0 Introduction

With the acceleration and deepening of the digital, networked, and intelligent transformation of the manufacturing industry, the strategic significance of industrial software has become increasingly prominent. During the “14th Five-Year Plan” period, the Ministry of Industry and Information Technology added industrial basic software to the traditional industrial “four basics” of key basic materials, basic components (parts), advanced basic industries, and industrial technology foundation, forming the “new five basics” of industrial foundation reconstruction. Therefore, it is necessary to grasp the characteristics and development trends of industrial software, assess the competitive landscape of the industrial software market, and find opportunities and paths for the development of industrial software in China.

1 Classification and Characteristics of Industrial Software

1.1 Classification of Industrial Software

Industrial software provides critical support for intelligent manufacturing and can be said to be the “brain” and “soul” of modern industry. Industrial software is the product of the softwareization of industrial technology, essentially encapsulating and solidifying industrial technology and experiential knowledge in the form of software tools to solve specific problems in industrial scenarios.

The Ministry of Industry and Information Technology classifies industrial software into product R&D design software, production control software, and business management software in the “Statistical Survey System for Software and Information Technology Services Industry”. Among them, product R&D design software is used to enhance enterprises’ capabilities and efficiency in product R&D, including 3D virtual simulation systems, Computer-Aided Design (CAD), Computer-Aided Engineering (CAE), and Computer-Aided Manufacturing (CAM); production control software is used to improve the level of control during manufacturing processes and enhance the efficiency and utilization of production equipment, including industrial control systems, Manufacturing Execution Systems (MES), and Advanced Process Control (APC) systems; business management software is used to improve enterprises’ management governance levels and operational efficiency, including Enterprise Resource Planning (ERP), Supply Chain Management (SCM), and Customer Relationship Management (CRM).

1.2 Characteristics of Industrial Software

Industrial software empowers industrial transformation and upgrading. On one hand, industrial software transforms production methods through digital means, promoting productivity and efficiency improvements, serving as a key element supporting the conversion of old and new industrial drivers; on the other hand, industrial software solidifies and transmits knowledge and experience scattered in the minds of technical personnel, greatly promoting the reuse and reconstruction of industrial technical knowledge, thus strengthening the foundation of industrial production. Industrial software has characteristics that differ from general application software.

1.2.1 High Technical Barriers, Requiring Extensive Knowledge and Experience

Industrial software has a high degree of technical complexity. Key core algorithms such as geometric modeling engines and constraint solvers are extremely challenging, and model optimization requires a vast amount of production and operational data as a foundation, all built on long-term practice and accumulation. Rendering components and human-computer interaction technologies also significantly impact the usability of industrial software. Furthermore, developing industrial software requires not only software skills but also specialized knowledge from numerous disciplines such as mathematics, physics, and mechanical engineering, along with a deep understanding of manufacturing processes and industrial mechanisms. These factors create technical barriers in the field of industrial software.

1.2.2 Industrial Software is Rooted in the Actual Needs of the Industrial Sector, Requiring Deep Interaction with Industrial Enterprises

Industrial software is an application-driven product closely linked to industrial enterprises. During the deep application of industrial software, industrial enterprises provide improvement suggestions regarding its functions and mechanisms, assisting in the rapid optimization and iteration of industrial software, thereby better supporting industrial production and operations. The development of industrial technology and the growth of industrial software are mutually reinforcing, and a sound interaction mechanism between industrial software enterprises and industrial enterprises is the foundation for a win-win situation.

1.2.3 Long R&D Cycles and High Investment in Industrial Software

R&D of industrial software requires knowledge from multiple fields and has high reliability requirements; the system is much more complex than general application software, making R&D difficult, with long cycles and slow version iterations. It is estimated that the R&D cycle for general large-scale industrial software takes 3-5 years, and gaining market recognition takes about 10 years. Additionally, industrial software enterprises require significant R&D investment. In fiscal year 2020, leading global Computer-Aided Engineering (CAE) company ANSYS invested $355 million in R&D, accounting for 21.1% of its revenue; leading Electronic Design Automation (EDA) company Synopsys invested $1.279 billion in R&D, accounting for 34.7% of its revenue.

