Abstract:

Domestic manufacturers of complete machines and optics possess global competitiveness, with significant potential for domestic substitution of emitters and detectors.The acceleration of LiDAR industrialization has brought investment opportunities to the domestic supply chain.Domestic companies in the optical system field have global competitiveness in areas such as collimating mirrors, beam splitters, diffusers, and mirrors.The proportion of VCSEL in emitters is expected to increase, with the market size projected to reach $3.9 billion by 2027.For detectors, APD is evolving towards SiPM and SPAD.Frost & Sullivan predicts that the global automotive LiDAR market size is expected to reach $24.7 billion by 2026 and grow to $87.2 billion by 2030.

01

LiDARIndustry ChainAnalysis

1.1 Product Breakdown: Composed of Emitter, Scanning Module, Receiver Module, and Control Module

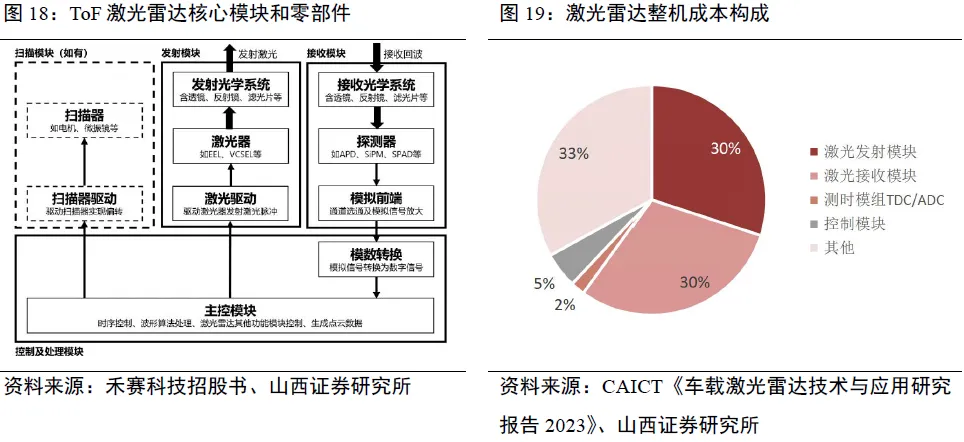

The LiDAR industry chain mainly includes upstream components, midstream complete machine manufacturing, and downstream applications such as robots and autonomous vehicles. A complete LiDAR system generally consists of four parts: emitter module, scanning module, receiver module, and control module. According to the China Academy of Information and Communications Technology, the four major optoelectronic systems (emitter module, receiver module, timing module (TDC/ADC), and control module) account for about 70% of the cost of the LiDAR system.

Chinese LiDAR companies hold over 70% of the global market share. Currently, the most competitive manufacturers in the LiDAR market are mainly located in China, the United States, and Europe. According to Yole data, in 2022, Hesai Technology maintained the largest share of 47% in the global automotive LiDAR market for two consecutive years, leading in both ADAS and autonomous driving LiDAR fields; Innovusion (now renamed Seyond) secured second place with a 15% market share, relying on continuous shipments from NIO; Valeo, Robosense, and Livox ranked third, fourth, and fifth with 13%, 9%, and 5% market shares, respectively. The total market share of Chinese LiDAR companies exceeds 70%.

1.2 Emitter Module: High Potential for Domestic Substitution of Emitters, Competitive Domestic Optical Industry Chain

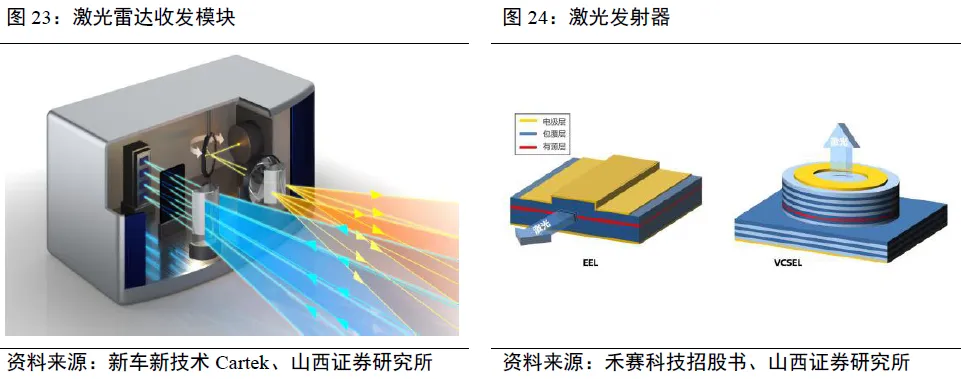

The laser emitter module mainly includes the laser emitter and optical system, which are the core systems of LiDAR.The laser emitter provides the laser light source for the entire LiDAR system. The optical system mainly collimates and shapes the output beam from the laser, improving the output beam quality by adjusting the beam divergence, beam width, and cross-sectional area. The optical system typically consists of collimating mirrors, beam splitters, and diffusers.

