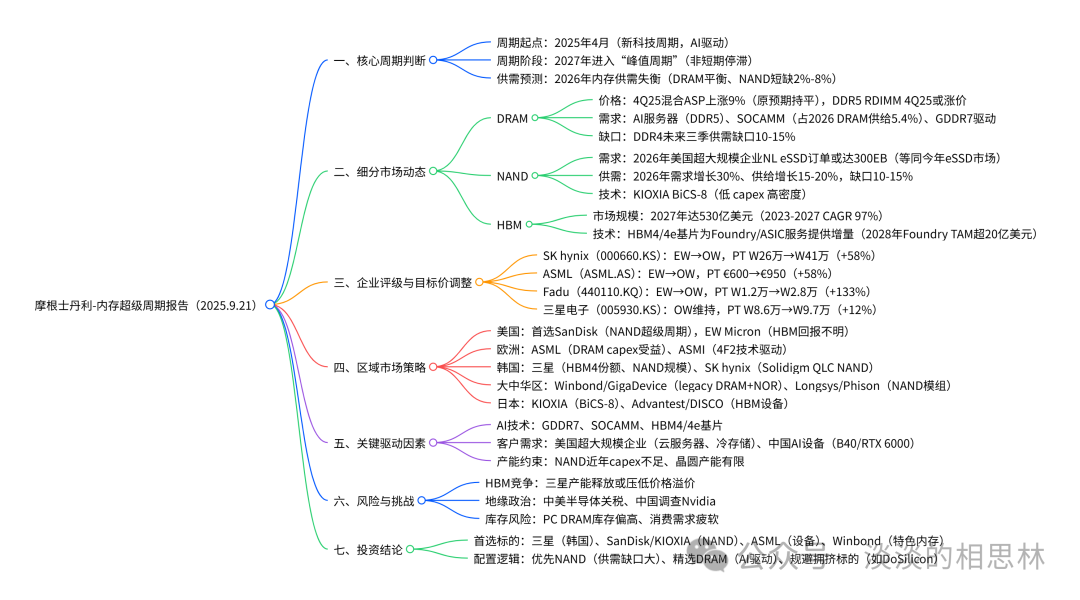

We have compiled the storage supercycle report released by Morgan Stanley on Sunday, starting with a mind map, followed by a translation of the overall industry outlook, and concluding with an analysis of companies favored in different markets. Overall Trends in the Storage Market: The dynamics of the storage industry are changing, with supply shortages emerging in various regions. Recently, we have seen a surge in orders for high-density NAND from U.S. hyperscale companies for 2026. The scale of these orders alone could exceed the entire eSSD market size for this year, and given the underinvestment in recent years and limited wafer capacity, its impact may extend to other areas of the NAND market. We believe that after years of production cuts, the current capital allocation for NAND indicates that the return on investment will significantly improve throughout the cycle (see “NAND – The Era of AI Finally Arrives for NAND”). We do not expect DRAM prices to adjust downward before the end of the year; instead, driven by a surge in cloud server orders, the average selling price in Q4 2025 is expected to rise by 9% (previously expected to remain flat). We note that there are several new drivers for the storage market’s strength led by artificial intelligence, including SOCAMM, GDDR7, and HBM logic base chips.

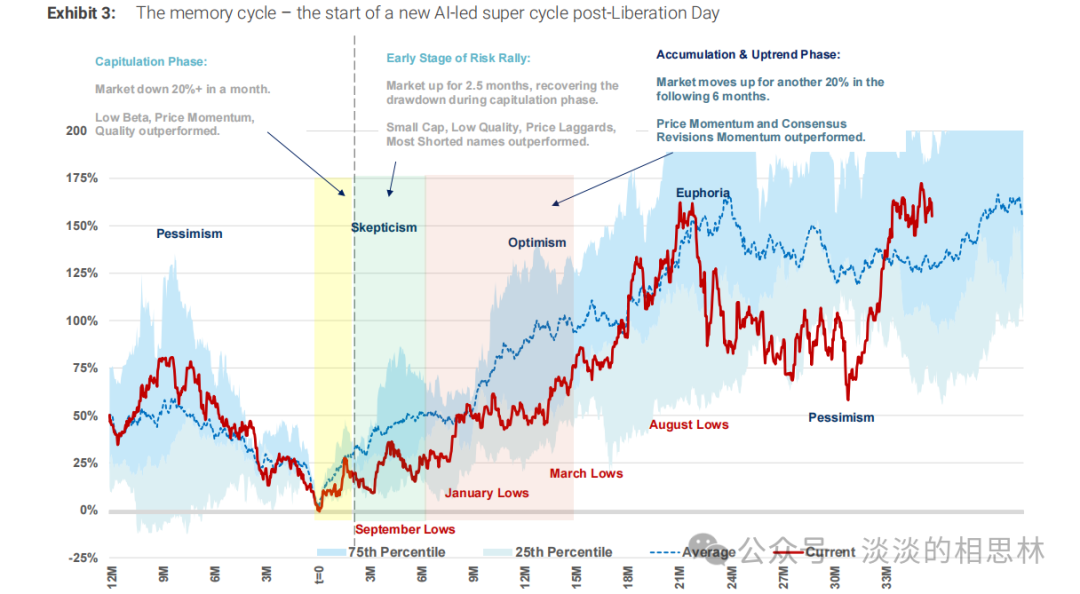

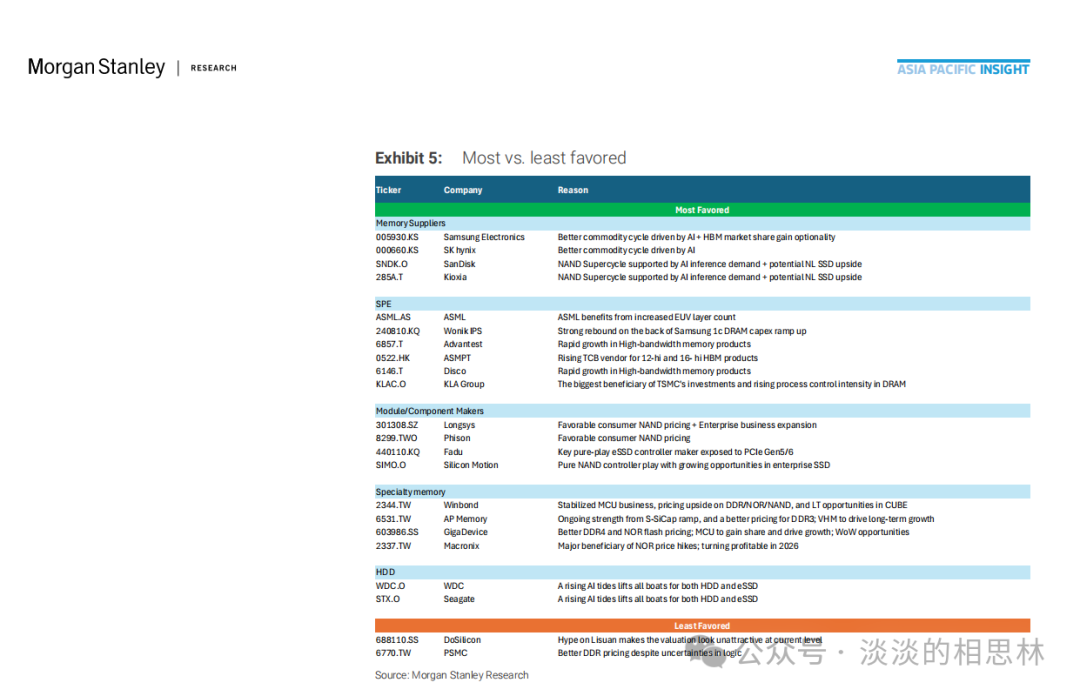

Overall Trends in the Storage Market: The dynamics of the storage industry are changing, with supply shortages emerging in various regions. Recently, we have seen a surge in orders for high-density NAND from U.S. hyperscale companies for 2026. The scale of these orders alone could exceed the entire eSSD market size for this year, and given the underinvestment in recent years and limited wafer capacity, its impact may extend to other areas of the NAND market. We believe that after years of production cuts, the current capital allocation for NAND indicates that the return on investment will significantly improve throughout the cycle (see “NAND – The Era of AI Finally Arrives for NAND”). We do not expect DRAM prices to adjust downward before the end of the year; instead, driven by a surge in cloud server orders, the average selling price in Q4 2025 is expected to rise by 9% (previously expected to remain flat). We note that there are several new drivers for the storage market’s strength led by artificial intelligence, including SOCAMM, GDDR7, and HBM logic base chips. Changes – Five Surprises: 1) The demand for high-density QLC enterprise solid-state drives (eSSD) is prominent, with new orders for 2026 potentially equating to this year’s entire enterprise solid-state drive demand. 2) Several emerging terminal markets led by artificial intelligence are experiencing turning points in demand, particularly B40 (or RTX 6000), with approximately 2 million GDDR7 expected to be sold to China in the second half of 2025, and potentially more in 2026; additionally, the demand for SOCAMM is driven by the launch of the Rubin GPU, which has boosted the demand for LPDDR5x. 3) Since the beginning of this quarter, the demand for DDR5 RDIMM servers has significantly increased, which may drive prices up in Q4 2025. 4) Due to supply allocation and inventory levels being below normal, this may affect customer behavior in other areas of the DRAM market. 