1. Industry Background

1. Industry Background

(1) Basic Situation

In recent years, both national and local governments have placed great emphasis on the development of the electronic information industry, implementing a series of industry standards and policies aimed at optimizing the policy and institutional environment for industrial development, encouraging the deep integration of smart manufacturing and industrial internet, and promoting significant progress in digitalization, informatization, and intelligence in the manufacturing sector, which has brought new development opportunities to the electronic information industry.

The electronics industry, as a vital pillar of the national economy, plays a key role in promoting technological innovation, improving production efficiency, and enhancing the quality of life for the people. It has now become an important driving force for economic growth and social progress.

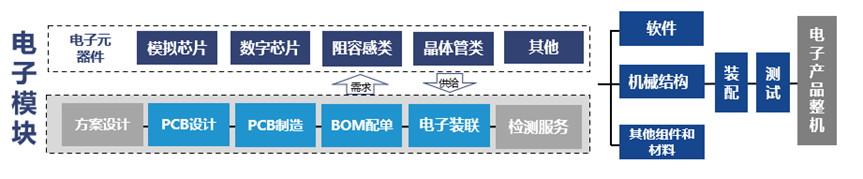

Electronic products, as the specific product form of the electronics industry, can typically be viewed as composed of multiple electronic modules, mechanical structures, software, and other components and materials. Among these, electronic modules are circuits that can operate independently, consisting of one or more devices, usually with specific functions. They are crucial components of electronic products, and their performance directly affects the quality and usability of the entire electronic product.

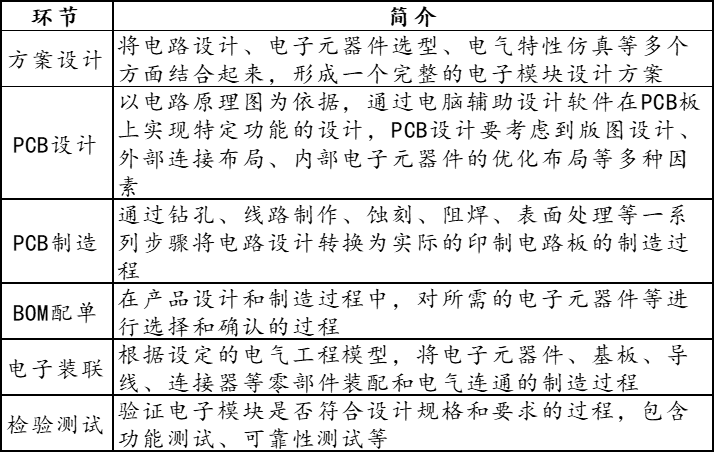

The manufacturing of electronic modules typically requires several stages, including scheme design, PCB design, PCB manufacturing, BOM allocation, electronic assembly, and inspection testing. An overview of each stage is as follows:

(2) Characteristics

1. Broad Scope of Technology Involvement

From the perspective of industry division, the electronics industry encompasses multiple subfields, including software development, PCB manufacturing, electronic component trading, PCBA processing, and mechanical manufacturing. In terms of application scenarios, the downstream of the electronics industry covers various sectors such as consumer electronics, communications, industrial control, medical, and aerospace. Each field has unique technical and process requirements, necessitating that one-stop service providers possess interdisciplinary and diversified technical service capabilities.

2. High Requirements for Technological Innovation and Upgrades

With the rapid iteration of electronic products and the continuous upgrading of customer demands, the professionalism, complexity, and comprehensiveness of the one-stop service model in the electronics industry are increasingly enhanced. Firstly, the product update cycle of electronic products is continuously shortening, with increasing demands for performance, integration, and structural complexity, driving upstream material suppliers and service providers to continuously upgrade their technologies, products, and services. Secondly, the demands of downstream application fields are constantly changing, with new market hotspots emerging, placing high demands on the rapid response capabilities and technological innovation iteration capabilities of one-stop service providers in the electronics industry.

3. High Requirements for Stability in Technology and Processes

The supply of materials and services upstream of electronic products has the characteristic of “a single thread affecting the whole body”; any issues with a particular material or service may lead to failures or performance impacts on the entire product. Therefore, one-stop service providers in the electronics industry must possess stable and reliable production processes and technologies to meet customer requirements for products and services at all stages.

