Follow our official account, click the top right corner of the homepage to set a star mark, and stay updated on the latest news in the power semiconductor ecosystem.

Source: Components and Software Domestic Substitution

Introduction: Compared to logic chips, the technical difficulty of power semiconductors catching up to international standards is relatively lower, and the domestic supporting industrial chain is more complete, making it one of the fastest-growing segments for domestic substitution.

As an important subfield of the semiconductor industry, power semiconductors are the core of energy conversion and circuit control in electronic devices.

The application fields of power semiconductors have expanded from industrial control and consumer electronics to many subfields such as renewable energy, rail transportation, smart grids, and variable frequency appliances, with a robust growth trend in market size.

As the world’s largest market for power semiconductors, China accounts for as much as 35% of global demand. Driven by the demand in electric vehicles and industrial sectors, the domestic market is expected to continue maintaining rapid growth.

According to Guoyuan Securities, by 2025, the domestic power semiconductor market is expected to provide a pure incremental scale of 20 billion yuan.

In terms of domestic substitution, the technical difficulty of catching up in power semiconductors is relatively low, and the domestic supporting industrial chain is also more complete.

Considering various factors such as market demand and technical difficulty, power semiconductors are expected to become one of the fastest-growing segments for domestic substitution in the foreseeable future.

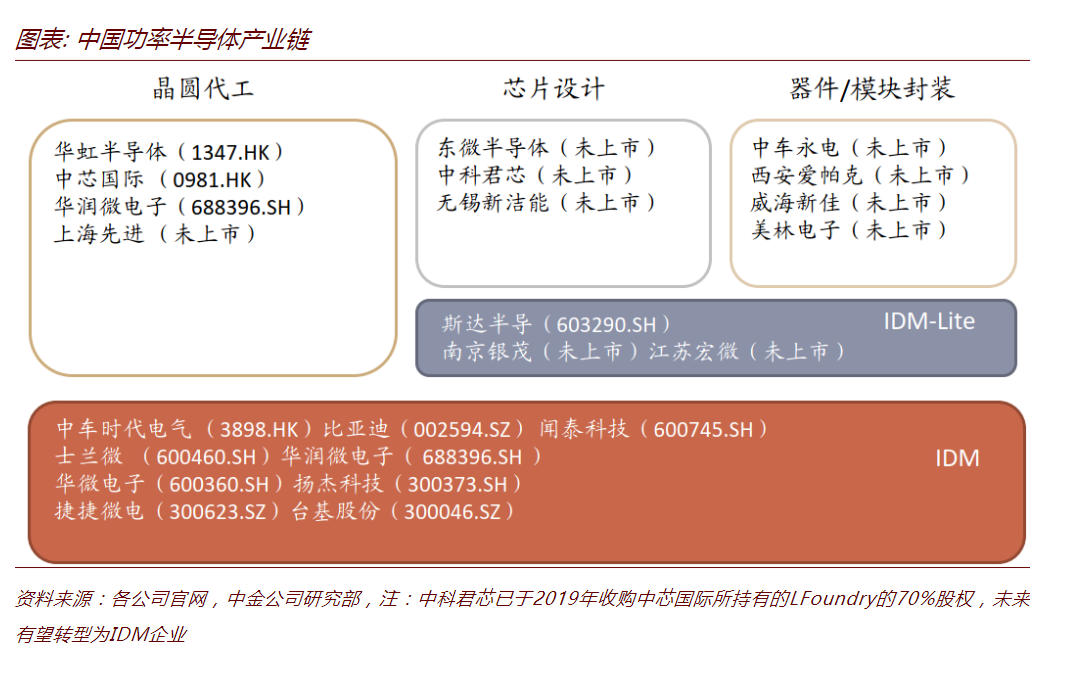

From the perspective of the industrial chain, companies involved in the power semiconductor industry in China are distributed throughout the entire industrial chain. This includes Huahong Semiconductor, one of the world’s largest power semiconductor foundries, as well as China Resources Microelectronics, and Wingtech Technology, which are IDM factories worth paying close attention to in the future.

01

What are Power Semiconductors?

