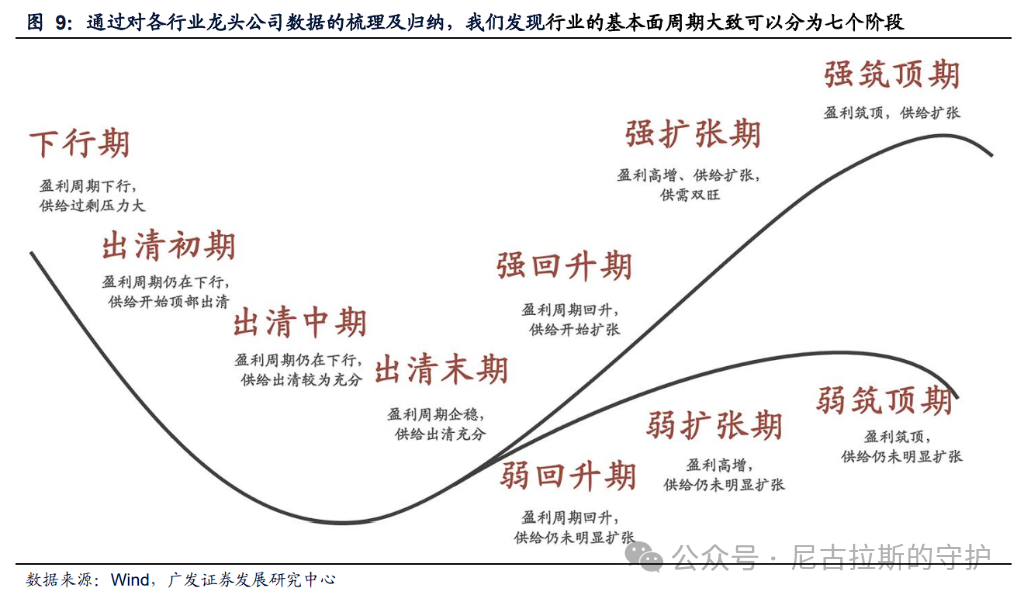

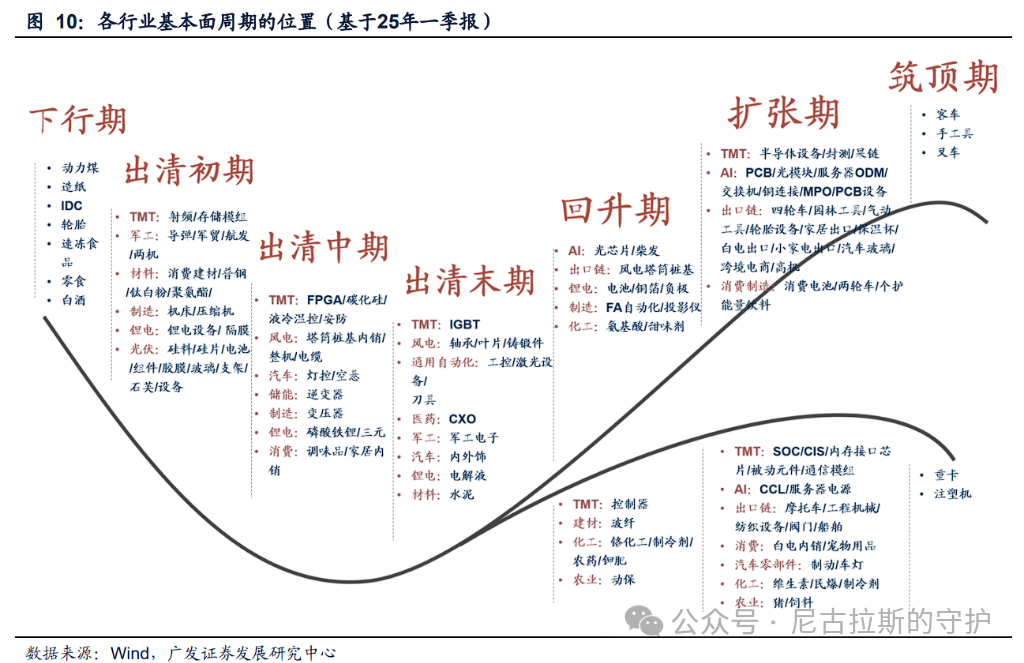

In this bull market, the first half was not missed because I had some undervalued stocks in non-ferrous metals and many undervalued overseas small caps. However, other sectors like banking and the internet have remained lukewarm. Investment is like a ship floating on the sea; you never know when the wind will blow or when the waves will come. What you can do is to layout undervalued stocks in good models.Writing this account is mainly for my own reference. In investment, very few people achieve long-term results. Over the years, I have seen too many dramatic stories where buildings rise and fall based on a single model. The reason is that the leading sectors in each bull market are different, and many people are just random walkers. In contrast, the skilled warriors often appear foolish, significantly underperforming the index in every bull market.However, the key is still survival in the market, which relies on cycles and value.…Looking back, based on the constructed industry comparison database, by analyzing the profit cycles and financial data of leading companies, the fundamentals of various industries in the A-share market can be divided into seven stages: downturn, early clearing, mid clearing, late clearing, recovery, expansion, and topping.Guangfa’s chart is very well done: The industries currently in the strong expansion period are mainly concentrated in AI, exports, and new consumption-related fields, which exhibit characteristics of high revenue and profit growth, capacity expansion, and rising inventory.The varieties in the late clearing period are mainly in the upstream supply chains of pharmaceuticals, automobiles, military industry, and wind power, where supply is clearing, capacity utilization rates are stabilizing at the bottom, and profit cycles are bottoming out and improving for the first time.

