No matter where you go

Please click the blue text, we miss you

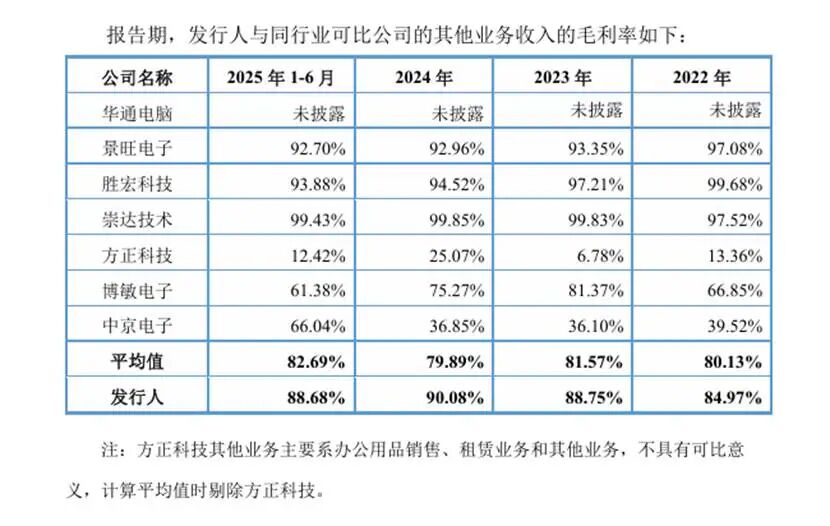

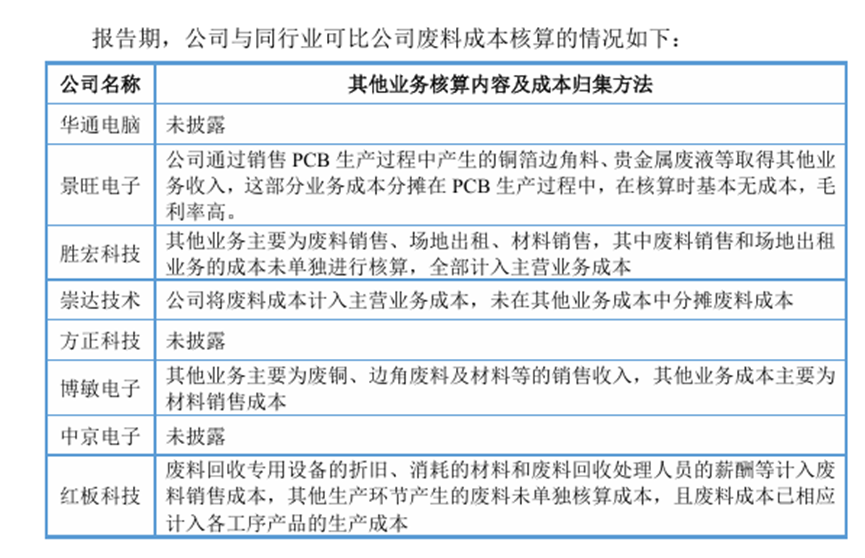

The calculation of waste material costs, transfer methods, and whether the related cost accounting complies with the provisions of enterprise accounting standards, as well as whether there are significant differences and reasons compared to the waste material sales revenue and gross profit ratios of comparable companies in the same industry.

(1) Calculation and transfer methods of waste material costs

The company’s PCB waste is generated during various production processes, and the production process of PCB products is relatively long, involving multiple steps such as lamination, copper plating, drilling, electroplating, etching, solder mask application, and surface treatment. Additionally, some products undergo multiple processing steps, making it difficult to accurately measure and account for the different types of waste generated by each process, as well as the waste material costs included in the finished products and various processes during rolling production. Therefore, the industry generally adopts the method of including waste material costs in product costs for accounting purposes.

During the reporting period, the company included the depreciation of specialized waste recovery equipment, consumed materials, and salaries of personnel involved in waste recovery processing in the cost of waste sales. Other waste generated in production processes was not accounted for separately, and the waste material costs have been appropriately included in the production costs of products from each process.

(2) Related cost accounting and other accounting treatments comply with enterprise accounting standards

The PCB production process is complex, and the aforementioned waste is generated from various PCB processes, with numerous types and quantities that are difficult to allocate corresponding costs. Considering the feasibility of cost accounting, the company included the depreciation of specialized waste recovery equipment, consumed materials, and salaries of personnel involved in waste recovery processing in the cost of waste sales. Other waste generated in production processes was not accounted for separately, and the waste material costs have been appropriately included in the production costs of products from each process, resulting in a higher gross profit margin for the company’s other businesses, in compliance with enterprise accounting standards.

Among comparable listed companies in the same industry, companies such as Jingwang Electronics, Shenghong Technology, Chongda Technology, and Bomin Electronics have higher gross profit margins in their other businesses, and their waste material cost accounting methods are similar to those of the company.

In addition, among listed companies in the same industry, companies such as Aoshikang, Junya Technology, Kexiang Co., Ltd., Mankun Technology, Jinlu Electronics, and Weiergao also have higher gross profit margins in their other businesses.

In summary, the company’s waste material cost accounting complies with enterprise accounting standards and industry practices.