(Report Produced By: Tianfeng Securities, Pan Yan)

1. Automotive Chips: Accelerating Industry Transformation and Upgrading, Opportunities Emerging Amidst the Waves of Intelligence and Electrification

We are optimistic about the automotive industry, which is expected to welcome a revaluation opportunity from value to growth under the wave of intelligence and carbon neutrality policies. Automotive chips are likely to be revalued under the empowerment of intelligence, becoming a new driving force in the semiconductor industry. Driven by intelligence, the automotive industry is expected to achieve industrial transformation and accelerate into a new era of Internet of Everything and Intelligent Connectivity. Currently, consumer electronics have already stepped into the era of intelligence, while the automotive industry, which is lagging behind the consumer electronics industry (from feature phones to smartphones), is still in the information age. In the future, it faces a new industrial upgrade from the information age to the intelligent age, and the overall process can be likened to the transition from feature phones to smartphones.

1.1. Growth Momentum: Electrification + Intelligence Accelerate, Automotive Chips Are the Fastest Growing Downstream

According to data released by HiSilicon at the 2021 China Automotive Semiconductor Industry Conference, the era of automotive intelligence + electrification has begun, driving both the volume and price of automotive chips to rise. It is expected that the proportion of automotive electronics in the total cost of vehicles will reach 50% by 2030. Under the trend of electrification and intelligence, the main control chips, memory chips, power chips, communication and interface chips, sensors, and other chips are rapidly developing, with the unit value of chips continuously increasing and the overall value of vehicle chips continuously climbing.

The automotive intelligent terminal will become the nerve endings of the intelligent age, and automotive chips are the core enabling the automotive industry to enter the intelligent age. From perception of the physical world to expression of the physical world, automotive intelligent terminals will become the nerve endings of the intelligent age, requiring four basic capabilities: connectivity, perception, expression, and computing capabilities, which need a large number of chips to support realization. Policies benefit from carbon neutrality promotion, and the wave of electrification is rising, with a positive outlook for the rapid growth of new energy vehicles. According to the global ban on fuel vehicles announced by STMicroelectronics at the 2021 China Automotive Semiconductor Industry Conference, China is expected to completely ban gasoline and fuel vehicles by 2040. The IEA predicts that by 2050, electricity will account for 45% of the overall transportation sector, while the proportion of fossil energy will decrease to 10%.

Electrification has perfectly completed its carbon reduction mission in the first half, and the industry pattern has gradually taken shape. As we enter the second half, how should numerous new energy vehicle players compete? The baton is now passed to “intelligence”, which is the top priority for automakers in the second half. This is not only a competition between new energy and “new forces”. The trend of automotive intelligence is clear, and L2+/L3 has become a basic consumer need. iResearch predicts that by 2025, the production and sales of intelligent driving vehicles in China will exceed 20 million units, with L2+/L3 accounting for more than half, and the continuous iteration of autonomous driving will drive the rapid growth of automotive chips.

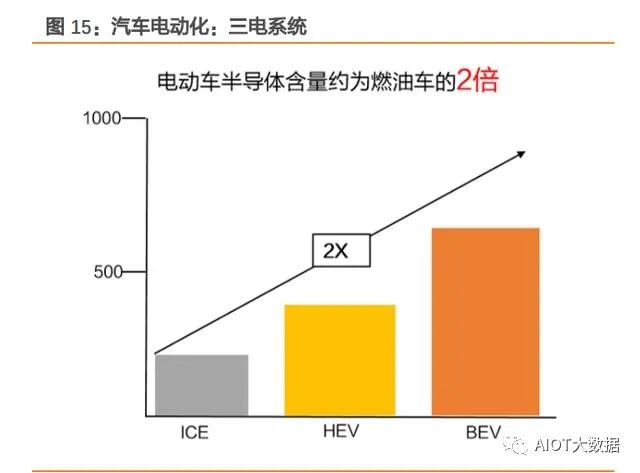

Automotive intelligence + electrification lead to a continuous increase in the semiconductor content of vehicles, with intelligence driving a higher increase in semiconductor content. The semiconductor content of electric vehicles is about twice that of fuel vehicles, while the semiconductor content of intelligent vehicles is N times that of traditional vehicles, indicating a new round of growth trend in the semiconductor industry driven by new energy vehicles.

Taking intelligent sensors as an example, under the wave of automotive intelligence, the semiconductor content will increase from the L2 level of $160-180 to the L2+ level of $280-350, and to above $1150-1250 at the L4/L5 level.

