1、Overview of Competition in the PCB Industry

The Printed Circuit Board (PCB) is an essential component in electronic products, widely used in various fields such as communications, computers, consumer electronics, and automotive electronics. With the continuous development of the global electronics industry, the market size of the PCB industry is also expanding, attracting numerous companies to enter the market, leading to increasingly fierce competition.

From a market perspective, the global PCB industry is relatively fragmented, with a large number of companies, including industry giants like Suzhou Dongshan Precision Manufacturing Co., Ltd. and Unimicron Technology Corp., as well as many small and medium-sized enterprises (SMEs) with smaller revenue scales. In terms of technology, the R&D investment and technical levels of different companies vary significantly. Large enterprises, with their strong financial resources and talent reserves, can continuously increase R&D investment, gaining a leading edge in high-end PCB technologies such as High-Density Interconnect (HDI) boards and rigid-flex boards, meeting the demands of high-end fields like communications and aerospace; while SMEs often have limited technical capabilities, focusing on low to mid-range products like standard single-sided and multi-layer boards, leading to severe product homogeneity, with competition mainly centered on price and cost.

2、Analysis of Competitive Hierarchy in the PCB Industry

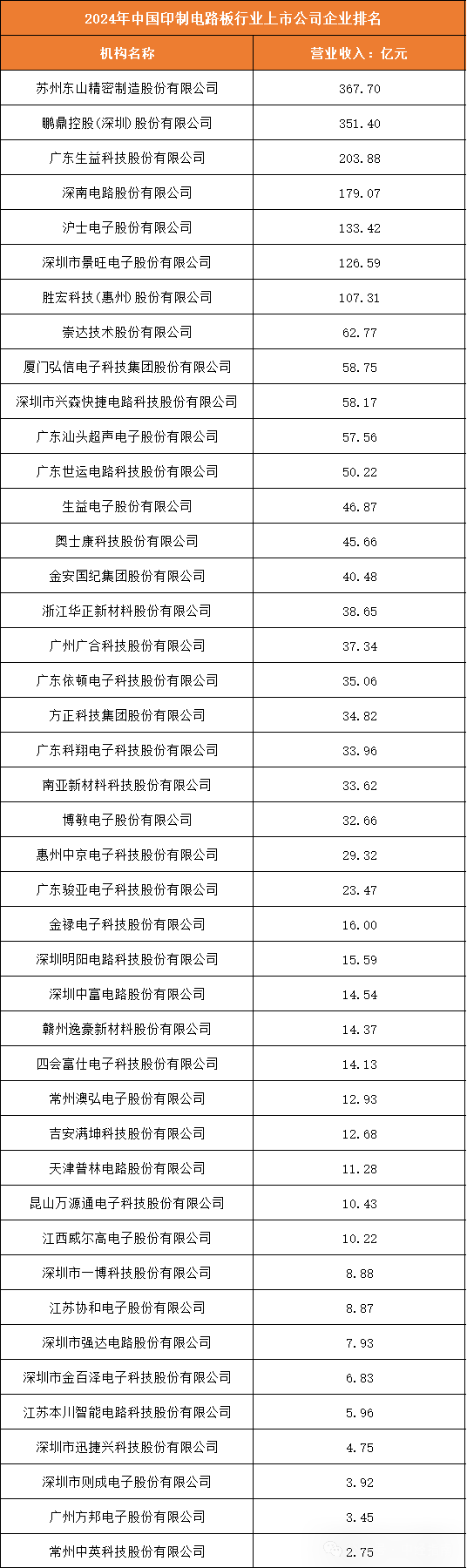

According to the Shenwan industry classification, the ranking of publicly listed companies in China’s PCB industry by revenue for the year 2024 is as follows:

The first tier consists of leading companies in the industry, such as Suzhou Dongshan Precision Manufacturing Co., Ltd. and Unimicron Technology Corp. They lead in revenue scale and have high recognition and market share in the global market. These companies not only possess advanced production equipment and process technologies capable of producing high-end, complex PCB products but also have strong R&D capabilities and a comprehensive customer service system, serving numerous internationally renowned electronic brand manufacturers and dominating high-end fields like communications and computers.

The second tier is represented by companies such as Guangdong Shengyi Technology Co., Ltd. and Shenzhen Shennan Circuits Co., Ltd. They have a revenue scale that is above average, with relatively strong technical capabilities, possessing unique competitive advantages in certain niche areas, enabling them to produce mid to high-end PCB products, with product quality and technical levels recognized in the market, holding a certain market share in both domestic and some international markets.

The third tier consists of a large number of SMEs, which have relatively small revenue scales and relatively outdated technology and equipment, mainly focusing on the production of low to mid-range PCB products, with low product added value. Market competition primarily relies on price advantages, leading to significant survival pressure, and they have weak risk resistance when facing market fluctuations and intensified industry competition.

3、Analysis of Competitive Trends in the PCB Industry

In the future, competition in the PCB industry will exhibit the following trends.

Technical competition will become increasingly intense. With the rapid development of emerging technologies such as 5G communications, artificial intelligence, and the Internet of Things, higher demands are placed on the performance, functionality, and reliability of PCBs. Companies need to continuously increase R&D investment to enhance their technical levels in high density, high performance, and miniaturization, developing more advanced products to meet market demands and capture more market share in high-end product areas.

Industry consolidation will accelerate. The intensification of market competition and the increase in technical barriers will further compress the survival space of SMEs, while large enterprises will seek to expand market share, enhance technical strength, and achieve synergies through mergers and acquisitions, integrating industry resources to achieve scale expansion and extend the industrial chain, leading to a further increase in industry concentration.

Environmental protection requirements will raise competitive thresholds. In the context of increasingly stringent environmental policies, environmental issues in the PCB production process have attracted significant attention. Companies need to continuously optimize production processes, reduce pollutant emissions, and improve resource utilization to meet green environmental requirements. This will increase production costs for companies, creating elimination pressure on some SMEs that do not meet environmental standards, while companies with green production capabilities will have a competitive advantage in the market.