Author: RunningLuSource: Flying Deer (ID: RunningLu666)

Author: RunningLuSource: Flying Deer (ID: RunningLu666)

01

Industry Chain Overview

02

Introduction to PCB

PCB, or Printed Circuit Board, is the “connection hub + support frame” of electronic products. Its core function is to connect various electronic components through circuits, allowing smooth transmission of current and signals, serving as a critical “connecting bridge”. Almost all electronic devices rely on it: it not only provides support as a “fixed base” for electronic components but also plans the circuit, enabling power supply or insulation, ensuring electrical performance.

The quality of PCB manufacturing directly affects the stability and longevity of electronic products and influences the overall competitiveness of the product, which is why it is referred to as the “mother of electronic products”.

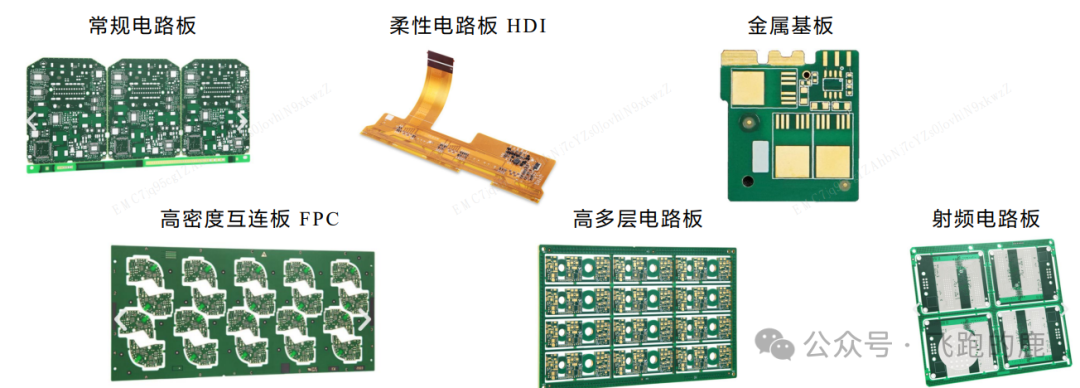

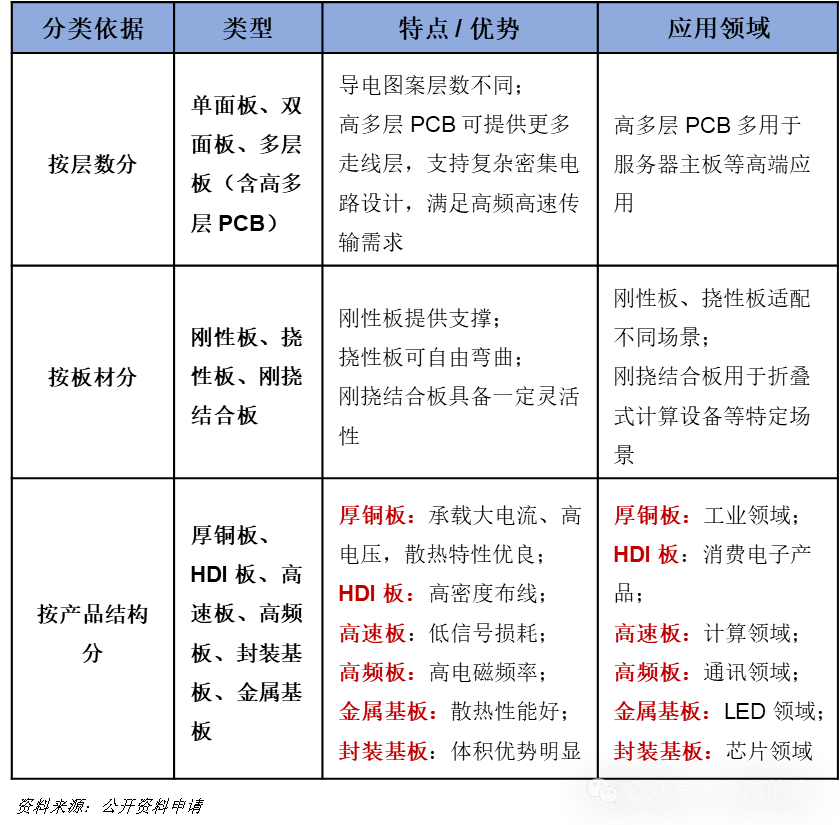

PCB Diagram

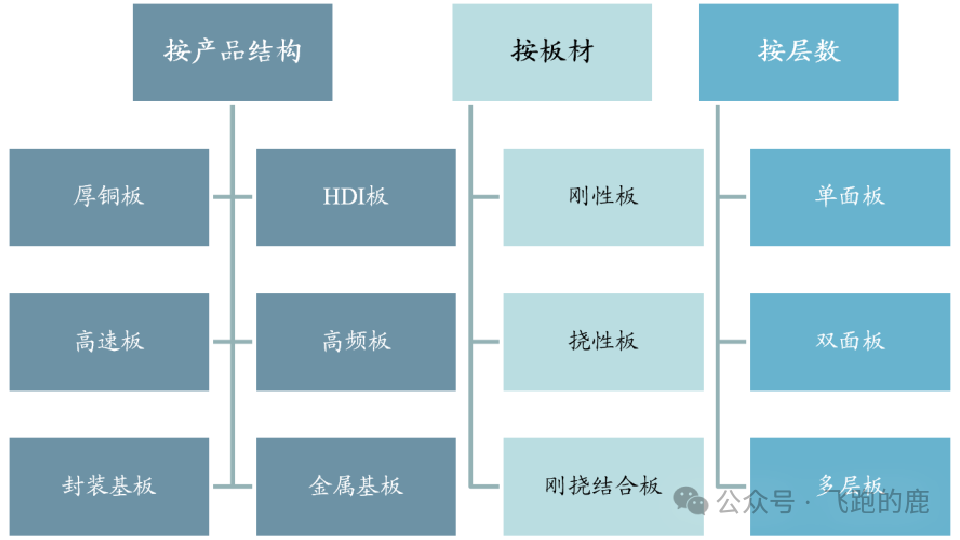

There are many classification methods for PCBs, but three are commonly used in the industry: one is based on the number of conductive layers, another is based on the material used for the board, and the third is based on the structure of the product itself.