Historically, the growth of the semiconductor industry has been driven by a few killer applications. We are optimistic about the rapid growth of automotive semiconductors under the background of the intelligence + electrification era, which may become a new driving force leading semiconductor development. From the development of the semiconductor industry in the past few decades, we can see that before 2000, semiconductors mainly benefited from demand driven by aerospace, military, and other downstream fields. Between 2000 and 2010, semiconductors mainly benefited from the growth driven by computers and laptops. Between 2010 and 2020, mobile phones, tablets, and other devices drove the growth of semiconductor demand. We predict that between 2020 and 2030, the automotive industry may become a new driving force leading semiconductor development.

1.2. Value Calculation: The New Four Modernizations Development Is Clear, Automotive Chip Demand + Value Growth Together

The new four modernizations of automobiles (“M.A.D.E”, i.e., M-Mobility, A-Autonomous driving, D-Digitalization, E-Electrification) will lead to a significant increase in the value of the entire vehicle’s electronic and electrical components. The BOM (Bill of Materials) value related to automotive electronics and electrical components (including batteries and motors) is expected to increase from approximately $3,145 in 2019 (for luxury brand L1 level ADAS gasoline vehicles) to approximately $7,030 in 2025 (for luxury brand L3 level autonomous electric vehicles).

According to data released by ST at the 2021 China Automotive Semiconductor Industry Conference, compared to traditional vehicles, the forecasted number of various chips used in new energy vehicles will significantly increase. The following are the semiconductor increment calculations for new energy vehicles compared to traditional vehicles: 1) Power management chips: It is expected that the number of power management chips required for new energy vehicles will increase by nearly 20% compared to traditional vehicles, reaching 50 chips; 2) Gate driver: It is expected that the gate driver used in new energy vehicles is a completely new demand, with 30 chips required for each vehicle; 3) CIS, ISP: The demand for CIS and ISP used in new energy vehicles is expected to increase by 50%, with 20 chips required for each vehicle; 4) Display: It is expected that each new energy vehicle will require 8 displays; 5) MCU: The demand for MCUs in new energy vehicles is expected to increase by 30%, with at least 35 chips required for each vehicle; 6) SiC: Similarly, new energy vehicles have a completely new demand for semiconductors.

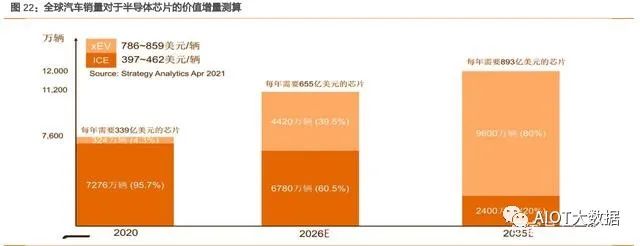

The change in global automotive sales volume has a significant impact on the demand for semiconductor chips: Assuming that the number of semiconductor chips required for traditional vehicles is 500-600 chips/unit, and for new energy vehicles is 1000-2000 chips/unit: Based on the 2020 sales of traditional vehicles of 72.76 million units and 3.24 million units of new energy vehicles, the total global demand for automotive chips is expected to be 43.9 billion chips per year. It is expected that by 2026, the sales of traditional vehicles will be 67.8 million units, and new energy vehicles will be 44.2 million units, with the total global demand for automotive chips increasing to 90.3 billion chips per year. By 2035, the sales of traditional vehicles are expected to be 24 million units, and new energy vehicles will be 96 million units, with the total global demand for automotive chips increasing to 128.5 billion chips per year.

The change in global automotive sales volume has a significant impact on the value increment of semiconductor chips: Assuming that the value of semiconductor chips required for traditional vehicles is $397-462/unit, and for new energy vehicles is $786-859/unit: Based on the 2020 sales of traditional vehicles of 72.76 million units and 3.24 million units of new energy vehicles, the total global automotive chip value is expected to be $33.9 billion. It is expected that by 2026, the sales of traditional vehicles will be 67.8 million units, and new energy vehicles will be 44.2 million units, with the total global automotive chip value expected to be $65.5 billion. By 2035, the sales of traditional vehicles are expected to be 24 million units, and new energy vehicles will be 96 million units, with the total global automotive chip value expected to be $89.3 billion.