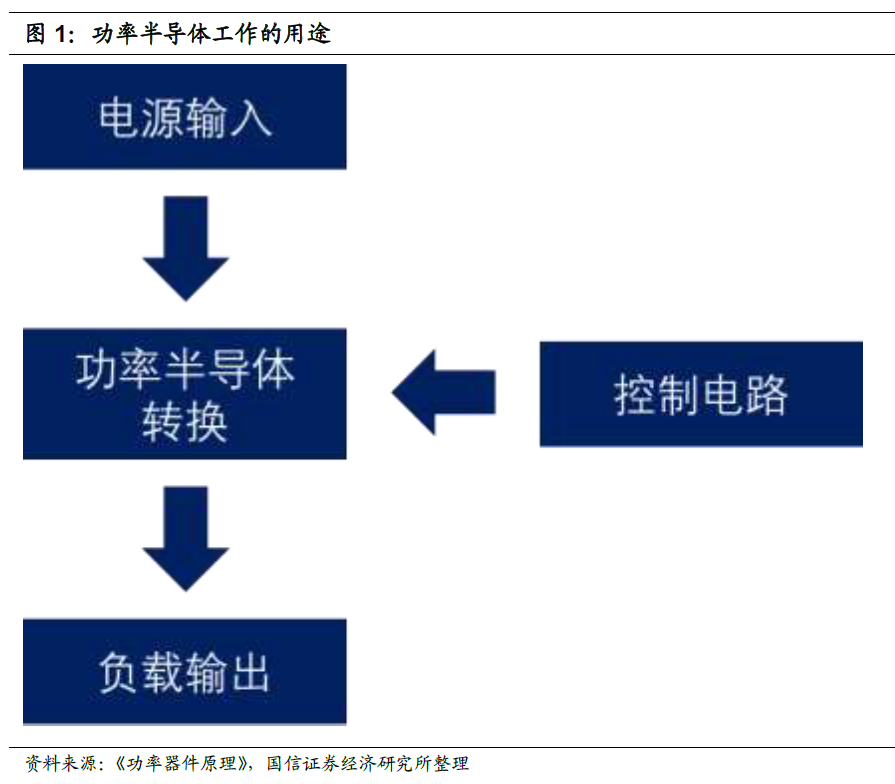

Power semiconductors are an important subfield within the semiconductor industry, serving as the core devices for energy conversion and circuit control, primarily used in electronic devices for voltage and frequency conversion, as well as DC-AC conversion.The core function of these devices is to ensure the output power size and delay with the minimum input control power.

Image Source: Guosen Securities

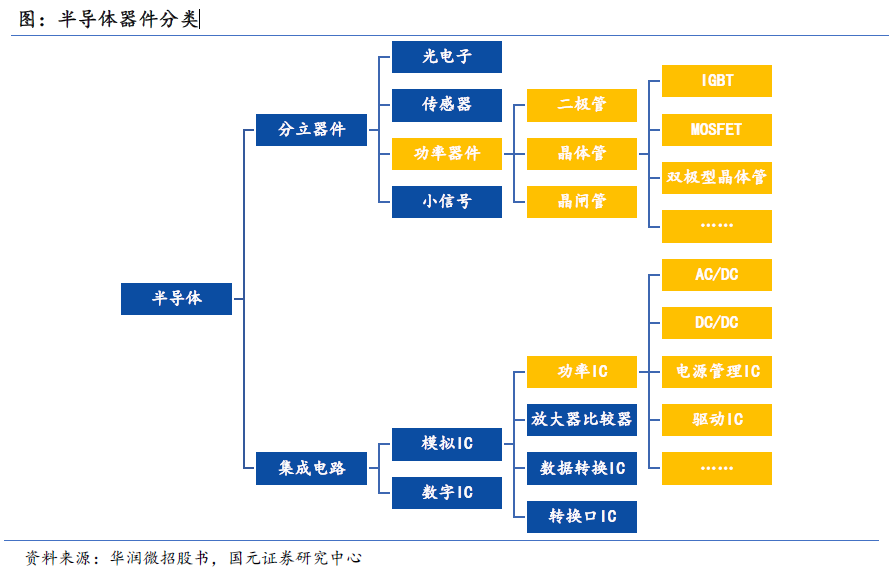

Classified by integration level, power semiconductors can be divided into power ICs and power discrete devices: the former integrates control circuits and high-power devices on the same chip, while the latter mainly includes diodes, transistors, and thyristors, each suitable for different fields based on voltage resistance and operating frequency.

Image Source: Guoyuan Securities

Transistors are the main components of discrete devices, with sub-products including bipolar transistors, MOSFETs (Metal-Oxide-Semiconductor Field-Effect Transistors), and IGBTs (Insulated Gate Bipolar Transistors).

MOSFETs and IGBTs have seen rapid market growth in recent years due to their superior performance and widespread applications, with their market share continuously increasing. IHS Markit predicts that MOSFETs and IGBTs will be the strongest growing semiconductor power devices in the next five years.

Image Source: GF Securities

02 Industrial and Automotive Sectors Dominate, with Automotive Growing the Fastest

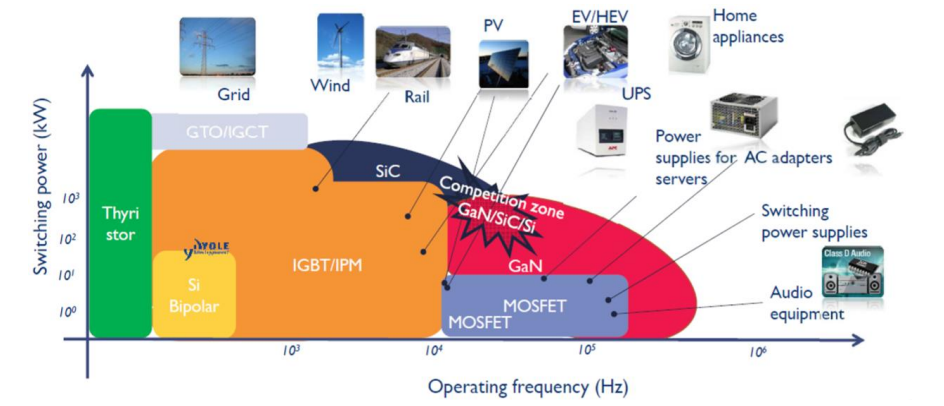

In terms of application scenarios, the main application fields of power semiconductors currently include six major directions: electric vehicles, renewable energy generation, industrial automation, energy storage, data centers and servers, consumer electronics/white goods.