1.2.4 Low Generality of Industrial Software and Limited Economies of Scale

Industrial software customers come from diverse industries with varied needs, making it difficult to solve all problems with standardized products; often, customization or secondary development for different industrial scenarios is required. Specialized industrial software usually applies to a specific sub-industry or situation, lacking universality, with limited market space and difficulty in achieving economies of scale. Some industrial giants develop their own “in-house” software based on project needs, which is not commercially promoted. For example, Boeing’s entire 787 development process utilized over 8,000 types of software, of which fewer than 1,000 are common commercial software, while the remaining 7,000-plus are proprietary software developed by Boeing over years of experience.

2 New Trends in Industrial Software Development

The rise of new technologies such as cloud computing and artificial intelligence has brought continuous innovation and reconstruction to industrial software, ushering it into a new era of technological transformation, with new trends emerging in products, development, deployment, and business models.

2.1 In Product Models, Industrial Software is Shifting from Isolated Products to Integrated and Unified Solutions

Industrial software companies are enhancing collaboration between strongly related software products through integration, providing customers with comprehensive integrated solutions for the entire process, effectively increasing customer stickiness, expanding brand effects, and improving efficiency across the entire value chain of manufacturing. The integration of CAD, CAE, and CAM aids enterprises in advancing design-manufacturing simulation integration, optimizing production processes; the integration of ERP, SCM, and CRM can help enterprises improve management levels and reduce operational costs. Additionally, industrial software is evolving towards lightweight solutions, with some large industrial software rapidly deconstructing, leading to the emergence of new architectural industrial software like industrial apps.

2.2 In Development Models, Industrial Software Development is Gradually Shifting Towards Componentized and Modular Approaches

The “loosely coupled” microservices architecture helps industrial software companies achieve agile development and flexible maintenance through application and function segmentation. The development environment for industrial software is becoming more open-source and collaborative, laying the groundwork for software function expansion and secondary development. Relying on cloud platforms, various stakeholders in the industrial chain can participate in the development process, enabling collaborative development of industrial software. Furthermore, the maturity of low-code development technology is expected to lower the development threshold for industrial software, allowing many enterprises, particularly small and medium-sized enterprises, to join the development and application of industrial software, facilitating their digital transformation.

2.3 In Deployment Models, Industrial Software is Accelerating its Migration to the Cloud

Industrial software is transitioning from initial deployment within enterprises to being deployed, updated, and maintained on private clouds, public clouds, or hybrid clouds. This deployment model significantly reduces infrastructure investment and operational costs for industrial enterprises, lowering the barriers for digital transformation. Especially for enterprise customers with multiple production locations, local deployment cannot achieve data interconnectivity; cloud-deployed industrial software can help enterprises aggregate, process, and share data from multiple locations, meeting their rigid demands. At the same time, cloud transformation allows industrial software companies to more conveniently provide update and maintenance services to customers, optimizing customer experience and enhancing customer loyalty.

2.4 In Business Models, the Migration of Industrial Software to the Cloud Drives a Shift from One-Time Purchases to Subscription Models

The subscription model opens a new win-win situation for industrial enterprises and industrial software companies. On one hand, industrial enterprises convert large one-time capital expenditures into long-term subscription expenses, alleviating cash flow pressures. On the other hand, the income of industrial software companies becomes more sustainable, promoting steady development; if customers subscribe for a longer period, subscription income will exceed that of one-time purchases. Under the subscription model, more customers, especially small and medium-sized enterprise customers, can afford industrial software, helping them better cope with competition from cheaper alternatives. The subscription model also increases the flexibility of enterprises’ pricing strategies, such as pricing by function or usage time, providing more possibilities for business expansion.