03

Market Size

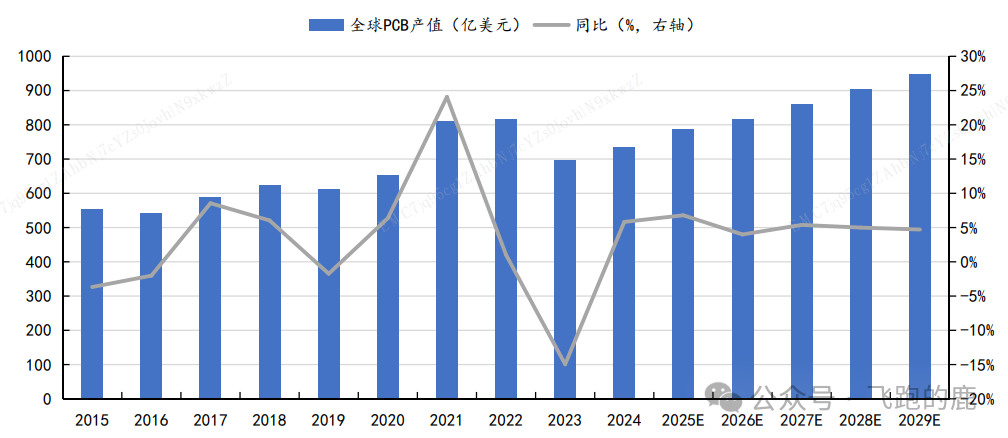

With market inventory adjustments and a softening demand for consumer electronics coming to an end, coupled with accelerated AI applications, the inventory reduction and interest rate hikes of 2023 have passed, and the PCB industry is entering a new growth cycle.

In 2024, the global PCB market value is projected to reach $73.565 billion (up 5.8% year-on-year), and it is expected to reach $94.661 billion by 2029, with a CAGR of 5.2% from 2024 to 2029, indicating a revival in global value.

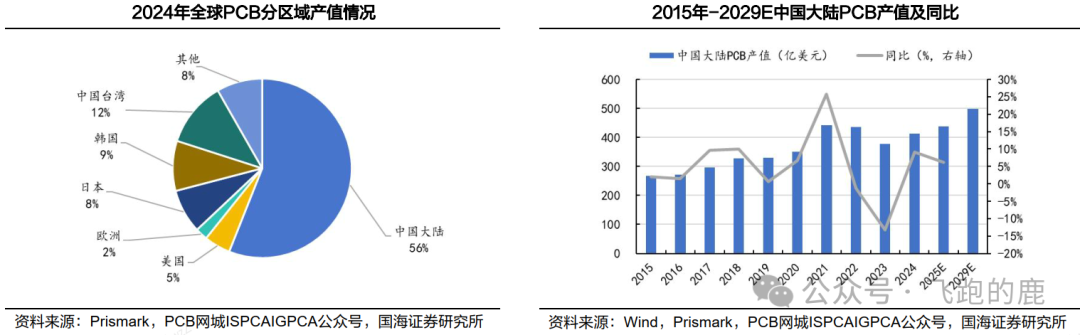

In 2006, mainland China surpassed Japan to become the world’s largest PCB production base, marking a shift in the industry landscape; in 2024, mainland China’s output value is expected to reach $41.213 billion, accounting for 56% of the global total (Prismark data).

Global PCB production capacity is shifting to mainland China, driven by the development of downstream electronic terminal industries, consumer electronics, AI, and new energy vehicle applications, which are boosting PCB demand. Prismark predicts that by 2025, mainland China’s output value will reach $43.734 billion (up 6.1% year-on-year), and by 2029, it will reach $49.704 billion, with a CAGR of 3.3% from 2025 to 2029.

04

Cost Breakdown

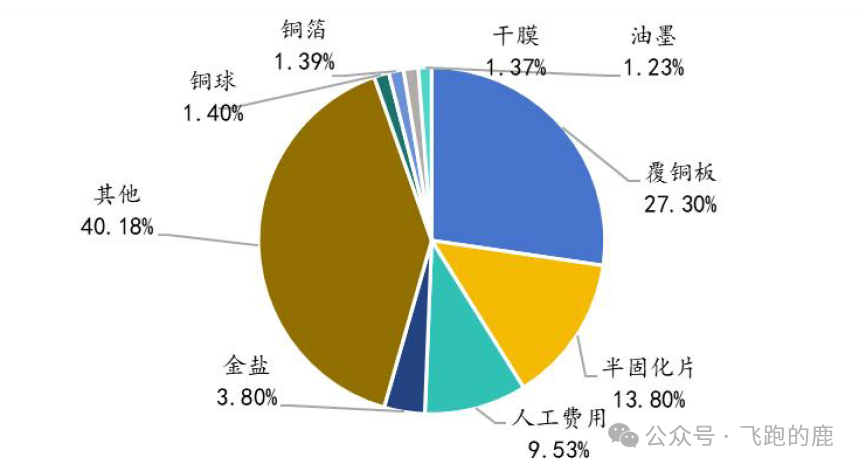

Relevant data shows that the cost breakdown of PCBs is as follows, with copper-clad laminates holding the highest cost:

05

Copper Clad Laminate

Copper Clad Laminate (CCL) is the core material for making PCBs, akin to the “load-bearing wall” of a house—first, electronic glass fiber cloth and other reinforcing materials are soaked in resin adhesive, dried, cut into prepreg, and then copper foil is hot-pressed on one or both sides to form a structure that allows for interconnection of components, insulation of current, and structural support for the PCB.

