First, let’s look at an article to enhance our understanding (partially):

The benefit ranking of the Google Gemini 3 + TPU full-stack upgrade supply chain is as follows: [TPU/OCS core hardware supply chain → Core components such as HBM → Upstream materials and equipment → Downstream AI applications and Google ecosystem → Industry ecology and indirect benefits]. The core logic is “direct matching demand first, core components driven by essential needs, and demand transmitted step by step along the supply chain.”

1. First beneficiary tier: TPU and OCS core hardware supply chain (most direct benefits, largest increment)

Core logic: The core carrier of Google’s “training – inference” computing architecture is directly responsible for large, certain orders for TPU mass production and OCS networking, with a large single cluster scale (Ironwood single cluster has 9216 chips), and high technical barriers, resulting in the highest degree of benefit.

TPU chip manufacturing and packaging: TSMC is the exclusive wafer foundry for Google’s TPU (v6e/Ironwood), monopolizing supply based on advanced N5/N3 processes and CoWoS packaging technology, with mass production of TPU driving the utilization rate of its advanced process capacity. Changdian Technology and Tongfu Microelectronics have entered the supply chain through CoWoS packaging technology, with the value of single-chip packaging being five times that of traditional packaging.

OCS optical circuit switching equipment and core components: Optical Library Technology is the exclusive foundry for Google’s OCS switches, with a single unit valued at $30,000, and a foundry share exceeding 70%, directly benefiting from the large-scale deployment of OCS networking; Tengjing Technology supplies core optical components (ring resonators/prisms), and Silicon Microelectronics provides MEMS mirrors, all of which are indispensable key components for OCS, with the value of single devices ranging from hundreds to thousands of dollars.

High-speed optical modules: Inspur is the exclusive supplier of Google’s 1.6T optical modules, with Ironwood single cluster demand exceeding 100,000 units, and related order amounts exceeding 5 billion yuan by 2025; New Yisheng and Changxin Bochuang’s 800G optical modules/active optical cables adapt to edge nodes, benefiting from TPU cluster expansion.

2. Second beneficiary tier: Core components such as HBM (driven by essential needs, with both volume and price rising)

Core logic: Gemini 3’s long context and high computing density impose rigid requirements on memory bandwidth/capacity, and the TPU architecture upgrade directly stimulates explosive demand for components such as HBM, with industry supply and demand tension enhancing bargaining power.

High Bandwidth Memory (HBM): SK Hynix and Samsung are the core suppliers of HBM for Ironwood TPU, which is equipped with 192GB HBM, a six-fold increase compared to v6e, with HBM4 prices rising over 50% compared to previous generations, and orders from leading suppliers booked until 2027. Taiji Industrial and Changdian Technology benefit indirectly by providing HBM packaging testing services to SK Hynix.

Regarding the impact on semiconductor storage, it is worth mentioning that the advancement of Google Gemini 3 and the widespread application of TPU will exacerbate the current and future memory shortage situation. The core reason behind this is that the explosive growth of AI computing power is reshaping the supply-demand structure of the entire storage chip market. Based on various information, this memory shortage is not a short-term phenomenon. Major storage chip manufacturers, such as Samsung and SK Hynix, have reportedly booked all HBM production capacity for 2026. Additionally, as it takes several years for new wafer fabs to release capacity, the industry generally expects this shortage to last at least until 2026, possibly extending to 2027. The following table can quickly illustrate how AI expansion triggers a “battle” across different memory types.

High-end PCB: Shenzhen South Circuit is the exclusive supplier of Ironwood TPU 44-layer high-end PCBs, while Shenghong Technology and Dongshan Precision have been evaluated by Google. The stable operation of TPU chips relies on the signal transmission capability of high-end PCBs, with the value of a single PCB significantly higher than that of consumer-grade products.

3. Third beneficiary tier: Upstream materials and equipment (demand transmission, barrier support)

Core logic: The mass production demand for core hardware and components transmits upstream, with materials and equipment manufacturers enjoying certain growth based on technical barriers, benefiting from the long-term upgrade trend in the industry.

Semi-conductor materials: Yake Technology’s HBM precursor materials and Xingfu Electronics’ electronic-grade phosphoric acid directly support HBM manufacturing and TPU wafer production; the demand for electronic-grade silicon micropowder, epoxy molding compounds for packaging, and other materials grows in sync with TPU/OCS capacity expansion.

Semi-conductor equipment: Zhongwei’s etching equipment is used for TPU chip manufacturing, and Jingce Electronics’ HBM testing equipment supports SK Hynix’s capacity expansion, with equipment demand directly linked to the mass production rhythm of core hardware, providing strong order visibility.