Image Source: Yole Development

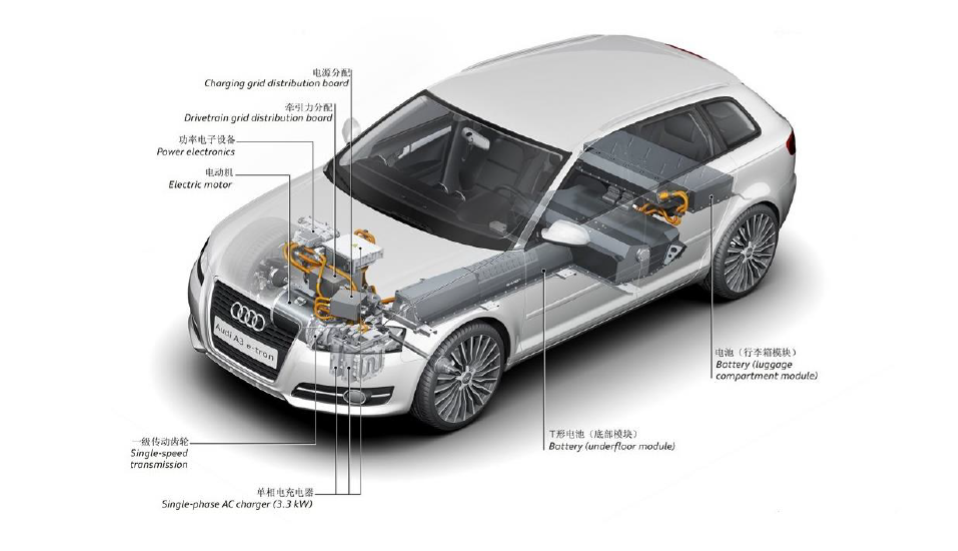

In the electric vehicle sector, power semiconductor components are converters needed to power the vehicle’s high-torque electric motors, DC/DC converters to reduce battery voltage, and additional similar components for battery chargers, making them critical for electric vehicle operation. The value of power semiconductors in electric vehicles is five times greater than that in traditional vehicles.

Image Source: Autohome

In the industrial sector, IGBT-based variable speed drives are increasingly replacing traditional motors in industrial applications: they can significantly improve energy efficiency, precisely control industrial motors, and save about 20-30% of energy consumption.

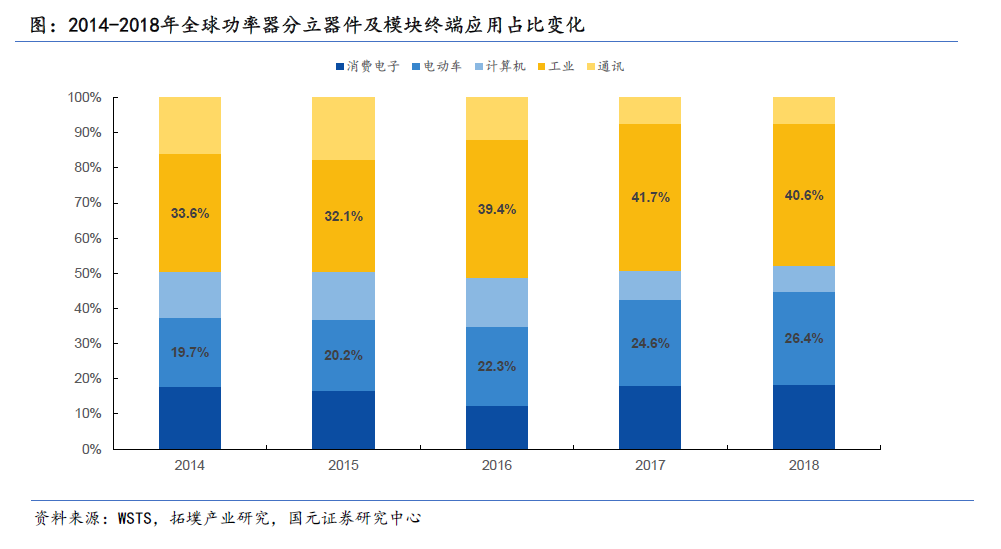

In terms of market share, WSTS statistics show that from 2014 to 2018, the main application fields for power semiconductors were industrial, automotive, and consumer electronics. The largest share was in the industrial sector, which exceeded 40% in 2018; followed by the electric vehicle sector, which reached 26.4% in 2018.

Image Source: Guoyuan Securities

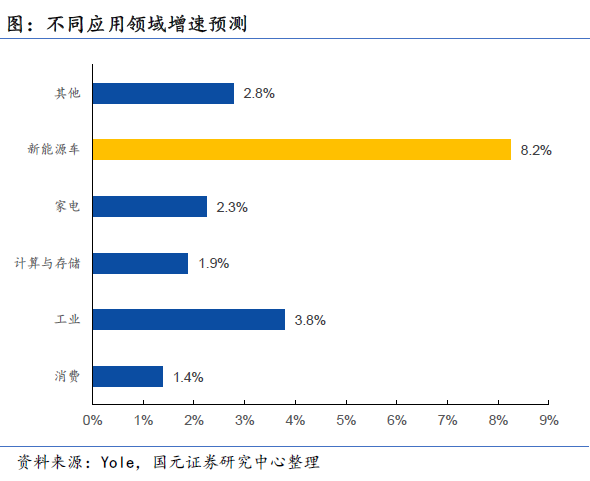

In addition to market share, the demand growth rate for power semiconductors in the automotive and industrial sectors is also remarkable, with compound annual growth rates of 8.2% and 3.8%, respectively. Yole predicts that by 2023, the market space for power semiconductors in the industrial and new energy vehicle sectors is expected to reach $3.7 billion, with the industrial sector accounting for $2.5 billion.

