Robots controllers are the core brain of robot control systems. The main task of the controller is to solve the robot’s forward and inverse kinematics, enabling the conversion between the robot’s operational space coordinates and joint space coordinates, completing the robot’s trajectory planning tasks, and achieving high-speed servo interpolation calculations and servo motion control. The robot controller consists of both hardware and software. The software part of the robot controller is the “heart” of the industrial robot, and with the development of technology, there have been varying degrees of research achievements in the application software from lower machines to upper machines.

Robots controllers are the core brain of robot control systems. The main task of the controller is to solve the robot’s forward and inverse kinematics, enabling the conversion between the robot’s operational space coordinates and joint space coordinates, completing the robot’s trajectory planning tasks, and achieving high-speed servo interpolation calculations and servo motion control. The robot controller consists of both hardware and software. The software part of the robot controller is the “heart” of the industrial robot, and with the development of technology, there have been varying degrees of research achievements in the application software from lower machines to upper machines.

The market share of controllers is basically consistent with that of robots, and domestic companies have not yet formed a significant market share in controllers. Like robots, controllers and software are generally designed and developed independently by robot manufacturers. Currently, the mainstream controllers from foreign robot manufacturers are independently developed based on general multi-axis motion control platforms, and each brand of robot has its own control system to match it. Therefore, the market share of controllers is basically consistent with that of robots, and domestic companies have not yet formed a competitive advantage in the controller market.

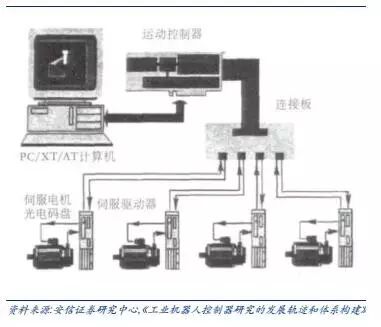

Robot controller hardware part

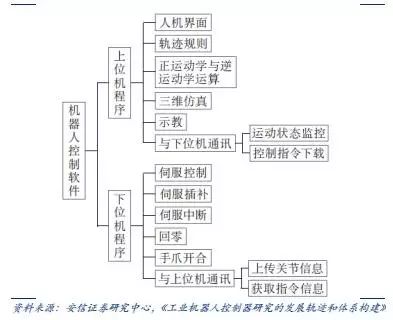

Robot controller software structure

Domestic robot controller products have matured and are key components with the smallest gap compared to foreign products. The gap between domestic controllers and foreign products mainly lies in control algorithms and the usability of secondary development platforms. The development of control systems involves many core technologies, including hardware design, underlying software technology, and upper-level functional application software. With the accumulation of technology and application experience, the hardware platforms used by domestic robot controllers are not significantly different from foreign products. The gap mainly lies in control algorithms and the usability of secondary development platforms.

In the coming years, China’s domestic robots will experience rapid development, and the application market for domestic robot controllers faces good development opportunities, especially for companies that have been deeply involved in motion control for many years. The more axes a robot has, the higher the performance requirements for the controller: the degree of freedom of a robot depends on the number of movable joints it has. The more joints there are, the higher the degree of freedom and the higher the displacement accuracy. Consequently, the number of servo motors used is relatively large, meaning that the more precise the industrial robot, the more servo motors it requires.

Generally, a multi-axis robot is controlled by a single control system, which also means that the performance requirements for the controller are higher. With the rapid development of industrial robots in China, companies with strong R&D capabilities will have a stronger competitive advantage.

Main controller manufacturers and representative products

The body: Connecting the upstream and downstream industrial chains, what is the value of the robot body? The robot body falls under the category of equipment integration. According to mechanical structure, robot bodies can be divided into Cartesian robots, SCARA robots, articulated robots, parallel robots, and others. Different types or industries of robots have different emphasis on technical indicators. For example, welding robots in the automotive industry have high precision and speed requirements for articulated robots, while palletizing and handling robots have higher load capacity requirements. SCARA robots, often used in the electronics industry, require high precision and speed. The global industrial robot market is mainly composed of articulated global industrial robots.

