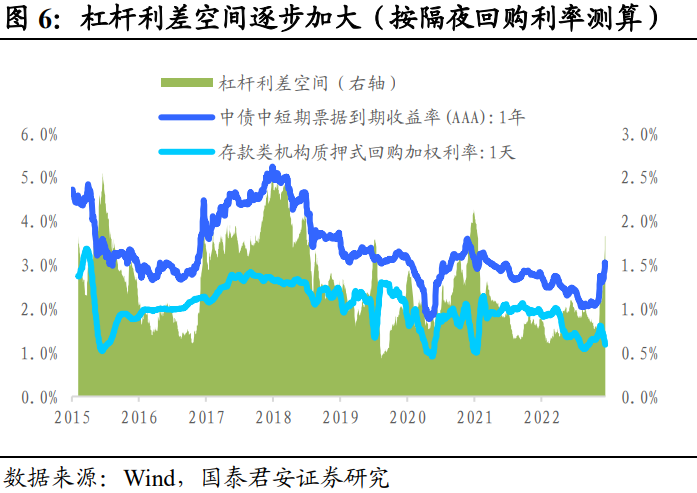

Liquidity is likely to remain loose, favoring short-duration leveraged strategies in credit bonds. First, the leverage spread is gradually widening. Based on the 7-day repurchase rate, the current spread between one-year medium-term notes and the 7-day repurchase rate has reached 100 basis points, a new high since 2018. Based on the overnight repurchase rate, the current spread between one-year medium-term notes and the overnight repurchase rate has reached 180 basis points, a new high in nearly two years.

Second, monetary policy is unlikely to tighten in the short term, and liquidity will continue to be loose. Under the “weak reality, strong expectations” scenario, coupled with the issue of financial product redemptions, monetary policy will maintain a loose tone, and market repurchase rates will remain below policy rates, with liquidity easing expected to continue for some time.

Third, the leveraged strategy for short-duration (around 1.5 years) credit bonds combines both yield and certainty. From an absolute point of view, the interest rate spread for holding credit bonds around 1.5 years to maturity is relatively certain. Even if the holding period is less than one year, the probability of success in a carry trade is relatively high. Therefore, attention can be paid to the carry trade space of short-duration credit bonds.

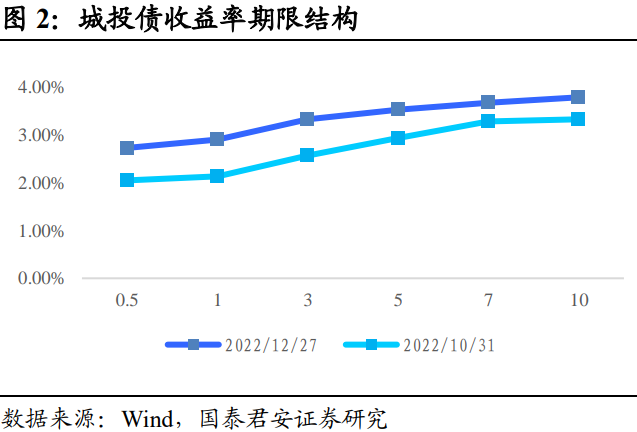

2. Credit Bond Selection: Short-Duration Urban Investment Bonds and Weak-Quality State-Owned Enterprise Real Estate Bonds

2.1 Urban Investment Bonds: Multiple Positive Factors Resonating, Diminishing Concerns About Credit Risk, Recommending Short-Duration Downward Strategy