The industries currently in the strong expansion period are mainly concentrated in AI, exports, and new consumption-related fields, which exhibit characteristics of high revenue and profit growth, capacity expansion, and rising inventory.The varieties in the late clearing period are mainly in the upstream supply chains of pharmaceuticals, automobiles, military industry, and wind power, where supply is clearing, capacity utilization rates are stabilizing at the bottom, and profit cycles are bottoming out and improving for the first time. 1. In the strong expansion cycle, taking the popular Yizhongtian as an example,specifically,Zhuhai Orbita achieved a revenue growth rate of 37.8% in Q1 2025, with a profit growth rate of 56.8%;New Yisheng performed even better, with a revenue growth rate of 264.1% and a profit growth rate of 384.5%;Tianfu Communication had a revenue growth rate of 29.1% and a profit growth rate of 21.1%. These data fully reflect the strong growth trend of the optical module industry driven by the AI wave.

1. In the strong expansion cycle, taking the popular Yizhongtian as an example,specifically,Zhuhai Orbita achieved a revenue growth rate of 37.8% in Q1 2025, with a profit growth rate of 56.8%;New Yisheng performed even better, with a revenue growth rate of 264.1% and a profit growth rate of 384.5%;Tianfu Communication had a revenue growth rate of 29.1% and a profit growth rate of 21.1%. These data fully reflect the strong growth trend of the optical module industry driven by the AI wave.

