Click the blue text to follow us

In the third quarter of 2025, the global semiconductor market reached a milestone, with the market size exceeding $200 billion for the first time, and the recovery momentum in the first three quarters far exceeded expectations.

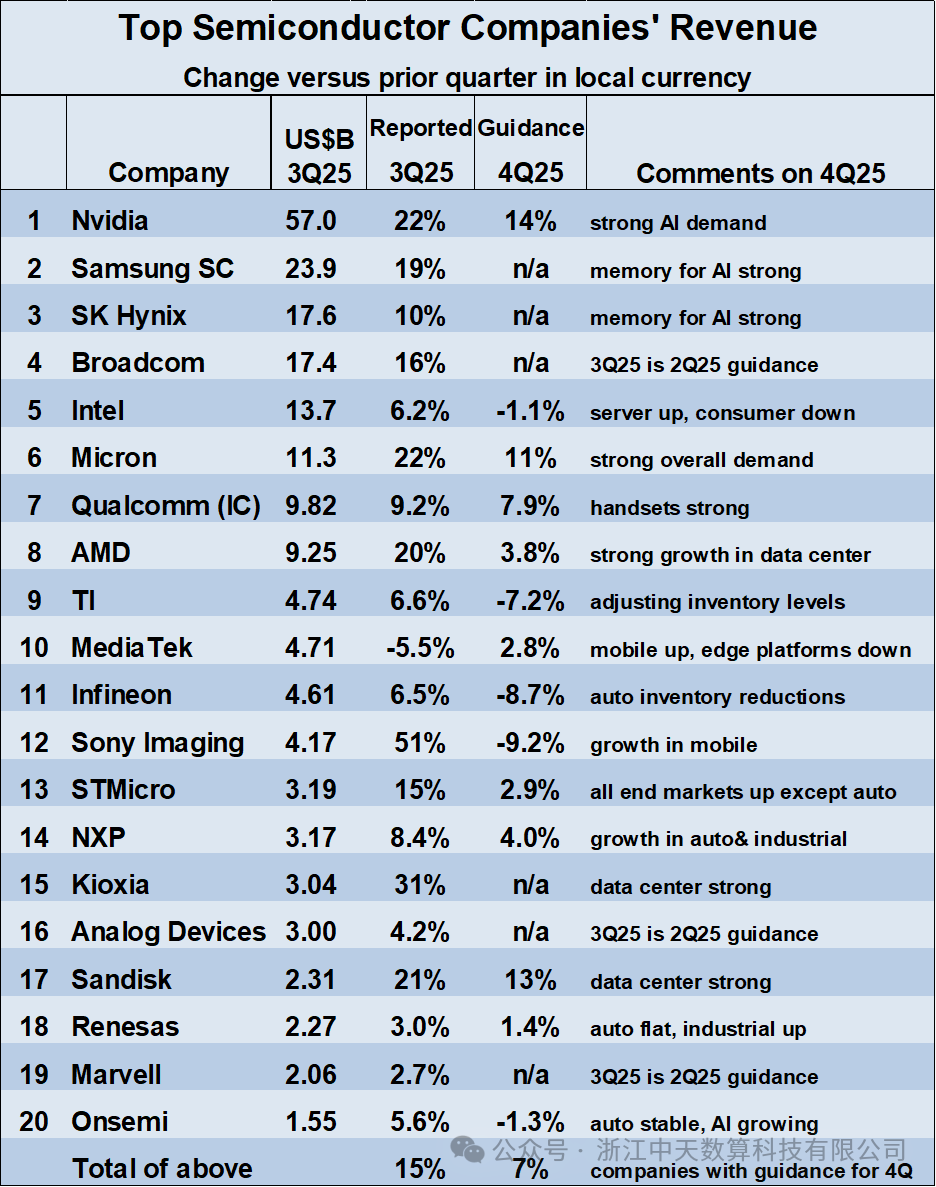

1. Global TOP 20 Landscape

Image from the internet

The leading companies show a pattern of “one strong leader and two strong competitors.” NVIDIA, with its absolute advantage in AI chips and GPUs, secured the top position with $57 billion in revenue, becoming the biggest winner. Samsung and SK Hynix ranked second and third with $23.9 billion and $17.6 billion, respectively, benefiting from the rebound in memory chip prices and demand for AI infrastructure, with year-on-year revenue growth of 19% and 10% for both companies.

The memory sector has fully rebounded, with Kioxia, Micron Technology, and SanDisk achieving revenue growth rates of 31%, 22%, and 21%, respectively. In the non-memory sector, Sony Imaging leads with a 51% quarter-on-quarter growth rate, while AMD, Broadcom, and others achieved around 20% quarter-on-quarter growth thanks to AI-related products. MediaTek is the only leading company with a revenue decline, reflecting a 5.5% drop due to intensified competition in the mobile terminal market.

