Author: Jay Yu (Pantera Capital)

Co-authored by Ryan Barney

A dormant HTTP status code for 25 years is being revived, and the “payment required” scenario it describes is transitioning from a technical prophecy to a daily reality in global trade.

If you have never lived in Latin America, Africa, or Central Asia, it is hard to truly understand one thing: why developers there are not discussing “how to integrate Stripe,” but rather “how to parse a 402 response.”

While Silicon Valley is still debating which L2 is faster, e-commerce platforms in Buenos Aires are already using the 402 status code to automatically complete USDC payments — this is not a technical demonstration, but a production system handling tens of thousands of transactions daily.

01

When traditional finance is absent, emerging markets begin to choose “on-chain dollars”

To understand why Latin America has become the largest incremental market for stablecoins, we must first acknowledge a harsh reality: not every country has a reliable banking system.

In Argentina, cumulative inflation over ten years exceeds 800%;

In Venezuela, the local currency’s “savings utility” is nearly zero;

In Mexico and Brazil, domestic payment systems are mature, but cross-border transactions remain expensive, slow, and cumbersome.

The so-called financial infrastructure does not exist in many countries. Thus, stablecoins have become “the most stable thing.”

This is why USDT/USDC serves a unique function in Latin America:it is both a store of value and a cross-border payment tool, as well as a medium of exchange.This is not that crypto has created “demand,” but rather that demand itself has forced the technological route.

The deeper globalization goes, the more useful stablecoins become; the less stable the currency, the more necessary stablecoins are.

02

A new payment infrastructure is reconstructing corporate payment systems

While the market still equates on-chain payments with personal wallet transfers, real change has quietly occurred on the enterprise side. In 2024, the scale of enterprise-level stablecoin payments will exceed $100 billion, with B2B stablecoin payments processed by Coinbase alone growing by 380% year-on-year. This marks the official evolution of stablecoins from speculative assets tothe infrastructure for cross-border payments in enterprises.

The three major cost barriers of traditional cross-border payments are being dismantled by technology:

R&D costs are absorbed by standardized APIs, reducing the time for enterprises to integrate stablecoin payments from months to days;

Compliance costs are significantly reduced through on-chain regulatory technology, with Chainalysis data showing a 60% improvement in compliance efficiency for enterprises using KYT tools;

Account system costs disappear due to borderless wallet addresses, allowing enterprises to settle directly without intermediaries.

Real-world cases confirm this trend: the cross-border e-commerce platform Shopify integrated Coinflow, enabling its North American merchants to receive USDC payments from overseas customers, compressing settlement time from 3-5 days to real-time; cross-border payroll service provider Deel uses Circle’s B2B suite to reduce multinational payroll costs by 70%. These practices demonstrate that stablecoins are completing a critical leap from a medium of exchange tosettlement infrastructure.

