Preliminary observations on Nvidia’s Vera Rubini PCB/HDI and CCL upgrades

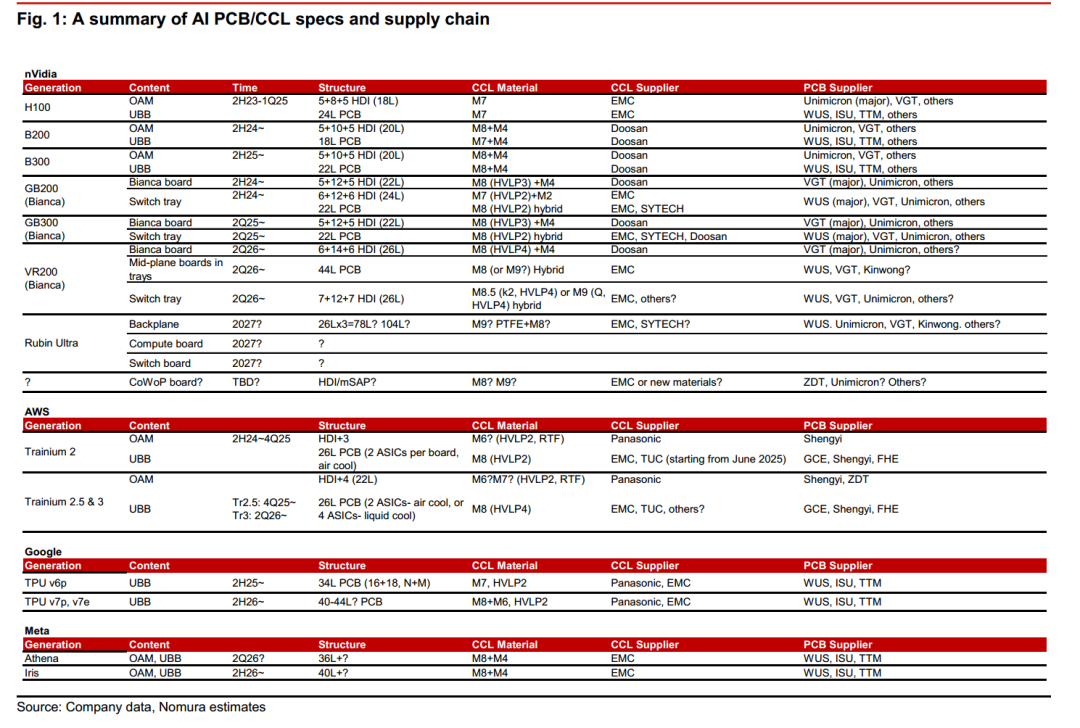

We believe that the design discussions for Nvidia’s Vera Rubini (US version, non-rated) Vera Rubini (VR) system are nearing their final stages. We summarize some observations regarding its PCB and Copper Clad Laminate (CCL) supply chain, as shown in Figure 1.

1. For the compute tray, we believe that VR will continue to use the Bianca architecture, just like the GB200 and GB300, with each compute tray requiring two HDI Bianca modules. We have observed that the Bianca HDI board will upgrade to HDI+6 (from HDI+5 for GB200/300), still using Dooosan’s (000150 KS, non-rated) M8-M4 grade CCL materials, but upgrading the copper foil from HVLP3 to HVLP4.

2. For the NVL exchange tray, we observe that it may upgrade to HDI+7 (from the original HDI+5/+6 or 22L high-layer count [HLC] PCB), using EMC’s (2383 TT, buy) M9 or M8.5 CCL materials.

3. By adopting wireless designs within the compute tray and NVL exchange tray, additional mid-layer PCBs may be required to replace the connection cables within the VR (6 PCIe, MCIO cables, etc.) tray. Due to the thinner and longer mid-layer PCBs (less than 1U height, approximately the width of the tray), they will be vertically placed in the middle of the compute/exchange tray, attempting to connect the Bianca or exchange board on one side of the tray with the peripheral board on the other side. Considering their slim shape, the PCB design may be 44L HLC, using M8 or M9 materials (possibly from EMC).

4. The backend wiring of Rubini Ultra. Although Rubini Ultra is still far from arrival (possibly in 2027), there is still much discussion about its backend PCB supply chain, likely due to the advanced design and material innovations required by the Kyber architecture that need early preparation and validation. Four backend PCBs are needed to connect each computer rack with the switch rack, and the backend PCBs may be 78L or even higher (for example, by compressing three 26L+ PCBs), as shown in Figure 1.