The growth forecast for global semiconductor wafer demand: 12 inches: The demand in 2020 was 1.98 million pieces, expected to increase to 4.04 million pieces by 2026, with a CAGR of 12.6%. 8 inches: The demand in 2020 was 11.21 million pieces, expected to increase to 20.88 million pieces by 2026, with a CAGR of 10.9%. 6 inches: The demand in 2020 was 4.43 million pieces, expected to increase to 13.06 million pieces by 2026, with a CAGR of 19.7%. 4 inches: The demand in 2020 was 2.52 million pieces, expected to increase to 8.45 million pieces by 2026, with a CAGR of 22.3%.

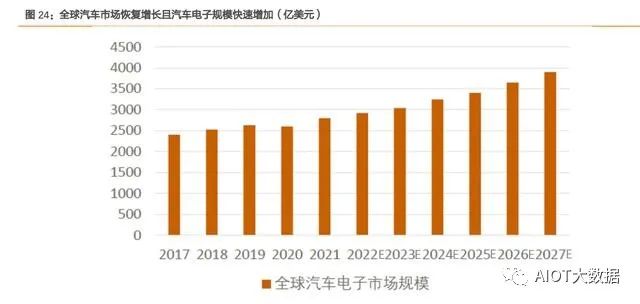

The automotive electronics market size forecast: According to data released by HiSilicon at the 2021 China Automotive Semiconductor Industry Conference, the global automotive electronics market in 2021 was approximately $270 billion, and it is expected to reach nearly $400 billion by 2027. The automotive electronics market is expected to grow at a compound annual growth rate of nearly 7%, with the growth rate of electronic components exceeding that of the automotive market, and the rate of electronicization continuing to increase.

The automotive semiconductor market size forecast: According to data released by HiSilicon at the 2021 China Automotive Semiconductor Industry Conference, the global automotive semiconductor market in 2021 was approximately $50.5 billion, and it is expected to approach $100 billion by 2027, with growth rates of over 30% from 2022 to 2027. The automotive semiconductor market in China is steadily rising, with approximately 100 billion RMB in 2020.

1.3. Chip Shortage Analysis: Automotive Chip Shortage May Persist Throughout the Year, Delivery Cycles Continue to Lengthen

Since September 2020, the issue of work stoppages and production halts due to chip shortages has been particularly prominent, and the pressure to ensure supply of automotive chips has reached unprecedented levels. Since the second half of 2020, the chip shortage has continued to affect the normal supply of ECUs and the production and manufacturing of complete vehicles due to multiple factors such as the pandemic and demand, with a deteriorating trend in chip supply in some areas.

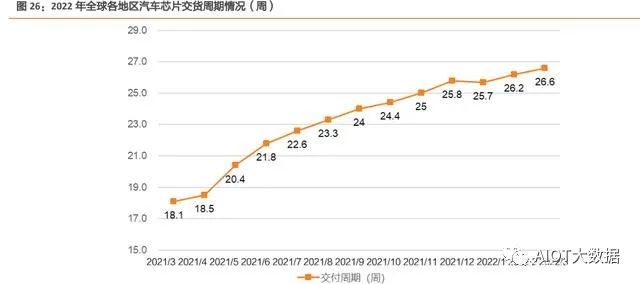

In March 2022, the average delivery cycle for global automotive chips (the cycle from ordering to delivery) increased by two days compared to February, reaching 26.6 weeks, a historical high since March 2021.

According to the latest data from AutoForecast Solutions (AFS), a forecasting company in the automotive industry, as of April 10, due to the chip shortage, the cumulative production reduction in the global automotive market this year is approximately 1.4378 million vehicles. Among them, the cumulative production reduction in the Chinese automotive market remains unchanged at 70,900 vehicles, accounting for 4.9% of the cumulative production reduction in the global automotive market.

Looking at automotive chips, the main types of chips in shortage include: main control chips MCU + power supply chips, driving chips, according to the GAC Research Institute’s calculations, these three account for 74% of the medium to high-risk chip shortage, followed by signal chain chips such as CAN/LIN communication chips.

From the distribution of chip shortages by brand, it can be seen that the shortage mainly comes from traditional automotive chip companies such as NXP, Texas Instruments, Infineon, and STMicroelectronics, with a total of 75% of the medium to high-risk shortages coming from these four companies. In terms of the distribution of the sources of the chip shortage, 77% of the shortage comes from Southeast Asia and the United States, mainly due to the severe pandemic situation in Southeast Asia and the United States, while Taiwan, Japan, and Europe are also facing chip shortage situations.

The ongoing shortage of automotive chips, along with the