Author | Danny @IOSG

Summary

The SIMD 0228 proposal, a significant decision that recently stirred all participants in the Solana ecosystem, ultimately did not pass. The voting participation rate reached a historic high for Solana (nearly 50% of the total token supply), but the proportion of supporting votes was insufficient to meet the supermajority threshold required for passage (66.67%).

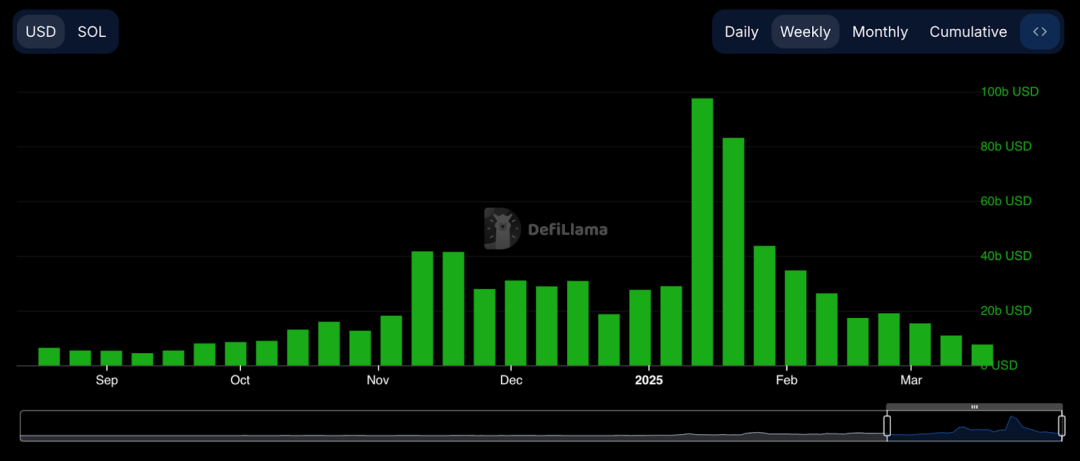

The background of such a proposal is that Solana, after the launch of the Trump token, has gradually returned to a calmer phase following the on-chain frenzy brought by Memecoins. The weekly trading volume has retreated from nearly $100 billion at the beginning of the year to less than $10 billion, a 90% decline, now lower than the trading volume during the initial rise of Memecoins.

Along with Memecoins, Solana became the most successful public chain of this cycle. As the Memecoin cycle gradually wanes, Solana also faces a transformation and the need to redefine its positioning. It was at this time that Solana’s largest capital supporter, Multicoin, proposed the 0228 proposal. The proposal sparked intense debate within the community. Twitter became the main battleground, with different stakeholders arguing their points until the last moment of voting.

During the debate over the proposal, we could see many echoes of previous changes pushed within the Ethereum community. The window for the proposal itself was short, presenting many long-term considerations and short-term solutions, along with many interests that were not easy to articulate. However, its transparency allowed us to see the current attitudes and strategies of many Solana leaders.

Despite the proposal being rejected, Tushar from Multicoin, the proposer, still referred to it as “a victory” due to the high participation rate in voting and the extensive community discussion, showcasing Solana’s decentralized governance capabilities.

What was behind the governance of this proposal in Solana? What does it mean, why did it not pass, and was the process just and successful? Let’s take a closer look.

SIMD 0228 — A Hasty Proposal

What is the 228 proposal?

The 228 proposal aims to dynamically adjust the inflation rate based on the staking rate, with the goal of maintaining a 50% staking rate and gradually reducing the issuance rate of SOL.

Solana’s current inflation model is a gradually declining curve over time. At the launch of the mainnet (March 2019), an inflation rate of 8% was set, which has since decreased, with the current inflation rate at approximately 4.8% and a long-term target inflation rate of 1.5%-2%.

If this proposal were to pass, short-term staking rewards would decrease (ranging from 1% to 4.5% based on the staking rate), while the long-term inflation rate would approach 1.5%.

Currently, the staking rate is 70%, so if 228 passes, short-term staking rewards for SOL would decrease, while long-term issuance would reduce, and staking yields would be adjusted in real-time based on the staking rate.

Unlike proposals like SIMD 0123, where validators could choose to opt-in, 0228 is mandatory, meaning that once initiated, it will affect the interests of all stakers.