2. Overview of the Printed Circuit Board (PCB) Industry

(1) Industry Introduction

The Printed Circuit Board (PCB), also known as a printed wiring board or printed circuit board, primarily functions to connect various electronic components through circuits, serving as a conductor and transmission medium. It is a key electronic interconnection component of electronic products. The vast majority of electronic devices require printed circuit boards to provide the mechanical support necessary for assembling electronic components, achieving wiring and electrical connections or electrical insulation, and providing the required electrical characteristics. The quality of its manufacturing directly affects the stability and lifespan of electronic products, as well as the overall functionality and market competitiveness of system products, earning it the title of “mother of electronic products.” As an indispensable component of electronic terminal devices, the development level of the printed circuit board industry reflects, to some extent, the speed and technological level of the electronic information industry in a given country or region.

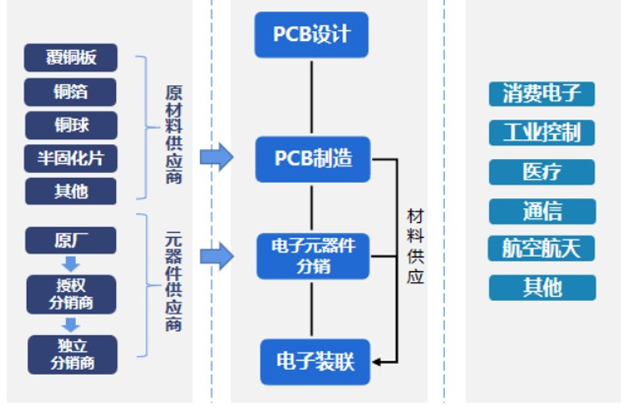

(2) Industry Chain Situation

The upstream of the industry mainly includes suppliers of raw materials used in the PCB production process and suppliers of electronic components. The downstream application fields are extensive, covering consumer electronics, industrial control, automotive electronics, communication equipment, aerospace, and many other sectors, encompassing most national economic industries.

(3) Industry Development Overview

1. Global Market Overview

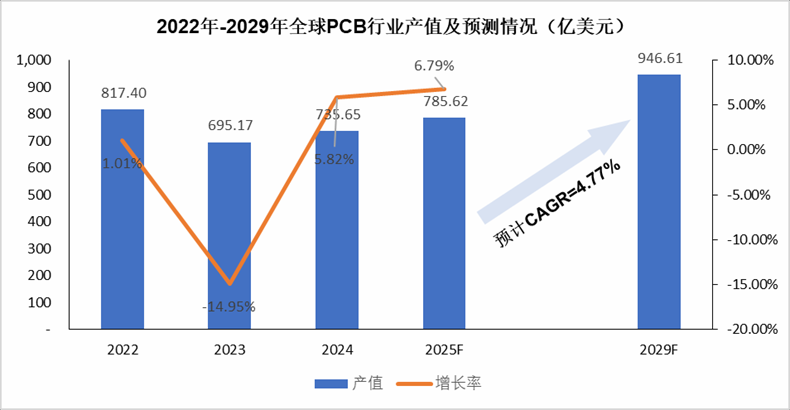

Against the backdrop of accelerated development in cloud technology, 5G technology, big data, integrated circuits, artificial intelligence, information technology, industrial 4.0, and the Internet of Things, the global PCB industry has seen steady growth in output value. According to statistics from Prismark, in 2023, influenced by macroeconomic fluctuations, the global PCB industry output value decreased by 14.95%, reaching 69.517 billion USD. In 2024, the global PCB industry output value is expected to rebound to 73.565 billion USD, with a growth rate of 5.82%.

In the future, with the vigorous development of downstream application fields such as new energy vehicles, AI, cloud computing, the Internet of Things, smart homes, and wearable devices, the PCB industry is expected to usher in a new round of development cycle. According to predictions from Prismark, by 2029, the global PCB industry output value will reach approximately 94.661 billion USD, with a compound annual growth rate of about 4.77% from 2025 to 2029.

According to statistics from Prismark, the output value proportions of mass-produced boards, small-batch boards, and prototypes in the PCB market are approximately 80%-85%, 10%-15%, and 5%, respectively. Based on this estimate, the global small-batch board market size in 2024 is expected to be around 7.357 billion to 11.035 billion USD, and by 2029, the market size is expected to reach 9.466 billion to 14.199 billion USD. The global prototype market size in 2024 is expected to be around 3.678 billion USD, with an expected market size of 4.733 billion USD by 2029.