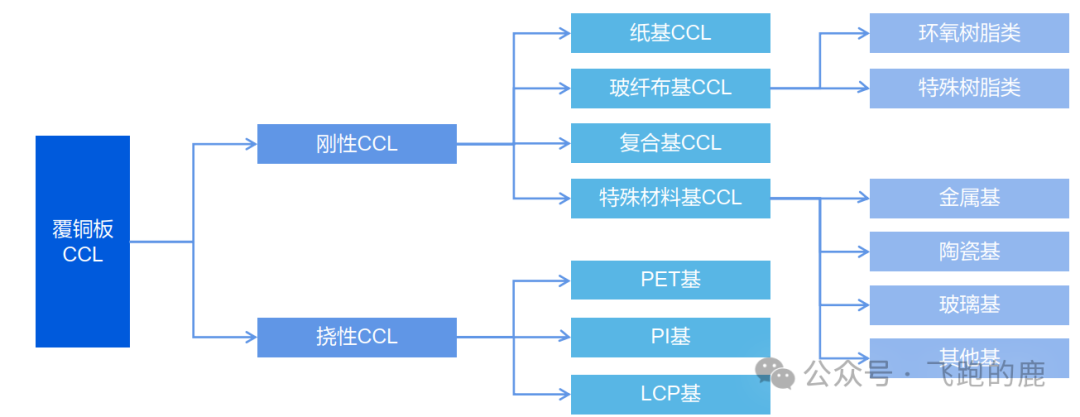

Based on composition materials and mechanical properties, common copper clad laminates are mainly divided into two categories: “rigid” and “flexible”. Rigid CCLs are further divided based on substrate materials into paper-based, glass fiber cloth-based, composite-based, and special material-based; flexible CCLs are categorized based on flexible materials into PET-based, PI-based, and LCP-based.

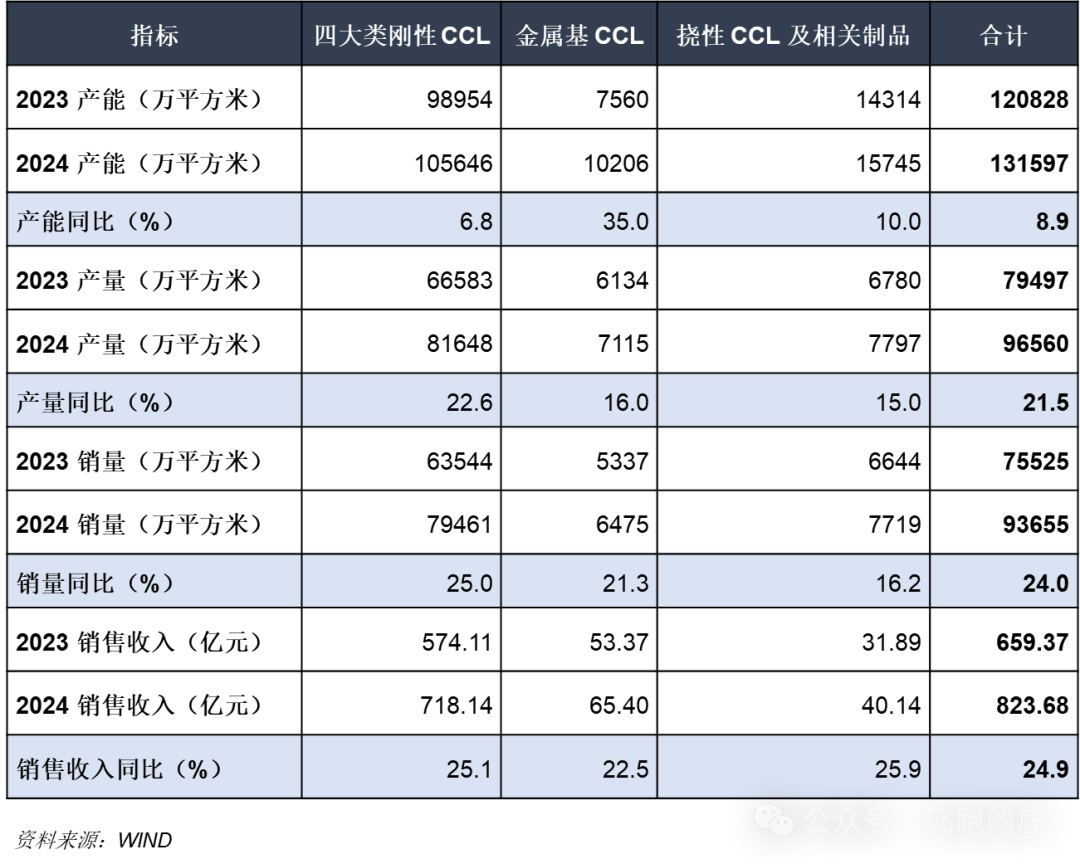

In 2024, both the production and sales of copper clad laminates in China are expected to achieve rapid growth, as detailed below:

05-1. Copper Foil

PCB copper foil is a thin layer of copper deposited on the substrate of the circuit board, serving as the “signal transmission line” of the circuit board, and is an important raw material for manufacturing CCL and PCB, with the core function of signal transmission. It is made together with electronic-grade glass fiber cloth, special wood pulp paper, synthetic resin, and other materials to form copper clad laminate, which is then processed through a series of processes to ultimately form the PCB.