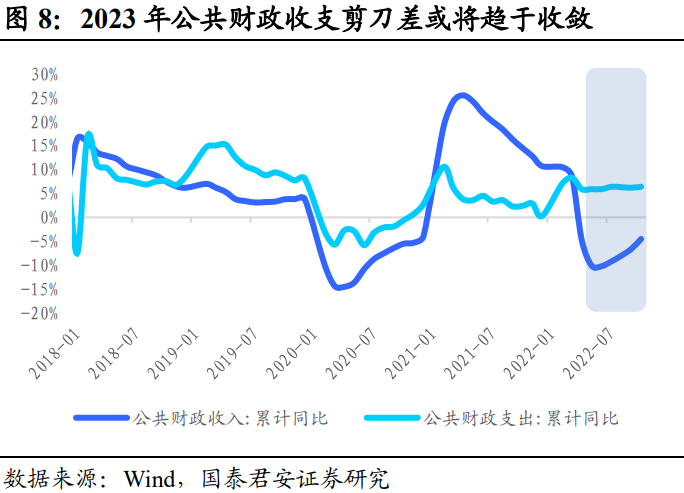

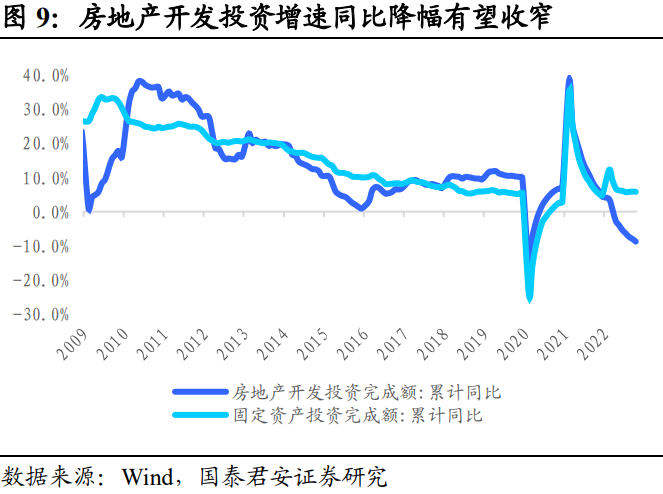

Urban investment bonds benefit from multiple positive factors, and concerns about credit risk are diminishing: (1) The government is increasing leverage, and government bonds and broad fiscal tools may be further enhanced. In the early stages of economic recovery, the government will take on more leverage responsibilities, whether through budgeted government bonds or off-budget broad fiscal tools, which may be further enhanced. (2) The optimization of epidemic prevention policies continues, reducing the fiscal burden on local governments: Since November, the optimization of epidemic prevention policies has continued, and public health expenditures of local governments in 2023 may stabilize or decrease, with the scissors gap between public fiscal revenues and expenditures expected to converge. (3) Real estate policies are being strengthened, improving expectations for land finance: The land market is currently in a “weak reality, strong expectations” phase. In 2022, land transfer revenue in most regions significantly declined, and urban investment has shown a clear bottoming trend. In 2023, land auctions in core cities will warm up first. (4) In the second half of 2023, the economy is expected to shift from recovery to prosperity, with increased on-balance-sheet income for local governments: As the economic fundamentals gradually recover, local government tax revenues and land transfer revenues are expected to bottom out and rebound, with increased on-balance-sheet income alleviating local fiscal burdens.