5) Driven by HBM4 and tighter supply conditions, capital expenditure for DRAM may significantly increase in 2026.Turning Point Signals – Buy Signals Persist: Ultimately, we are focused on the turning points throughout the cycle and the direction of profit expectations. We now find that the cyclical recovery of the former is continuing, rather than a second bottom, while the risks associated with the latter (high bandwidth memory, HBM) are decreasing. We now believe: 1) The current tariff-driven cyclical recovery will continue to accelerate in 2026, with stocks typically reflecting this expectation 1-2 quarters before year-on-year price improvements; 2) Driven by inventory depletion, the oversupply of dynamic random-access memory (DRAM) will become more balanced in 2026, while flash memory (NAND) will face shortages as demand for AI embedded solid-state drives (eSSD) doubles next year; 3) Despite the demand for consumer technology products being suppressed, growth indicators are better than expected;From a Relative Pricing Perspective: We are more optimistic about NAND and have upgraded several ratings. We have upgraded ASML’s rating (see link below) as it is the main beneficiary of the upward risk in DRAM capital expenditure; at the same time, we have upgraded SK Hynix’s rating from hold to buy, as investors have fully understood the downside risks of HBM, and the market narrative has begun to shift towards the commodity upcycle in 2026. We have upgraded the rating of the South Korean technology sector from in line with the market to attractive, with Samsung, SanDisk, Kioxia, and SK Hynix being our preferred targets that we believe will benefit from the NAND and commodity DRAM cycles. Our other buy targets include NAND module manufacturers Phison Electronics and JMicron Technology.In the Consumer Electronics Semiconductor Field: We believe Winbond Electronics (buy) and GigaDevice (buy) will benefit from both traditional DRAM and NOR flash; other beneficiaries of traditional DRAM include Nanya Technology (buy), Macronix (buy), and Powerchip (hold), while another beneficiary of NOR flash is Macronix (buy). We maintain a hold rating on Micron Technology and a reduce rating on Tongfu Microelectronics. Among the targets we cover, our current expectations for 2026 earnings per share are on average 19% higher than market consensus, and we believe stocks will return to peak multiples, which forms the basis of our target price.The Situation in the Storage Market is Changing: The current risk-reward ratio is improving. In the storage sector, we are more optimistic about NAND, as our channel surveys indicate that by 2026, NAND will face significant capacity constraints. This is driven by a surge in demand from hyperscale companies for cold storage replenishment, which has become tighter due to insufficient hard disk drive (HDD) capacity. Due to the similarity of end markets and overlapping customer bases, the cyclicality of NAND and DRAM tends to be somewhat synchronized, which makes us more optimistic about price trends in 2026. All non-AI server customers are in good inventory consumption status, and although demand has exceeded supply (partly due to tariffs), we believe the recent surge in demand from U.S. hyperscale companies was unexpected.

