Abstract

1

Review: How Texas Instruments Has Navigated Cycles for Growth

1) Business Dimension: Over the past 20 years, Texas Instruments (TI) has experienced four rounds of technology cycles. In the first cycle, TI transformed from a complex conglomerate and laid out its DSP and analog-related products; in the second cycle, TI shone with its OMAP processors; in the third cycle, TI focused on analog; in the fourth cycle, TI achieved record performance relying on industrial and automotive analog chips, reduced agents, and emphasized cost control and product supply capability. Currently, standing at the starting point of a new cycle, we are optimistic about the long-term demand for analog chips driven by AI, electric vehicle intelligence, and AIoT innovations.

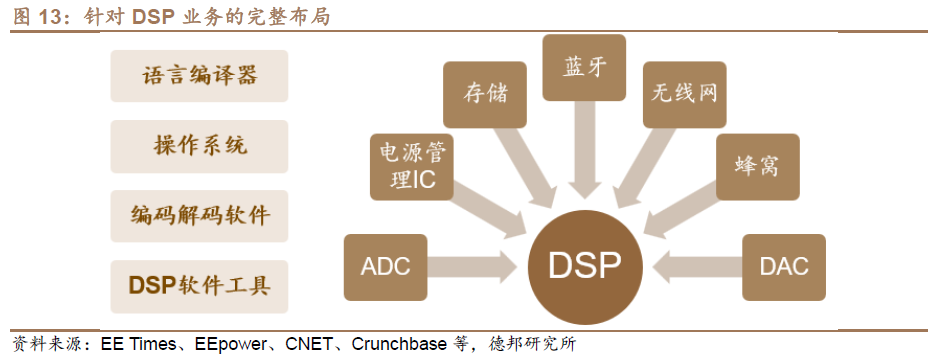

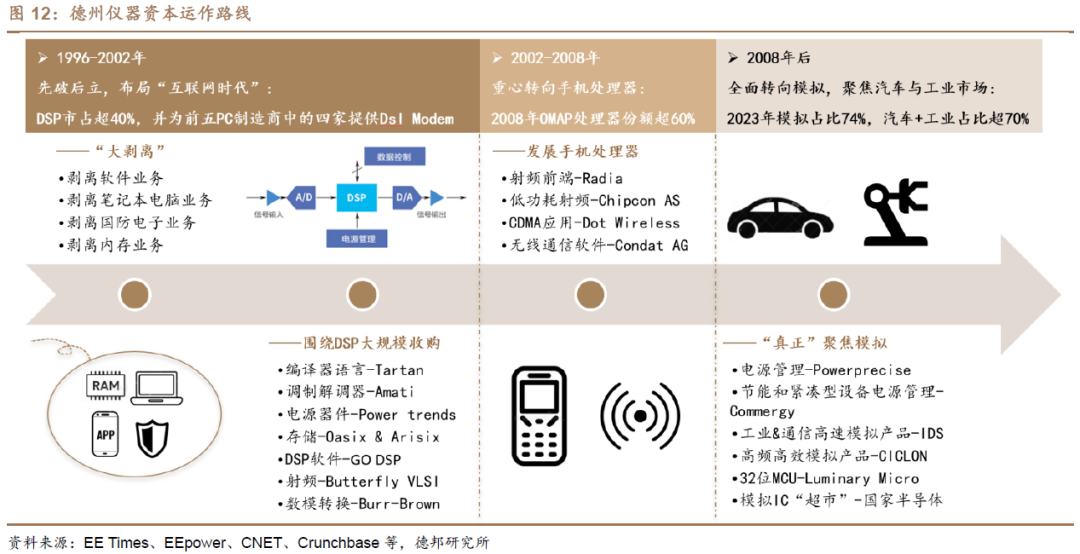

2) M&A Dimension: Since the 1990s, TI has completed nearly 30 divestitures and acquisitions, which we roughly divide into three major transformation periods. Starting in 1996 with “first break then establish,” laying out for the “Internet era”; in 2002, shifting focus to mobile processors; and in 2008, fully transitioning to analog, focusing on the automotive and industrial markets. Through three rounds of external acquisitions and focused transformation, TI has established its leading position in analog ICs.