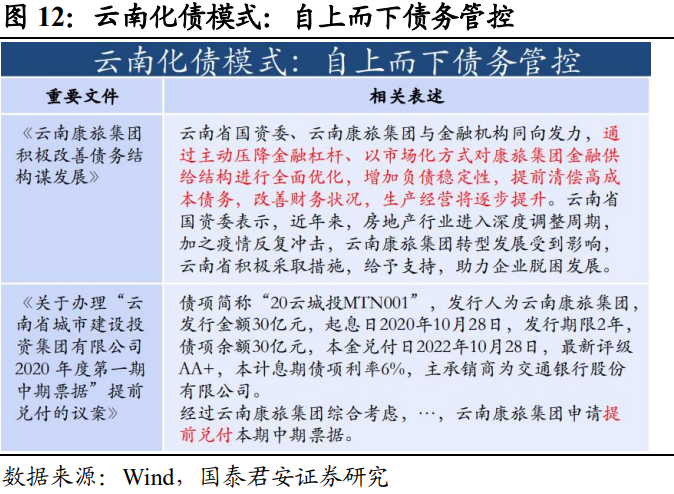

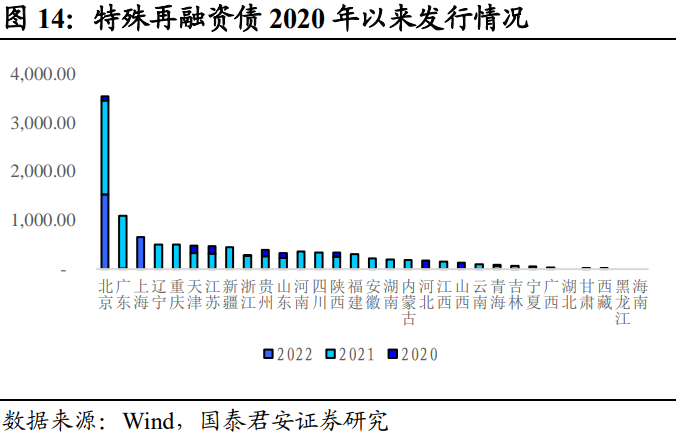

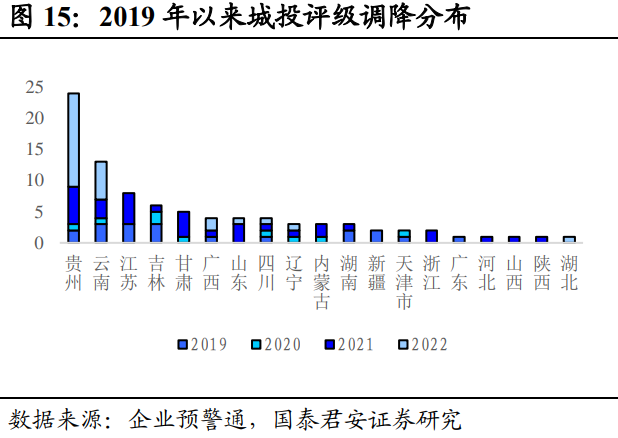

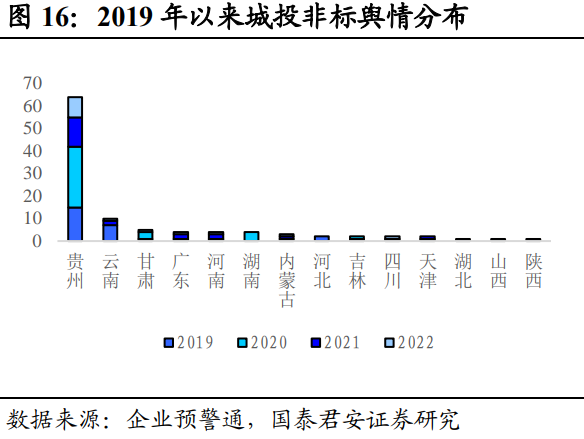

Urban investment bond outlook one: Transitioning from refinancing to debt restructuring, further clarifying the main line of cost reduction. The logic of short-term financing for urban investment bonds is changing. As the marginal effect of infrastructure multipliers weakens, the effectiveness of infrastructure investment is becoming difficult to cover the financing costs of high-debt areas. Regions such as Yunnan and Guizhou are gradually promoting debt restructuring for non-public bonds. It is expected that in 2023, the scope of debt extension and restructuring will expand to more regions.

Debt negotiations need to consider the needs of the government, financial institutions, and platform companies. Government-led debt control is easier to promote, with a focus on the support of local financial resources for urban investment platforms. If platform companies can achieve a dignified exit after public debt repayment, it will further enhance the safety margin of urban investment bonds.

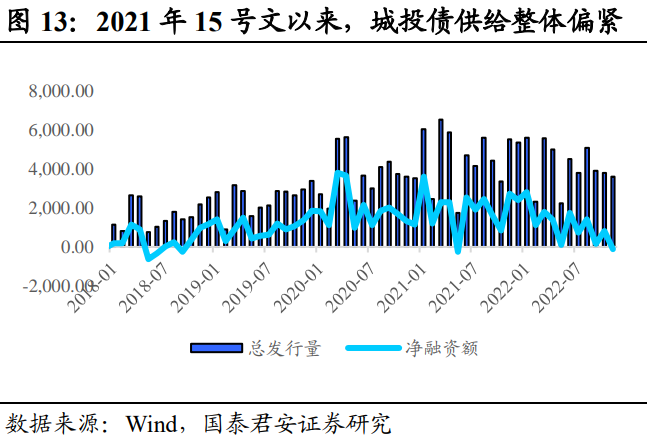

Urban investment bond outlook two: Under strict regulation of hidden debts, the financing environment will remain tight. In the past, special refinancing bond issuance was mainly divided into two phases: (1) Pilot projects for resolving hidden debt risks in established counties (2) Pilot projects without hidden debts in regions. In the coming years, the strict regulatory framework for local government hidden debts will continue. Against the backdrop of weak economic fundamentals in 2022, the Ministry of Finance reported cases of accountability for hidden debts twice, indicating that local governments must not incur new hidden debts as a bottom line. In the coming years, the consolidation, transformation, and replacement of hidden debts for urban investment platforms will continue. Additionally, after bank wealth management funds return to the balance sheet, there will be strong demand for bank lending, which may suppress the supply of bonds. Therefore, in 2023, the supply of urban investment bonds will remain tight.

