Nvidia’s $5 billion investment in Intel has sparked extensive discussions within the chip industry. Some have shared the cover of Wired magazine from July 2002, featuring Jensen Huang, with his full head of black hair and dressed in black, exuding determination. At that time, he wasn’t wearing a leather jacket, and Nvidia’s market value was only a fraction of Intel’s. The cover story was titled ‘The Next Intel – How Nvidia is Changing the Chip Industry with GPUs.’

In response, some poetically commented: Twenty years ago, Nvidia chased the shadow of Intel’s dominance;

At this moment, Nvidia has given the ‘king’ a new weight. (Two decades ago, Nvidia chased Intel’s crown. Today, Nvidia is helping redefine it.)

Some have calculated: If you had invested the $3.3 spent on this magazine into Nvidia’s stock back then, it would now be worth $150,000.

This title seems prophetic; Nvidia has created a new market with GPUs – the AI data center, where Nvidia has become the leader, while Intel has gained almost nothing. Although Intel faces pressure from AMD, its foundation in the x86 market remains, but these markets have stabilized for many years. No matter how much they refine their offerings in these areas, maintaining their current share would be considered a success, and significant growth is unlikely, especially with the onslaught of non-x86 architecture AI PCs.

Thus, it truly is a case of thirty years east of the river, thirty years west of the river. Around the year 2000, it was nearly impossible for chip design companies to defeat Intel, as Intel’s advantage in the x86 market was unparalleled; competitors were virtually invisible even with a telescope. This year, several chip design companies have surpassed Intel in market value, and most did not do so by defeating Intel in the x86 market but by carving out their own independent development paths.

Currently, we also see little possibility of surpassing TSMC in advanced processes. According to Yole’s data, the process used by HiSilicon will be equivalent to 5nm by 2026, which is about four years behind TSMC’s most advanced technology.

However, as the industry continues to fragment, more chip design companies will have to adopt local processes to mitigate policy risks, allowing our own advanced processes to gradually mature. Coupled with the optimization capabilities of complete machines and systems, it is highly likely that a new advanced manufacturing process suitable for local chip companies will develop. Of course, this may take a long time, and currently, we are likely in the most challenging phase of being constrained by advanced processes.

Appendix: Two other noteworthy industry updates

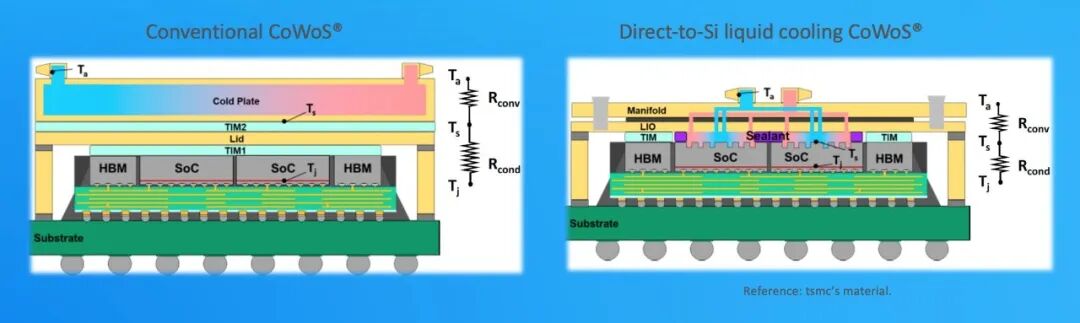

1. TSMC has launched liquid cooling CoWoS packaging. In the context of high power consumption in large chips, heat dissipation has become one of the hot technologies. This technology brings liquid cooling to CoWoS-level packaging, bringing it closer to the chip.

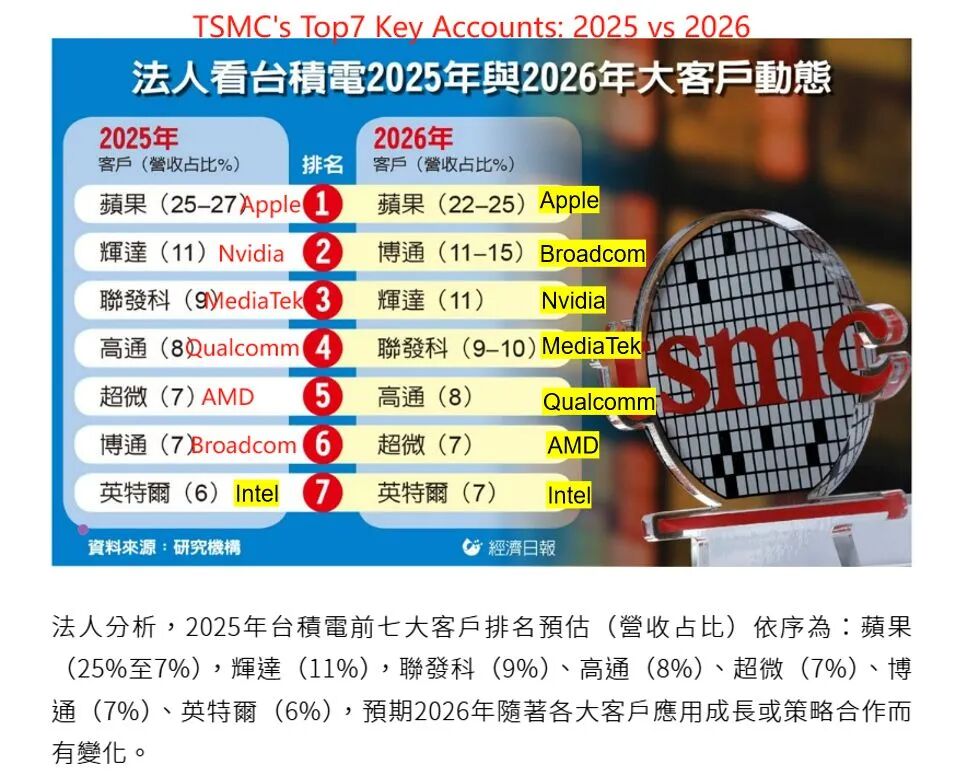

2. TSMC’s top seven customers. Broadcom is expected to see the highest share growth by 2026, surpassing Nvidia. This forecast indicates a positive market outlook for ASIC customization in interconnect chips.