According to WSTS forecasts, the global semiconductor market size will reach $728 billion in 2025, a year-on-year increase of 15%, and is expected to exceed $800 billion in 2026, aiming for a trillion-dollar mark before 2030. This growth is not a single-point explosion but shows three major trends:

-

The entire AI industry chain continues to benefit, with demand covering data centers, smart vehicles, consumer electronics, and more, from cloud computing chips to edge AI sensors.

-

Technological iterations may focus on advanced process and packaging technologies, with TSMC’s 3nm and 5nm processes accounting for 60% of revenue, and the capacity of advanced packaging technology CoWoS continuously doubling, becoming key to breakthroughs in AI chip performance.

-

The market structure is increasingly differentiated, with rapid growth in AI servers, power management, and high-value-added storage, while traditional consumer electronics-related fields show a mild recovery.

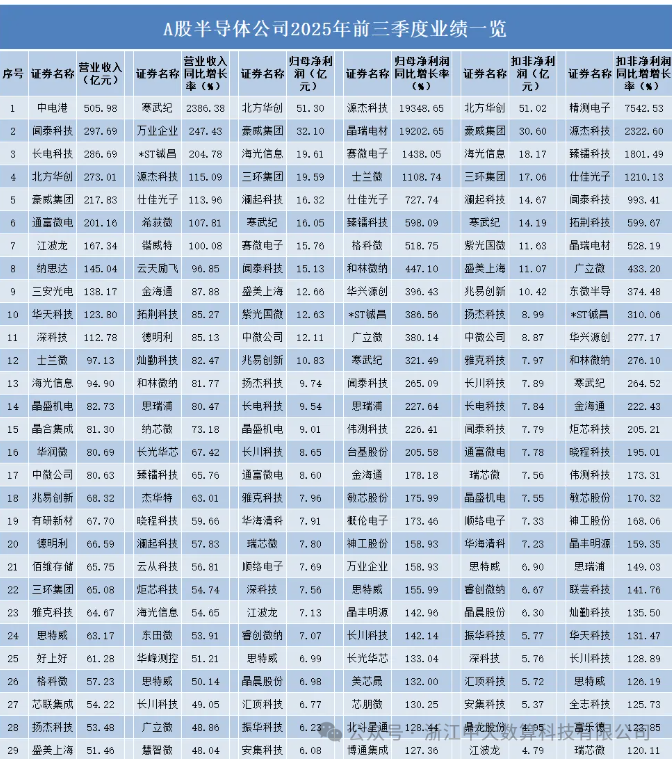

2. Domestic Semiconductors: Performance Explosion and Accelerated Substitution Drive

Image from the internet

In sync with the international market, the domestic semiconductor industry also delivered impressive results in the first three quarters of 2025. Among the 228 semiconductor companies listed in A-shares, 84.65% achieved revenue growth, and 78.51% saw year-on-year increases in net profit attributable to shareholders, with Cambrian Technology achieving a staggering revenue growth rate of 2386.38%, becoming a dark horse in the sector.

Among the leading companies, China Electronics Port ranked first in the sector with a revenue of 50.598 billion yuan, while Changjiang Electronics Technology and Northern Huachuang both surpassed 20 billion yuan in revenue, consolidating their advantages in packaging and testing and semiconductor equipment; SMIC’s revenue grew by 23.14% year-on-year, demonstrating the scalability of mature processes. More importantly, domestic substitution has made breakthroughs in key areas: automotive-grade AI chips have been installed in models from BYD, NIO, and others, and the localization rate of semiconductor equipment is steadily increasing, with several companies achieving high growth in areas such as optical chips and RF front-end.

From the global landscape to domestic breakthroughs, the semiconductor industry in 2025 is standing at a new growth starting point. The deep penetration of AI technology and the continuous deepening of domestic substitution will jointly drive the industry to achieve qualitative leaps in the next five years. For domestic companies, this is both a track of opportunities and challenges, as well as a critical window for achieving self-controllable industrial chains.

The data and information in this article come from:

- World Semiconductor Trade Statistics (WSTS) Q3 2025 Global Semiconductor Market Report

- Semiconductor Industry Association (SIA) Q3 2025 Sales Data

- Jiemi Network “2025 Q1-Q3 A-share Semiconductor Company Performance Rankings”

- Sina Finance “Nearly 50 Chip Companies Latest Financial Reports: Rise, Rise, Rise!”

- China Business Journal “2025 Expected to Grow 11% Global Semiconductor Returns to Growth Track”

- Semiconductor Industry Observation “Top 20 Semiconductor Companies, Latest Rankings”

- Eastmoney “2025 First Half Semiconductor Listed Companies Revenue and Profit Rankings”

- IDC “2025 Global Semiconductor Industry Outlook” Report

END