Thermal management and power management: Invec’s liquid cooling solutions adapt to Ironwood’s 30W/cm² high power density, while Magmita’s efficient power modules achieve a conversion efficiency of 96%, both entering Google’s data center supply chain, maintaining a gross margin above 40%.

4. Fourth beneficiary tier: Downstream AI applications and Google ecosystem (capability empowerment, scene implementation)

Core logic: Gemini 3’s agent and multimodal capabilities lower the development threshold for complex AI applications, allowing enterprises deeply integrated with the Google ecosystem to directly reuse technological advantages, achieving dual growth in product efficiency and user volume.

Google ecosystem application vendors: Wondershare Technology deeply integrates Gemini capabilities, improving product efficiency by 70%, selected for the keynote speech at the Google Developer Conference, and will benefit from the global promotion of Gemini 3.

AI computing power demand side: AI startups like Anthropic have already reserved 1 million Ironwood TPUs for running the Claude model, and the technological breakthroughs of Gemini 3 will drive more enterprises to procure TPU computing power, indirectly stimulating upstream hardware demand.

Vertical industry applications: Industries such as intelligent driving, medical imaging, and enterprise services can upgrade products using Gemini 3’s multimodal reasoning and complex task execution capabilities, promoting an increase in industry AI penetration rates.

5. Fifth beneficiary tier: Industry ecology and indirect benefits (trend-driven, relatively weak elasticity)

Core logic: Google’s full-stack upgrade reshapes the competitive landscape of the AI industry, indirectly driving related technology routes to follow or ecological collaboration, but the benefits lack direct order support, with relatively weak elasticity.

Other AI chip manufacturers: Domestic AI chip companies like Cambricon have had their technologies cited in Google’s TPU papers, and Google’s “dedicated chip + scale cluster” path will promote industry attention to TPU-like chips, indirectly benefiting technology followers.

Advertising and marketing industry: Advertising agents like the Provincial Advertising Group can leverage Gemini-enabled precise delivery and efficient creative tools to enhance service capabilities, benefiting from the AI-driven transformation of the marketing industry.

Chip IP and design services: Companies like Chipone’s processor IP can adapt to AI chip design needs, benefiting from the global AI chip design boom, but with low relevance to Google’s direct supply chain.

In summary, the updates of Google Gemini 3 and TPU v6e demonstrate a clear trend in AI computing power development: expanding model scale, increasing inference demand, and multimodal integration. This trend is reshaping the investment focus of computing power infrastructure.

From the perspective of the supply chain impact, optical modules and optical chips are the most certain beneficiaries, as the expansion of TPU clusters and the increase in interconnect bandwidth directly drive demand. PCB/carrier boards and HBM storage also significantly benefit from the increased complexity of TPU chips and the increase in memory capacity. Liquid cooling technology is gradually becoming a standard in high-end data centers due to the increase in computing power density.

For investors, understanding the key to this technological transformation is recognizing that AI competition has shifted from a simple model race to a full-stack integration of chips, models, and applications. In this context, companies that can provide high-value-added technology in key areas of computing power infrastructure will gain sustained growth momentum in the AI computing arms race.

At this point, can we also understand why Buffett was able to make a significant purchase of Google at a high point? Is it because he saw Google’s “chip-model-application” full-stack advantage? With users, ecosystems, models, chips, data centers, and applications, this integrated software and hardware may allow Google to surpass Nvidia and become the world’s most valuable company in the future, which is not impossible.

From the above, we can see the investment targets needed in general cases, but further sorting requires looking at market feedback:

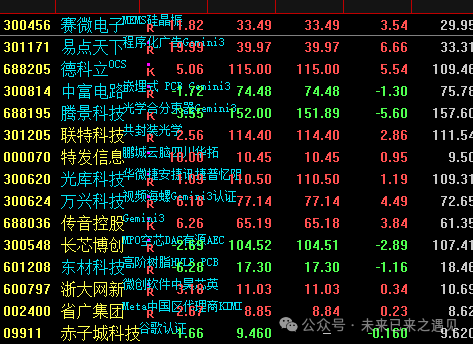

In actual speculation, the average three-day increase ranking of the Google chain is as follows:

AI application direction (overlaying Alibaba) average three-day increase ranking is as follows:

From this, we see that AI applications are ahead of the Google chain, as the AI application news catalyzed a day or two earlier than Google, and the subsequent second tier has not yet started speculation (for example, as a supplementary rise, while the first tier has just begun). Additionally, the author of the above article is merely a personal opinion and may have omissions.