Voices in Support

This proposal was put forward by Tushar and Vishal from Multicoin Capital, with support from Anza and former Consensys researcher Max. Their reasons include:

# Reducing unnecessary token issuance and lowering inflation costs

Solana’s current fixed inflation model is a form of “dumb emissions” because it does not take into account the actual economic activity or security needs of the network. Based on the inflation rate of 4.8% at the beginning of 2025, approximately $3.82 billion worth of new tokens would be issued annually (based on an $80 billion market cap). This high inflation essentially dilutes SOL holders, especially given the current staking rate of 65.7% — the network’s security is already well assured.

Passing this proposal would mean shifting the staking philosophy from “overpaying to ensure security” to “finding the minimum necessary payment”.

Interestingly, this point echoes some criticisms from certain KOLs within Solana against Ethereum’s economic security argument, which claims that excessive assets support an economy viewed as “meme” security.

# Releasing capital to promote DeFi ecosystem development

The current high staking rate (65.7%) leads to a large amount of SOL being locked, suppressing capital flow within the DeFi ecosystem. Kamino founder Marius pointed out, “Staking encourages hoarding but reduces financial activity.” This is similar to how high interest rates suppress investment in traditional finance.

It is worth noting that the main supporters of major DeFi protocols on Solana are also the VCs proposing the proposal, so releasing liquidity into DeFi is also a significant motivation.

# Reducing the “leaky bucket effect” and enhancing ecosystem autonomy

The leaky bucket effect refers to the significant wear and leakage of value within the ecosystem during economic activities. Since the newly issued SOL due to inflation is considered ordinary income and is taxable in the U.S., the amount generated by inflation will proportionally extract value from the entire ecosystem. For Solana, approximately $650 million in taxes and about $305 million in exchange fees have already leaked out of the ecosystem.

From a first principles perspective, it essentially indicates that Solana has entered a stable phase, and the initially arbitrary inflation model has become unreasonable. The chain’s development should aim to enhance economic activity and should correspondingly improve the inflation scheme.

Placeholder partner Chris summarized that true benefits should come from demand-side spillovers to the supply side, rather than relying on a fixed inflation setting that favors cold starts. In the long run, the supporters’ arguments do hold some merit. Once a public chain ecosystem has passed the cold start phase, it naturally requires a more idealized economic system to drive economic development.

Voices of Opposition

Led by Solana Foundation Chair Lily, a faction opposed the passage of this proposal. The main point of contention was whether to implement this proposal in such a short time frame, rather than allowing for a longer discussion given the significant changes in asset attributes that would affect different participants (engineers at the network layer, developers at the product layer, and institutions at the economic layer). Currently, most discussions are among core network personnel and product layer personnel, with fewer voices from the product layer and institution-led economic layer groups who are further from the information channels. Therefore, it should not be rushed through before the arguments are sufficiently developed.

Many opponents expressed concerns about the loss of small validators. Small nodes are inferior to large nodes in both scale effects and bargaining power, so a reduction in inflation would first eliminate these small nodes, harming Solana’s decentralization. However, after speaking with some Solana nodes, I found that most nodes still support passage, primarily due to Solana’s substantial subsidies and a general belief in the value of SOL as it continues to improve. There is a palpable sense of community cohesion within Solana, but that is a side note.

It is clear that both sides are dissatisfied with the current inflation model and agree that it needs improvement. The point of contention is whether to implement it hastily within two weeks.

Additionally, there may be some interest considerations at play. The simplest is that many SOL holders, especially those who can obtain higher returns from non-staking ecosystems (DeFi), naturally do not want inflation to remain at such a high level. The typical profile here is the VCs behind Solana and the projects they support.

Currently, an important adoption direction for Solana is towards institutions, including ETFs and more traditional institutional use cases. Therefore, those promoting institutional adoption will certainly oppose this. Whether the passage of SIMD would be beneficial for institutional adoption is debatable; supporters argue that traditional institutions are more averse to high-inflation assets, while opponents believe that traditional assets have greater uncertainty concerns regarding assets with dynamically changing inflation rates.

I believe that the uncertainty of the mechanism may hinder institutional adoption — institutions can assess the asset attributes under the mechanism, but if this mechanism keeps changing, it creates obstacles for their evaluations. Therefore, for institutions, it is either to pass quickly or to wait until initial adoption is completed and then negotiate together — at that point, the entanglement of interests may make it even harder to pass.

Why Now?

This raises the question of why such a hasty proposal was introduced and pushed forward?