Urban investment bond outlook three: Short-term and medium-term investment logic returns to fundamentals. Since the second quarter of 2022, influenced by liquidity easing, ample liquidity has chased core assets, leading to a general decline in urban investment bond yields and spreads. Under the backdrop of weak economic fundamentals and the real estate cycle, urban investment has become an important credit issuance vehicle, with a clear phenomenon of market collective buying. In the investment logic of 2023, attention to economic fundamentals is increasing. As economic fundamentals gradually recover and monetary policy tightens marginally, the focus on economic fundamentals is expected to rise, benefiting urban investment bonds in provinces and cities with steep recovery slopes due to improved government financial strength.

Recommending a short-duration downward strategy for urban investment bonds, suggesting attention to two investment lines: (1) Integration of weak-quality urban investment platforms. Focus on investment opportunities arising from effective control of financing costs after top-down integration and optimization of asset quality. (2) National-level park urban investment bonds. High-tech zones can enjoy national policy support and are important growth poles in their regions. Attention can be paid to short-duration medium-quality urban investment bonds to avoid tail risks.

2.2 Real Estate Bonds: Industry Cleanup, Survivors Thrive, Weak-Quality State-Owned Enterprise Real Estate Bonds Show Value Under Policy Support

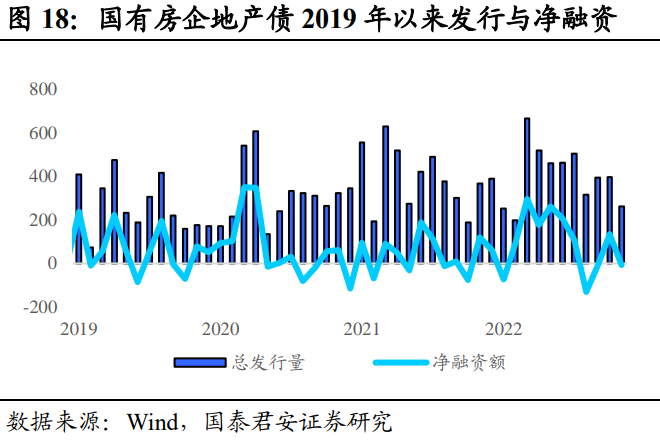

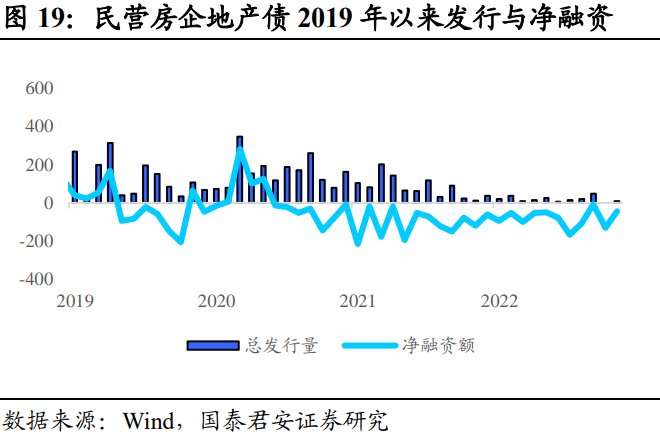

The investment logic for real estate bonds: survivors thrive. The relaxation of refinancing for real estate companies is a round of supply-side cleanup. State-owned enterprises with low net assets will benefit from this relaxation of refinancing, rapidly expanding their net assets and bringing mid-term growth, while other state-owned enterprises will see significant valuation recovery.