2. Domestic Market Overview

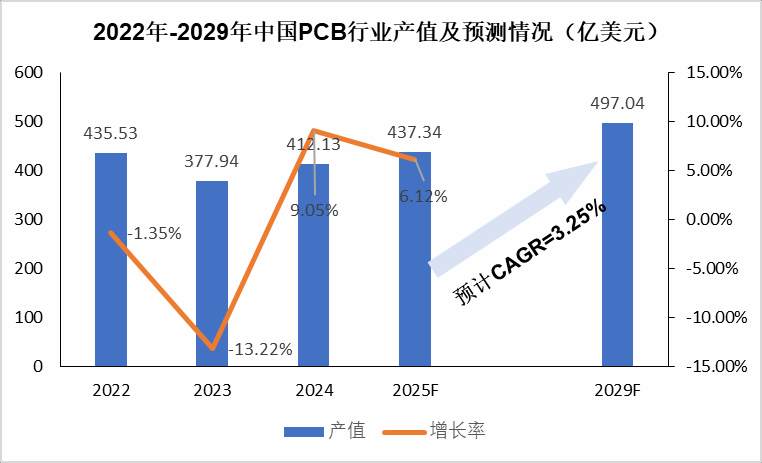

Benefiting from the continuous development of China’s electronic information industry and the global transfer of PCB production capacity, the overall trend of China’s PCB industry has shown rapid development. In 2006, China’s PCB output value surpassed that of Japan, becoming the world’s largest PCB manufacturing base. In 2023, affected by macroeconomic fluctuations, the output value of PCB in mainland China is expected to decrease by 13.22% to 37.794 billion USD. In 2024, the output value of PCB in China is expected to rebound to 41.213 billion USD, with a growth rate of 9.05%.By 2029, the output value of PCB in mainland China is expected to reach 49.704 billion USD, with a compound annual growth rate of 3.25%.

According to estimates from Prismark, in 2024, the market size of small-batch boards in China is expected to be around 4.121 billion to 6.182 billion USD, and by 2029, it is expected to reach 4.970 billion to 7.456 billion USD. The prototype industry in China is expected to have a market size of around 2.061 billion USD in 2024, with an expected market size of 2.485 billion USD by 2028.