Image Source: Guoyuan Securities

03 $40 Billion Market: China’s Demand Exceeds 30%

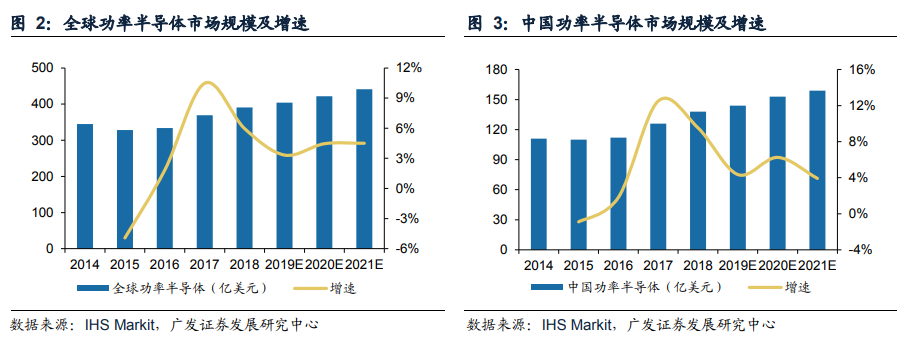

On a global scale, the power semiconductor market is showing a robust growth trend. According to IHS Markit data, the global power semiconductor market size was approximately $39.1 billion in 2018, and it is expected to grow to $44.1 billion by 2021, with an annual growth rate of 4.1%.

Image Source: GF Securities

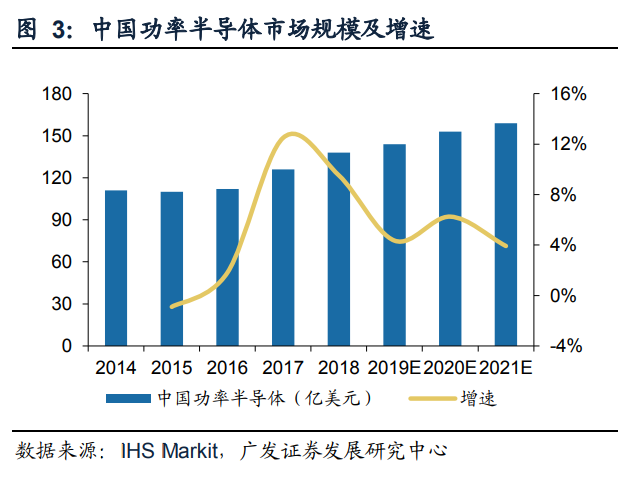

China is currently the largest consumer market for power semiconductors in the world.

According to IHS Markit data, in 2018, the demand scale in the Chinese market reached $13.8 billion, with a growth rate of 9.5%, accounting for 35% of global demand. The market is generally expected to continue to grow at a high speed in the future, with the market size expected to reach $15.9 billion by 2021, with a compound annual growth rate of 4.8%.

Image Source: GF Securities

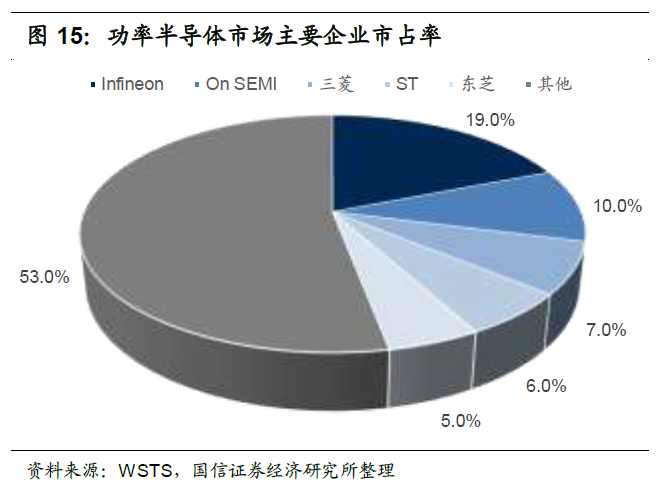

On the supply side, overseas giants still dominate the supply of power semiconductors.

WSTS data shows that in 2018, most of the top ten global power semiconductor companies are from the United States, Europe, and Japan, including Infineon, TI, NXP, and Renesas. The top ten manufacturers hold 57% of the market share. However, compared to the integrated circuit industry, the market concentration of power semiconductors is relatively low, and the commercial ecological barriers are not high.

Image Source: Guosen Securities

In terms of leading companies, the largest company in the market is Infineon, accounting for about 19%. The company’s most important products are MOSFETs and IGBTs.