Perhaps it is because Solana still retains a large trading volume in the wake of the meme, leading to current node fees and MEV income remaining high, thus adjustments to the staking mechanism would not encounter significant controversy. In 2024, Solana’s total MEV earnings reached $675 million, with a clear upward trend; in Q4, node MEV earnings even exceeded inflation rewards. For this reason, nodes are currently relatively insensitive to short-term inflation income. If the Solana chain were to cool down completely, the income losses caused by this proposal would undoubtedly provoke opposition from the staking community.

Solana’s Restaking is about to begin, with Renzo, Jito, and others already showing signs. Looking at Ethereum’s history, the emergence of liquid staking and Restaking will provide substantial subsidized returns for stakers and validators, allowing nodes to reduce concerns about inflation rewards.

The Ethereum Foundation also proposed a proposal to improve the inflation curve last year, similar to anchoring the staking rate to a fixed ratio to reduce excessive staking. The argument at that time was to release more liquidity while reducing the substitutive effect of Lido ETH and other LSTs on ETH, given that economic security was already more than sufficient.

This proposal sparked brief discussions after it was introduced. It was a time when OGs re-examined Ethereum’s economic mechanisms after the transition to PoS. The proposal itself, along with the discussion process, presented a wealth of computational reasoning support, but ultimately, due to unclear theoretical foundations, the proposal did not advance. Ethereum’s economic arguments may provide some reference for 228, but the opposition it faced also reflects the difficulties of passing such a “dilution” proposal.

The final result was not unexpected. Perhaps under the foundation’s leadership, validators formed a bearish view of the proposal, coupled with concerns about institutional adoption. Or perhaps this decision was indeed too hasty, leading to a lack of consensus among validators and resulting in voting discrepancies. Alternatively, small validators may have formed a consensus on short-term income pressure and collectively chose to oppose. The breadth of discussion does not necessarily imply depth; without depth, divisions can occur. The hasty push of the proposal also reflects the current lack of clarity regarding the chain’s positioning and the next steps after the memecoin supercycle.

The Governance Process as a Victory

This proposal, while hasty, sparked very transparent and open discussions in just a few weeks. Both sides spoke candidly on Twitter, with no moderates, directly stating their support or opposition and providing arguments. This discussion model allowed everyone to understand both sides’ considerations. At the most intense moments, a Space was even organized, where stakeholders expressed their views.

Another highlight was the acceptance of community voices. Many Solana projects/builders received responses to their candid suggestions on Twitter, which were included in the discussions in the Space. The proposal transformed from an obscure formula into the voice of each community, being brought forth for discussion. One criticism of the voting process was that stakers could not directly participate in the opinion vote, which also led to many large nodes’ self-contradictions — how to coordinate the opinions of all stakers and provide a final decision. This is a problem that all public chains need to solve, and Solana has illuminated this issue for the first time.

The proposal attracted 74% of the staking supply to participate, demonstrating a high level of community engagement. The clear voting mechanism and passage threshold of SIMD made the decision-making process more transparent and predictable. In contrast, Ethereum’s proposal decision-making process is relatively vague, relying mainly on discussions and consensus among core developers, lacking a formal voting mechanism.

Finally, there is the efficiency of the proposal. Even though we often criticize it for being too hasty, the proposal was introduced, voted on, and completed within less than two months, which is impressive for the efficiency of idea implementation from top to bottom in this ecosystem. This is likely why Tushar considers it a victory.

Conclusion

Overall, the SIMD 228 proposal reflects Solana’s transition into a phase of institutional adoption and continued development of on-chain consumer applications after the prosperous period of innovating asset issuance models, where conflicts in interest distribution have become the catalyst for the entire event.

Supporters need to leverage this prosperous phase of on-chain activity to push for reforms quickly, but the haste has led to intense discussions that were not sufficiently deep, with inadequate support and education for small validators, resulting in a lack of consensus among validators. The proposal’s lifecycle was very short, and this process also demonstrated Solana’s execution power and openness, serving as an excellent governance case for all ecosystems to learn from.

Due to adjustments in the public account push logic, old readers please star the Wu Shuo public account, otherwise you may not receive updates.

How to set a star for the public account:How to set a star for the public account

According to the notice issued by the central bank and other departments on “further preventing and handling risks of virtual currency trading speculation,” the content of this article is for information sharing only and does not promote or endorse any business or investment behavior. Readers are strictly required to comply with the laws and regulations of their respective regions and not to participate in any illegal financial activities. This article does not provide transaction entrances, guidance, or issuance channels for any virtual currency or digital collectibles. Unauthorized reproduction or copying of Wu Shuo content is prohibited, and violators will be held legally accountable.