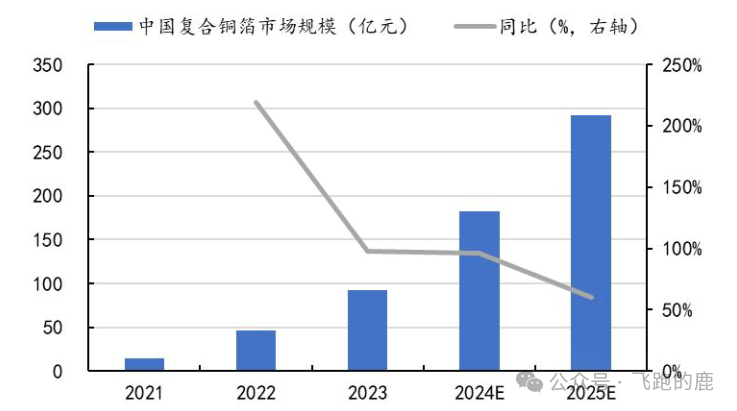

The domestic composite copper foil has now entered a critical stage of material certification and loading tests, with the potential for a breakthrough in large-scale application from 0 to 1. The market forecast changes are as follows:

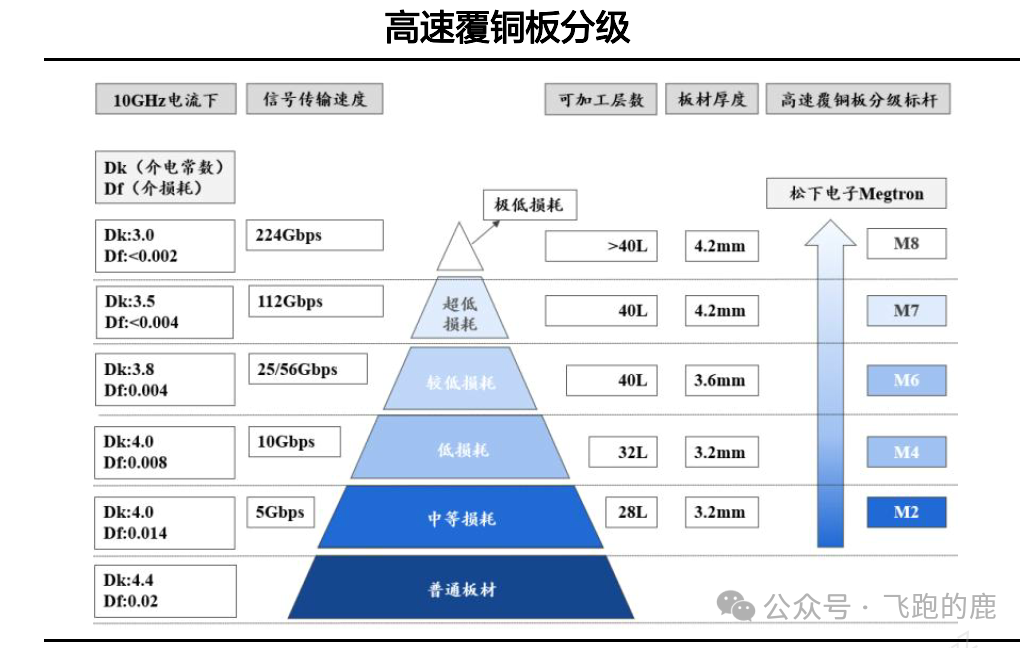

05-2. High-Frequency High-Speed Copper Clad Laminate

High-speed copper clad laminate is like a “high-speed network cable” in the circuit board, capable of achieving fast signal transmission of 10-50Gbps, with high accuracy, minimal signal dispersion, and low loss, primarily used in data processing centers, servers, switches, and routers.

High-frequency copper clad laminate (High Frequency Copper Clad Laminate) is a “dedicated receiver” for ultra-high frequency signals, operating at frequencies exceeding 5GHz, suitable for ultra-high frequency scenarios, requiring ultra-low dielectric constant (Dk) and as low as possible dielectric loss (Df). It is a core material for 5G base stations, autonomous driving millimeter-wave radar, and high-precision satellite navigation, with demand continuously increasing.

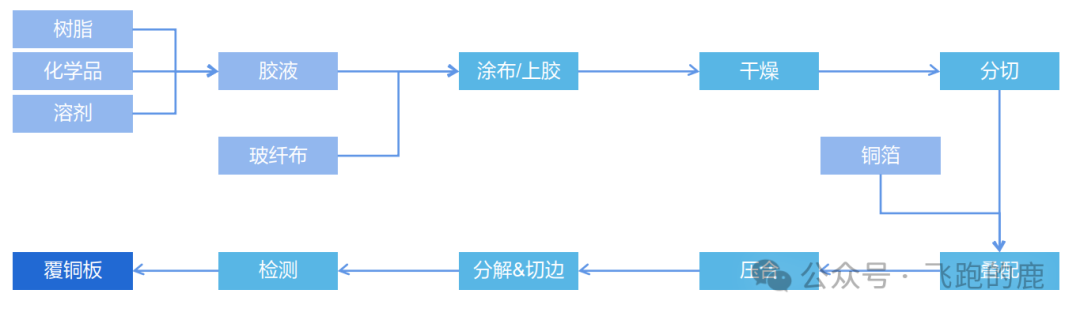

Similar to high-speed copper clad laminates, to reduce Dk, the main approach is to modify insulating resins, glass fibers, and overall structure. Currently, the mainstream high-frequency copper clad laminates on the market are mostly made from polytetrafluoroethylene (PTFE) and hydrocarbon resins, with the following production process:

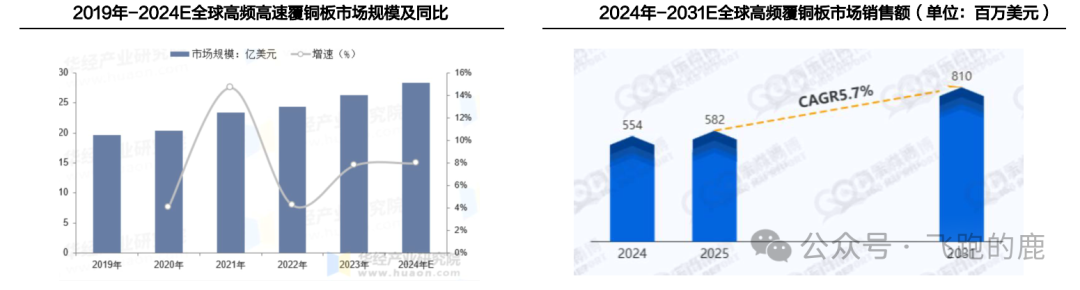

High-frequency high-speed copper clad laminates are growing faster than the entire copper clad laminate industry, driven by upgrades in base stations and core network servers. With the advent of the 5G era, antennas/RF modules for macro and micro base stations, as well as optical communication modules and new packaging processes, will increasingly utilize these materials. According to Huajing Intelligence, the global high-frequency high-speed copper clad laminate market size is projected to reach $2.63 billion in 2023, and is expected to reach $2.8 billion in 2024, with a year-on-year growth of approximately 8%.

As 5G networks expand and the number of smart driving vehicles increases, the high-frequency copper clad laminate industry will have even greater potential. According to Jianleshangbo (168Report), global sales of high-frequency copper clad laminates are expected to reach $554 million in 2024, and $810 million by 2031, with an average annual growth rate of 5.7% from 2025 to 2031.

06

Electronic Resin

Electronic resin is akin to a specialized “functional adhesive” in the electronics industry, meeting stringent requirements for purity, performance, and stability, primarily used for copper clad laminates, semiconductor packaging materials, PCB inks, electronic adhesives, etc., with the core functions of insulation and adhesion.

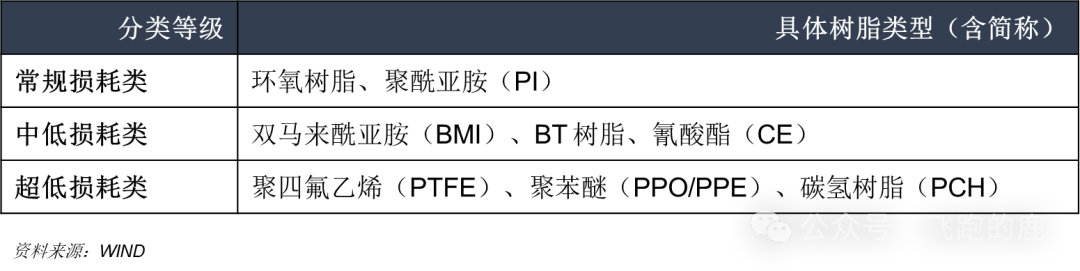

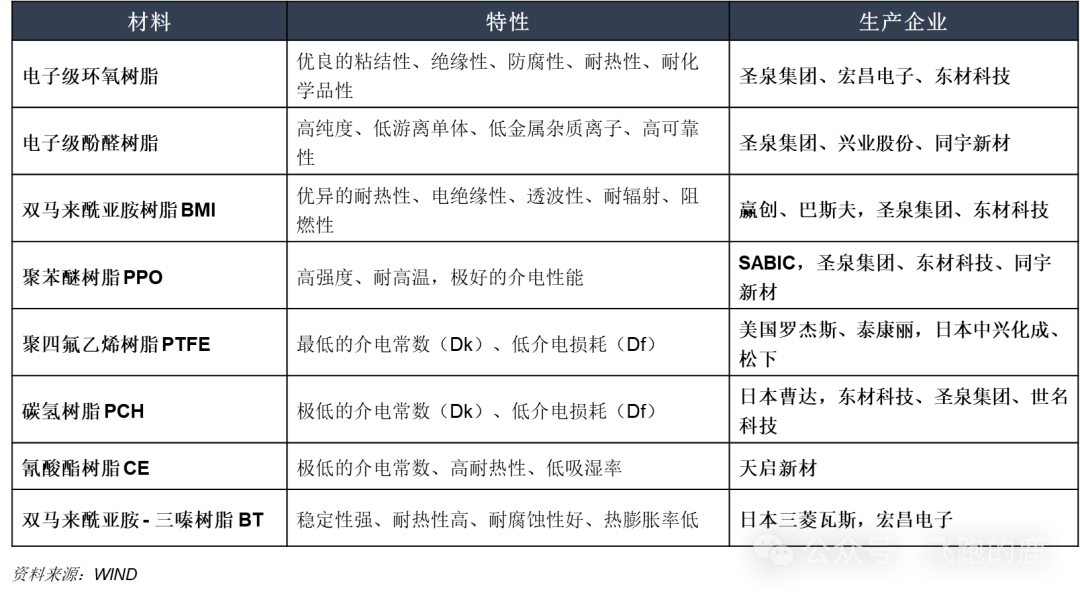

Among them, the electronic resin used for copper clad laminates is classified into three categories based on dielectric performance:

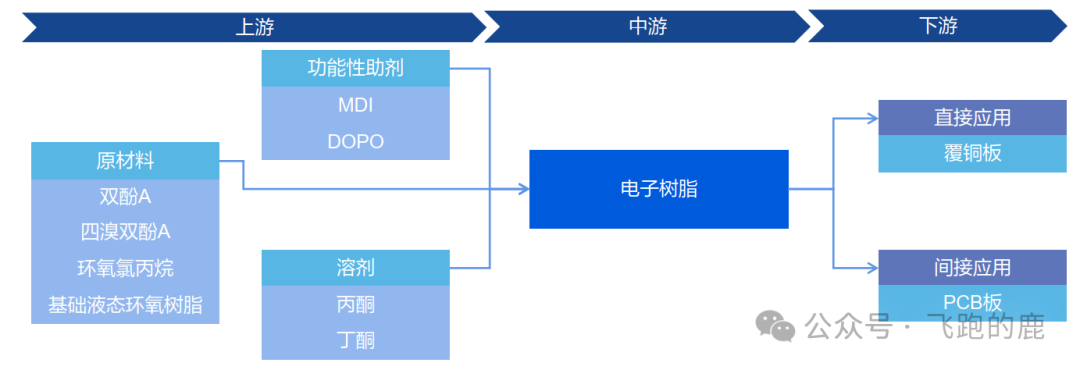

The electronic resin industry chain has clear divisions of labor: upstream includes raw materials such as bisphenol A, epoxy chloropropane, functional additives like MDI and DOPO, and solvents like acetone and butanone, responsible for “supply”; midstream involves the production and manufacturing of electronic resins, which is the “processing stage”; downstream connects with the copper clad laminate industry, indirectly supplying to PCBs, ultimately landing in terminal fields such as computers, consumer electronics, automotive electronics, and communication equipment.

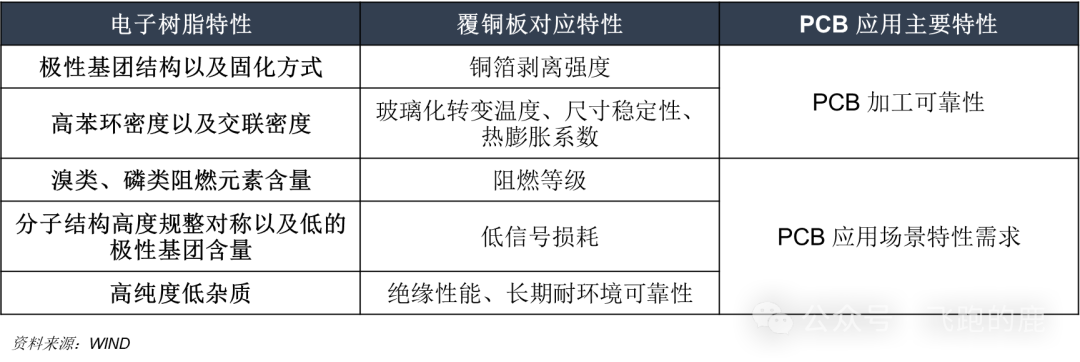

Electronic resin acts as a “characteristic regulator” for copper clad laminates—different resins can enhance different characteristics of copper clad laminates, and upgrades in copper clad laminate characteristics will further improve PCB performance. For example, the polarity group structure and curing method of the resin can affect the copper foil peel strength and interlayer adhesion of the copper clad laminate, making PCB processing more reliable; the more bromine and phosphorus flame-retardant elements in the resin, the higher the flame-retardant grade of the copper clad laminate; a more regular molecular structure and fewer polar groups in the resin can reduce signal loss in copper clad laminates, adapting to high-speed and high-frequency communication scenarios, meeting various application needs of PCBs.

Electronic-grade Epoxy Resin

Electronic-grade epoxy resin is one of the “core building materials” for high-performance copper clad laminates, with good mechanical properties, strong adhesion, high insulation, and heat resistance advantages, small shrinkage after curing, and not prone to cracking; special structures can also achieve low dielectric and intrinsic flame retardancy, meeting the needs for high-frequency signal transmission and high-speed information processing, widely used in next-generation servers, automotive electronics, communication networks, and other fields.

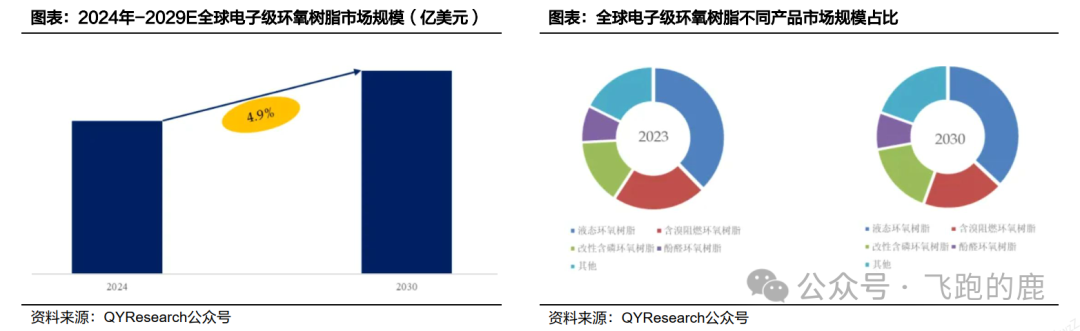

Demand for electronic-grade epoxy resin is expected to grow rapidly, with QYResearch estimating the global market size to be approximately $2.4 billion in 2024, expected to reach $3.22 billion by 2030, with a CAGR of 4.9% from 2024 to 2030.

Currently, the companies producing resins are listed as follows:

07

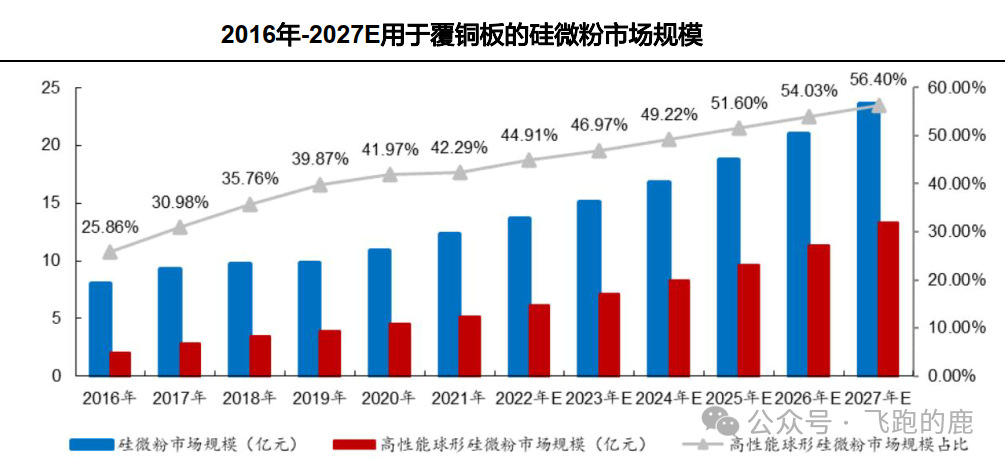

Silica Micro Powder

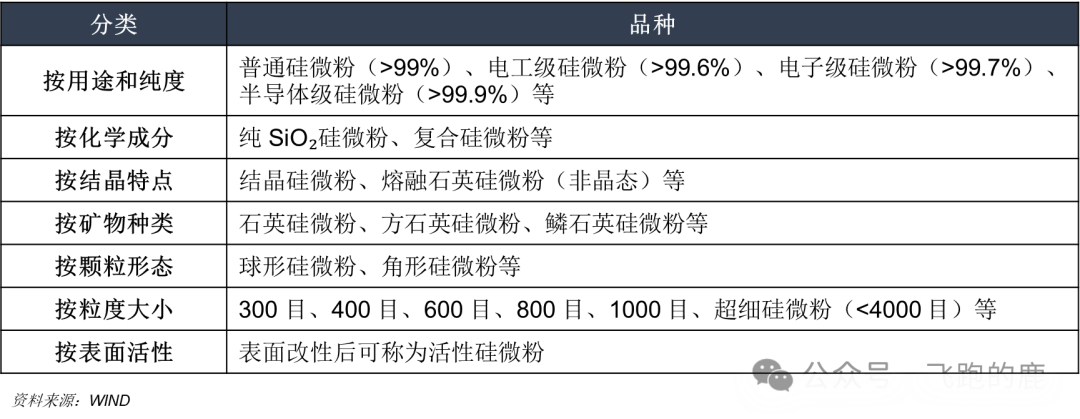

Silica micro powder is made from crystalline quartz and fused quartz as raw materials, processed through grinding, classification, impurity removal, and high-temperature spheroidization, belonging to non-toxic and odorless silica powder. It serves as a “high-performance functional filler” in the inorganic non-metallic field, with advantages of high heat resistance, high insulation, low expansion, and good thermal conductivity.

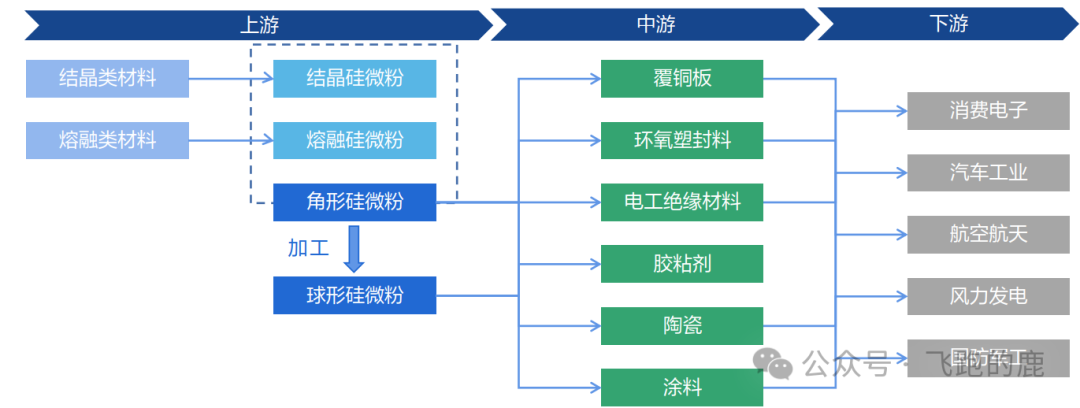

Silica micro powder is classified into angular and spherical types based on particle shape, widely used in copper clad laminates, chip epoxy encapsulants, insulating materials, adhesives, etc., with end applications in consumer electronics, automotive, aerospace, and wind power industries. Its industry chain is as follows:

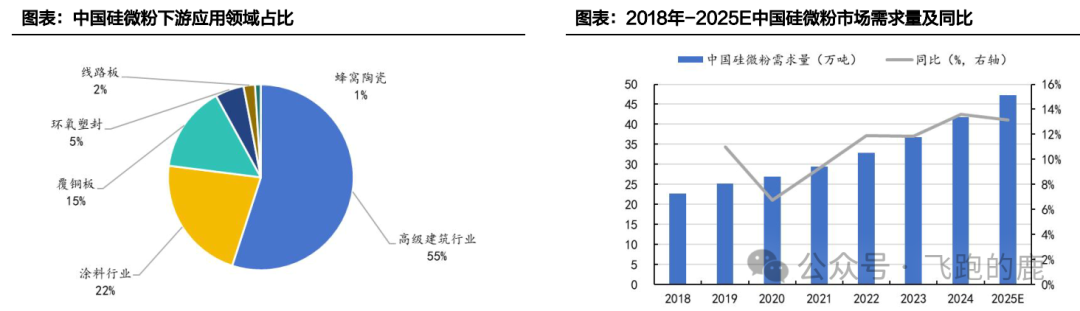

According to Huajing Intelligence, in the downstream applications of silica micro powder, advanced building materials account for 55.1%, coatings account for 21.7%, copper clad laminates account for 15.1%, and epoxy encapsulants account for 4.9%.

As the electronics industry advances towards high precision, the requirements for silica micro powder in copper clad laminates are increasing, driving market growth. According to Beizhesi Consulting, the demand for silica micro powder in China is expected to reach 418,000 tons in 2024, and 473,000 tons in 2025, with a year-on-year increase of 13.2%.