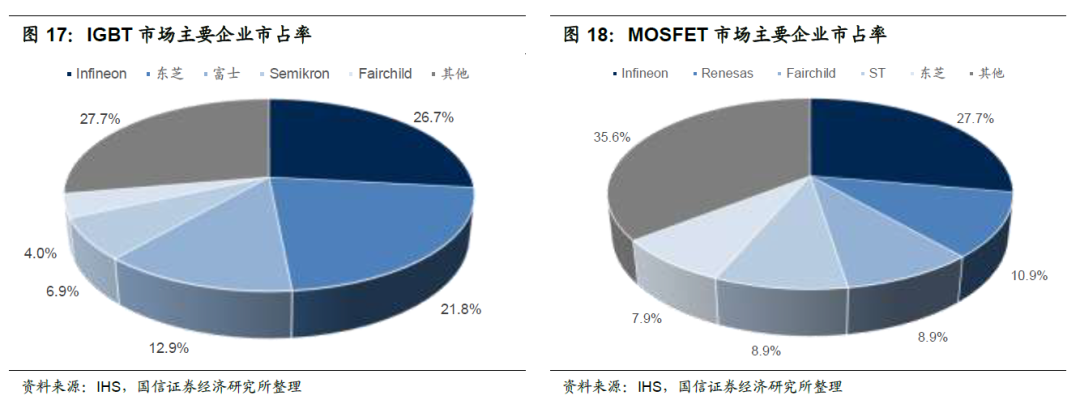

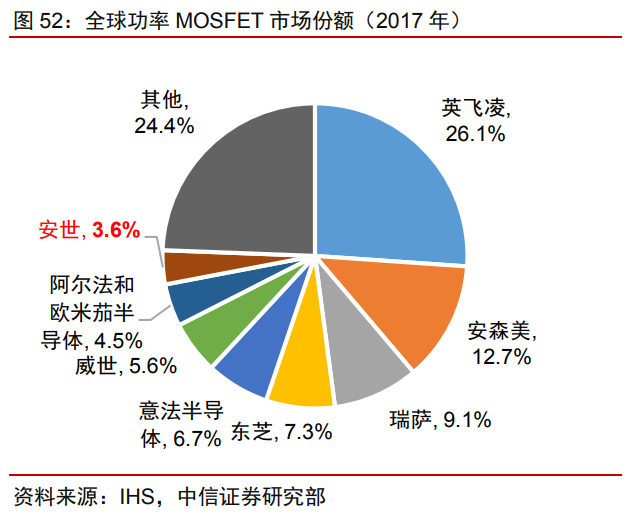

Infineon is also a leader in the MOSFET and IGBT submarkets, ranking first globally with market shares of 27% and 28%, respectively. Unlike the highly fragmented diode and transistor markets, the IGBT and MOSFET markets have higher market concentration due to their higher technical barriers.

Image Source: Guosen Securities

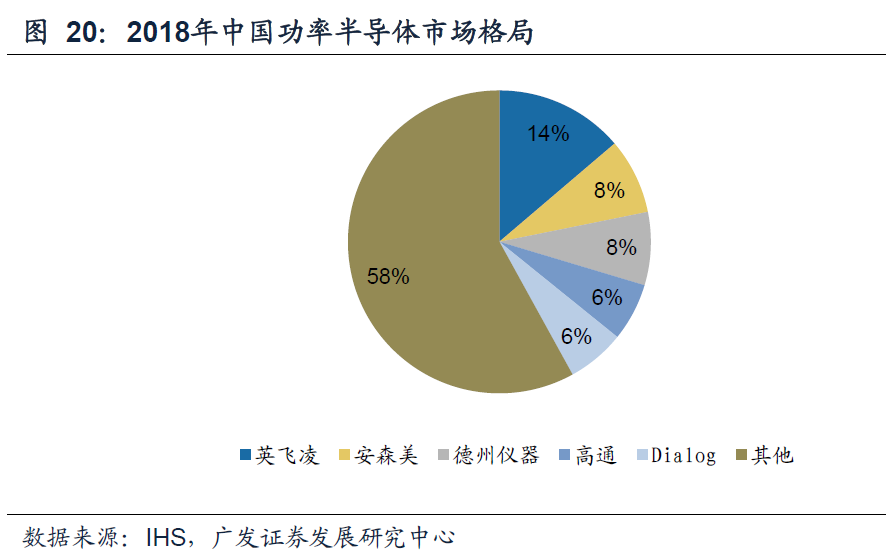

In terms of domestic power semiconductor supply, overseas giants also dominate: the top five suppliers in the market are Infineon, ON Semiconductor, Texas Instruments, Qualcomm, and Dialog, with a combined market share of 42%, with Infineon leading with a 14% market share.

Image Source: GF Securities

04 Is it One of the Fastest-Growing Segments for Domestic Substitution?

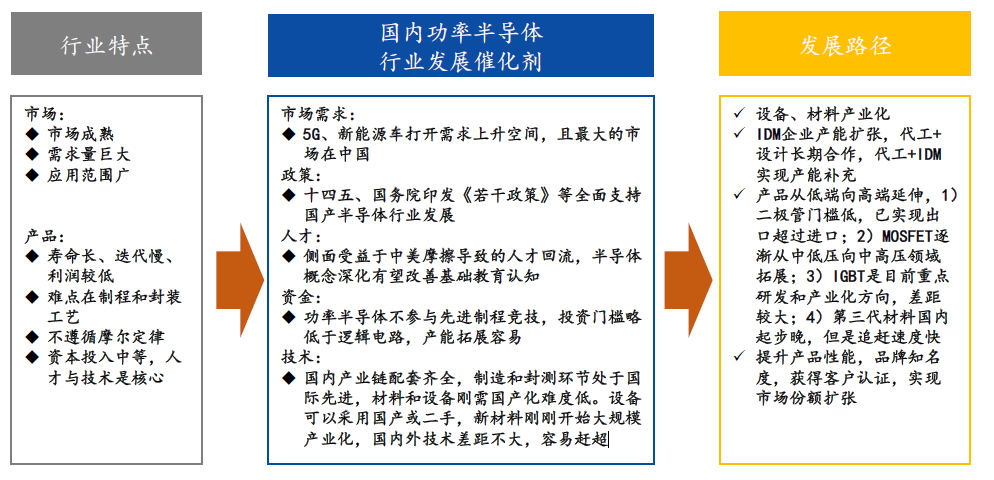

The dominance of overseas giants in supply does not mean that domestic power semiconductor manufacturers have no opportunities.

Although there is still a real gap between domestic manufacturers and overseas giants like Infineon, considering various factors such as market demand and technical difficulty, power semiconductors are expected to become one of the fastest-growing segments for domestic substitution in the foreseeable future, with a potential market size exceeding 110 billion yuan based on the domestic market share of overseas manufacturers.

Image Source: Zhongjin Securities

Compared to logic chips, the technical difficulty of catching up in power semiconductors is relatively low, and the domestic supporting industrial chain is also more complete..

In terms of industry attributes, power semiconductors do not need to catch up with Moore’s Law, mostly adopting mature processes, relying more on process technology, packaging design, and new material iterations, with an overall trend towards integration and modularization.