3 Competitive Landscape of the Industrial Software Market

3.1 Global Market Competitive Landscape

Currently, the global industrial software industry has formed a relatively stable market structure, with stable growth in industry scale. In 2020, the global industry scale was estimated at $435.8 billion, with a compound annual growth rate of approximately 5.3% from 2015 to 2020 (as shown in Figure 1).

Figure 1 Global Industrial Software Industry Scale and Growth Rate from 2012 to 2020

Source: China Industrial Technology Software Alliance

Leading enterprises in various sub-sectors have formed relatively solid competitive barriers. In the field of product R&D design software, European and American giants have essentially formed a monopoly, with CAD design software dominated by Autodesk, PTC, Dassault Systèmes, and Siemens, while CAE simulation software is almost monopolized by ANSYS, ALTAIR, and NASTRAN, and EDA chip design software is led by the three giants Synopsys, Cadence, and Mentor Graphics (acquired by Siemens in 2016). In the field of production control software, traditional industrial giants hold a leading advantage, with Siemens, Schneider, and Rockwell being industry leaders. In the field of business management software, products are relatively mature, and market competition is more intense, with market concentration significantly lower than the other two types of industrial software, led by SAP and Oracle, with Workday, Infor, and Sage in the second tier.

In the short term, it is difficult for industrial software giants to be caught up or surpassed. On one hand, large leading enterprises are accelerating acquisition steps, continuously expanding product lines, building product ecosystems, and creating a comprehensive integrated product system from R&D design to production control to business management, which increases customer dependence. On the other hand, giant enterprises hold proprietary core technology intellectual property and continue to invest massive R&D funds each year, raising the entry barriers for the entire industry.