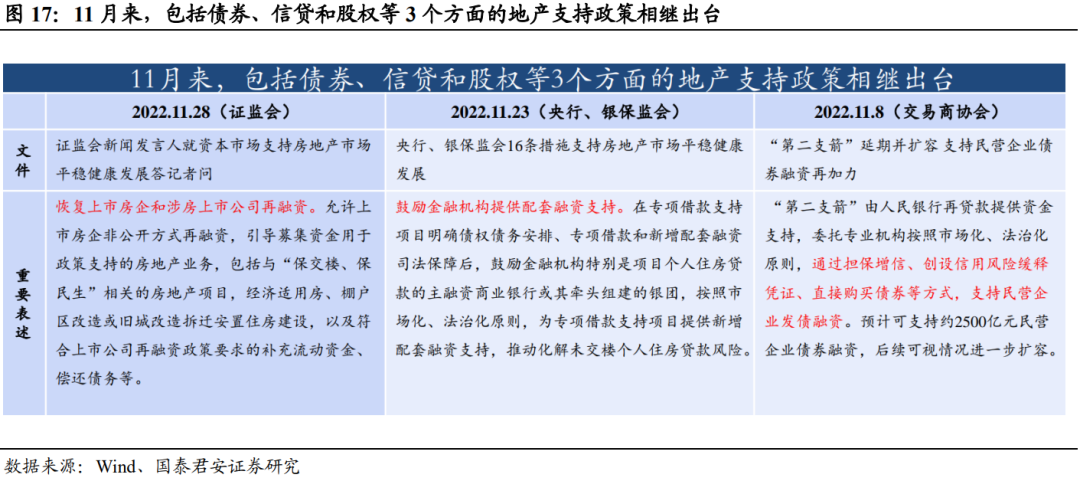

Since November, a series of real estate policies have been introduced. The core logic driving the market is not the effect of any single policy, but rather the significant changes in the underlying assumptions of the stock and bond research framework following the introduction of a series of policies.The essence of real estate is the credit cycle. Before housing prices return to a price that reflects their true commodity nature, more attention should be paid to the expansion and contraction of the credit cycle..

Real estate bond outlook one: Under the collateral guarantee model, benefits accrue to real estate companies with quality remaining assets. Recently, some real estate companies have obtained bank credit and bond issuance quotas. We believe that the future of the real estate industry will primarily follow the asset guarantee route, and companies unable to provide new asset guarantees will face significant pressure. Support for distressed real estate companies will still focus on “ensuring delivery of buildings,” as most projects of distressed companies have already been mortgaged, limiting their ability to provide asset guarantees, making significant liquidity improvements difficult in the short term. The policy tone remains focused on “ensuring delivery of buildings” to minimize the negative externalities of distressed companies.

Real estate bond outlook two: Expectations for supportive policies on the demand side after the 2023 Two Sessions. The supply-side cleanup will further elevate industry concentration. In the future, the main players in the real estate industry will consist of state-owned enterprises, local state-owned enterprises, construction companies, urban investment transformation enterprises, and quality private enterprises coexisting. Expectations for supportive policies on the demand side after the 2023 Two Sessions remain. Under the current background of mortgage rates linked to the LPR, the limited benefits of a slight reduction in the LPR on the demand side are expected. After the 2023 Two Sessions, expectations for subsequent supportive policies on the demand side remain.

The turning point of real estate policies does not completely correspond with the turning point of real estate bonds. The reason is that the repayment order of bonds is behind all stakeholders in real estate, only ahead of equity. The series of real estate policies introduced in November provided some support from the financing side, but the structural characteristics of this round of policies are relatively strong. Whether it is the 16 measures or the “third arrow,” the beneficiaries are companies with quality remaining assets. Real estate companies and urban investment companies both face the issue of short-term financing for long-term investments, making it difficult for the short-duration liabilities of real estate companies to support long-duration assets. Therefore, it is essential to manage expectations in the credit market. Since the second half of 2022, although real estate policies have been introduced intensively, they still rely more on external credit enhancement and counter-guarantee measures, making pure credit financing difficult to recover in the short term. The collateral guarantee model is likely to impact the credit distribution of real estate companies, which still face pressure to shrink their balance sheets.

From an investment strategy perspective, we are optimistic about investment opportunities in weak-quality state-owned enterprise real estate bonds, while remaining cautious about private and mixed-ownership real estate bonds. The reason is that under the collateral guarantee model, most real estate companies have relatively limited quality assets that are not pledged, while state-owned enterprises are more likely to receive external credit support from controlling shareholders. Additionally, small-cap state-owned enterprises may benefit from this round of refinancing relaxation, further expanding their net assets and enhancing their safety margins. Therefore, weak-quality state-owned enterprises exhibit strong resilience and some yield space, making them suitable for investment.