At the same time, the domestic industrial chain is well-equipped, with manufacturing and testing processes at an internationally advanced level, and the difficulty of domesticating materials and equipment is low. Equipment can be sourced domestically or second-hand, and new materials are just beginning large-scale industrialization, with little technical gap between domestic and foreign technologies, making it easier to catch up.

In terms of policy, the State Council has previously issued the “Notice on Encouraging the Development of the Software Industry and Integrated Circuit Industry,” fully supporting the domestic semiconductor industry.

Image Source: Guoyuan Securities

Under the catalysis of multiple factors such as market demand, policy, talent, funding, and technology, the domestic power semiconductor industry is expected to enter a golden development period in the next 3-5 years. Power semiconductors are expected to become one of the fastest-growing segments for domestic substitution in the foreseeable future.

05

Who are the Main Competitors in the Domestic Market?

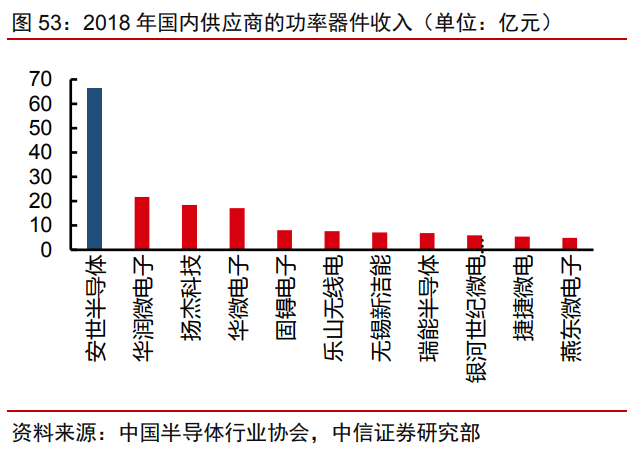

From the perspective of the industrial chain, companies involved in the power semiconductor industry in China can be divided into several types.

One type is foundry companies represented by Huahong Semiconductor, which has gradually grown to become one of the world’s largest power semiconductor foundries by focusing on MOSFET/IGBT process platforms, and has nurtured a number of power chip design companies such as SIDA Semiconductor, Zhongke Junxin, Wuxi Xinjieneng, and Dongwei Semiconductor.

The other type includes IDM factories represented by China Resources Microelectronics and Wingtech Technology, which integrate design and production.

Image Source: Zhongjin

In terms of key enterprises, Huahong Semiconductor, Wingtech Technology, and China Resources Microelectronics are three companies worth paying close attention to.

06

Huahong Semiconductor: Second in Domestic Foundry Rankings

Huahong Semiconductor is the seventh largest foundry globally and the second largest in mainland China. The company is controlled by Huahong Group, with strategic investment from the National Integrated Circuit Fund, and the actual controller of Huahong Group is the Shanghai State-owned Assets Supervision and Administration Commission. The company was listed on the Hong Kong Stock Exchange in 2014. By the end of 2019, the company had achieved profitability for 36 consecutive quarters.

Image Source: Industrial Securities

In terms of business, Huahong Semiconductor provides foundry services covering processes above 90nm for domestic and foreign customers. The 250nm and above nodes mainly focus on discrete devices and power management chips, including power MOSFETs, super junctions, and IGBTs.

The Wuxi 12-inch factory, which started production in the fourth quarter of last year, extends the process node to 55nm, covering products such as SIM cards, bank cards, automotive and security chip MCUs, NOR Flash, power management, CIS, and power devices, and is the industry’s first 12-inch power device wafer foundry line, which has already begun delivering products to customers.

Image Source: Huahong Semiconductor Official Website

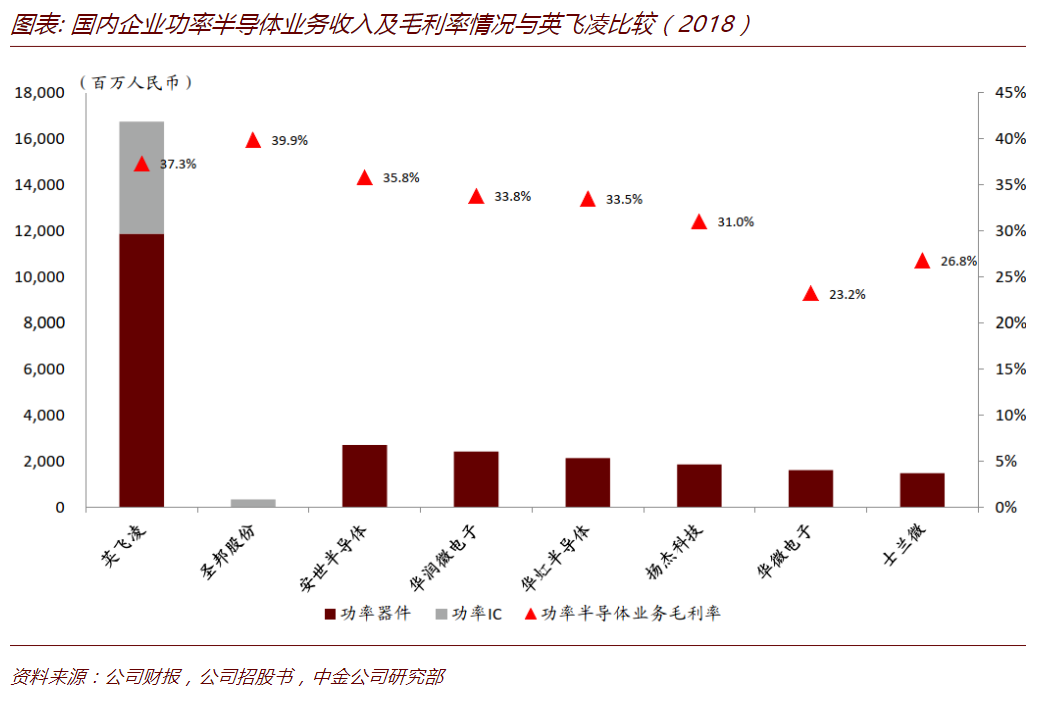

From a revenue perspective, power discrete devices are the fastest-growing technology platform for the company, with a revenue share of 37.3% in Q1 2020. The company’s power discrete devices mainly include MOSFETs, SJNFETs, and IGBTs. These products are customized in small quantities, and due to the shortage of 8-inch wafers, the average selling price remains relatively stable.