3.2 Competitive Landscape of the Chinese Market

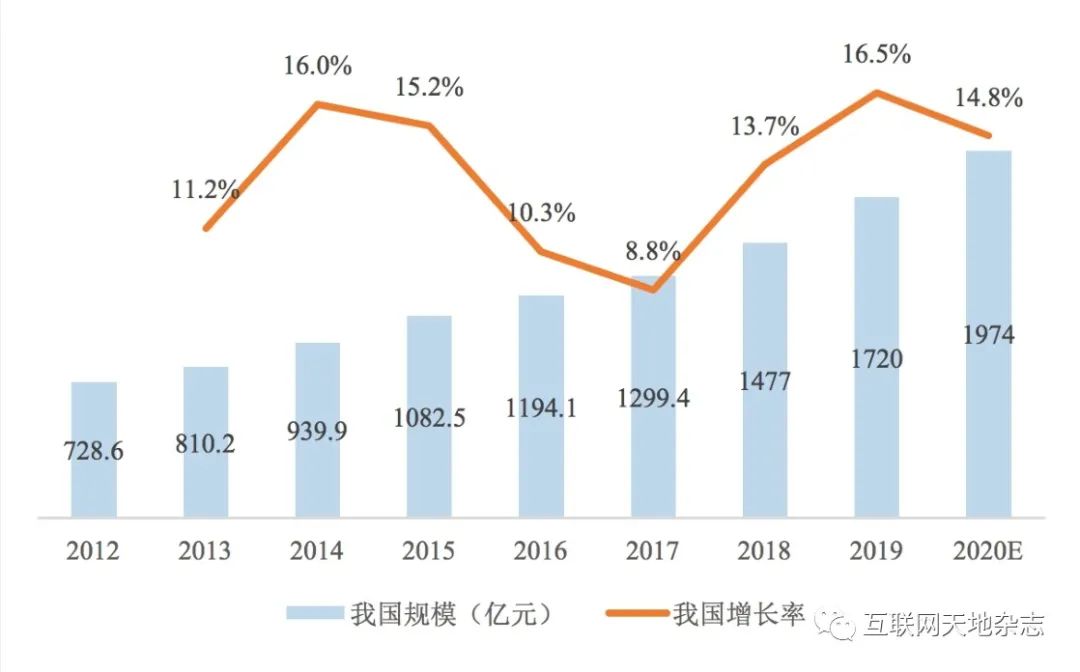

In recent years, China’s industrial software market has developed rapidly, with domestic suppliers’ competitiveness improving, and domestically controllable industrial software products continuously emerging. The industry scale has grown significantly faster than the global average. In 2020, China’s industry scale was estimated at 197.4 billion yuan, with a compound annual growth rate of approximately 12.8% from 2015 to 2020 (as shown in Figure 2).

Figure 2 China’s Industrial Software Industry Scale and Growth Rate from 2012 to 2020

Source: China Industrial Technology Software Alliance

However, it is also important to note that the scale of China’s industrial software industry is highly mismatched with its industrial scale. China has formed an independent and complete modern industrial system and is the only country in the world that has all industrial categories listed in the United Nations industrial classification. According to World Bank data, in 2020, China’s industrial added value accounted for about 25% of the global total, while the scale of the industrial software industry accounted for only about 7% of the global total.

Technologically, although there have been some breakthrough advancements in certain technologies in China’s industrial software products, a large number of key core technologies remain missing, especially in product R&D design software, where the core is highly dependent on imports and primarily targets the mid-to-low-end market for secondary development. In terms of industry, there is a disconnect between industrial software enterprises and industrial enterprises, and the industrial chain is immature. Industrial enterprises believe that domestic industrial software cannot meet production needs and are unwilling to use it, while domestic industrial software products cannot be iterated and optimized in actual usage scenarios, making it even more challenging to provide support for industrial enterprises.

Currently, China’s industrial software market generally exhibits characteristics of “strong management software, weak engineering software, many low-end software, and few high-end software”.

In the field of product R&D design software, except for a few vertical fields such as military and aerospace, high-end R&D design software is a major pain point for China’s industrial digital transformation, with software algorithms, mechanisms, and performance becoming “bottleneck” issues. Domestic software products have simple industrial mechanism models and weak support capabilities for advanced processes, failing to meet the complex scenario demands of high-end customers. Currently, the vast majority of R&D design software in China relies on imports, with over 90% of market share in domestic sub-markets such as CAD, CAE, and EDA occupied by leading European and American enterprises.

In the field of production control software, domestic suppliers have limited capability to encapsulate complex production processes and industrial mechanisms into software products, primarily meeting the needs of specific links in the production chain and unable to provide comprehensive, systematic, one-stop solutions. International giants still hold significant competitive advantages in the domestic market, but in certain vertical industries such as steel metallurgy and petrochemicals, companies like Baoxin Software and Petrochemical Yingke have been deeply cultivating the market and are gradually entering the high-end market.

In the field of business management software, China already has relatively mature software products, with the competitive landscape of traditional software such as ERP being relatively stable, with domestic suppliers like Yonyou and Kingdee occupying the main market, especially in the small and medium-sized enterprise user market. However, high-end users still primarily use foreign products, and the majority of domestic suppliers’ customers are distributed in mainland China, making it difficult to compete with international giants in terms of product and technology exports.

4 Opportunities for Development of China’s Industrial Software Industry

Currently, China’s industrial software industry is entering an important strategic opportunity period.

First, the ongoing technology blockade by the United States against China’s high-tech industries has intensified, with multiple Chinese companies and institutions being placed on the “entity list”. R&D software represented by EDA and engineering software represented by MATLAB have been banned, and the external pressures brought by China-U.S. trade friction are forcing the accelerated localization of industrial software, making it imperative to build a domestic industrial software industry system that is controllable, secure, and reliable.