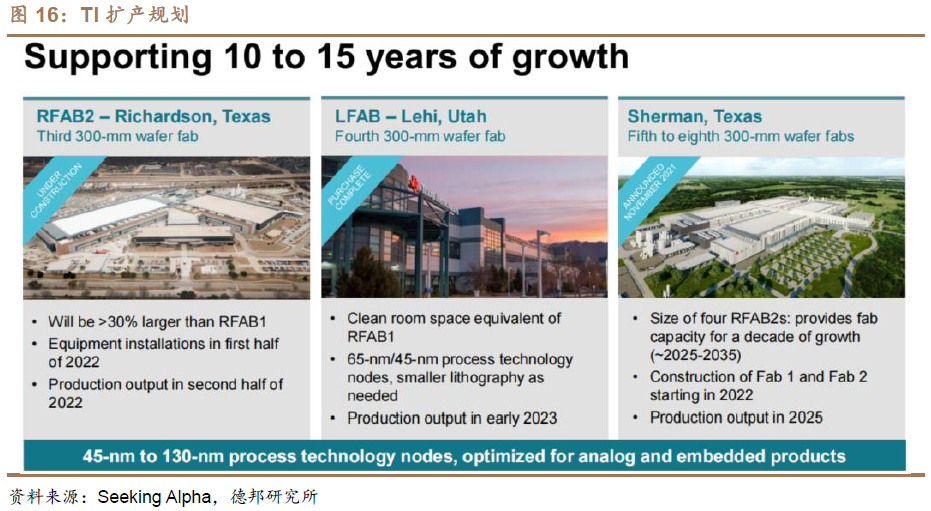

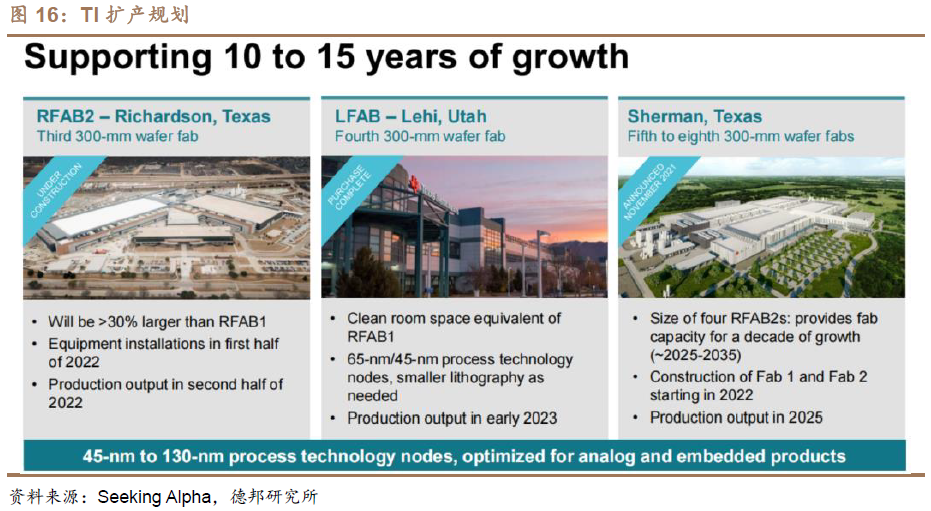

3) Capacity Expansion Dimension: Since 2009, TI has been the first to migrate from 8-inch to 12-inch production lines, reducing chip manufacturing costs by 40%. Additionally, at the bottom of this cycle, TI has expanded capacity counter-cyclically, planning to add six 12-inch wafer fabs from 2021 to 2030 to support growth for the next decade. We believe that as the business stabilizes, cost control and product supply capability may become TI’s future focus areas.

2

Understanding: Why Is the Analog IC Sector a Long and Steady Path?

1) The foundation for electronic devices to “understand” and “operate,” emphasizing deep cultivation and long-term accumulation. Signal chain analog chips act as a bridge between external analog signals and the digital signals that processors can “understand,” while power chain analog chips serve as the “heart” of electronic devices, fulfilling the mission of supplying energy, which is fundamental to the operation of electronic devices. Therefore, analog chips can be found in almost all electronic devices.

Compared to digital chips, which can quickly drive revenue by launching a hot-selling product, analog chips focus more on long-term accumulation, achieving steady revenue growth through the accumulation of part numbers and products. We believe that“entering the market through a strong product, then expanding other products around that market to meet customer needs, and finally providing a complete set of solutions or reference designs” may be the standard path for domestic analog companies to grow stronger.

2) Balanced offense and defense: Broad market space and high growth + excellent anti-cycle properties. According to Statista, the global analog chip market size is expected to reach $77.3 billion in 2023, accounting for about 19% of the global semiconductor market size. Benefiting from the rapid growth in demand for AI and automotive electrification, the market size CAGR is expected to reach 8.5% from 2023 to 2029. Additionally, the wide range of downstream applications, diverse product types, and long product life cycles effectively reduce the overall risk and uncertainty in the analog chip industry, providing a more stable operating environment for analog chip companies.

3) Competitive landscape is fragmented, with vast domestic substitution space. China is the largest analog chip market, but the self-sufficiency rate was only 15% in 2023. Foreign leading manufacturers have revenues in China that far exceed domestic firms. For example, in 2023, TI and ADI’s revenues in China reached $3.3 billion and $2.2 billion, respectively, while leading domestic firms like Sanken and Siretta had revenues of only $140 million and $120 million, respectively. This contradiction may change under the trend of de-globalization. Moreover, the competitive landscape of the analog chip industry is fragmented, with a CR5 of about 50% in 2021, providing opportunities for domestic manufacturers to enter the market.

3

Breaking the Deadlock: How Can Domestic Analog ICs Break Through the Deep Water Zone?

1) The rise, transition, and fall of the current domestic chip cycle:

Beginning (2019): U.S. restrictions on domestic manufacturers’ chip supply to Huawei and other terminal manufacturers directly stimulated domestic terminal manufacturers’ inclination to procure domestic chips.

Development (2019-2021): Technological innovations like 5G and AIOT rapidly boosted consumer electronics demand, while the pandemic affected the supply chain. Therefore, downstream manufacturers adopted conservative inventory strategies, driving up demand for analog chips.

Transition (2021-2023): Due to demand falling short of expectations, along with high channel and terminal inventory from previous stocking strategies, industry competition intensified, leading to a downward cycle for the analog chip industry.

Conclusion (2024 and beyond): Consumer electronics have now recovered, and we expect that as automotive and industrial inventories gradually normalize, the trend of AI and automotive intelligence will steadily increase demand and market size for analog chips.

2) Transition to conclusion: Where does the analog chip industry currently stand?

Short-term view on inventory: The inventory cycle is nearing its end, with consumer electronics recovering first;

Mid-term view on the landscape: The new “National Nine Articles” and “Science Eight Articles” are working together to accelerate industry resource integration, and competition is expected to optimize;

Long-term view on demand: Trends in AI and automotive electrification will contribute to incremental growth, and domestic substitution space is vast;

3) Breaking strategies: “R&D innovation + M&A expansion” may be the main melody for the development of the analog IC industry.

Looking back at TI, it has undergone several acquisitions of analog chip companies throughout its development, including National Semiconductor and Burr-Brown, which rapidly expanded TI’s product portfolio and customer resources. At the same time, transitioning to high-end markets such as industrial control and automotive has also been an inevitable choice. Since 2007, TI has expanded its market and technology through acquisitions while investing more resources in automotive and industrial sectors, gradually achieving results post-2013: the revenue share from automotive and industrial sectors has rapidly increased. The high barriers, broad market, and long product life cycle in these sectors have laid a solid foundation for TI’s leading position in analog.

Combining TI’s development path, we believe that domestic analog manufacturers have sufficient internal conditions to pursue acquisitions and develop high-end markets, while external conditions necessitate industry resource integration and a shift towards high-end:

First, before 2023, the primary market was booming, and the semiconductor industry has been a key focus of domestic policy, allowing many analog IC companies to accumulate substantial funds, enabling them to acquire high-quality targets. At the same time, the tightening financing environment and intensified industry competition forced some small to medium-sized companies to consider being acquired.

