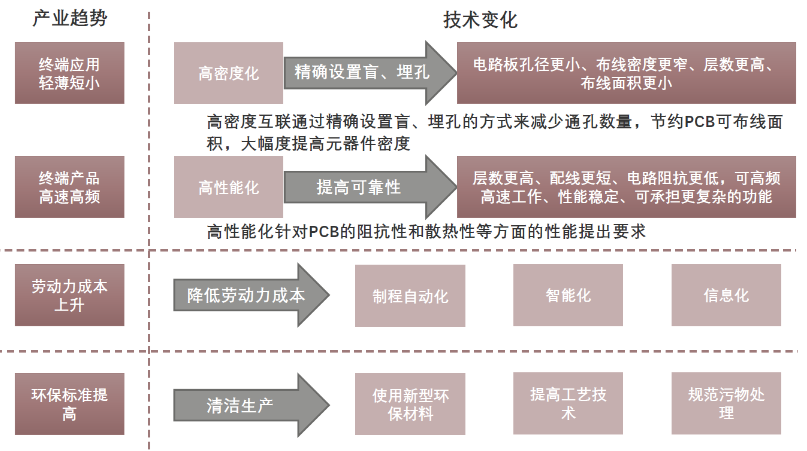

From Phones to Refrigerators: Understanding the PCB Industry

Click the above“Mechanical and Electronic Engineering Technology” to follow usPCB, or Printed Circuit Board, is the “heart” of electronic products, and nearly all electronic devices rely on it. The phone in your hand, your computer, and even the television and refrigerator at home all hide the presence of PCBs. In 2024, the PCB industry is experiencing a “spring breeze”, with overall profits soaring, a rare sight among many industries. Why is that? It turns out that the tide of the artificial intelligence era has brought a massive downstream demand to the PCB industry, especially for high-end PCBs, which have become a hot commodity in the market.

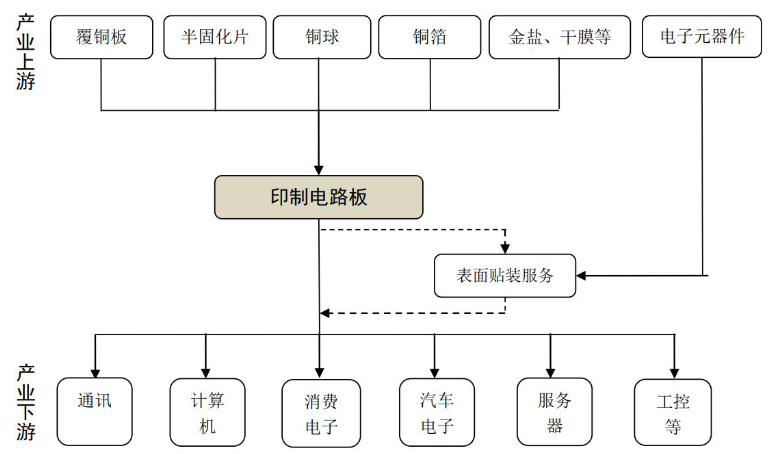

Speaking of PCBs, they are not simple; there are many types. Based on the flexibility of the substrate material, there are rigid boards, flexible boards, and rigid-flex boards. In rigid boards, the number of copper foil layers categorizes them into single/double-layer boards and multi-layer boards. Among multi-layer boards, differences in technology and processes transform them into HDI boards and special boards. Within special boards, there are various types including carrier boards, packaging substrates, backplanes, thick copper boards, high-frequency boards, and high-speed boards. When the density of PCBs exceeds eight layers, HDI manufacturing is used, which is cheaper than traditional complex lamination processes, marking a significant technological breakthrough.Next, let’s look at the upstream of PCB; copper foil is the “main character” in manufacturing copper-clad laminates, accounting for 30% (thick boards) and 50% (thin boards) of the cost. The top ten global copper foil producers account for 73% of the output, giving them significant bargaining power, which allows them to smoothly transfer copper price increases downstream. When copper foil prices change, the prices of copper-clad laminates follow, triggering a chain reaction in printed circuit board prices. Nord Technologies is a representative company in this field.

Copper-clad laminates are made from raw materials such as copper foil, epoxy resin, and fiberglass, and are the core substrate for PCB manufacturing. In the operating costs of PCBs, the raw material costs account for as much as 60-70%. Copper-clad laminates account for 20%-40% of the total PCB production cost, making them the highest proportion of material costs in PCBs. The leading company in domestic copper-clad laminates is Shengyi Technology, with a market share of 12%. Major companies in the industry have strong bargaining power, but the CR10 of the PCB industry downstream of copper-clad laminates is only 26%, indicating a perfectly competitive industry.