Laser emitter

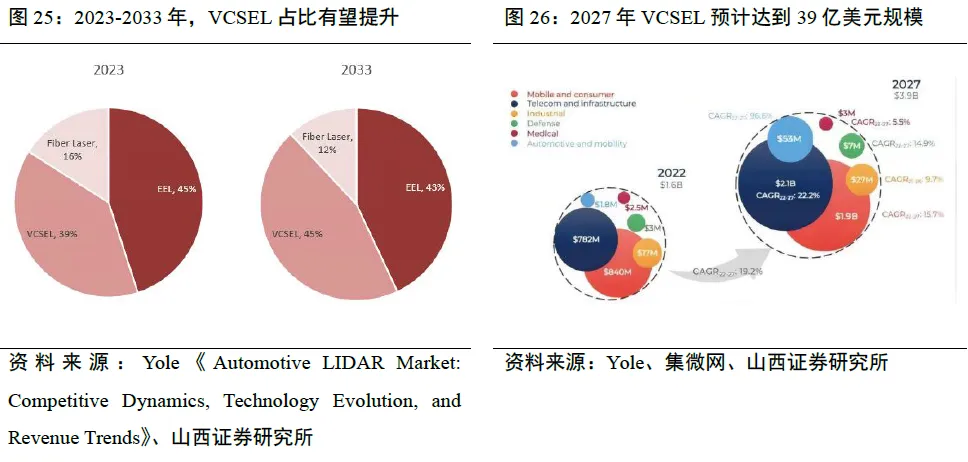

VCSEL proportion is expected to increase, with the market size projected to reach $3.9 billion by 2027.Structurally, laser emitters can be divided into edge-emitting lasers (EEL), vertical-cavity surface-emitting lasers (VCSEL), and fiber lasers. EEL has advantages in output power and electro-optical efficiency, but its beam quality is poorer, and production costs are relatively higher than VCSEL. VCSEL offers advantages such as small size, ease of integration, scalable production, low cost, and high reliability, but its output power and electro-optical efficiency are lower than EEL.

Fiber lasers are more complex and have a smaller application proportion in the LiDAR field. In recent years, domestic and foreign manufacturers have successively introduced high-power multi-layer VCSELs, significantly increasing optical power density, and high-power VCSELs have started to replace some traditional EEL solutions. Yole predicts that by 2033, the proportion of VCSEL is expected to gradually increase from 39% in 2023 to 45%, while EEL will slightly decrease to 43%. In terms of market size, VCSEL is expected to reach $3.9 billion by 2027, while EEL is projected to reach $7.4 billion.

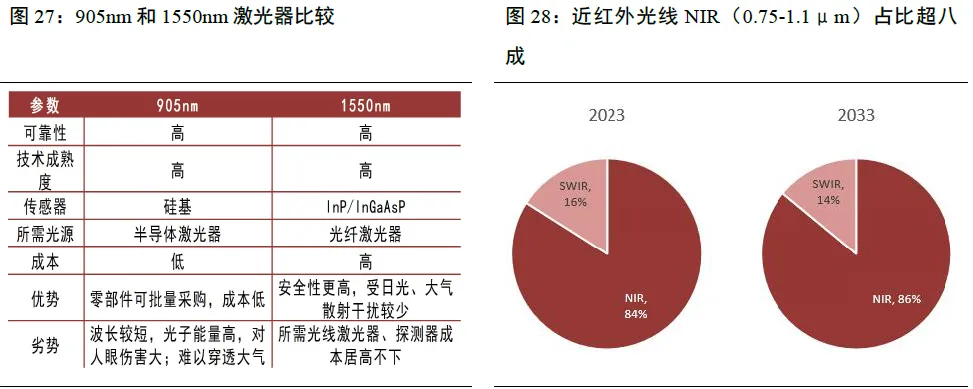

905nm light source is expected to remain dominant. The selection of laser wavelengths balances performance and safety for human eyes; currently, the mainstream LiDAR systems primarily operate at 905nm and 1550nm wavelengths.The advantage of 905nm is based on the GaAs material system, which is mature and low-cost; its disadvantage is that the output power is limited by safety for human eyes, resulting in shorter detection distances. The advantage of 1550nm is that it is more retina-friendly, allowing for higher power output and longer detection distances; however, it cannot use conventional silicon absorption and requires more expensive indium gallium arsenide (InGaAs) material, leading to higher costs.