Second, domestic analog manufacturers have developed by leveraging opportunities from trade conflicts, but these supply chain advantages will not last forever. To compete with international leaders and even expand into overseas markets, domestic manufacturers must take a long-term view, develop high-end markets, focus on R&D investment and resource integration, and create a positive feedback loop.

Third, overseas leaders adopt IDM models and are gradually shifting to 12-inch production lines, significantly enhancing cost control and product supply capabilities. Domestic analog chip players often use Fabless models; transitioning to IDM or Fab-lite models may be crucial for their development.

Investment Recommendations

Over the past two years, the analog industry has been severely impacted by downstream destocking, resulting in both performance and valuation being hit hard. As consumer electronics recover and markets like automotive and industrial continue to destock, the current inventory cycle is nearing its end. On the other hand, the launch of the “National Nine Articles” and “Science Eight Articles” accelerates industry resource integration, and an optimized competitive landscape can be anticipated.

Standing at the starting point of a new cycle, we are optimistic about the long-term demand for analog chips driven by AI, electric vehicle intelligence, and AIoT innovations. Domestic analog chip manufacturers are expected to benefit from the domestic substitution trend, achieving steady growth and highlighting investment value. We recommend focusing on “companies with strong financial strength and robust product portfolios” and “companies with strong R&D capabilities and forward-looking layouts in key areas”.

Risk Warning

Downstream demand recovery may fall short of expectations; international leaders’ operational strategy changes; trade policy changes;

Table of Contents

Main Text

1

Review: Observing the Analog Development Cycle from TI’s Path

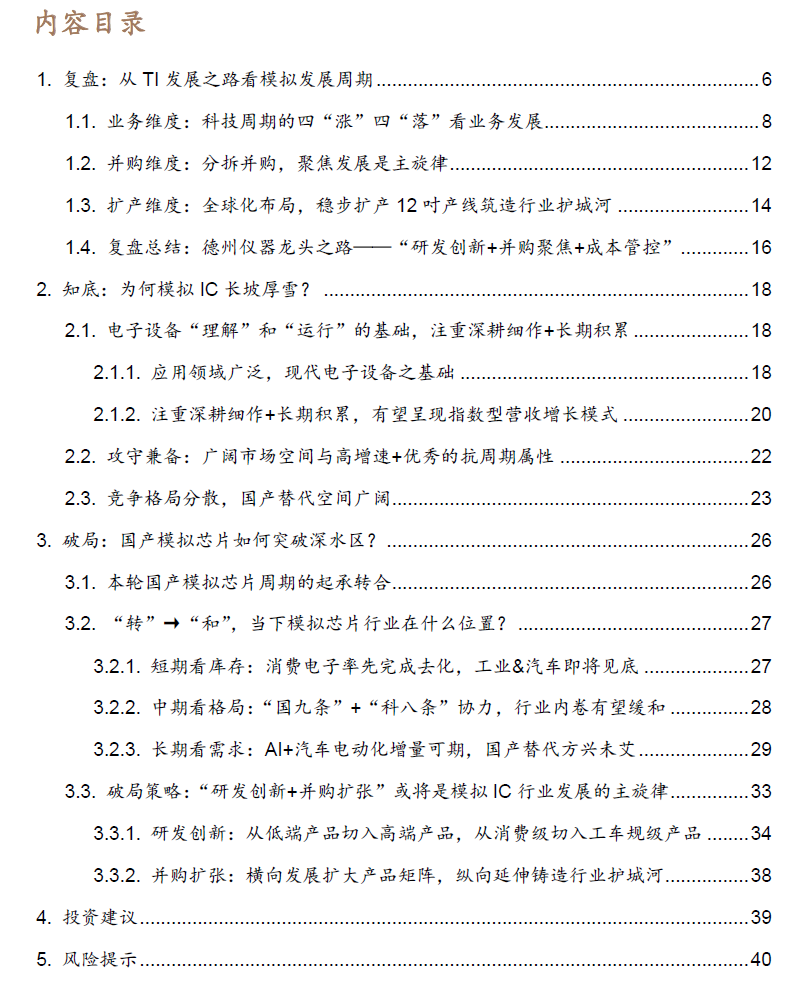

TI is a pioneer in the semiconductor era, the creator of the transistor. TI originated from a geophysical business company, initially producing equipment related to seismic industry and defense electronics. In the early 1950s, it began researching transistors and produced the world’s first commercial silicon transistor. Subsequently, it entered various businesses, including defense systems and consumer electronics. TI’s TMS320 series 16-bit programmable DSP devices were launched in 1983, widely used in consumer products ranging from mobile phones to toys, laying the foundation for its current business. Since the 21st century, TI has ascended to the position of the world’s leading analog chip manufacturer through forward-looking industry layout, focused acquisitions, and stable capacity expansion, holding an absolute market leadership position in the analog chip field. TI’s development history is representative of the industry, and we hope to study the analog industry’s development cycle by reviewing TI’s path.

Vertically, we divide TI’s development into three stages:

1) 2000-2009: Diversified business → Focusing on analog, wireless, and embedded business;

2) 2009-2019: Focusing on analog, with a focus on automotive and industrial markets;

3) Since 2019: Actively expanding capacity, fully transitioning to 12-inch lines, strengthening cost control and supply capabilities.

Before 2000, TI, besides analog and embedded, also had numerous businesses such as laptops, memory, and software contributing to revenue, most of which were divested from 1997 to 2000;

From 2000 to 2009, revenue was primarily contributed by wireless, embedded, and analog businesses. During this period, as feature phone shipments grew and the Internet became widespread, TI’s revenue grew steadily. However, with the advent of the smartphone era, TI, lacking baseband chips, fell behind in competition with Qualcomm and Samsung, choosing to exit the mobile phone market, thus ending its wireless business.