Changes – Five Surprises: 1) The demand for high-density QLC enterprise solid-state drives (eSSD) is prominent, with new orders for 2026 potentially equating to this year’s entire enterprise solid-state drive demand. 2) Several emerging terminal markets led by artificial intelligence are experiencing turning points in demand, particularly B40 (or RTX 6000), with approximately 2 million GDDR7 expected to be sold to China in the second half of 2025, and potentially more in 2026; additionally, the demand for SOCAMM is driven by the launch of the Rubin GPU, which has boosted the demand for LPDDR5x. 3) Since the beginning of this quarter, the demand for DDR5 RDIMM servers has significantly increased, which may drive prices up in Q4 2025. 4) Due to supply allocation and inventory levels being below normal, this may affect customer behavior in other areas of the DRAM market. 5) Driven by HBM4 and tighter supply conditions, capital expenditure for DRAM may significantly increase in 2026.Turning Point Signals – Buy Signals Persist: Ultimately, we are focused on the turning points throughout the cycle and the direction of profit expectations. We now find that the cyclical recovery of the former is continuing, rather than a second bottom, while the risks associated with the latter (high bandwidth memory, HBM) are decreasing. We now believe: 1) The current tariff-driven cyclical recovery will continue to accelerate in 2026, with stocks typically reflecting this expectation 1-2 quarters before year-on-year price improvements; 2) Driven by inventory depletion, the oversupply of dynamic random-access memory (DRAM) will become more balanced in 2026, while flash memory (NAND) will face shortages as demand for AI embedded solid-state drives (eSSD) doubles next year; 3) Despite the demand for consumer technology products being suppressed, growth indicators are better than expected;From a Relative Pricing Perspective: We are more optimistic about NAND and have upgraded several ratings. We have upgraded ASML’s rating (see link below) as it is the main beneficiary of the upward risk in DRAM capital expenditure; at the same time, we have upgraded SK Hynix’s rating from hold to buy, as investors have fully understood the downside risks of HBM, and the market narrative has begun to shift towards the commodity upcycle in 2026. We have upgraded the rating of the South Korean technology sector from in line with the market to attractive, with Samsung, SanDisk, Kioxia, and SK Hynix being our preferred targets that we believe will benefit from the NAND and commodity DRAM cycles. Our other buy targets include NAND module manufacturers Phison Electronics and JMicron Technology.In the Consumer Electronics Semiconductor Field: We believe Winbond Electronics (buy) and GigaDevice (buy) will benefit from both traditional DRAM and NOR flash; other beneficiaries of traditional DRAM include Nanya Technology (buy), Macronix (buy), and Powerchip (hold), while another beneficiary of NOR flash is Macronix (buy). We maintain a hold rating on Micron Technology and a reduce rating on Tongfu Microelectronics. Among the targets we cover, our current expectations for 2026 earnings per share are on average 19% higher than market consensus, and we believe stocks will return to peak multiples, which forms the basis of our target price.The Situation in the Storage Market is Changing: The current risk-reward ratio is improving. In the storage sector, we are more optimistic about NAND, as our channel surveys indicate that by 2026, NAND will face significant capacity constraints. This is driven by a surge in demand from hyperscale companies for cold storage replenishment, which has become tighter