3. Prototypes and Small-Batch Market

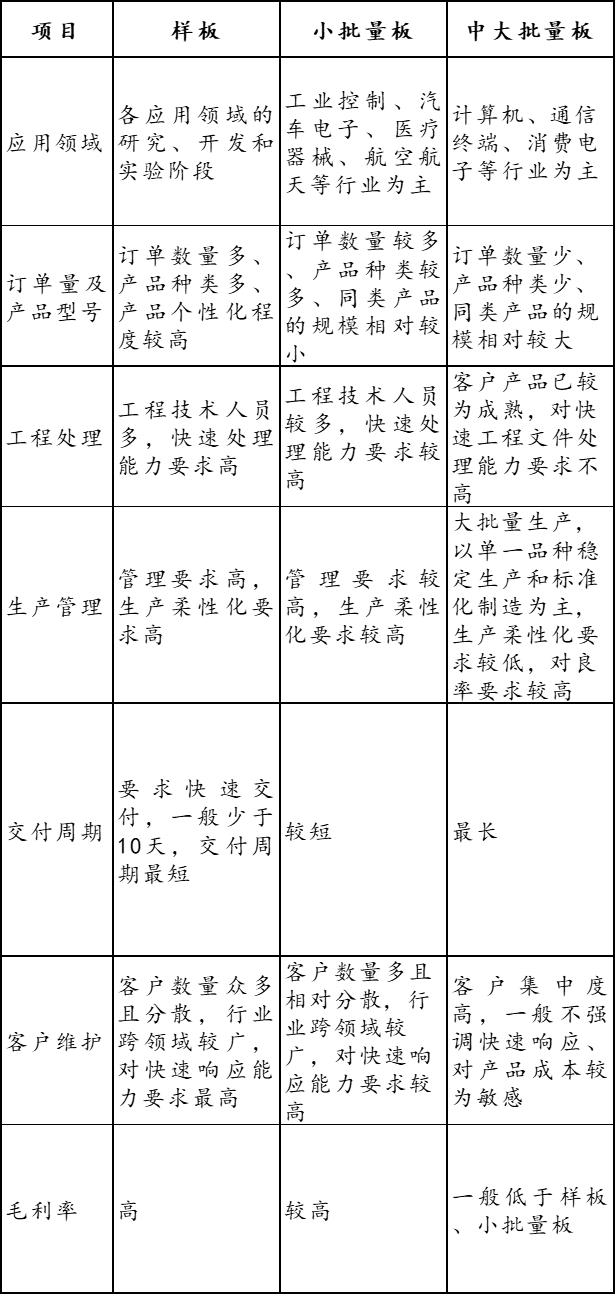

(1) Significant Differences Between Prototypes, Small-Batch Boards, and Mass Production Boards

Prototypes, small-batch boards, and mass production boards differ in application fields, order quantities, product models, project handling, production management, delivery cycles, customer maintenance, and gross margins, as detailed below:

Orders for prototypes and small-batch boards are characterized by “small quantities, diversification, and fast delivery,” which places extremely high demands on the planning, implementation, control, and management of production. Companies need to possess flexible production capabilities, efficiently organize the collaboration between production factors, and quickly respond to diverse customer needs. Prototypes and small-batch boards have high similarities in order quantities, production management, and customer maintenance, and PCB companies focusing on prototypes typically have the capability to also undertake small-batch board orders. In contrast, mass production board orders can achieve scale production by increasing automation levels, focusing more on their capacity, yield, and cost control factors.

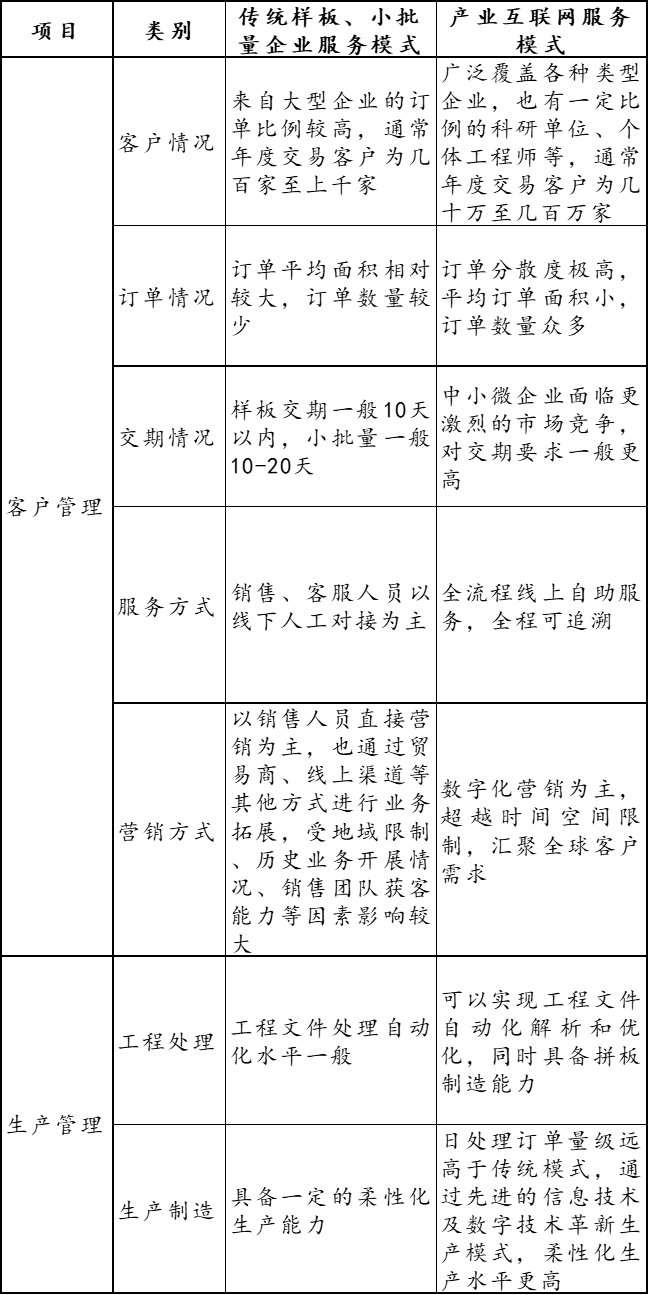

(2) The Rise of the Industrial Internet Model

The electronics industry is witnessing a surge in personalized demands from small and medium-sized enterprises, research institutions, and individual engineers. However, the service models and capabilities of traditional prototype and small-batch enterprises can no longer meet the customer demands in the new business landscape. With the development of information and digital technologies, some prototype and small-batch enterprises in the industry have begun to undergo information and digital upgrades, giving rise to the PCB industrial internet service model, which deeply integrates new generation information technology with traditional manufacturing models, providing smarter and more flexible solutions for prototype and small-batch board customers.