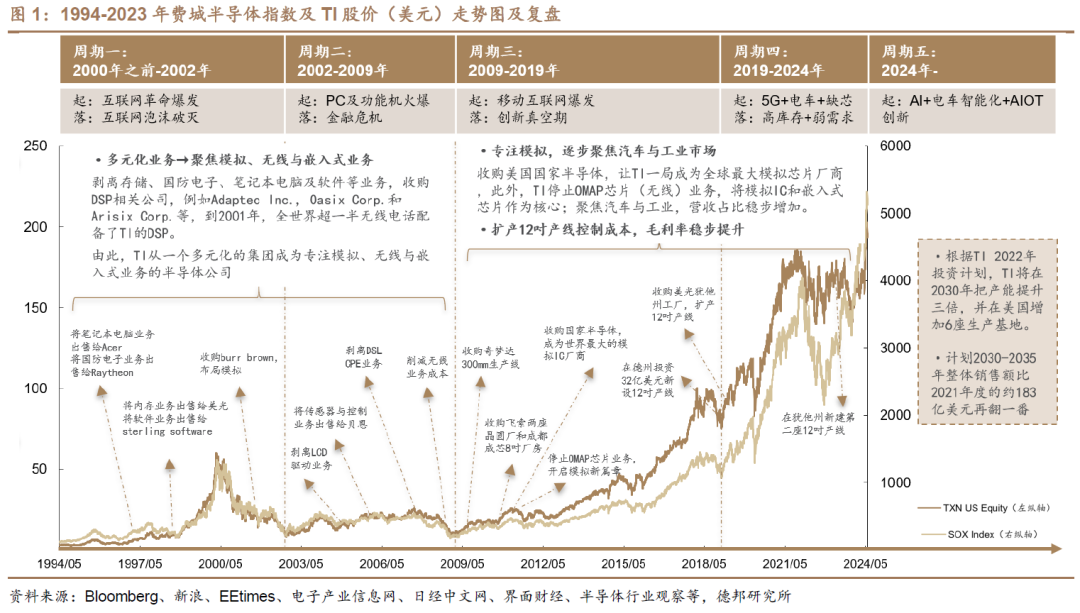

Since 2009, TI’s revenue has mainly come from analog and embedded businesses, with total revenue reaching $20 billion in 2022, of which revenue from analog business accounted for over 70%, and the combined share from industrial and automotive markets exceeded 60%, achieving record highs in both performance and stock price.

At the same time, TI has focused on cost control to improve overall gross margin. On one hand, starting from 2009, TI reduced production costs by expanding its 12-inch lines (acquiring the production line of TSMC), and on the other hand, it announced in October 2019 to reduce agents. TI’s gross margin has steadily increased since 2011, reaching nearly 70% in 2022, a historical high. Meanwhile, a direct sales-focused model requires strong product supply capabilities, and through expanding its 12-inch lines, TI’s inventory days have also shown a long-term growth trend.

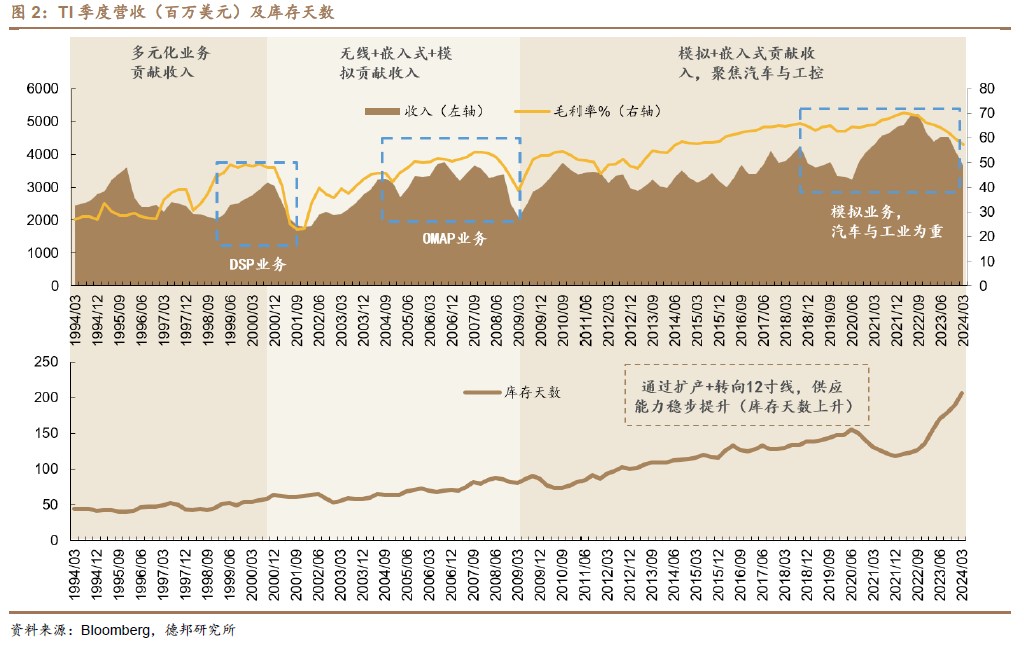

With business transformation, TI’s main downstream applications have shifted from communication devices to industrial control and automotive. The company’s downstream includes industrial, automotive, personal electronics, communication devices, etc. In earlier years, communication was the main market, accounting for more than 40% during 2004-2011. As TI gradually exited the wireless business and fully invested in industrial and automotive sectors, the revenue share from these two areas has increased significantly, reaching a combined revenue share of 74% in 2023. Specifically, the industrial market’s segmented scenarios include industrial control automation, power grids, medical, motors, and industrial transport; the automotive market’s segmented scenarios include power systems, ADAS, body electronics, lighting, and safety.