Second, the national level is highly concerned, with several policies released in recent years to support the development of domestic industrial software. In August 2020, the State Council issued “Several Policies for Promoting High-Quality Development of the Integrated Circuit Industry and Software Industry in the New Era”, requiring a focus on the R&D of key core technologies for integrated circuit design tools, basic software, industrial software, and application software. In July 2021, six ministries, including the Ministry of Industry and Information Technology and the Ministry of Science and Technology, jointly issued the “Guiding Opinions on Accelerating the Cultivation and Development of High-Quality Manufacturing Enterprises”, requiring the promotion of industrial digital development and vigorously promoting the application of controllable industrial software to improve the softwareization level of enterprises.

Additionally, China is transitioning from a “manufacturing power” to an “intelligent manufacturing strong country”, with the digital, networked, and intelligent transformation and upgrading of industries continuously accelerating. The demand for technological empowerment from industrial enterprises is urgent, and the COVID-19 pandemic has accelerated the transformation of industrial production methods. As a new driving force for economic growth, industrial software and other new-generation information technologies have broad market space.

Finally, the migration of industrial software to the cloud has become an inevitable trend, requiring the reconstruction of the overall architecture of previously standalone products. The development of lightweight products such as industrial apps is also based on the decoupling of traditional large industrial software. These significant adjustments and changes faced by industrial software products have, to some extent, weakened the competitive advantages built by overseas giants, providing valuable opportunities for domestic suppliers to accelerate catch-up or even overtaking.

5 Conclusion

After assessing the technological trends and market structure of industrial software, this article attempts to propose the main line of development for China’s industrial software industry in the coming years—deeply promoting the structural reform of the supply side of industrial software, cultivating leading suppliers, and building core competitiveness in the industry.

At the government level, central and national agencies should establish feasible long-term overall planning to guide the development of the industrial software industry. Local governments should actively utilize policy tools to implement central planning based on local development realities, fully mobilizing enterprise enthusiasm and continuously providing good policy and institutional guarantees.

At the level of industrial software enterprises, on one hand, they should firmly innovate independently, increase R&D investment, deeply study industrial mechanism models, strengthen communication and cooperation with demand parties, establish rapid iteration and optimization mechanisms, and provide high-quality industrial software products to establish competitive advantages; on the other hand, they should extend enterprise layouts, attempt to achieve technological supplementation or market expansion through mergers and acquisitions of quality targets, and effectively integrate with their own products and businesses to enhance their strength.

At the level of universities, alliances, and other social institutions, there should be an emphasis on the systematic cultivation of industrial software talents to reserve quality labor resources for the market; accelerate the transformation of scientific research achievements, support the industrialization of emerging technologies; promote the integration of production and research and the docking of supply and demand, cultivating a good industrial ecosystem.

References:

[1] China Industrial Technology Software Alliance. White Paper on China’s Industrial Software Industry (2020) [R]. 2021.5.

[2] Ning Zhenbo. Building the Foundation of Industry and Recasting the Soul of Intelligent Manufacturing [J]. Software Guide, 2021, 20(01): 1-5+261.

[3] Tao Zhuo, Huang Weidong. Research on the Development Path of China’s Industrial Software Industry [J]. Research on Technology Economics and Management, 2021(04): 78-82.

[4] Dong Hao, Deng Changyi. Promoting the Development of Independent Industrial Software through Diversified Investment [J]. China Science and Technology Forum, 2020(09): 13-15.

[5] Zhou Fanli. Innovative Breakthroughs in the Bottlenecks of Industrial Software Development [J]. China Industry and Information Technology, 2020(03): 28-34.

[6] Xu Heng, Wu Lilin. Development and Countermeasure Suggestions for Industrial Software Enterprises—Based on R&D Design Software Development [J]. Industrial Technology Innovation, 2019, 06(01): 99-102+106.

This article was published in the “Internet World” August 2021 issue, authors: Yun Mengyan, Jia Fei, Institution: China Academy of Information and Communications Technology Data Research Center

Submission Email: [email protected]

Cover Inquiry: 010-66049047