The differences between traditional prototype and small-batch enterprise service models and the industrial internet service model are illustrated below:

(4) Industry Competitive Landscape

1. Competitive Landscape of the PCB Industry

There are numerous manufacturers in the global printed circuit board industry, with low market concentration and intense competition. Currently, there are nearly 3,000 PCB companies worldwide.

The domestic PCB industry also has low concentration, forming a competitive landscape involving Taiwanese, Hong Kong, American, Japanese, and local enterprises. Foreign enterprises generally have large investment scales and technological advantages, while domestic enterprises are numerous and widely distributed but have certain gaps in scale and technology compared to foreign enterprises. According to data from CPCA, in 2024, the top ten PCB manufacturers in China are expected to have a combined revenue of 160.995 billion CNY, with a total market share of 54.34%.

2. Competitive Landscape of the Prototype and Small-Batch Industry

There are many participants in the prototype and small-batch industry, and the market competition landscape is diversified. In the traditional model, there are mainly two types of participants in the prototype and small-batch PCB market: large PCB manufacturers engaged in prototype and small-batch board manufacturing for the purpose of obtaining mass orders, and manufacturers specializing in providing PCB prototypes and small-batch boards. Among them, manufacturers specializing in prototypes and small-batch PCBs can be further divided into those with strong overall capabilities and broad customer coverage and those with weaker overall capabilities and limited service areas. The booming and personalized demands from small and medium-sized enterprise customers and individual consumers have raised higher requirements for the service capabilities of traditional prototype and small-batch PCB manufacturers, leading to the emergence of PCB enterprises adopting the industrial internet model.

Domestic companies primarily using traditional offline service models for prototypes and small-batch PCBs include Xingsen Technology, Jinbaize, and Xunjiexing, while most companies adopting the industrial internet service model are smaller and do not have any listed or planned listed companies.

Overseas Major Enterprises

[DDiCorp.DDiCorp. was established in 1978, headquartered in Anaheim, California, originally a NASDAQ-listed company, acquired by Viasystems Group, Inc. in 2012, becoming its wholly-owned subsidiary. DDi’s main business is prototypes and small-batch boards, with products primarily applied in defense and aerospace, communication equipment, industrial control, computers, testing/medical, and consumer electronics.

[KSGKundenfreudlich-Schnell-Gut (abbreviated as “KSG”) is located in Saxony, Germany, with main products including double-sided boards, multilayer boards, HDI boards, rigid-flex boards, aluminum-based boards, and thick copper foil boards, positioned in the niche market of “diverse varieties, small batches, and short delivery times.”

[Qing Sheng Electronics] Taiwan Qing Sheng Electronics Co., Ltd. (abbreviated as “Qing Sheng Electronics”) was established in 1984, headquartered in Taoyuan County, Taiwan, and listed on the Taiwan Stock Exchange in 2003. Qing Sheng Electronics’ main business is semiconductor and other electronic component manufacturing, with products primarily applied in servers, industrial equipment, computers, communications, and consumer electronics.

Domestic Major Enterprises

[Xingsen Technology] Shenzhen Xingsen Quick Circuit Technology Co., Ltd. was established in 1999, listed on the Shenzhen Stock Exchange’s SME board in 2010. Xingsen Technology’s main business is the production and sales of printed circuit prototypes and small-batch boards, with products primarily applied in communication equipment, industrial and medical electronics, computers, and defense. According to periodic reports, Xingsen Technology’s revenue in 2024 is expected to be 581,732.42 CNY, with a net profit attributable to shareholders of the parent company of -19,828.98 million CNY.

[Jinbaize] Shenzhen Jinbaize Electronic Technology Co., Ltd. was established in 1997, listed on the Shenzhen Stock Exchange’s Growth Enterprise Market in 2021. Jinbaize’s main business is printed circuit boards, electronic manufacturing services, and electronic design services, with core products primarily applied in smart hardware, communications, industrial control, medical, defense, power, automotive, and computers. According to periodic reports, Jinbaize’s revenue in 2024 is expected to be 68,265.59 million CNY, with a net profit attributable to shareholders of the parent company of 3,906.30 million CNY.