Below, we will analyze TI’s development history from the following three dimensions:

1. Business Dimension: Strategic development from the perspective of cycles;

2. M&A Dimension: M&A expansion and focused development are the main themes;

3. Capacity Expansion Dimension: Integrated cost reduction is the main trend.

1.1. Business Dimension: Observing the Four “Rises” and Four “Falls” of Technology Cycles in Business Development

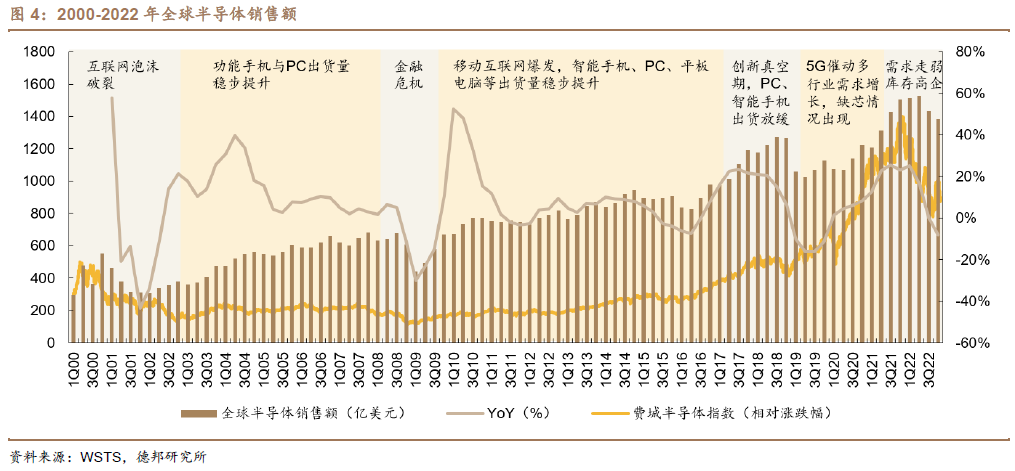

Since 2000, the semiconductor industry has undergone four cycles. It can be said that in any corner that has been digitized, there is the presence of analog chips, and the cycle of the analog industry is strongly correlated with downstream technology cycles. We combine the Philadelphia semiconductor index with the global semiconductor market size, dividing technology cycles into “four rises and four falls,” and focus on TI’s development strategy to observe the history of TI’s development through technology cycles.

1. The PC Internet Bubble Burst

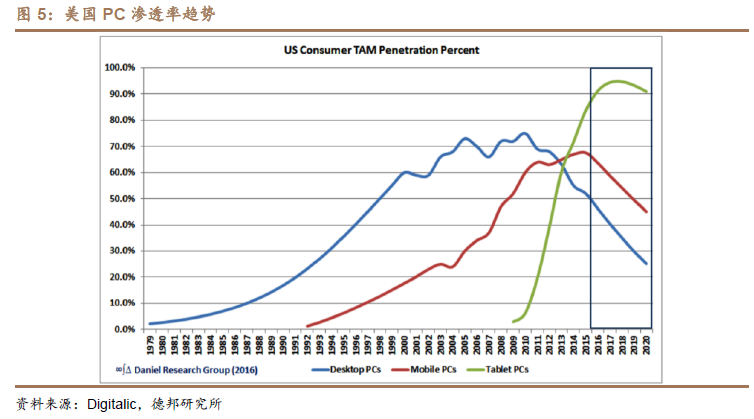

Rise — Internet Bubble (Before 2000): The Internet bubble refers to the speculative bubble events related to information technology and the Internet that occurred between 1995 and 2001. During this period, speculators in Western countries saw the rapid growth of the Internet sector and related fields, pouring funds into this emerging market. On December 15, 1994, Netscape officially released the Netscape Navigator 1.0 browser, promoting the development and popularization of the PC Internet among the public, marking the beginning of the PC Internet cycle; from 1990 to 1997, as computers evolved from “luxury goods” to necessities, the proportion of American households owning computers increased from 15% to 35%.

Fall — Internet Bubble Burst (2000-2002): We believe the main reasons for the bursting of the Internet bubble are twofold: 1) As PC penetration gradually saturated, growth in the Internet hardware sector slowed. At the same time, poor performance from internet retailers during the 1999 Christmas season was revealed to the public in March 2000, demonstrating that the strategy of “growing larger first” was wrong for most companies; 2) The stock prices of internet companies at that time generally lacked fundamental support, and with multiple interest rate hikes by the Federal Reserve between 1999 and 2000, along with Japan’s economic recession in March 2000, market risk appetite changed, leading to a sell-off of internet company stocks. Thus, this round of cycle began to decline.

#Focusing on TI:Divesting multiple businesses, focusing on developing analog and DSP businesses, and concentrating on the signal processing market.

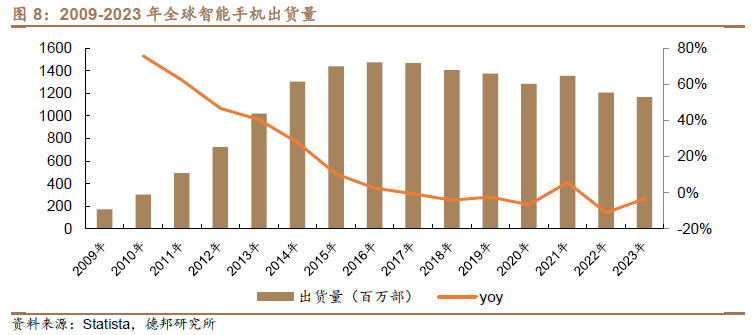

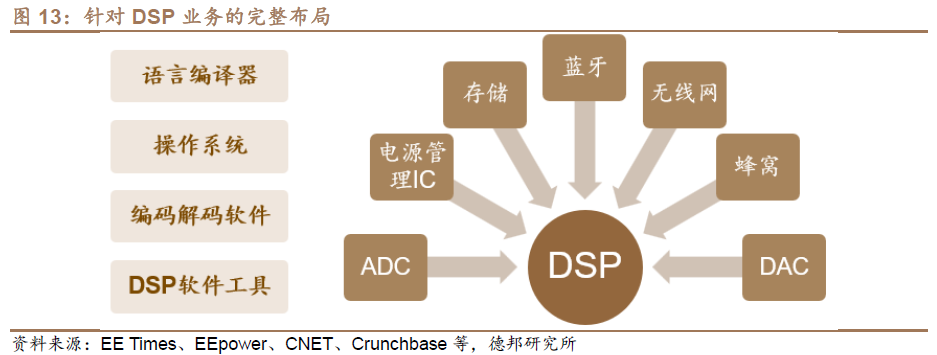

In 1996, TI began a series of acquisitions and asset divestitures, focusing on developing analog and DSP businesses. The revenue share of DSP and analog businesses in the entire semiconductor business increased from 45% in Q4 of FY1997 to 65% in Q1 of FY2001.