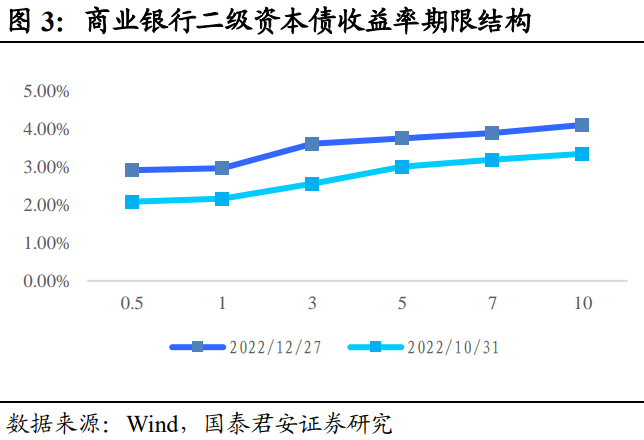

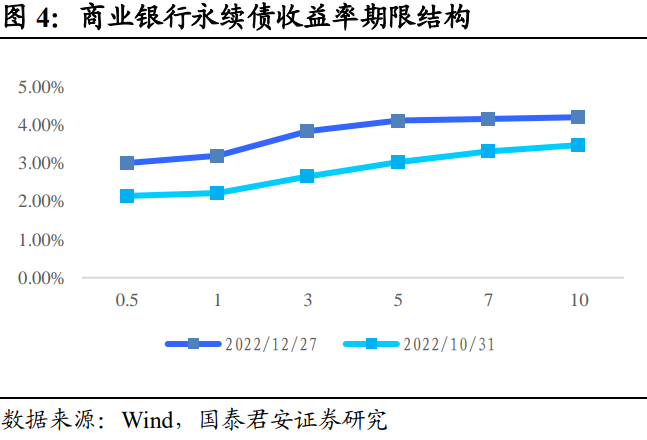

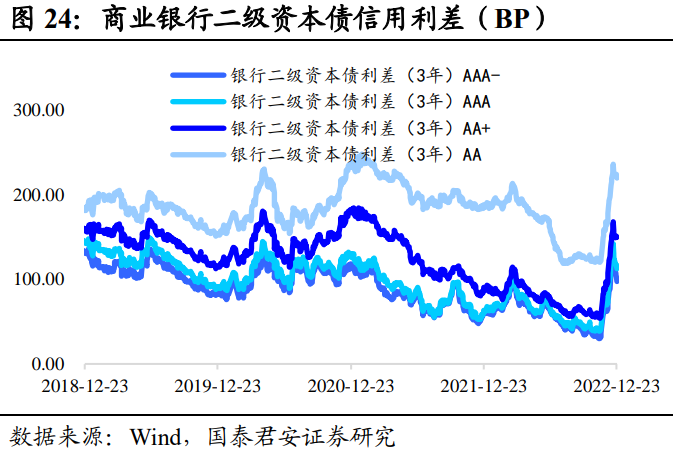

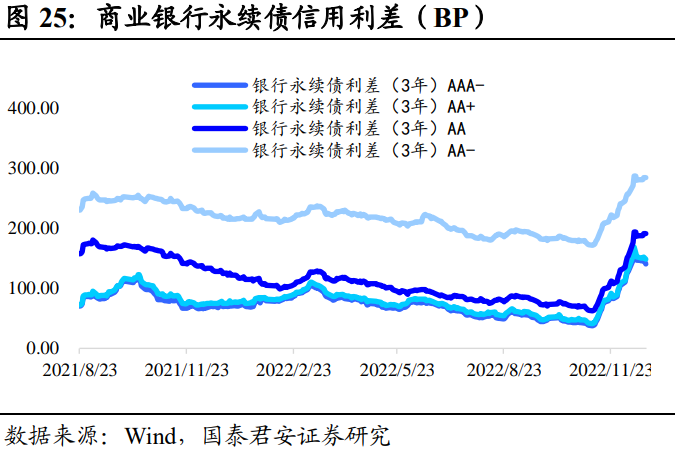

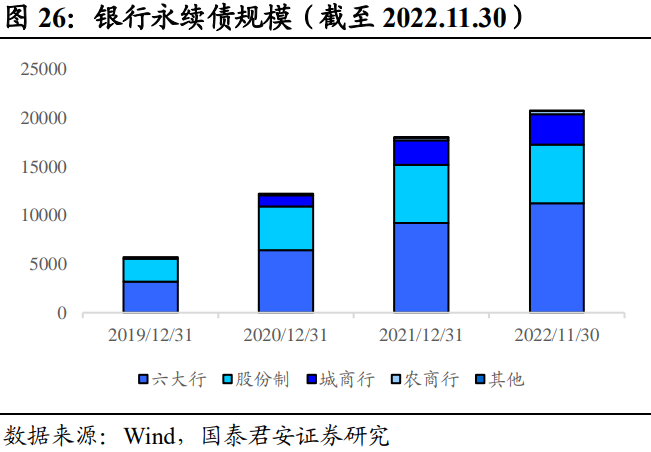

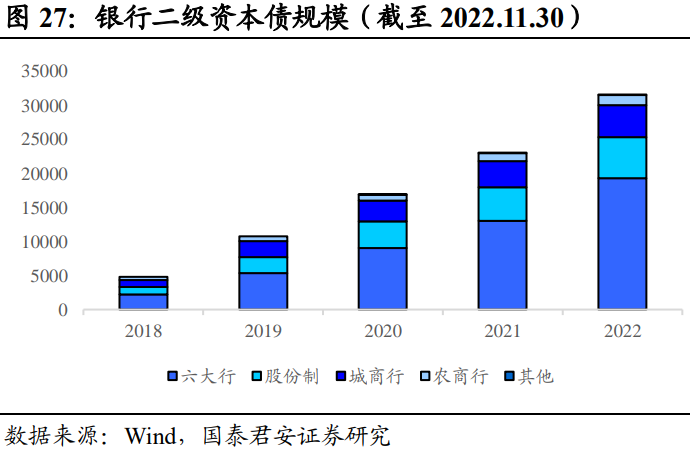

2.3 Financial Bonds: Under New Regulatory Rules, Subordinated Debt Holding Structure Faces Adjustment, Primarily Passive Allocation

For liquid financial bonds, on one hand, improved liquidity has increased the demand for subordinated debt allocation from non-bank institutions. The liquidity of commercial banks’ subordinated capital bonds and perpetual bonds has improved, coupled with the “quasi-interest rate bond” attributes of leading issuers, leading to a clear trend of institutional “collective allocation.” On the other hand, when the bond market adjusts, coupled with redemptions from financial products and bond funds, the adjustment amplitude of liquid bond assets may be larger.

Financial bond outlook one: Under new regulatory rules, the structure of subordinated debt holdings faces adjustments. The “Basel III” agreement may affect the demand for subordinated debt allocation. The “Basel III” agreement will officially take effect on January 1, 2023, adjusting the risk weights of commercial banks’ subordinated capital bonds from the current 100% to 150%; for commercial banks’ perpetual bonds, if counted as debt, the risk weight will be adjusted from 100% to 150%, and if counted as equity, the risk weight will be adjusted from 250% to 400% (for speculative non-listed equity) or 250% (for other equity). As domestic banks adjust their self-operated allocation of subordinated capital bonds and perpetual bonds, the short-term holding structure will face adjustments, and attention should be paid to the implementation progress of “Basel III” in China.