Nvidia’s key PCB/HDI suppliers remain largely unchanged, with some new entrants. As shown in Figures 1 and 2, Nvidia’s key HDI suppliers are VGT (300476 CH, non-rated) and Unimicron (3037 TT, buy), while the main PCB/HLC manufacturers are WUS (002463 CH, buy), VGT, TTM (TTM US, non-rated), and ISU (007660 KS, non-rated). We observe that the key suppliers for the aforementioned VR PCBs/HDIs remain these suppliers.

However, we also observe that Nvidia is urgently seeking OOC PCB/HDI suppliers outside of China/Taiwan. Therefore, supply chain feedback indicates that some new entrants with OOC capacity (e.g., Thailand) may enter Nvidia’s supply chain, such as Dynamic (3715 TT, non-rated) and ZDT (4958 TT, buy). Our supply chain research suggests that some suppliers with solid-state HDI or HLC capabilities may also be evaluated, such as Kiwong (603228 CH; showcased 78L backend PCB at GTC 2025) and Founder (600601 CH, non-rated).

For trials of chip-to-wafer (CoWoP) technology directly on mSAP/HDI PCBs (a potential future technology that can directly bond GPUs on mSAP/HDI PCBs, bypassing traditional FCBGA substrates, see our report), we believe that Unimicron and ZDT are engaged in this project. However, it may take at least 2-3 years to realize, and there is no guarantee it will be completed on time.

AWS Trainium – The origin of the “shortage” factor, but keep an eye on its products

AWS Trainium 2 (Tr2) has been a key growth driver in the AI PCB/CCL industry to date.

Due to its UBB PCB adopting one of the highest specifications in current AI platforms – 26L PCB, using “full” M8 grade CCL (compared to most others using 20-26L, mixed M7/8+M4/6 CCL). Since May, orders for Trainium 2 have increased to downstream components and assemblers, including PCB/CCL, significantly raising sales and earnings expectations for 2025-4Q25F and 2026-2QF, while also raising concerns about shortages of HLC PCBs and high-end materials (CCL, fiberglass cloth).

Recently, the growth of Trainium 2.5 (Tr2.5) starting from 4Q25F has triggered an upgrade of PCB copper foil from HVLP2 to HVLP4. We believe that many next-generation ASICs, GPUs, and switch ICs launched in 2026 will also require upgrades to HVLP4 for motherboard PCBs and switch PCBs to reduce signal loss during AI performance enhancements. The market has begun to worry about potential shortages of high-end copper foil HVLP3/4 during 2026-27F. We will provide more details about high-end copper foil in the upcoming section “Game Changer for Copper Foil in Upcoming CCL Upgrades”.

However, as we emphasized in our mid-August report, we observe that AWS Tr2 orders may peak in 3Q25F and begin to transition in 4Q25F. The transitional Tr2.5 may start production during the 4Q25F-1H26F period, while Trainium 3 (Tr3) may achieve meaningful output by the end of 2026F. The transition period may last 6-8 months (from September to the following April or May). We observe that the monthly operating rate of Tr2.5 (even at peak) will be lower than the peak operating rate of Tr2 in 3Q25F, and we are uncertain how low it will be when the transition begins in 4Q25F.

We believe Tr3 will be the next focus for AWS, and we estimate its lifecycle output may be 1.5-2 times that of Tr2. However, delays in mass production of Tr3 may create potential gaps for its suppliers, including PCB/CCL manufacturers, during the transition period. We have seen several PCB/CCL suppliers downgrade their expectations for AWS sales contributions for August-September and 4Q25F, but most have maintained flat guidance for 4Q25F sales, as they can ship other unfulfilled orders to compensate for AWS’s “slight” decline in 4Q25F. However, we are concerned that these risks have not been fully reflected, as: 1) currently available unfulfilled orders are generally lower-grade CCL/PCBs for general servers (i.e., lower ASICs), unlike Tr2’s 26L full M8 CCL, as some Taiwanese PCB/CCL manufacturers tend to have higher exposure to AWS than to Google (GOOG US, non-rated) TPU and Nvidia’s GPUs; 2) the transition period for AWS may be longer and deeper than PCB/CCL manufacturers expect (some of whom expect only 2-3 months).

However, we remain optimistic about the strong specification upgrades in the AI PCB/CCL industry over the next 2-3 years.