Among the inorganic functional powders used in copper clad laminates, silica micro powder has the widest application. For copper clad laminates that require dielectric properties and dielectric loss, modified silica micro powder that meets particle size and purity standards is selected—it can improve the expansion coefficient and thermal conductivity of PCBs, enhancing the reliability and heat dissipation of electronic products.

With the upgrade of terminal devices and the increase in AI server applications, the demand for silica micro powder in copper clad laminates will rise rapidly in the future.

08

Prepreg

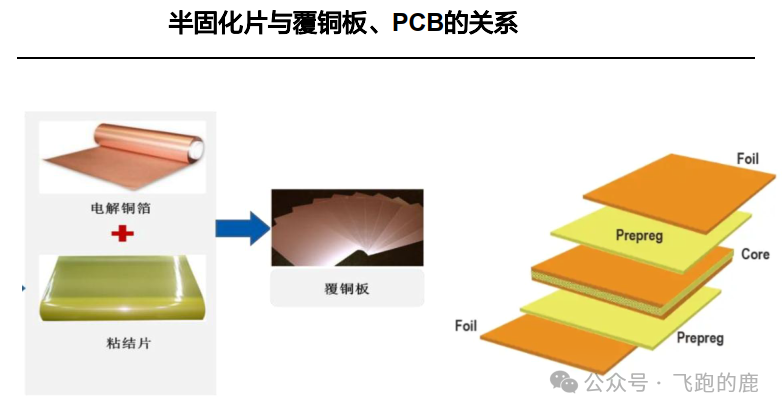

Prepreg (PP, also known as bonding sheet or adhesive film) serves as the “insulating interlayer” of PCBs—sandwiched between the core board and copper foil or between two core boards, it acts as a dielectric layer for insulation, primarily composed of glass fiber cloth, resin, and curing agents.

It is a precursor product of copper clad laminates, made by soaking glass fiber cloth in resin, which is then reacted to form a solid resin that is not fully cured; during the lamination process, the core board, PP, and copper foil are stacked according to design, and under heat and pressure, the resin in the PP bonds adjacent layers, ultimately curing and forming the final product.

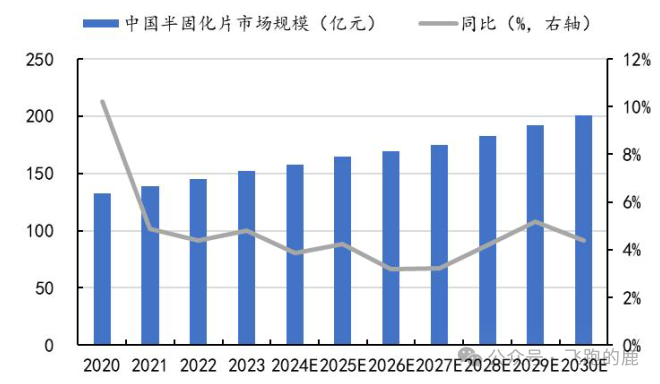

Demand growth driven by downstream industries such as AI, servers, and consumer electronics is leading to an upward trend in the prepreg market size. According to Zhiyan Consulting, the market size of prepregs in China was 15.192 billion yuan in 2023, and is expected to reach 20.044 billion yuan by 2030, with a CAGR of 4.0% from 2023 to 2030.

09

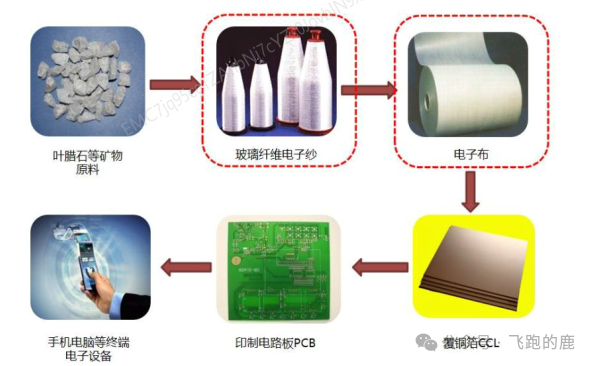

Electronic-Grade Glass Fiber Cloth

Electronic-grade glass fiber cloth (referred to as electronic-grade glass fiber) serves as the “insulating skeleton” of copper clad laminates—woven from electronic-grade glass yarn with a single filament diameter of less than 9μm, primarily used as an insulation reinforcement material for copper clad laminates, ultimately applied in various terminal electronic products.

Electronic-grade glass fiber cloth has high technical and financial barriers, with strong value creation capabilities across the entire industry chain, enabling substrates to possess excellent electrical properties and mechanical strength. The booming development of global 5G and consumer electronics markets is driving the copper clad laminate and PCB industries towards a broad prospect, which will also boost the growth of the electronic-grade glass fiber industry.

10

Conclusion

PCBs are the “core framework” of electronic devices, and in 2024, the explosive demand from AI + downstream consumer electronics/5G/servers is expected to drive industry prosperity, with both volume and price likely to rise. HDI and 18+ layer multilayer boards will benefit, with Prismark predicting a CAGR of 6.4% and 15.7% for global output value from 2024 to 2029, respectively.

Copper clad laminates are the core substrate of PCBs, evolving towards high-frequency and high-speed applications, with copper foil, resin, and glass fiber cloth as key raw materials; according to Zhongshang Intelligence (2025/05), they account for approximately 27% of PCB costs, with high growth in AI/5G demand.

Electronic resins influence the performance of copper clad laminates,with AI driving upgrades, and domestic efforts promoting local alternatives, with PTFE resin likely becoming a trend.

Silica micro powder is used in copper clad laminates, with downstream upgrades and AI servers driving demand;Beizhesi Consulting predicts a demand of 473,000 tons in China by 2025 (up 13.2% year-on-year).

Copyright Notice: Some articles were unable to contact the original authors during the push. If there are copyright issues, please contact us.