In terms of profitability, Huahong is in the second tier of foundries. Unlike large foundries like Foxconn that pursue advanced processes, Huahong focuses on 8-inch wafer foundry and adopts mature processes, although its gross margin is significantly lower than that of TSMC and other large foundries, the company’s capital expenditure and depreciation are significantly lower than those of 12-inch wafer foundries pursuing advanced processes. As of Q4 2019, the company had achieved profitability for 36 consecutive quarters.

However, due to a decrease in capacity utilization and the impact of the Wuxi 12-inch capacity and yield, the company’s gross margin has recently declined. Analysts believe that as Huahong Semiconductor completes the expansion of its Wuxi plant, its capacity scale will surpass the world’s advanced levels. Future attention should be paid to whether the overall market supply and demand will be excessive and whether government subsidies will be maintained.

07

China Resources Microelectronics: The Largest Power Semiconductor IDM in China

China Resources Microelectronics (CR Micro) is the largest power semiconductor company in China and the only IDM company among large semiconductor enterprises in the country.

The company was listed in Hong Kong in 2004, but due to the characteristics of the industry (capital and technology-intensive) and external competitive pressures (the company needs to compete directly with first-tier semiconductor manufacturers in Europe and the United States), the company’s stock price has been lackluster, and during the 2008 financial crisis, the stock price plummeted by over 90%, ultimately delisting in 2011.

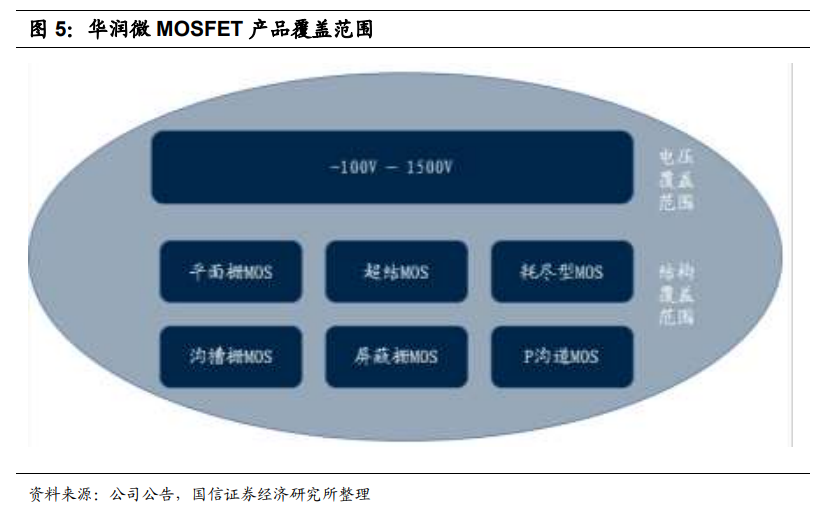

In terms of product lines, CR Micro is the domestic manufacturer with the most comprehensive product lines for power discrete devices. The MOSFET product line has the largest revenue scale in China, with leading technical capabilities. The domestic market share of MOSFET products is 9%, second only to Infineon and ON Semiconductor, ranking first among Chinese companies..

Image Source: Guosen Securities

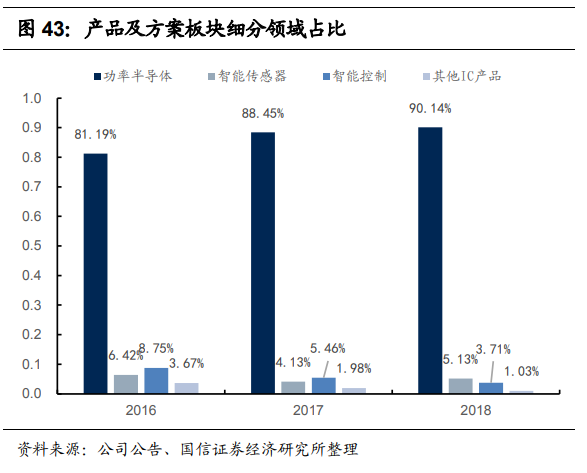

In terms of revenue, the company achieved total revenue of 6.27 billion yuan in 2018 (43% from self-owned products and 57% from foundry), ranking tenth among all semiconductor companies in China, with power semiconductor business revenue ranking first.

Power semiconductors account for the absolute majority of the company’s revenue, exceeding 80%, while other product lines include smart sensors, smart control, etc.

