Below is a summary of the core content from Morgan Stanley’s research report dated August 19, 2025, covering key trends, investment opportunities, and risk analysis in the Asia-Pacific semiconductor industry (especially in Greater China):1. Industry Insights and Core Conclusions

- Industry Rating Upgraded

- Upgraded the semiconductor industry outlook for the second half of 2025 to “Attractive” (Attractive), with a focus on AI Semiconductors (outperforming non-AI sectors).

- Driving Factors: Easing concerns over tariffs and exchange rates, decreasing inventory days (historically, a decline in inventory indicates rising stock prices), and the spread of generative AI demand across multiple sectors.

- Key Risks

- AI Replacement Effect: The recovery in the second half of 2025 may be affected by tariff costs.

- Chinese Production Capacity Expansion: Overcapacity in mature process wafer fabs (such as SMIC and Hua Hong) leads to price pressure, with gross margins remaining low (around 5-25%).

- Exchange Rate Fluctuations: The appreciation of the New Taiwan Dollar puts pressure on the gross margins of Taiwanese companies like TSMC (each 1% appreciation affects gross margins by 0.4-0.5 percentage points).

2. AI Semiconductor Supply Chain Dynamics

- Demand Driven

- Surge in Inference Demand: Models like DeepSeek drive low-cost inference demand, but NVIDIA’s B30 chip may dilute the local GPU supply chain share.

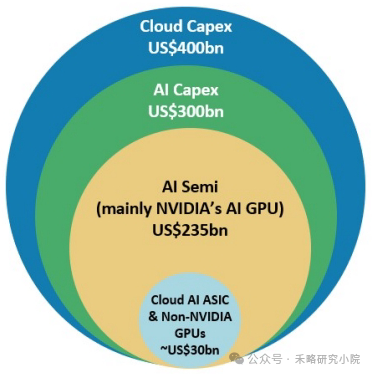

- Cloud Service Providers (CSP) Capital Expenditure: Cloud capital expenditure is expected to reach $102.7 billion in 2025-2026, with the AI semiconductor TAM (Total Addressable Market) potentially reaching $235 billion.

- Edge AI and Custom Chips: The growth rate of edge AI semiconductors (22% CAGR) may surpass that of cloud, while custom chips (39% CAGR) will outpace general-purpose chips.

- Supply Chain Bottlenecks and Breakthroughs

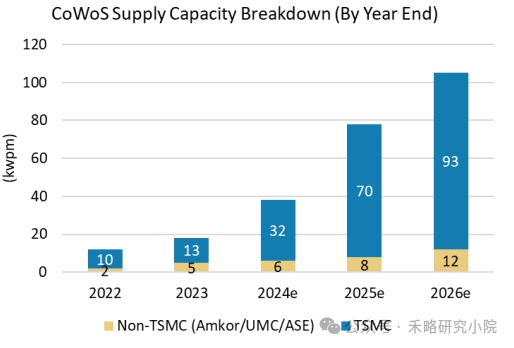

- CoWoS Capacity: TSMC plans to expand CoWoS capacity to 90kwpm by 2026 to alleviate NVL72 server rack bottlenecks.

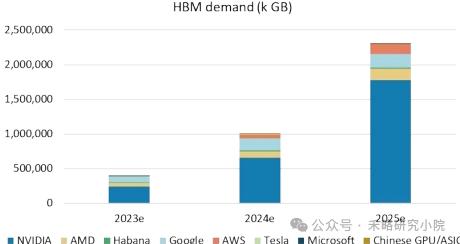

- HBM Supply: HBM demand may reach 16 billion Gb in 2025, with NVIDIA holding a dominant share.

- Domestic GPU in China: The self-sufficiency rate is expected to rise from 34% in 2024 to 82% in 2027, with SMIC’s 7nm capacity being a core driver.

3. Key Companies and Investment Opportunities

- AI-Related Targets

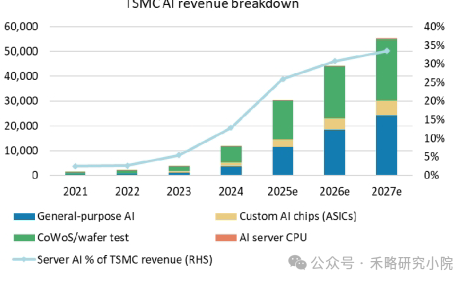

- TSMC: AI revenue share may reach 34% by 2027, benefiting from CoWoS expansion (target price NT$1,888, +34% upside potential).

- KYEC: NVIDIA testing business may contribute over 25% of revenue in 2025, driving performance growth.

- GUC and Alchip: Leaders in custom AI chip design services, benefiting from the trend of CSP self-developed chips.

- Leaders in Niche Fields

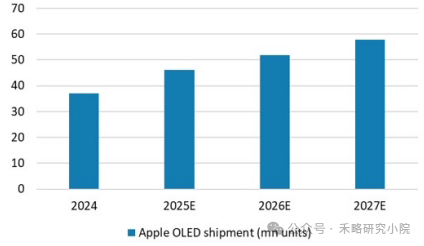

- Driver ICs: Novatek benefits from OLED DDI demand (expected to ship 46 million OLED DDIs for iPhone in 2025).

- Power Semiconductors: Starpower and Yangjie benefit from the localization of automotive semiconductors.

- Equipment and Materials: ASMPT (packaging equipment) and AMEC benefit from advanced packaging and domestic substitution.

- Emerging Technology Layout

- CPO (Co-Packaged Optics): A key technology to reduce power consumption in high-speed transmission, with Broadcom and ASE as major players.

- WoW (Wafer-on-Wafer): Winbond’s CUBE solution can enhance bandwidth and reduce costs, with a CAGR of 257% expected from 2025 to 2030.

4. Focus on the Chinese Market

- Automotive Semiconductors

- Localization Opportunities: China leads the world in electric vehicle penetration, but the self-sufficiency rate for automotive chips is only 15% (2024), expected to rise to 28% by 2027.

- Key Targets: Horizon Robotics (autonomous driving chips), OmniVision (CIS sensors), GigaDevice (MCU).

- Equipment Import Substitution

- In the first half of 2025, equipment imports are expected to grow by 2% year-on-year, with Singapore becoming a major source. Equipment vendors (North Huachuang, AMEC) continue to benefit from policy support.

5. Risk Warnings

- Mature Process Competition: Overcapacity in mature nodes at Chinese fabs puts pressure on gross margins (SMIC’s gross margin is around 15-25%).

- Geopolitical Issues: U.S. restrictions on high-end GPU exports may accelerate domestic substitution, but the technology gap is difficult to bridge in the short term.

- Exchange Rate Fluctuations: The appreciation of the New Taiwan Dollar puts pressure on the profitability of Taiwanese companies.

6. Key Data Overview

|

Indicator |

2024/2025e |

2027e/2030e |

|---|---|---|

|

China’s GPU Self-Sufficiency Rate |

34% (2024) |

82% (2027e) |

|

Cloud AI Semiconductor TAM |

– |

$235 billion (2025e) |

|

Edge AI Semiconductor CAGR |

– |

22% (2023-2030e) |

|

CoWoS Capacity (TSMC) |

32kwpm (2024e) |

90kwpm (2026e) |

|

HBM Demand |

– |

16 billion Gb (2025e) |

Conclusion: AI semiconductors (especially inference and custom chips), localization of automotive semiconductors, and advanced packaging (CoWoS/WoW) are core growth points. It is recommended to overweight leading AI supply chain companies such as TSMC, KYEC, and GUC, as well as automotive chip targets like Starpower and Horizon Robotics, while also paying attention to exchange rate and geopolitical risks.