due to insufficient hard disk drive (HDD) capacity. Due to the similarity of end markets and overlapping customer bases, the cyclicality of NAND and DRAM tends to be somewhat synchronized, which makes us more optimistic about price trends in 2026. All non-AI server customers are in good inventory consumption status, and although demand has exceeded supply (partly due to tariffs), we believe the recent surge in demand from U.S. hyperscale companies was unexpected. Market Segmentation:U.S. Stock Market: We prefer NAND over DRAM and have recently listed SanDisk as our top pick. Relative to current valuations, NAND benefits the most from the tailwinds of artificial intelligence, but the tailwinds for DRAM remain strong as well. We expect Micron’s fundamentals to end this year with very strong performance, but due to the unclear returns of high bandwidth memory (HBM) in 2026, we believe its upside will remain limited, as investors have priced the stock based on the “most optimistic” assumptions.Greater China Memory Market: Among semiconductor companies in Greater China, we believe Winbond Electronics (buy) and GigaDevice (buy) will benefit from traditional DRAM and NOR flash; other beneficiaries of traditional DRAM include Nanya Technology (buy), Macronix (buy), and Powerchip (hold), while another beneficiary of NOR flash is Macronix (buy). Given the favorable price cycle of NAND flash and its business expansion, we are optimistic about JMicron Technology and Phison Electronics. We also want to emphasize that the complexity and customization of HBM base chips may become an important growth driver for integrated circuit design service providers and foundries.Kioxia in Japan is another top pick: We believe that the company’s BiCS-8 presents a unique revaluation opportunity, as this technology combines planar shrink, new architecture (CBA), and multi-layer cell technology to achieve higher storage density with a lower capital expenditure burden.

Market Segmentation:U.S. Stock Market: We prefer NAND over DRAM and have recently listed SanDisk as our top pick. Relative to current valuations, NAND benefits the most from the tailwinds of artificial intelligence, but the tailwinds for DRAM remain strong as well. We expect Micron’s fundamentals to end this year with very strong performance, but due to the unclear returns of high bandwidth memory (HBM) in 2026, we believe its upside will remain limited, as investors have priced the stock based on the “most optimistic” assumptions.Greater China Memory Market: Among semiconductor companies in Greater China, we believe Winbond Electronics (buy) and GigaDevice (buy) will benefit from traditional DRAM and NOR flash; other beneficiaries of traditional DRAM include Nanya Technology (buy), Macronix (buy), and Powerchip (hold), while another beneficiary of NOR flash is Macronix (buy). Given the favorable price cycle of NAND flash and its business expansion, we are optimistic about JMicron Technology and Phison Electronics. We also want to emphasize that the complexity and customization of HBM base chips may become an important growth driver for integrated circuit design service providers and foundries.Kioxia in Japan is another top pick: We believe that the company’s BiCS-8 presents a unique revaluation opportunity, as this technology combines planar shrink, new architecture (CBA), and multi-layer cell technology to achieve higher storage density with a lower capital expenditure burden.