However, as the 905nm technology continues to upgrade (Hesai has released the 905nm cabin LiDAR ET25, with a detection distance of 250 meters @10%, comparable to 1550nm), and due to the high cost of 1550nm, it is expected that 905nm lasers will remain dominant in the future. Yole data shows that by 2033, NIR (0.75-1.1μm, mainly 905nm and 940nm) is expected to increase its proportion from 84% in 2023 to 86%.

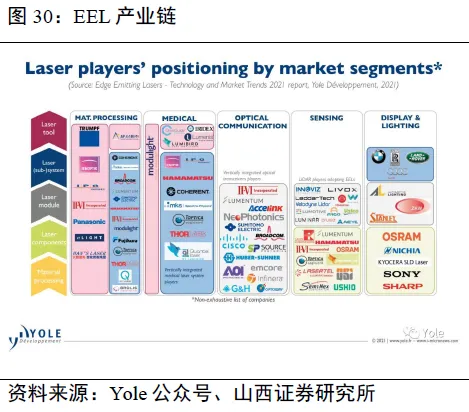

Overseas companies lead the laser emitter market, with significant potential for domestic substitution.The primary participants in the VCSEL market include Coherent, Lumentum, Ams-Osram, Trumpf, etc., with Osram leading in automotive applications (such as LiDAR or in-cabin sensors). The market leaders for EEL include Coherent, Lumentum, Ams-Osram, Hamamatsu, Laser Components, etc. Domestic companies in the relevant industry chain include Changguang Huaxin, Juguang Technology, Ruibo Optoelectronics, and Zonghui Xinguang.

1.3 Optical System

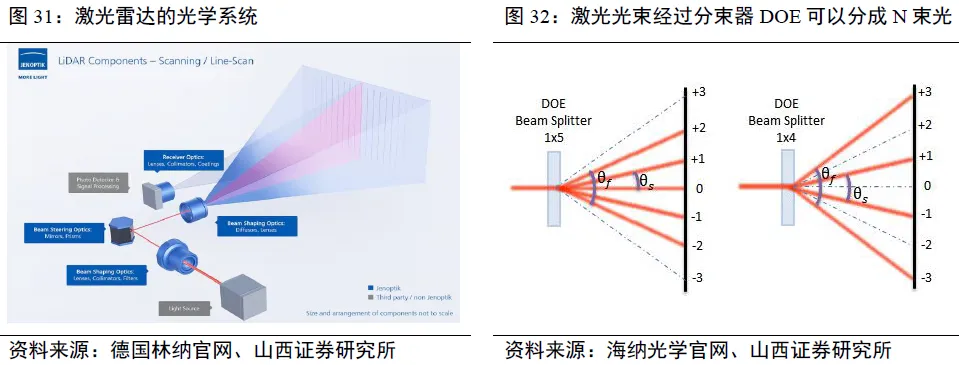

The domestic optical system industry chain is competitive. The optical system generally consists of collimating mirrors, beam splitters, and diffusers.Collimating mirrors address issues such as large divergence angles and irregular beam shapes from laser emissions, allowing for adjustments to beam divergence, beam width, and cross-sectional area to improve output beam quality.

Beam splitters, also known as laser beam splitters or beam splitter DOE, function to evenly divide an incident laser beam into N outgoing beams, maintaining the same beam diameter, divergence angle, and direction of the incident laser.Diffusers, also known as homogenizing lenses or homogenizers (DF/HM), convert incident lasers into uniformly shaped, sized, and intensity-distributed spots. The domestic optical system industry chain is relatively mature, with companies such as Juguang Technology, Yongxin Optics, Lante Optics, Crystal Optoelectronics, Tengjing Technology, and Fuzheng Technology having relevant business layouts.

1.4 Receiver Module: Detector Mainly from Overseas Manufacturers, Urgent Development Needed for Domestic Supply Chain

Laser detectors are devices that convert optical signals into electrical signals.Detector types mainly include PIN photodiodes, avalanche photodiodes (APD), single-photon avalanche diodes (SPAD), and silicon photomultiplier diodes (MPPC/SiPM). PIN detectors are low-cost and simple in structure but have lower sensitivity due to the lack of gain (the ability to amplify electronic signals after converting optical signals). APDs have high sensitivity due to the