Practical Guide to VAT Refunds for Embedded Software: How to Benefit from Policy Incentives?

The VAT refund policy for embedded software is an important tax incentive that encourages the development of the software industry. Eligible enterprises can enjoy a refund of the portion of the actual tax burden that exceeds 3%. This article provides a step-by-step analysis of the calculation logic and declaration process.

1. Policy Basis and Applicable Conditions

1. Policy Document: “Notice on VAT Policy for Software Products” (Cai Shui [2011] No. 100) issued by the Ministry of Finance and the State Administration of Taxation.

2. Scope of Application:

Embedded software must be sold bundled with hardware and be able to account for software sales separately;

Obtain testing certification materials issued by a testing institution recognized by the provincial software industry authority;

Obtain the “Software Product Registration Certificate” issued by the software industry authority or the “Computer Software Copyright Registration Certificate” issued by the copyright administration department.

2. Steps for Calculating the Refund Amount

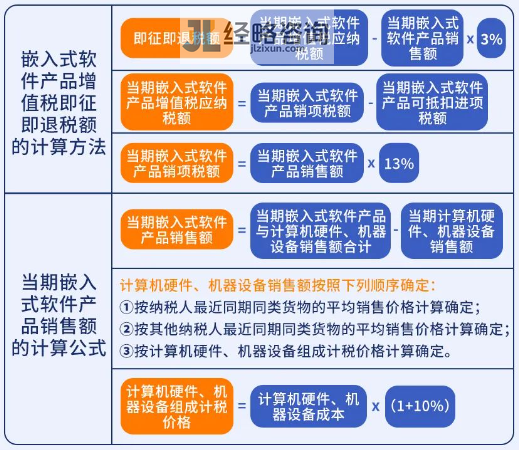

Formula:

Refund Amount = Embedded Software Sales × Applicable Tax Rate – Actual Tax Burden Rate × Sales × (Applicable Tax Rate – 3%)

Key Steps:

1.Separate Hardware and Software Sales:

Hardware sales are determined based on the cost profit margin (default 10%), formula:

Hardware Sales = Hardware Cost × (1 + 10%)

Software Sales = Total Sales – Hardware Sales.

2.Calculate the Taxable Amount:

The software portion is calculated at a 13% tax rate for output tax;

The hardware portion is taxed at the applicable tax rate (usually 13%).

3.Determine the Refund Amount:

Actual Tax Burden Rate = Tax Payable / Total Sales;

If the actual tax burden > 3%, the difference can be refunded.

Example:

A company sells embedded devices with total sales of 1 million yuan and hardware costs of 600,000 yuan, then:

Hardware Sales = 60 × (1 + 10%) = 660,000 yuan;

Software Sales = 1,000,000 – 660,000 = 340,000 yuan;

Software Output Tax = 340,000 × 13% = 44,200 yuan;

If the actual tax payable is 50,000 yuan, then the refund amount = (50,000 – 1,000,000 × 3%) × (13% – 3%) = 20,000 yuan.

3. How to Operate the Tax Refund Declaration? (Key Process)

1.Declare Taxes on Time:

During the specified VAT declaration period (usually from the 1st to the 15th of the following month), complete the normal declaration for general VAT taxpayers through the electronic tax bureau and pay the tax in full (including the portion payable for embedded software products).

2.Prepare Tax Refund Application Materials:

Fill out the complete “Tax Refund (Offset) Application Form” (template available for download or online filling in the electronic tax bureau).

Testing certification materials for embedded software products issued by a testing institution recognized by the provincial software industry authority (very important!).

A copy of the “Computer Software Copyright Registration Certificate” issued by the copyright administration department.

A copy of the main VAT declaration form and Schedule 1 for the month recording the sales of embedded software products.

Relevant explanations and cost accounting materials (such as BOM, cost allocation calculation table, etc.) documenting the hardware cost composition and sales calculation of embedded software products (for reference).

Other materials required by the tax authority (there may be slight differences in various regions, please consult in advance for confirmation).

3.Submit the application through the electronic tax bureau:

Log in to the electronic tax bureau of the enterprise’s location.

Find the “General Tax Refund (Offset) Management” or similar module.

Select the corresponding item such as “Inventory Reduction and Tax Refund (excluding VAT system reserve tax refund)”.

Fill in the information online as required and upload the prepared electronic application materials (must be clearly scanned).

Carefully verify that the information is correct before submitting.

4.Tax Authority Review:

After receiving the application, the tax authority will review the completeness, compliance, and accuracy of the calculations of the materials.

The review time is usually within 20 working days (the specific time limit may vary slightly depending on the region and workload).

During this period, the enterprise may be asked to provide additional explanations or materials.

5.Refund Payment:

After approval, the tax authority will issue a “Tax Revenue Refund Notice”.

The refund will be paid to the bank account designated by the enterprise.

4. Precautions

1.Accounting Requirements: Software and hardware costs and revenues must be accounted for separately; otherwise, the benefits cannot be enjoyed;

2.Declaration Deadline: Applications must be submitted within the declaration period of the tax payable;

3.Policy Validity: The policy is valid for a long time, but attention should be paid to differences in local implementation.

The embedded software tax refund policy can effectively reduce the tax burden on enterprises, but strict compliance with conditions and standardized accounting is required. It is recommended that enterprises communicate with the tax authority in advance to ensure that materials are complete and compliant, avoiding tax refund risks.