[Xunjiexing] Shenzhen Xunjiexing Technology Co., Ltd. was established in 2005, listed on the Shanghai Stock Exchange’s Sci-Tech Innovation Board in 2021. Xunjiexing’s main business is the research, production, and sales of printed circuit boards, with products primarily applied in security electronics, industrial control, communication equipment, medical devices, automotive electronics, and rail transit. According to periodic reports, Xunjiexing’s revenue in 2024 is expected to be 68,265.59 million CNY, with a net profit attributable to shareholders of the parent company of 3,906.30 million CNY.

[Sihui Fushi] Sihui Fushi Electronic Technology Co., Ltd. was established in 2009, listed on the Shenzhen Stock Exchange’s Growth Enterprise Market in 2020. Sihui Fushi’s main business is the research, production, and sales of printed circuit boards, with products primarily applied in industrial control, automotive electronics, transportation, communication equipment, and medical devices. According to periodic reports, Sihui Fushi’s revenue in 2024 is expected to be 141,317.77 million CNY, with a net profit attributable to shareholders of the parent company of 14,028.49 million CNY.

[Qiangda Circuit] Shenzhen Qiangda Circuit Co., Ltd. was established in 2004, listed on the Shenzhen Stock Exchange’s Growth Enterprise Market in 2024. Qiangda Circuit’s main business is the research, production, and sales of PCB, focusing on mid-to-high-end prototypes and small-batch boards, with products widely applied in industrial control, communication equipment, automotive electronics, consumer electronics, medical health, and semiconductor testing. According to periodic reports, Qiangda Circuit’s revenue in 2024 is expected to be 79,304.14 million CNY, with a net profit attributable to shareholders of the parent company of 11,264.82 million CNY.

(5) Industry Development Prospects

1. Industry Development Opportunities

(1) Intensive Policy Support Provides Strong Assurance for Industry Development

China is currently transitioning from high-speed economic growth to high-quality development, with the digital economy playing an important role in promoting industrial transformation and upgrading and cultivating new growth momentum. The country has successively introduced a series of policy documents that outline a top-level design blueprint from aspects such as technological research and development, application of results, infrastructure, and platform construction, providing strong policy support for the development of the digital economy.

(2) Research Investment Boosts R&D Development

With the increasing emphasis on scientific innovation in recent years, China’s basic research investment scale has rapidly grown. From 2017 to 2024, China’s research and experimental development expenditure has increased from 1.76 trillion CNY to 3.61 trillion CNY, with the proportion of research and experimental development expenditure to GDP rising from 2.12% to 2.68%. As the country continues to emphasize technological innovation, the intensity of research funding is expected to steadily increase, continuously driving the vigorous development of R&D activities.

(3) New Market Development Space

The penetration of new generation information technology into the electronic manufacturing industry has made the demands of downstream application fields more diverse than ever, with R&D demands also continuously increasing. Strong innovation and R&D motivation create a vast market space for enterprises focused on providing one-stop technical support and production manufacturing needs for global customers in the product R&D and hardware innovation process.

2. Potential Issues in the Industry

(1) Increasing Complexity of Downstream Demand

With the development of downstream applications driven by new technologies such as 5G, artificial intelligence, big data, cloud computing, and the Internet of Things, user demands are evolving towards diversification and complexity. The increasingly complex and variable personalized demands of customers place high requirements on suppliers’ rapid response capabilities and flexible production capabilities. If companies in the industry cannot continuously conduct R&D and innovation in line with cutting-edge industry technology trends and changes in downstream demand, future profit margins will be affected.

(2) Lack of High-Quality Composite Talent

The electronic manufacturing industry integrates knowledge from various fields such as electronic engineering, mechanical engineering, and materials science, while also requiring long-term practical experience accumulation, resulting in a long training cycle for relevant talents. As the digital transformation speed of the electronic manufacturing industry accelerates, there is a significant demand for cross-disciplinary composite talents who not only master professional technologies related to products but also excel in new generation digital technologies such as cloud computing and big data. Coupled with intensified market competition, the shortage of relevant talents remains a common challenge, posing certain challenges to the future development of the industry.