In the first half of 2025, the global semiconductor industry continues to recover, driven by strong demand from emerging applications such as AI, automotive electronics, and others. Against this backdrop, the power management integrated circuit (PMIC) market shows significant structural differentiation: traditional consumer applications are experiencing weak demand, while high-performance and high-reliability PMIC for automotive electronics, data centers, industrial control, and AI terminals are in high demand, becoming the core driving force for the growth of local enterprises.

This article is based on the financial reports and key dynamics of 15 local listed PMIC companies for the first half of 2025, combined with industry trends, to analyze the current market landscape and corporate performance. Due to the diverse product lines of most companies, this article does not rank them and does not include non-listed or undisclosed financial companies (as of September 18).

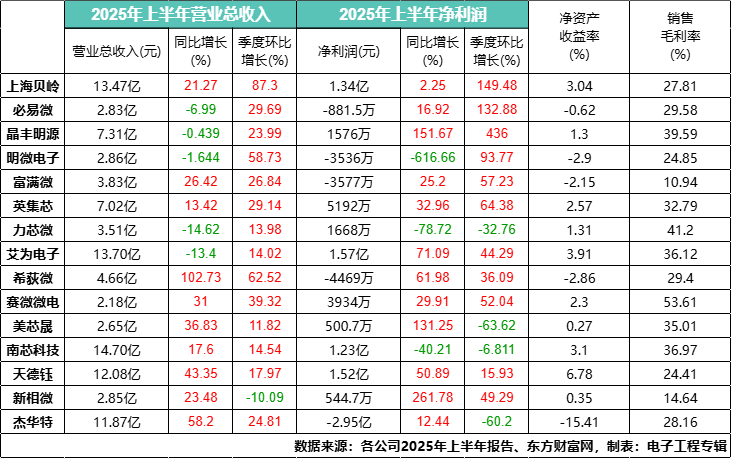

Profit and Loss Ranking

From a financial performance perspective, the differentiation among companies has intensified, with some companies achieving a leap in profit quality through high-end transformation.

In terms of return on equity (ROE), Tiande Yu (6.78%) performed the best, demonstrating strong asset operation efficiency and profitability; Aiwei Electronics (3.91%) and Nanjing Semiconductor (3.1%) followed closely. Companies with negative ROE include Jiehuate (-15.41%), Mingwei Electronics (-2.9%), Xidiwei (-2.86%), Fumanwei (-2.15%), and Biyiwai (-0.62%), which are mostly experiencing short-term losses due to strategic transformation investments or pressure on traditional businesses.

Gross profit margin is a key indicator of a company’s product competitiveness and cost control ability. Among the top three in gross profit margin, Saiwei Microelectronics (53.61%) focuses on high-precision battery management chips, with high technical barriers and strong product reliability; Lixin Micro (41.2%) has been deeply involved in fast charging and power management unit (PMU) fields for many years, with high integration and strong customer stickiness; Jingfeng Mingyuan (39.59%) has successfully optimized its product structure by exiting low-margin markets and expanding into new applications such as motor drives. Most other companies have gross margins concentrated in the 20% to 30% range.

In terms of total operating revenue, Nanjing Semiconductor (1.47 billion yuan) ranks first, followed by Aiwei Electronics (1.37 billion yuan) and Shanghai Beiling (1.347 billion yuan) in second and third place. Saiwei Microelectronics (218 million yuan) has the lowest revenue.

In terms of year-on-year revenue growth, Xidiwei (102.73%) achieved a doubling growth, leading the industry and demonstrating strong market expansion capabilities; Jiehuate (58.2%) and Tiande Yu (43.35%) also showed significant growth, with good business development trends. Lixin Micro (-14.62%), Aiwei Electronics (-13.4%), Biyiwai (-6.99%), Mingwei Electronics (-1.644%), and Jingfeng Mingyuan (-0.439%) experienced negative growth, mainly due to pressure from traditional businesses and facing certain market challenges.

In terms of quarter-on-quarter revenue, driven by the 618 shopping festival and the recovery of downstream demand, most companies achieved growth. Shanghai Beiling (87.3%), Xidiwei (62.52%), and Mingwei Electronics (58.73%) showed impressive quarter-on-quarter growth rates, reflecting the companies’ short-term market responsiveness and business growth vitality.