TI centered around DSP, with analog chips assisting DSP in providing a complete solution. During this period, it provided DSL modems (based on DSP) for four of the top five PC manufacturers, with DSP market share exceeding 40% in 2002. Benefiting from the rapid growth in PC demand during this cycle, the company’s revenue reached $11.9 billion in CY2000, a year-on-year increase of 22%, and the gross margin also reached a recent high of 49.3% in the third quarter of 2000.

2.3C Demand Cycle Initiation

Rise — Rapid Growth of Mobile Phones and PCs (2002-2007): Computers, communications, and consumer electronics began to enter the household view through the Internet. Starting in 2003, global PC shipments began to show a steady growth trend, breaking 200 million units for the first time in 2005. At the same time, the development of 2G and 3G wireless communication technology drove a surge in mobile phone sales.

Fall — Financial Crisis (2008): The global economy fell into an unprecedented financial crisis, which severely impacted developed countries such as the U.S. and Europe and had far-reaching effects on the global economic system. Subsequently, the economic crisis spread from the financial sector to the real sector, leading to a global economic recession and a downturn in the technology industry cycle.

#Focusing on TI:Falling behind in mobile processor market, fully transitioning to analog.

With the arrival of 3G, smartphones require baseband chips, but Texas Instruments’ processors only had GPUs and some DSP units, lacking a complete 3G and 4G baseband chip, thus losing to competitors like Qualcomm and Samsung. According to Strategy Analytics’ report on the global smartphone chip market in the first half of 2012, Qualcomm held 48% of the revenue market share, ranking first; TI’s ranking dropped from the top three to fifth place; Samsung, MediaTek, and Broadcom ranked second, third, and fourth, respectively. Against the backdrop of declining revenue and market share, TI finally announced a significant reduction in wireless business costs in November 2012, reallocating more resources to the automotive and industrial markets. From then on, TI fully transitioned to analog.

In fact, TI began reserving resources for the analog business through acquisitions as early as 2007, completing one of its most significant acquisitions in 2011: National Semiconductor, which expanded TI’s product numbers from 30,000 to 42,000, allowing it to achieve a market share of 15.4% in 2011, maintaining the top position with a share of 16.7% in 2012. Since then, TI’s analog IC business revenue has dominated globally, indicating that the development of the analog chip business has become TI’s strategic goal.

4. Disruptions from the Pandemic Triggering Supply-Demand Conflicts

Rise — Upward Cycle of Consumer Electronics + Chip Shortages (2019-2021): Since 2018, consumer electronics such as TWS and smartwatches have rapidly penetrated the market, leading to an upward cycle. Coupled with the emergence of the COVID-19 pandemic as a “black swan,” which led to a global trend of remote work and online education to reduce contact with pathogens, the demand for consumer electronics surged. On the supply side, the pandemic caused disruptions in production, affecting supply chain delivery times, while the booming consumer electronics market squeezed production capacity from other downstream markets, leading to severe chip shortages in markets such as automotive electronics, resulting in rising analog chip prices and an overall upward movement in the industry.

Fall — Demand Slows, Inventory Rises (2021-2023): As demand for consumer electronics such as PCs, smartphones, and tablets sharply declined, terminal sales plummeted. Coupled with severe inventory buildup from previous stocking strategies, downstream manufacturers significantly reduced purchases of upstream raw materials. The semiconductor market entered a significant adjustment cycle, starting a downward cycle for this round.

#Focusing on TI: Revenue and Business Stabilization, Emphasizing Cost Control

As the acquisitions accumulated during the previous cycle gradually took effect, TI achieved significant success in the analog field. From 2019 to 2022, the revenue share from the automotive and industrial sectors stabilized above 55%. Therefore, in this round of cycle, as revenue and business gradually stabilize, TI focused on cost control: on one hand, TI announced in October 2019 to reduce agents, and starting in 2021, it reduced its original four agents down to just one, shifting to a predominantly direct sales model. On the other hand, TI initiated a new round of 12-inch line expansion starting in 2019 to reduce chip production costs and ensure product supply capabilities under the direct sales model.

Additionally, during the downturn of the industry cycle, TI also chose to reduce capacity utilization under financial report pressure to reduce inventory and maintain gross margin, planning to close the last two 6-inch plants by 2023 and 2025, while starting to join price wars to retain more market share amid fierce industry competition. However, the final outcome showed that TI did not achieve significant success—expanding capacity to gain market share and reducing capacity utilization to protect gross margin inherently conflict, and execution presents certain pressures and difficulties. Ultimately, TI’s share and gross margin both declined. According to KHAVEEN Investment data, TI’s market share fell from 19.0% in 2021 to 16.1% in 2023. Gross margin also dropped from 70.2% in Q1 2022 to 57.2% in Q1 2024.

1.2. M&A Dimension: Divestiture and Acquisition, Focusing on Development is the Main Theme

Since the 1990s, TI has completed nearly 30 acquisitions, all closely related to its strategic goals. Reviewing TI’s acquisition path, it has acquired software companies to synergize with its DSP business, acquired RF frontend companies to synergize with its OMAP processors, and acquired analog chip companies to synergize with its DSP business. Ultimately, TI has divested software, storage, and mobile processor businesses, focusing on the path of analog ICs. Below, we classify TI’s acquisitions into three stages based on its key business development:

First Stage: Breaking First, Establishing Later, Moving Towards the “Internet Era”

TI began to divest software, laptops, defense electronics, and memory businesses in 1996, shifting its business focus to analog and DSP businesses, and conducting a series of acquisitions around DSP, including Tartan related to DSP software, Power Trends related to DSP power management, and Burr Brown in the signal chain, thereby providing customers with complete solutions. The revenue share of analog business in the total semiconductor business increased from 45% in Q4 FY1997 to 65% in Q1 FY2001, and in 2002, DSP market share exceeded 40%.