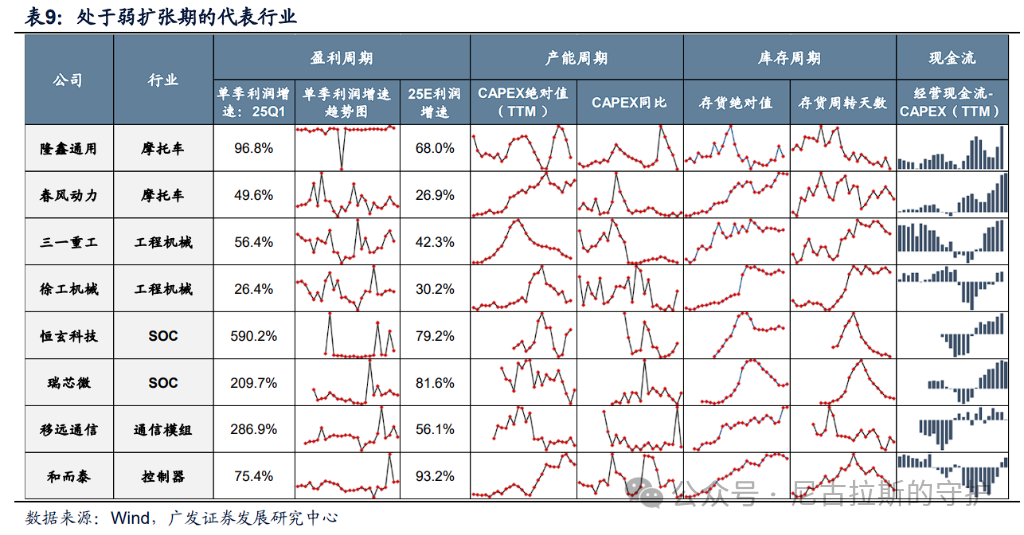

2. Industries in the weak expansion and weak recovery periods are mostly linked to downstream demand, such as consumption and domestic demand, or export chain varieties with a significant domestic demand share, such as SOC, motorcycles, and construction machinery. These varieties are experiencing a warming profit cycle, but due to unclear demand outlooks, companies have not significantly expanded production, accumulating a large amount of cash on their balance sheets. If signals of demand-side recovery can be further confirmed, there is potential for further supply expansion and driving prosperity. For example, in the SOC industry, Hengxuan Technology achieved a profit growth rate of 590.2% in Q1 2025, and Rockchip achieved a profit growth rate of 209.7%, but these companies are relatively cautious about capacity expansion, reflecting uncertainty about future demand.

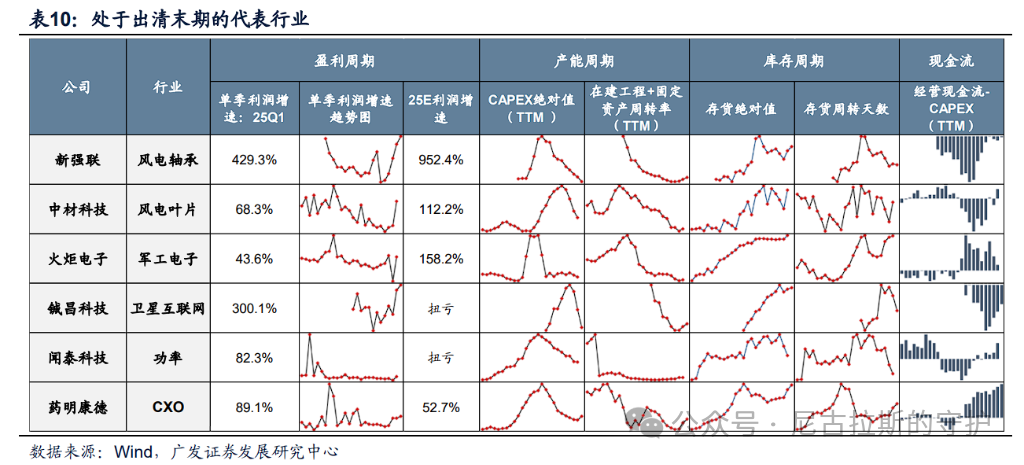

3. The late clearing period represents: CXO, IGBT, military electronics, with varieties in the late clearing period mainly in the upstream supply chains of pharmaceuticals, automobiles, military industry, and wind power, such as CXO, IGBT, military electronics, and wind power bearings. These varieties are clearing supply, capacity utilization rates are stabilizing at the bottom, profit cycles are bottoming out and improving for the first time, and some cash flows on the balance sheets are also improving, waiting for demand to further warm up and enter the recovery period. For example, in the CXO industry, WuXi AppTec achieved a profit growth rate of 89.1% in Q1 2025, and Kanglong Chemical achieved a profit growth rate of 52.7%, indicating that the fundamentals of the industry have begun to improve from the bottom. New Qianglian, as a representative of wind power bearings, achieved a profit growth rate of 429.3% in Q1 2025, reflecting the reversal characteristics of the late clearing period industry.

…

A picture is worth a thousand words, focusing on the strong expansion period and the late clearing period. However, human nature is often overly pessimistic, so the late clearing period and weak recovery period are more worthy of attention: innovative drug ETFs, WuXi AppTec, WuXi Biologics, Kanglong Chemical, New Qianglian, Longxin General,