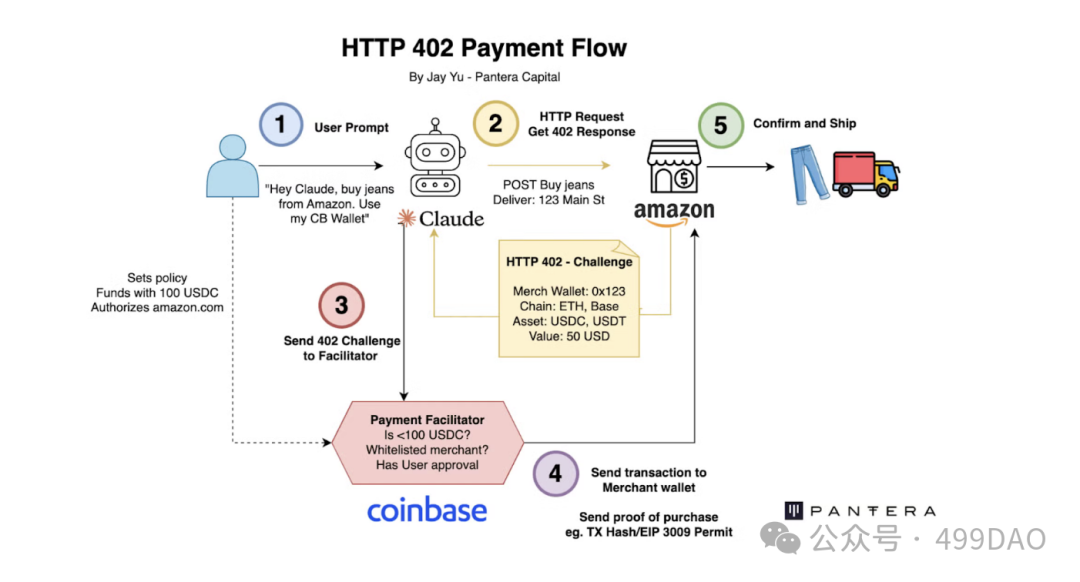

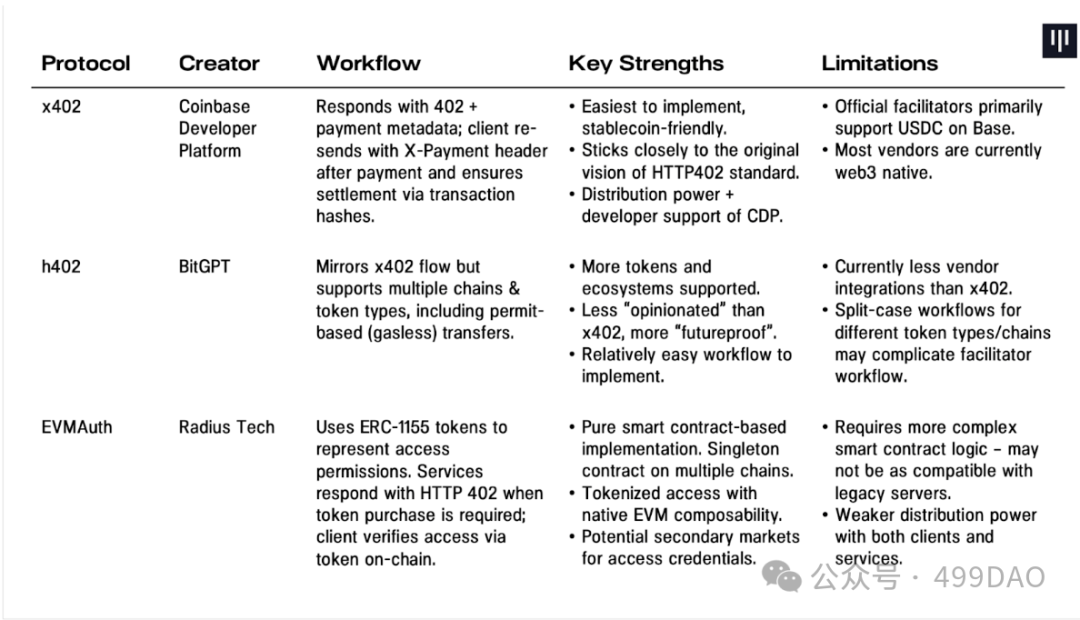

More profound changes are occurring at the protocol level. With the re-enabling of the HTTP 402 status, payment processes are evolving from “integrated” to “responsive.” When an enterprise server returns a 402 response, AI agents can automatically read payment metadata and complete on-chain transfers — this model has been validated in the integration of Google A2A protocol with Coinbase x402, achieving a new interaction paradigm of “conversation as payment.”

The essence of this transformation is a paradigm shift in payment logic: when payments transition from requiring complex integrations as a business function to being a native capability at the HTTP protocol level, the thresholds for global commerce will be redefined. Just as cloud computing abstracted IT infrastructure into callable services, on-chain payments are encapsulating global clearing and settlement capabilities into standardized interfaces.

Enterprises adopting stablecoin payments see an average gross margin increase of 5-8 percentage points in their cross-border business, which is concrete evidence of technology-driven business efficiency improvements. When enterprises can call upon global payment networks as easily as they call cloud services, Web3 truly demonstrates its disruptive power in reconstructing traditional financial infrastructure.

03

The arrival of regulatory technology makes the path for stablecoins increasingly “bright”

Before 2023, when Federal Reserve Chairman Powell spoke about stablecoins in congressional hearings, his keywords were always “systemic risk” and “urgent need for regulation.” However, in less than two years, a dramatic shift occurred — by early 2025, the Office of the Comptroller of the Currency (OCC) in the U.S. explicitly allowed national banks to issue stablecoins, and the EU took the lead in implementing a comprehensive regulatory framework. Behind this policy shift is a profound change in regulatory logic:

from defensive blocking to infrastructure co-construction.

The driving force behind this transformation is the unprecedented transparency provided by on-chain regulatory technology.

In the traditional financial system, tracking cross-border funds relies on layers of bank reporting, and anti-money laundering checks often lag by weeks; however, the public ledger of blockchain and smart analysis tools have enabled regulatory agencies to achievereal-time panoramic monitoring.