I saw in a certain public account that among the Google chain, OCS has the largest increment, so I specifically inquired which listed company has the largest increment in OCS (Optical Circuit Switching), and Doubao answered:The company with the largest increment and known as the “pioneer of the Google chain” is Dekoli (688205). Google OCS has chosen the MEMS mirror array-dominated optical circuit switching technology route, and besides Dekoli, Optical Library Technology, Silicon Microelectronics, and other listed companies also significantly benefit, with specific information as follows:

1. Technology route: Google’s OCS adopts the MEMS mirror array technology route for optical circuit switching (OCS). This route can achieve direct optical path switching, reducing latency by 90% compared to traditional electrical switching, and can also reduce the overall power consumption of the data center network by about 40%, adapting to the high bandwidth and low latency requirements of TPU clusters. Moreover, the first generation of OCS can match the upgrade of the third generation of electrical switches, reducing iteration costs, perfectly fitting Google’s deployment needs for tens of thousands of TPU clusters.

2. Core beneficiary listed companies

Dekoli (688205): As the core foundry for Google’s OCS optical switches, it aims to occupy 20%-25% of Google’s OCS supply chain share with its self-developed photonic routing engine controlling latency, expecting related revenue to reach $1.1 billion by 2026, and has planned domestic and international capacity assurance orders, making it the most representative enterprise in OCS increment, truly deserving the title of “pioneer of the Google chain.”

Optical Library Technology (300620): After acquiring Wuhan Jiefu, it has become the core foundry for Google’s OCS, with a market share of over 40% for its thin-film lithium niobate modulators, and a foundry share exceeding 70% in Google’s OCS supply chain, while also entering the supply chains of overseas giants like Microsoft and Meta.

Silicon Microelectronics (300456): As a core supplier of MEMS solutions, its subsidiary supplies critical mirror array wafers for Google’s OCS, with each OCS containing two MEMS chips supplied by it, with a single chip valued at approximately $3,000. This business has significantly driven the company’s performance growth in the third quarter of 2025.

Inspur (300308): As a global leader in optical modules, it is the exclusive supplier of Google’s TPU cluster 1.6T DR8 optical modules, with related order amounts exceeding 5 billion yuan by 2025, and its products meet the high bandwidth requirements needed for Google’s OCS, benefiting deeply from the incremental optical modules supporting OCS.

This is evidently different from what was seen earlier, and the following is copied from another source:

Optical Library Technology: The Wuhan Jiefu factory acquired in June 2025 is the past exclusive foundry for Google’s OCS switch scheme.

In the past two years, Optical Library Technology has frequently made acquisitions to strengthen its main business development. Last January, Optical Library Technology acquired 52% of Bai’an Industrial for 156 million yuan, with a premium rate as high as 1192.56%; in June of this year, Optical Library Technology announced the acquisition of 100% of Wuhan Jiefu, which is now included in the consolidated financial statements.

Optical Library Technology plans to purchase 99.97% of the shares of Anjie Xun held by six transaction counterparties. It is said that one of the six transaction counterparties, Sha Shuli, withdrew from this transaction for personal reasons, thus adjusting the transaction target assets to 99.97% of Anjie Xun’s shares.

Dekoli: The order for 10 OCS prototypes from Google is expected to be delivered by the end of 2025, with a unit price of $250,000.

Tengjing Technology: The core optical component supplier for Google’s OCS switches, with business revenue accounting for 28%.

Initially, I saw that the biggest beneficiary should be Tengjing Technology (I forgot to record it), which highlights the importance of information sources. For us outsiders, distinguishing between the best and true leaders when the market just begins is quite challenging! (This further illustrates the importance of tracking an industry.)

In addition to identifying the sectors, individual stocks also need to be determined based on technical aspects (in the absence of further information sources).

At this point, the most important part of the Google chain has roughly selected stocks. If you choose long-term targets, more information is needed to understand. Friends, if you see this, how would you choose?

Of course, the Google chain has many other important related targets besides OCS, such as Invec for liquid cooling, Zhongfu Circuit for PCB, and the related stocks mentioned above.

Then, let’s review the AI application direction, where Kunlun Wanwei, Yidian Tianxia, Keda Xunfei, and Wondershare Technology were tracked before speculation began. This week, they rose first with the Alibaba concept, with AI marketing video ads being the core. The main ones include BlueFocus, Yidian Tianxia, Vision China, Wondershare Technology, Rongji Software, Fushi Holdings, Shida Group, and Huanrui Century, among which the front row includes Rongji Software, Yidian Tianxia, Shida Group, and the middle army BlueFocus, etc. The main focus for continued speculation will be on these few, and the specific choices are quite complex, so I won’t elaborate on them! (Real-time operations also need to observe collective bidding.)

Summary: The Google chain can be focused on (currently the strongest narrative), although the market has plummeted, speculation is eternal. Dreams are always worth having; what if it succeeds?

That’s all for today!

The above is a personal opinion and does not constitute guidance for others’ operations. Please think independently and do not imitate casually!