Image Source: Guosen Securities

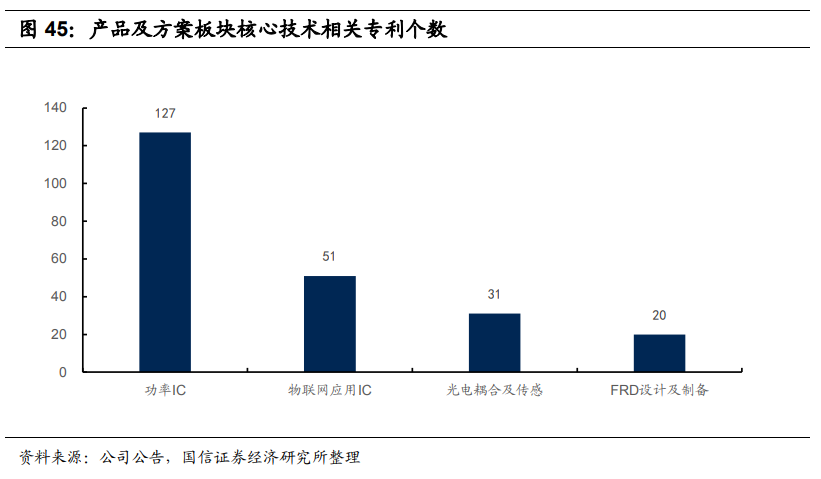

Statistics show that CR Micro has been granted 1,173 domestic patents and 152 domestic patents. In the product and solution sector, the company has a series of core technologies in IoT applications, power ICs, optocouplers, and sensors, leading domestically.

Image Source: Guosen Securities

In terms of capacity and product technology, the company currently has three 6-inch and one 8-inch semiconductor wafer manufacturing production lines, and an 8-inch production line is under construction, with the 8-inch capacity for power semiconductors ranking first in China. The company is also planning a 12-inch project, and external analysis suggests that once the 12-inch project is completed and reaches production, it will further enhance the company’s capacity reserves and product competitiveness, driving a new leap in revenue and profit scale.

Image Source: Zhongjin

From an investment perspective, future attention should be paid to capacity, gross margin, and the recovery of downstream demand.

08

Wingtech Technology: Acquiring a Global Top Ten Giant

Unlike the previous two relatively pure semiconductor manufacturers, Wingtech Technology was originally a global leader in mobile phone ODM and entered the power semiconductor market through acquisitions.

In 2018, the company initiated the acquisition of the semiconductor company Nexperia and officially consolidated its financials in November 2019. Currently, the revenue share of Wingtech headquarters and Nexperia is 79%/21%, and the profit share is 47% and 53%, respectively.

Nexperia was originally the standard device division of NXP, which began independent operations in February 2017, and is the ninth largest power device manufacturer globally, ranking seventh among domestic semiconductor companies.

Image Source: CITIC Securities

Nexperia adopts an IDM business model, with main products including discrete devices, logic devices, and MOSFET devices. The company currently has over 10,000 product models, adding 800 new models each year, and shipped approximately 100 billion units in 2019, corresponding to a revenue scale of 10.4 billion yuan, with a gross margin of 35.1% and a net profit margin of 12.2%, with an overall market share of nearly 15% in its subfield.

Image Source: CITIC Securities

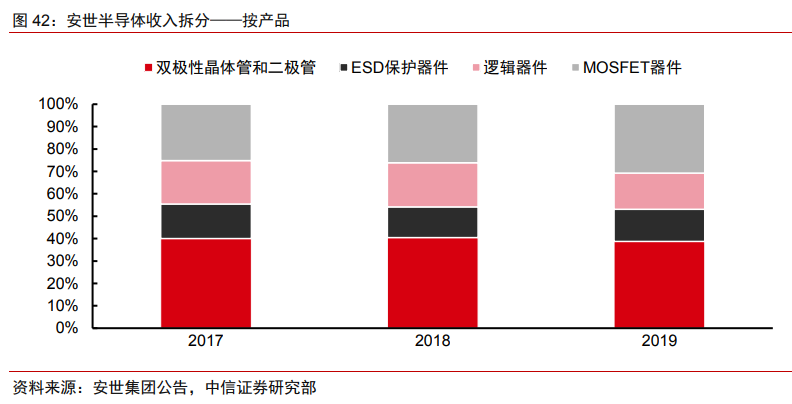

The company’s products can be categorized into three major divisions: bipolar transistors and diodes, MOSFET devices, and logic and ESD protection devices, with the first two belonging to discrete devices in power semiconductors. In 2019, the revenue share of these two divisions exceeded 65%.

Image Source: CITIC Securities

With superior technical capabilities and revenue scale compared to domestic competitors, especially in the automotive sector where product quality requirements are high, Nexperia is a rare automotive-grade manufacturer in China, and after the acquisition, it is expected to become a pioneer in domestic substitution in the power device field, filling the gaps in domestic layouts..

Image Source: CITIC Securities

In terms of customer resources, Nexperia has established a world-class global sales network, serving over 25,000 customers. Its coverage includes top manufacturers and service providers in various industries such as automotive, industrial and power, mobile and wearable devices, consumer electronics, and computing.

Image Source: CITIC Securities

In terms of product lines, Nexperia has previously focused on the research and production of standard devices, and its layout in some high-end power device fields has been relatively insufficient. With the support of domestic capital, the market expects Nexperia to further increase its investment in R&D resources and plans to enter the fields of high-power MOSFETs, GaN, and SiC, further strengthening its leading position in the domestic power device field.

Currently, capacity is the main constraint for the company. The company’s overall wafer capacity is close to 700,000 pieces/year, and the capacity utilization rate is already at a high level.

The acquisition has transformed Nexperia from a global leader in power devices to a domestic leader in power devices, and it is expected to receive support from domestic policies and funding, providing ample guarantees for subsequent revenue expansion through comprehensive capacity expansion. Future attention should be paid to the integration of both companies and new customer orders.

END

Distribution Map Available

【Disclaimer】 The article represents the author’s independent views and does not represent the power semiconductor ecosystem. If there are issues related to the content, copyright, etc., please contact the power semiconductor ecosystem within 30 days of publication for deletion or copyright negotiation. Online advertising cooperation: 17301750044