For example, Circle’s collaboration with Chainalysis allows its KYT (Know Your Transaction) system to mark suspicious USDC flows in real-time, with an accuracy rate exceeding 40% compared to traditional methods. This technological advantage has shifted the perspective of stablecoins from being a “source of risk” tothe most easily monitored payment track.

Deeper changes lie in thecodification evolution of regulatory enforcement mechanisms. The U.S. Treasury’s 2024 research report clearly states: “Programmable compliance will become the core of next-generation financial regulation.” In practice, enterprises can now encode requirements such as sanctions list checks and transaction limit controls into smart contract logic, achievingmillisecond-level automatic compliance verification.This transformation not only significantly reduces compliance costs but, more importantly, shifts regulatory requirements frompost-event checks to pre-embedded, forming a security layer that coexists with business.

It is worth noting that regulatory agencies themselves are also actively embracing technological change. The Monetary Authority of Singapore (MAS) has launched a “regulation as a service” platform that can directly connect to certified DeFi protocols, enabling non-intrusive data acquisition and risk assessment. This model ensures regulatory effectiveness while avoiding excessive interference with innovative businesses.

This marks the establishment of a new paradigm: when compliance evolves from textual regulations to executable code, and regulation upgrades from manual review to real-time protocols, the trust foundation for financial innovation can be reconstructed. Just as the explosion of the internet relied on the trustworthy environment built by TCP/IP and TLS encryption protocols, the current combination of on-chain regulatory technology and stablecoins is paving the way for the next generation of financial infrastructure for global value flow.

The ultimate goal of regulation is no longer to set up barriers but to establish traffic rules. When stablecoins can safely operate on transparent tracks, Web3 will truly gain the passport to enter the mainstream economy.

04

Stablecoins may become the “default option” for global value flow

When a technology transitions from being an “option” to a “default option,” it signifies the arrival of structural change. Stablecoins are standing at this critical point.

Data shows that in 2024, the settlement volume of stablecoins has exceeded $13 trillion, approaching the annual processing scale of the Visa network. This is not driven by speculation but by real value transfer needs. In the Philippines, over 6 million overseas workers remit money home through USDT, saving 15-20% in fees compared to traditional channels; in Argentina, with an annual inflation rate exceeding 200%, merchants prefer to accept dollar stablecoins rather than the continuously depreciating peso.

The rise of stablecoins stems from their unique five-in-one advantages:Global accessibility allows any internet connection point to become a financial node;No bank account barrier provides opportunities for 1.7 billion adults without bank accounts to participate in the modern economy;Anti-inflation properties serve as the last line of defense for people in hyperinflation countries to protect their wealth;Real-time settlement compresses the traditional cross-border remittance cycle from 3-5 days to seconds;Highly auditable on-chain records allow every fund flow to be traceable, providing unprecedented transparency for regulation.

This technology is not meant to replace SWIFT or Visa but to fill the significant gaps in the existing financial system. Just as the internet did not completely replace offline commerce but created a new form of digital economy, stablecoins are building a digital financial layer parallel to traditional banks. It specifically serves scenarios deemed “uneconomical” or “high-risk” by traditional systems: small cross-border remittances, trade settlements in emerging markets, and real-time payroll payments.

Circle CEO Jeremy Allaire has pointed out: “The digital dollar is becoming the native settlement layer of the internet.” This judgment is becoming a reality. From Shopify merchants accepting USDC payments to X platform integrating cryptocurrency payment features, the mainstream business ecosystem is quietly embracing this change.

In the next decade, as regulatory frameworks improve and technological infrastructure matures, stablecoins will gradually become “invisible” — just like today’s HTTP protocol, users will not need to understand the underlying technology but can seamlessly enjoy the convenience it brings. When value transfer becomes as simple as sending an email, we will have truly entered the era of the value internet.

The essence of this transformation is the ultimate evolution of financial democratization — lowering the threshold for global value flow to an infinitely low level, allowing everyone to participate equally in the global economy.

Conclusion: Stablecoins are not a narrative

They are the answer to reality.

Physical merchants in Latin America, freelancers in Africa, small traders in the Middle East, and e-commerce suppliers in Southeast Asia do not care about “what the next bull market for Web3 is”; they care about: Can the money arrive faster? Is the payment more stable? Are the cross-border fees worth it? Is there a more controllable option than black market dollars? Thus, stablecoins have become the answer. This change is also becoming a key turning point for Web3 to truly enter the global economy. The future of global finance will not be about crypto rewriting banks, nor banks eliminating crypto, but a new reality: value will automatically flow to the most efficient tracks. And this track is increasingly resembling stablecoins.