Second Stage (2002-2006): Focus Shift to Mobile Processors

Starting in 2002, TI acquired a series of RF and communication companies related to OMAP mobile processors, such as wireless communication software company Condat AG and RF companies radia, chipcon, and ICD. Subsequently, TI launched the well-known OMAP processor in 2002 for the then 2.5G/3G feature phones.

Based on the success of DSP and the comprehensive solution of OMAP, TI achieved great success with the OMAP processor, capturing over 60% of the mobile processor market share at that time. Under this main line, TI also laid out related analog chips to provide customers with more complete solutions. By 2008, TI’s analog business revenue reached $4.857 billion, with a revenue share close to 40%, gradually growing stronger.

3. The Explosion of Mobile Internet

Rise — Explosive Growth of Smartphones (2009-2017): With the maturation of 3G mobile networks, the popularization of smart terminals, and the increasing number of content and applications based on the mobile internet, the smartphone market experienced rapid growth and widespread adoption. In 2010, smartphones began to replace feature phones, especially maintaining a shipment growth rate of over 60% in 2010-2011, with shipments exceeding 700 million units for the first time in 2012. According to Zhiyan Consulting, the smartphone penetration rate surged from less than 15% in Q1 2009 to around 70% in Q4 2014. In 2013, smartphone shipments first surpassed feature phones, reaching 1 billion units.

Fall — Innovation Vacuum Period, Downward Cycle (2017-2018): Smartphone sales began to decline, with the 4G dividend exhausted, and no new innovations emerging. The overall smartphone market advanced significantly, with the average quality of phones improving, leading to longer device lifespans; industry innovation was weak, and the attractiveness of new products was insufficient, causing users’ willingness to upgrade to decrease. Smartphone shipments peaked in 2016 and began to decline thereafter.

#Focusing on TI:Failure in mobile processors, fully transitioning to analog.

With the arrival of 3G, smartphones needed baseband chips, while Texas Instruments’ processors only had GPUs and some DSP units, lacking a complete 3G and 4G baseband chip, thus losing to competitors like Qualcomm and Samsung. According to Strategy Analytics’ report on the global smartphone chip market in the first half of 2012, Qualcomm held 48% of the revenue market share, ranking first; TI’s ranking dropped from the top three to fifth place; Samsung, MediaTek, and Broadcom ranked second, third, and fourth, respectively. Against the backdrop of declining revenue and market share, TI finally announced a significant reduction in wireless business costs in November 2012, reallocating more resources to the automotive and industrial markets. From then on, TI fully transitioned to analog.

In fact, TI began reserving resources for the analog business through acquisitions as early as 2007, completing one of its most significant acquisitions in 2011: National Semiconductor, which expanded TI’s product numbers from 30,000 to 42,000, allowing it to achieve a market share of 15.4% in 2011, maintaining the top position with a share of 16.7% in 2012. Since then, TI’s analog IC business revenue has dominated globally, indicating that the development of the analog chip business has become TI’s strategic goal.

4. Disruptions from the Pandemic Triggering Supply-Demand Conflicts

Rise — Upward Cycle of Consumer Electronics + Chip Shortages (2019-2021): Since 2018, consumer electronics such as TWS and smartwatches have rapidly penetrated the market, leading to an upward cycle. Coupled with the emergence of the COVID-19 pandemic as a “black swan,” which led to a global trend of remote work and online education to reduce contact with pathogens, the demand for consumer electronics surged. On the supply side, the pandemic caused disruptions in production, affecting supply chain delivery times, while the booming consumer electronics market squeezed production capacity from other downstream markets, leading to severe chip shortages in markets such as automotive electronics, resulting in rising analog chip prices and an overall upward movement in the industry.

Fall — Demand Slows, Inventory Rises (2021-2023): As demand for consumer electronics such as PCs, smartphones, and tablets sharply declined, terminal sales plummeted. Coupled with severe inventory buildup from previous stocking strategies, downstream manufacturers significantly reduced purchases of upstream raw materials. The semiconductor market entered a significant adjustment cycle, starting a downward cycle for this round.

#Focusing on TI: Revenue and Business Stabilization, Emphasizing Cost Control

As the acquisitions accumulated during the previous cycle gradually took effect, TI achieved significant success in the analog field. From 2019 to 2022, the revenue share from the automotive and industrial sectors stabilized above 55%. Therefore, in this round of cycle, as revenue and business gradually stabilize, TI focused on cost control: on one hand, TI announced in October 2019 to reduce agents, and starting in 2021, it reduced its original four agents down to just one, shifting to a predominantly direct sales model. On the other hand, TI initiated a new round of 12-inch line expansion starting in 2019 to reduce chip production costs and ensure product supply capabilities under the direct sales model.

Additionally, during the downturn of the industry cycle, TI also chose to reduce capacity utilization under financial report pressure to reduce inventory and maintain gross margin, planning to close the last two 6-inch plants by 2023 and 2025, while starting to join price wars to retain more market share amid fierce industry competition. However, the final outcome showed that TI did not achieve significant success—expanding capacity to gain market share and reducing capacity utilization to protect gross margin inherently conflict, and execution presents certain pressures and difficulties. Ultimately, TI’s share and gross margin both declined. According to KHAVEEN Investment data, TI’s market share fell from 19.0% in 2021 to 16.1% in 2023. Gross margin also dropped from 70.2% in Q1 2022 to 57.2% in Q1 2024.

1.2. M&A Dimension: Divestiture and Acquisition, Focusing on Development is the Main Theme

Since the 1990s, TI has completed nearly 30 acquisitions, all closely related to its strategic goals. Reviewing TI’s acquisition path, it has acquired software companies to synergize with its DSP business, acquired RF frontend companies to synergize with its OMAP processors, and acquired analog chip companies to synergize with its DSP business. Ultimately, TI has divested software, storage, and mobile processor businesses, focusing on the path of analog ICs. Below, we classify TI’s acquisitions into three stages based on its key business development:

First Stage: Breaking First, Establishing Later, Moving Towards the “Internet Era”

TI began to divest software, laptops, defense electronics, and memory businesses in 1996, shifting its business focus to analog and DSP businesses, and conducting a series of acquisitions around DSP, including Tartan related to DSP software, Power Trends related to DSP power management, and Burr Brown in the signal chain, thereby providing customers with complete solutions. The revenue share of analog business in the total semiconductor business increased from 45% in Q4 FY1997 to 65% in Q1 FY2001, and in 2002, DSP market share exceeded 40%.