PCB manufacturers use copper-clad laminates as substrates for the production, design, manufacturing, and sales of printed circuit boards. To meet the procurement needs of leading brand customers downstream, PCB manufacturers often need to purchase electronic components to assemble and sell with PCB products. Speaking of leading PCB manufacturers, names like Shenzhen South Circuit, Huadian Technology, Pengding Holdings, Shenghong Technology, and Dongshan Precision are all well-known.

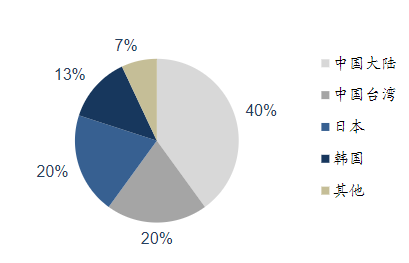

In the downstream application fields, the top three global PCB markets in 2023 are in the communications sector, computer industry, and consumer electronics sector. Although the server sector only accounts for 10% and ranks fourth, it has a market size of $8.5 billion, expected to reach $15 billion by 2028, with a compound growth rate of 12.5%, making it the fastest-growing downstream sector, far exceeding the industry average of 5.2%.From the segmented structure of PCB products, ordinary multi-layer boards are mainstream, with multi-layer boards accounting for 39% of the global PCB market in 2023, followed by packaging substrates at 18%; flexible boards and HDI boards account for 18% and 15%, respectively. In the future, the compound growth rate for global 8-16 layer boards and ultra-high layer boards (over 18 layers) will reach 5.5% and 5%, respectively. Downstream demand is gradually shifting towards high-end products, while the overall share of single/double-sided boards and low-end multi-layer boards is slowly declining.In terms of market size, the total output value of China’s PCB industry reached $50 billion in 2023. Among the top 100 PCB manufacturing companies globally in 2022, a total of 65 Chinese companies made the list, accounting for over 60% of the total. Among them, the number of companies from mainland China accounted for nearly 42%, while those from Taiwan accounted for over 21%. Compared with countries like Japan and South Korea, the proportion of high-end printed circuit boards in China’s PCB products is relatively low. In 2022, multi-layer boards, single and double-sided boards, and HDI boards accounted for over 78%, while flexible boards accounted for 16%, indicating significant room for improvement in higher technical content products.

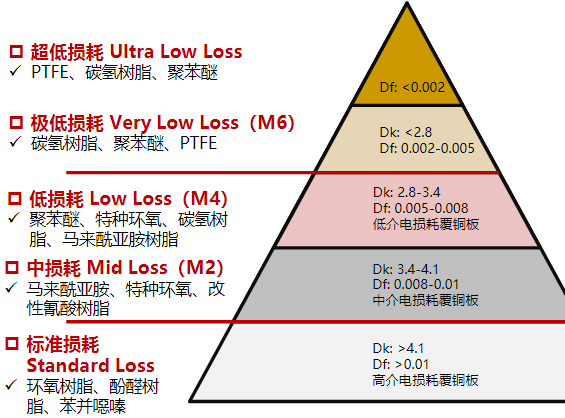

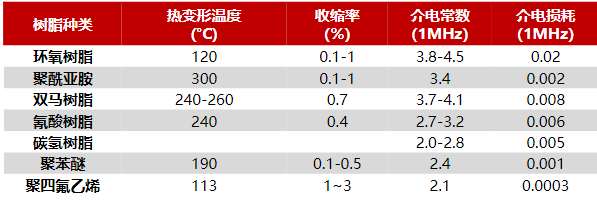

In the future, the increase in the number of PCB layers and the upgrading of materials is an inevitable trend. The supply of upstream copper-clad laminates is crucial, directly affecting the upgrading and costs of PCB products. Copper-clad laminates are the most significant part of the PCB cost structure, and as the number of PCB layers continues to increase, the amount of copper-clad laminate materials will also grow. At the same time, the requirements for thickness and transmission rates have raised higher demands for the material performance of copper-clad laminates, necessitating continuous reductions in Df and Dk values. The supply of copper-clad laminates will significantly impact the production and costs of PCBs.

The increase in server information transmission rates requires specific higher-layer boards and lower-loss materials for PCBs, which raises higher demands for manufacturers’ process levels. Currently, domestic PCB manufacturers have a high level of technology for high-layer boards, with leading PCB manufacturers like Huadian Technology, Shenzhen South Circuit, and Shengyi Electronics already achieving mass production of high-layer board products in the server field.