We believe that market expectations for the next 6-8 months need to be recalibrated due to the transition of AWS Trainium, which is the most significant demand for AI PCB/CCL recently, and may have some short-term impact on its suppliers’ sales or earnings compared to already high expectations. However, we remain optimistic about industry trends over the next 2-3 years, as we observe that most new GPUs/ASICs may upgrade to HDI+6 or HLC 30L+ (some even 40L+) structures, with CCL upgrades to M8/M8.5 (a few M9) in 2026F (see Figure 1). As new AI chip production gradually increases from 2Q26F, reaching mass production in 2H26F-1H27F, we believe that demand from PCB and CCL manufacturers will grow strongly starting in 2H26F.

Investment View: Reiterate Buy on Leading Companies – WUS and EMC. Second-tier TUC and ZDT are expected to seize AI PCB/CCL growth opportunities.

For CCL, we maintain a Buy rating on EMC (2383 TT, target price: TWD1,450) and TUC (6274 TT, target price: TWD372). We believe that the AWS ASIC transition may cause some volatility in stock prices in the short term. However, we are optimistic about the long-term upgrade trend for CCL and believe that any short-term weakness is a buying opportunity. EMC, in our view, is well-positioned among various GPU and ASIC customers. Although AWS is currently EMC’s largest AI customer, we believe that in 2026-27F, demand from Nvidia (potentially penetrating into the new mid-layer PCBs of Rubini, in addition to its existing position in switch boards and ASICs, with market share growth in Google and increased ASIC volume and PCB dollar content from Google and Meta) will lead to a more balanced customer exposure in 2H26-2027F. TUC’s stock price was affected in August-September by its sudden drop in AWS Tr2 shipments (due to model transition, it started becoming a second source in June), but we believe that the long-term upgrade trend for AI PCB/CCL and CSP’s competition for future demand will drive growth.

Diversification of the supply chain will make TUC a second source for next-generation products. We believe that by 4Q25F, the next-generation order allocation will become clearer.

For AI PCBs, we reiterate our Buy rating on WUS (002463 CH) and raise the target price to CNY86.8 (see our report). As we mentioned in our mid-August report, we are optimistic about Google’s TPU performance and Nvidia’s short-term downside, as we see an increase in demand for Google’s TPU from 2H25 to 1H26F. We believe WUS is one of the main beneficiaries of Google’s strong demand for TPU v6p and the next-generation TPU starting from 2H26F, which will upgrade PCBs to over 40L, using M8 mixed materials (currently 34L, using M7 materials). Additionally, we believe WUS will benefit from ASICs adopting full-scale switching technology in 2026F, given its close relationships with Quanta (2382 TT, buy), Celestica (CLS US, non-rated), Broadcom (AVGO US, non-rated), Marvell (MRVL US, non-rated), and CSP (AWS, Google). In Nvidia’s Rubini, besides its key position in NVL switch boards, we note that Nvidia will introduce mid-layer PCBs in compute trays and exchange trays to replace connection cables within the trays, and WUS may be one of the main PCB suppliers for these new mid-layer boards.

We maintain a Buy rating on ZDT (4958 TT, target price: TWD190). Although its AI PCB revenue is currently small, we believe it has the potential to penetrate various AI-related PCB opportunities in the next 2-3 years through its strong mSAP and HDI capabilities, as well as expansion in HLC OOC: 1) mSAP for 800G/1.6T optical modules, 2) AI OAM opportunities for GPUs and ASICs, given the upgrades in HDI in OAM, 3) HLC for general server or ASIC projects from Nvidia (especially in Thailand/Taiwan) and CSP. On August 19, ZDT announced plans to invest CNY8 billion in China over the next 2-3 years to build two new factories (one for HDI/mSAP and one for back-drilling processes) to further enhance its cost competitiveness and expand on its existing plans in Thailand and Taiwan.