Second Stage (2002-2006): Focus Shift to Mobile Processors

Starting in 2002, TI acquired a series of RF and communication companies related to OMAP mobile processors, such as wireless communication software company Condat AG and RF companies radia, chipcon, and ICD. Subsequently, TI launched the well-known OMAP processor in 2002 for the then 2.5G/3G feature phones.

Based on the success of DSP and the comprehensive solution of OMAP, TI achieved great success with the OMAP processor, capturing over 60% of the mobile processor market share at that time. Under this main line, TI also laid out related analog chips to provide customers with more complete solutions. By 2008, TI’s analog business revenue reached $4.857 billion, with a revenue share close to 40%, gradually growing stronger.

3. The Explosion of Mobile Internet

Rise — Explosive Growth of Smartphones (2009-2017): With the maturation of 3G mobile networks, the popularization of smart terminals, and the increasing number of content and applications based on the mobile internet, the smartphone market experienced rapid growth and widespread adoption. In 2010, smartphones began to replace feature phones, especially maintaining a shipment growth rate of over 60% in 2010-2011, with shipments exceeding 700 million units for the first time in 2012. According to Zhiyan Consulting, the smartphone penetration rate surged from less than 15% in Q1 2009 to around 70% in Q4 2014. In 2013, smartphone shipments first surpassed feature phones, reaching 1 billion units.

Fall — Innovation Vacuum Period, Downward Cycle (2017-2018): Smartphone sales began to decline, with the 4G dividend exhausted, and no new innovations emerging. The overall smartphone market advanced significantly, with the average quality of phones improving, leading to longer device lifespans; industry innovation was weak, and the attractiveness of new products was insufficient, causing users’ willingness to upgrade to decrease. Smartphone shipments peaked in 2016 and began to decline thereafter.

#Focusing on TI:Failure in mobile processors, fully transitioning to analog.

With the arrival of 3G, smartphones needed baseband chips, while Texas Instruments’ processors only had GPUs and some DSP units, lacking a complete 3G and 4G baseband chip, thus losing to competitors like Qualcomm and Samsung. According to Strategy Analytics’ report on the global smartphone chip market in the first half of 2012, Qualcomm held 48% of the revenue market share, ranking first; TI’s ranking dropped from the top three to fifth place; Samsung, MediaTek, and Broadcom ranked second, third, and fourth, respectively. Against the backdrop of declining revenue and market share, TI finally announced a significant reduction in wireless business costs in November 2012, reallocating more resources to the automotive and industrial markets. From then on, TI fully transitioned to analog.

In fact, TI began reserving resources for the analog business through acquisitions as early as 2007, completing one of its most significant acquisitions in 2011: National Semiconductor, which expanded TI’s product numbers from 30,000 to 42,000, allowing it to achieve a market share of 15.4% in 2011, maintaining the top position with a share of 16.7% in 2012. Since then, TI’s analog IC business revenue has dominated globally, indicating that the development of the analog chip business has become TI’s strategic goal.

Investment Recommendations

Domestic analog IC design manufacturers breaking through the “deep water zone” mainly rely on “R&D innovation” and “M&A expansion”. Through mergers and acquisitions and R&D innovation, domestic chip manufacturers can broaden their product categories, facilitate supply chain management for customers, enhance competitive advantages, improve product R&D efficiency and strength, while also strengthening cost control and product supply capabilities, and engaging in differentiated competition, such as penetrating high-end markets like industrial control and automotive, thereby effectively avoiding internal competition and achieving a positive feedback loop to “break the deadlock.”

We believe that in the analog industry, we should focus on two types of companies:

First type: Companies with strong financial strength and robust product portfolios: On one hand, during the industry downturn, these companies are cash-rich and can support themselves through the prolonged “bottoming out” phase. On the other hand, sufficient funds can support the acquisition of strong or synergistic companies, enhancing competitive strength and expanding market share, providing a higher performance elasticity when the industry rebounds.

Second type: Companies with strong R&D capabilities and forward-looking layouts in key areas: These companies possess strong R&D capabilities, sufficient patents, and technological barriers, allowing them to develop innovative and competitive products that meet diverse market demands, and lead the introduction of mid-to-high-end products in key areas, gaining a first-mover advantage.

5

Risk Warning

Downstream demand recovery may fall short of expectations: As analog chips are indispensable components in electronic systems, their market demand is closely tied to the prosperity of multiple downstream industries. If downstream demand recovery falls short of expectations, it could significantly impact the analog chip industry. For instance, the consumer electronics market has started to recover due to downstream manufacturers stocking up, but if downstream demand does not respond as expected, consumer electronics manufacturers may face inventory buildup risks, thus reducing orders to upstream analog chip manufacturers or module manufacturers. Additionally, although inventory in the automotive and industrial markets is nearing resolution, if demand continues to fall short of expectations, the market may face a “U-shaped” recovery, delaying the timing of recovery for upstream analog chips.

Changes in international leaders’ operational strategies: The pricing and production strategies of international analog chip giants will have a profound impact on the market, potentially triggering price wars and affecting inventory levels. For instance, in May 2023, Texas Instruments launched a price war in the Chinese market, intensifying competition in analog chips. If analog chip giants continue to adopt aggressive pricing strategies, it will impact the operational performance of domestic analog chip companies. Furthermore, the ongoing expansion of 12-inch production lines by some analog chip giants may place domestic analog chip companies at a competitive disadvantage.

Changes in trade policies: Changes in policies, trade restrictions, and technology export controls may impact the stability of the chip industry’s supply chain and market access. For example, supply chain disruptions caused by U.S.-China trade tensions and export restrictions on specific companies will pose challenges to the chip industry’s supply chain and market access. Moreover, technological restrictions may hinder R&D collaborations, affecting technological innovation and product upgrades, thereby impacting companies’ competitiveness and market share.

Team Introduction