Robot body structure classification diagram

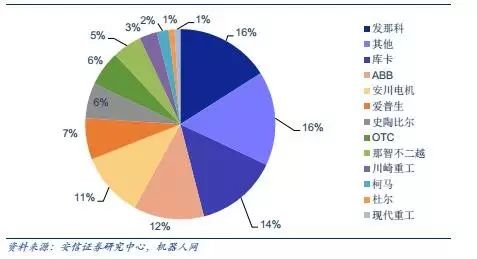

Robot body manufacturers can effectively integrate upstream component manufacturers and downstream system integrators. Robot body manufacturers are responsible for the production, processing, assembly, and sales of components such as industrial robot pillars, arms, bases, and precision reducers. Applications and integrations can be implemented by the body companies themselves or completed by integrators. Body companies have the capability to effectively integrate upstream components and downstream system integrators. International industrial robot body manufacturers include KUKA, ABB, Fanuc, Yaskawa Electric, etc. Domestic companies include Siasun Robot, Guangzhou CNC, ROKI, Estun, Efort, Jasic Technology, and Yaskawa. Most domestic robot body companies focus on procurement integration.

The core technologies of the four major families of industrial robots upstream of the body

In 2014, the market size of China’s industrial robot body was 8.4 billion, and it is expected to reach 30 billion by 2018, indicating a growth potential of 2.7 times. According to the latest data from the World Robotics Association and the “Made in China 2025” industrial robot technology roadmap, China’s robot market is expected to grow at a compound annual growth rate of about 30% over the next 4 years. If calculated at 200,000 yuan per unit, the market size of China’s robot body in 2018 is expected to be 30 billion, which is 2.67 times that of 2014.

The economical body is the development direction for domestic robot bodies. The foreign robot industry has grown alongside the automotive industry, which has very high precision, efficiency, and stability demands. In the automotive sector, domestic robot companies cannot compete with foreign companies in the short term. The development of economical robots applicable to general manufacturing outside the automotive industry is the current development direction for domestic robot bodies. Economical bodies include low-cost six-axis general-purpose robots and dedicated three- and four-axis robots. Economical bodies are divided into two categories: 1) General-purpose six-axis articulated robots that can be mass-produced at lower costs with domestic core components; 2) Dedicated robots for specific fields, such as SCARA robots and desktop robots used in the electronics industry, which belong to the dedicated machines within economical bodies. In industries such as electronics, home appliance manufacturing, metal manufacturing, plastic chemicals, and food, foreign robotic companies do not have significant advantages in industry experience and customer base, and customers pay more attention to the cost-performance ratio of robotic products. This presents an opportunity for domestic robots to catch up.

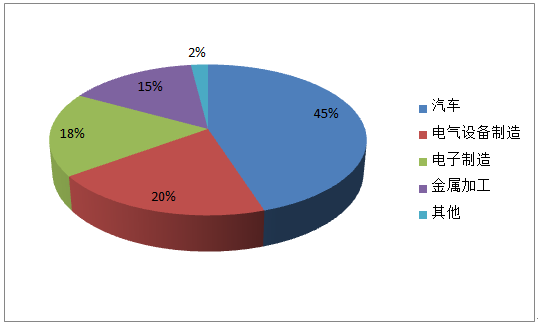

In 2015, the distribution of robot installations by industry in China

In 2015, the distribution of robot installations by industry in China

Long-term prospects are optimistic for companies that can develop robots suitable for the Chinese market and possess the five essential elements for success. The five core technologies known as the “five essential elements of robot bodies” include “servo systems,” “controllers,” “core algorithms,” “precision reducers,” and “application and integration technologies.” For domestic robot bodies to develop well, they should at least excel in two of these five areas.

First, they need to thoroughly understand servo systems and controllers, and then achieve good results in core algorithms. High-precision mechanical transmission (i.e., reducers) can be purchased externally. Applications and integrations can be implemented by the body companies themselves or completed by integrators. (Source: Anxin Securities)