Copper foil is a game changer in the upcoming CCL upgrades

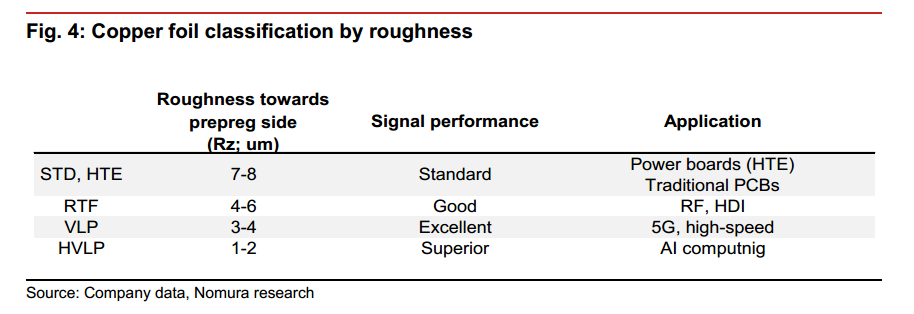

Copper foil is a key component in CCL, and its physical properties and roughness (Rz) parameters may determine the final high-speed digital performance of PCBs. Based on roughness, we mainly classify copper foil into three types: 1) Standard (STD) and High-Temperature Extension (HTE); 2) Reverse Treated Foil (RTF); 3) Very Low Profile (VLP) and Ultra Low Profile (HVLP). See Figure 4 for a summary of Rz comparisons. Within each type of copper foil, each copper foil manufacturer also names its products by generation.

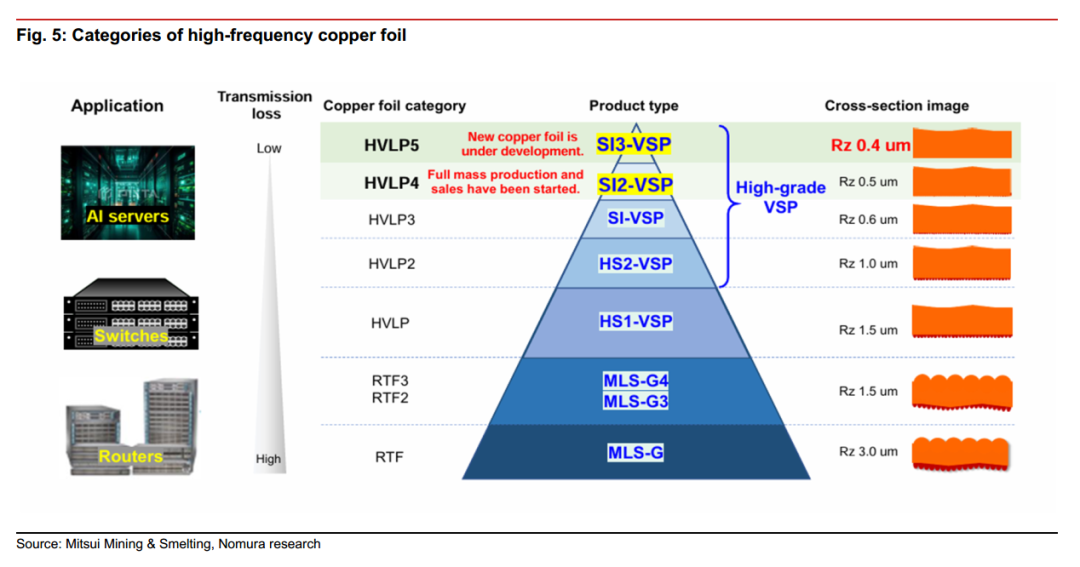

M8 grade CCL is currently the main mass production material used in 800G switches and AI servers, with the most advanced copper foil used in M8 being HVLP3. Given the stricter signal integrity requirements in AI servers (Figure 5), the industry may begin to use HVLP4 copper foil, with copper foil manufacturers including Mitsui Mining & Smelting (MMS; 5706 JP, neutral) and Co-Tech (8358 TT, non-rated) already formulating capacity expansion plans to meet potential demand surges (Figures 6 and 7).

As the PCBs for Nvidia Rubini and AWS Trainium 4 may lead to a supply-demand bottleneck for HVLP4 copper foil in 2026, rapid yield shifts may trigger a supply-demand bottleneck for HVLP4 copper foil in 2026. On the supply side, Co-Tech indicates that converting HVLP3 to HVLP4 incurs at least a 30% capacity loss. Co-Tech estimates that the supply-demand gap for HVLP4 in 1Q26E is negligible, with industry demand around 400-600 tons, but the supply-demand gap may widen to 500-600 tons in 2Q26E, with demand nearly doubling quarter-on-quarter (reaching 800-1000 tons), and further increasing to 1200-1500 tons in 3Q26E.

Meanwhile, industry feedback indicates that the processing price premium for HVLP4 relative to HVLP3 is about 40%, and recent media reports have also indicated that MMS has notified customers of an average price increase of 15% for copper foil.

This is an excerpt from the report, the original report:

“Nomura – AI Printed Circuit Boards and Copper Clad Laminates: Accelerated Upgrades by 2026 – 20250915 [16 pages]”“

Please click the “Read Original” link below to jump to the [Value Directory] computer site for download and reading.