Regarding net profit, Aiwei Electronics (157 million yuan) had the highest profit, occupying a strong position in the market; Tiande Yu (152 million yuan) and Shanghai Beiling (134 million yuan) also had good profit scales. Companies in a loss state include Jiehuate (-29.5 million), Xidiwei (-4.469 million), Fumanwei (-3.577 million), Mingwei Electronics (-3.536 million), and Biyiwai (-0.8815 million), which need to further optimize their business structure or enhance market competitiveness to achieve profitability.

In terms of year-on-year net profit growth, Xinxiangwei (261.78%) achieved significant growth, with notable improvements in business profitability; Jingfeng Mingyuan (151.67%) rebounded significantly, with improved operating conditions; Meixinsheng (131.25%) significantly enhanced profitability. Xidiwei (61.98%) is still in a loss state, but the loss amount has significantly narrowed year-on-year, showing a clear improvement trend. Nanjing Semiconductor (-40.21%) and Lixin Micro (-78.72%) have also seen declines, requiring attention to changes in their profitability.

In terms of quarter-on-quarter net profit growth, Jingfeng Mingyuan (436%), Shanghai Beiling (149.48%), and Biyiwai (132.88%) showed strong growth, indicating strong short-term profit enhancement capabilities. Meixinsheng (-63.62%), Jiehuate (-60.2%), and Lixin Micro (-32.76%) experienced declines in net profit, necessitating analysis of the reasons and taking corresponding measures to improve profitability.

Reasons for Decline / Loss

Fumanwei In the first half of 2025, revenue increased by26.42%, but net profit was a loss of35.7675 million yuan. The company has a wide range of core product lines, but faces fierce competition in the traditional consumer electronics market. Despite outstanding performance in the PMIC field and achieving cost reduction and efficiency improvement, overall profitability is still affected by low-margin product lines and strategic transformation investments.

Mingwei Electronics experienced a year-on-year revenue decline of1.64%, with a net profit loss of3.536 million yuan, a significant year-on-year decline of616.7%. The main reason is intensified competition in the traditional product field, leading to declines in both revenue and gross margin, coupled with increased asset impairment losses. Although sales of new products in smart landscape and Mini backlighting have risen, the new business has not yet fully compensated for the decline in traditional business.

Lixin Micro experienced a year-on-year revenue decline of6.99%, with a net profit loss of881.5 thousand yuan, a year-on-year decline of78.72%. This is mainly due to the saturation of traditional consumer electronics markets such as mobile peripherals and intense price competition. The company has increased R&D investment against the trend, with a year-on-year increase of51.31%, accounting for as much as26.67% of revenue, aiming to accelerate expansion into high-value markets such as automotive-grade and industrial electronics, putting short-term profits under pressure.

Nanjing Semiconductor experienced a year-on-year revenue growth of17.60%, but net profit decreased significantly year-on-year by40.21%. This “increased revenue without increased profit” phenomenon is mainly due to the company’s significant increase in R&D investment (up by54.62%) and sales expenses to seize market share and expand product lines, leading to short-term profit pressure.

Jiehuate had a return on equity of-15.41%, the lowest among all companies. Although the company achieved a year-on-year revenue growth of58.20%, showing strong growth momentum, high R&D and sales expenses have put pressure on net profit, and profitability has not yet been fully released.

Biyiwai experienced a year-on-year revenue decline of6.99%, with a net profit of-881.5 thousand yuan, and ROE of-0.62%. Although the company continues to layout in new energy fields such as photovoltaics and energy storage, launching high-efficiency DC-DC converters and BMS monitoring chips suitable for household energy storage systems, the recovery of demand in the traditional consumer electronics market has not met expectations, leading to overall performance pressure. At the same time, the company has made significant upfront investments to expand into the automotive-grade power chip market, further impacting short-term profitability.

Reasons for Increase / Profit

Xinxiangwei achieved a year-on-year net profit growth of261.78%, realizing significant growth and notable improvements in business profitability. As a professional manufacturer in the display driver chip field, its PMU and display driver chip (DDIC) integration solutions have gained wide recognition in the high-end smartphone and tablet markets. In the first half of 2025, benefiting from the end of inventory reduction by downstream panel manufacturers, the recovery of stocking demand, and the company’s increased market share in AMOLED driver chips, the shipment volume of its supporting power management chips has significantly increased, coupled with an increase in the proportion of high-margin products, achieving a strong rebound in profitability.

Tiande Yu achieved a return on equity of6.78%, ranking first among all companies, while revenue increased year-on-year by43.35%, with continuous improvement in profitability. The company focuses on power management chips for mobile smart terminals, the Internet of Things, and consumer electronics, benefiting from the recovery of downstream demand and product structure optimization, showing outstanding performance. The company actively expands into emerging applications such as smart home and wearable devices, continuously enriching its product line.