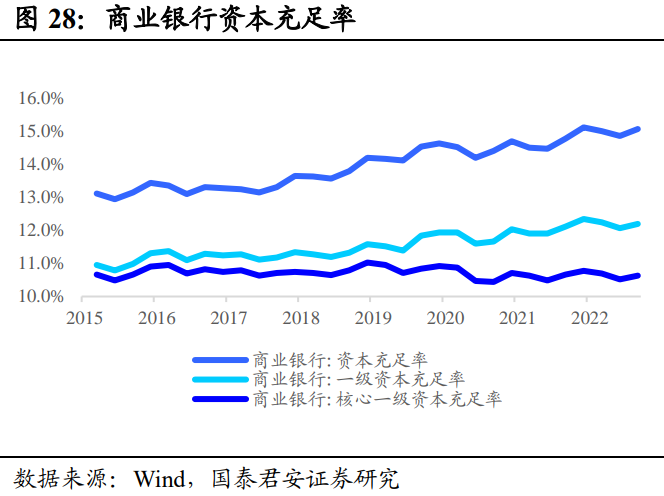

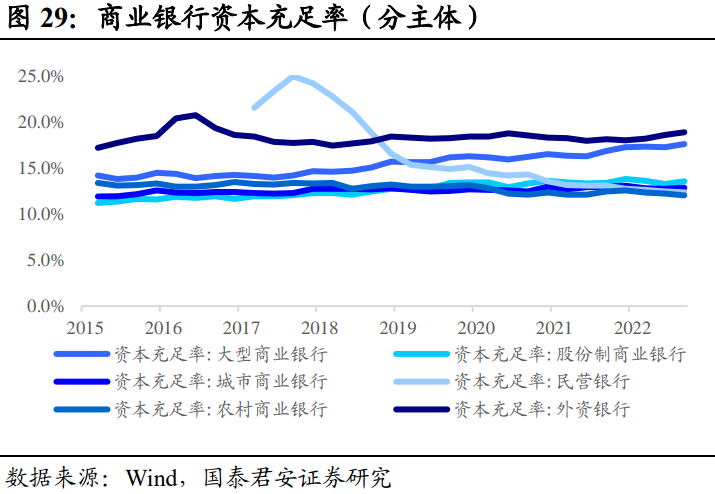

Financial bond outlook two: Focus on banks’ asset quality and capital adequacy levels. The level of capital adequacy is a key factor determining the quality of banks’ subordinated debt. When selecting bonds, attention should be paid to the safety margin of the issuer’s capital adequacy ratio. On one hand, banks with low tier one capital adequacy ratios may face certain operational risks, and their profitability may also be relatively weak; on the other hand, if issuers need to maintain their core tier one capital strength through maturity rollovers, it may lead to passive extensions of bond investment durations and increased valuation risks.

Overall, financial bonds are primarily passively allocated: Under the new regulatory rules, the structure of subordinated debt holdings faces adjustments, and coupled with the increased risk of a bond market correction in 2023, banks’ subordinated capital bonds and perpetual bonds will primarily be passively allocated to avoid tail risks.

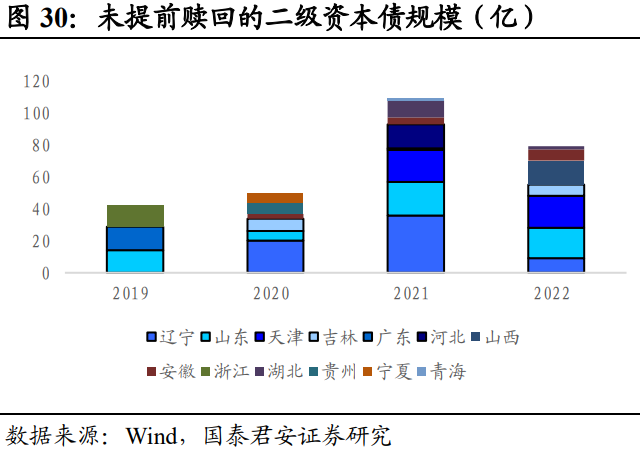

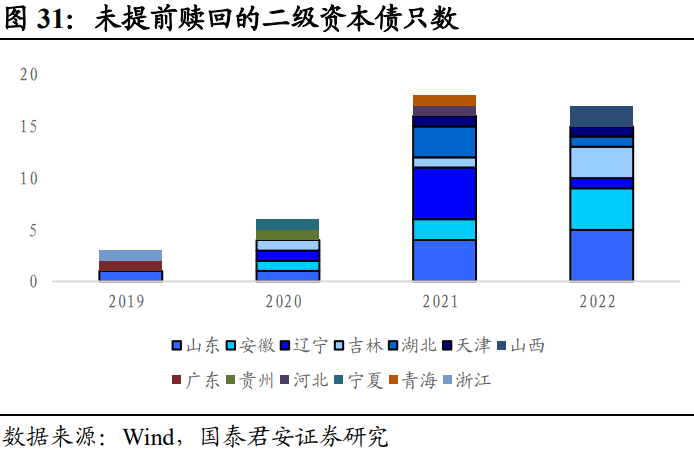

Be cautious with subordinated capital bonds that have not been redeemed early: The scale of subordinated capital bonds that have not been redeemed early has significantly increased in the past two years, mainly dominated by rural commercial banks. The main reason for not redeeming is the weak quality of the issuer, making it difficult to issue new bonds.

3. Risk Warning

Unexpected tightening of monetary policy, economic recovery exceeding expectations.

(End)