Aiwei Electronics achieved a return on equity of3.91%, ranking second among all companies. The company’s revenue in the first half of the year decreased year-on-year by13.40% to 1.369 billion yuan, but benefited from product structure optimization and an increase in the proportion of high-margin products, the company’s profitability has significantly improved: gross margin increased year-on-year by8.03 percentage points to 36.12%, and net profit attributable to the parent company increased year-on-year by71.09% to 157 million yuan, with a non-recurring net profit growth rate reaching81.88%. This indicates that the company has successfully countered the revenue pressure brought by the mismatch in downstream demand by enhancing product added value and operational efficiency.

Shanghai Beiling achieved a return on equity of3.04%, showing stable performance. The company has optimized its product structure, increasing the proportion of high-value-added products, and has made breakthroughs in sub-markets such as industrial control and communication, achieving a year-on-year revenue growth of18.80%, with net profit increasing year-on-year by10.21%. The company continues to strengthen cooperation with key domestic customers, consolidating its market position in power management and signal chain fields.

Jingfeng Mingyuan achieved a return on equity of1.3%, performing reasonably among profitable companies. The company’s revenue in the first half of the year slightly decreased year-on-year by0.439%, but net profit attributable to the parent company reached15.76 million yuan, a year-on-year increase of151.67%. This “revenue decrease with profit increase” is due to the company’s proactive optimization of its product structure: revenue from traditional LED lighting driver chips has declined, but gross margin has improved; at the same time, high-margin motor control driver chips (revenue up by24.30%) and high-performance computing power chips (revenue up by419.81%) have rapidly increased, driving the overall gross margin up to39.59%.

Saiwei Microelectronics achieved a year-on-year revenue growth of31.00%, with net profit attributable to the parent company increasing year-on-year by29.91%. The steady growth in performance is attributed to the recovery of downstream consumer electronics demand, the continuous launch of high-performance, differentiated products, and the seizing of domestic substitution opportunities, increasing market share in high-end applications.

Yingjixin achieved revenue of702 million yuan in the first half of the year, a year-on-year increase of13.42%; net profit attributable to the parent company was51.92 million, a year-on-year increase of32.96%, with a non-recurring net profit growth rate also reaching22.04%, significantly enhancing profitability. The high growth in performance is due to the optimization of the company’s product structure and breakthroughs in multiple fields: on the one hand, new products such as PMU, automotive-grade USB Hub, and highly integrated battery management chips have achieved bulk shipments in fields such as computing chips, automotive electronics, and electric tools; on the other hand, the integrated solution for AC-DC+ fast charging protocol has been recognized by major mobile manufacturers, and the photovoltaic new energy product line covers micro-light collection to high-power MPPT, continuously broadening application scenarios.

Xidiwei achieved a year-on-year revenue growth of102.73%, with a significant narrowing of net losses. The improvement in performance is attributed to the demand from emerging applications such as AI smartphones, smart glasses, and automotive electronics, as well as product structure optimization. The company focuses on high-end fields such as DC/DC and charge pump fast charging, with multiple products entering the supply chains of Qualcomm and brands like Samsung and Xiaomi, and achieving mass production delivery of automotive-grade chips, increasing the proportion of high-end products and driving the recovery of profitability.

Meixinsheng achieved a year-on-year net profit growth of12.33%, with gross margin increasing to35.01%. The company continues to increase R&D investment in fields such as wireless charging and automotive-grade power management, enhancing product competitiveness and successfully expanding high-end customers. The company has also made breakthroughs in power management chips in fields such as optical communication and photovoltaics, laying a foundation for future growth.

Conclusion

In the first half of 2025, the Chinese PMIC market is showing a structural trend of “ice and fire” driven by AI, automotive electrification, and industrial intelligence. The traditional market is under pressure, while the high-end market is booming. Local enterprises are accelerating their entry into high-value markets such as automotive, industrial, and high-performance computing through technological breakthroughs, product upgrades, and ecological cooperation. In the future, the PMIC industry will present a dual-track evolution of “high-end + scenario verticalization, with companies possessing core technological barriers and system-level solution capabilities taking the lead in the domestic substitution process, leading the industry towards high-quality development.

(Editor: Franklin)

THE END

Follow “Electronic Engineering Magazine” and add the editor’s WeChat

Regional groups are now open, please send messages 【Shenzhen】【Shanghai】【Beijing】【Chengdu】【Xi’an】 to the public account