Semiconductor Industry

In 2025, the semiconductor industry is in adual-driven phase of cyclical recovery and explosive AI demand, with global semiconductor sales increasing year-on-year for seven consecutive quarters, and China’s semiconductor self-sufficiency rate rising to 18%-26%. The A-share semiconductor sector has risen 36.66% year-to-date, significantly outperforming the CSI 300 index by 22.38 percentage points. In the five major sub-sectors of design, manufacturing, packaging and testing, equipment, and materials,the localization process of equipment/materials is accelerating (the localization rate of equipment is expected to exceed 25%), AI chip design demand is exploding (AI-related applications contribute nearly half of the market increment), and wafer foundry capacity utilization exceeds 90%, providing clear direction for short-term investment.

It is recommended to focus on key targets such as North Huachuang and Zhongwei Company (equipment), SMIC and Huahong Group (manufacturing), Haiguang Information and Cambrian (AI design).

1. Development Stage and Investment Environment of the Semiconductor Industry

1.1 Industry Prosperity Continues to Rise

In 2025, the semiconductor industry has entered aclear recovery upcycle, with strong growth momentum. According to data from the Semiconductor Industry Association (SIA), global semiconductor sales are expected to reach179.7 billion USD in the second quarter of 2025, up +20% year-on-year and +7.8% quarter-on-quarter, setting a historical quarterly record, and achieving “seven consecutive quarters of year-on-year positive growth,” with significant certainty in recovery.

From the annual forecast, the World Semiconductor Trade Statistics (WSTS) predicts that the global market size will reach700.9 billion USD (up +11.2% year-on-year) in 2025, while the International Data Corporation (IDC) is more optimistic, estimating it to reach800 billion USD (up +17.6% year-on-year), with the computing sector (including AI) growing by 36% to 349 billion USD. The core drivers of growth come fromartificial intelligence, cloud computing, 5G communication, and new energy vehicles, especially the explosive growth in demand for high-end chips driven by AI applications.

China’s market performance is outstanding: in the first half of 2025, industry revenue reached 321.2 billion CNY (up +16% year-on-year), with net profit attributable to shareholders of 24.5 billion CNY (up +30% year-on-year), and profit growth accelerating further; the A-share semiconductor sector rose 26.65% in August alone, with a cumulative increase of 36.16% year-to-date, significantly outperforming the market.

1.2 Unprecedented Favorable Policy Environment

In 2025, the semiconductor industry welcomesthe strongest policy support in history, with efforts in three dimensions:

Funding: The National Big Fund Phase III has officially launched, with a total scale of344 billion CNY, focusing on advanced processes, third-generation semiconductors, EDA tools, and other “bottleneck” areas; Taxation: Five departments have clarified tax incentives for enterprises in advanced processes of 28nm/65nm/130nm, and the proportion of R&D expenses for integrated circuit companies that can be deducted has been increased; Local: Shenzhen has established a 5 billion CNY “semi-industry private equity fund” to support industry chain optimization through “policy + capital”; Planning: The “2025-2026 Action Plan for Stable Growth of the Electronic Information Manufacturing Industry” proposes a “national goods for national use” strategy, requiring comprehensive localization of key components for 5G/6G, with a target of 70% localization rate for core semiconductor links by 2025, over 30% market share for 14nm processes, and a scale of over 100 billion CNY for third-generation semiconductor materials.

1.3 Accelerated Technological Breakthroughs for Domestic Substitution

In 2025, China’s semiconductor technology has achievedmultiple key breakthroughs, significantly accelerating the process of domestic substitution:

Advanced processes: SMIC’s 7nm process yield has improved to 60%, and 5nm trial production verification has been completed using DUV multi-patterning technology, with a yield of 95% for the 28nm process (international advanced level), and an additional monthly capacity of 150,000 wafers dedicated to AI chip foundry at its Beijing and Shenzhen bases; Equipment: Shanghai Microelectronics has achieved an 82% yield for the mass production of 28nm immersion lithography machines, with an annual capacity exceeding 100 units (localization rate of 90%); SMIC is testing the domestic DUV lithography machine from Shanghai Yuliangsheng, which can achieve 28nm production through multi-patterning, potentially promoting 7nm/5nm trial production; AI Chips: Huawei’s Ascend 910B (3nm process) has entered mass production, becoming a benchmark for domestic AI training chips; Alibaba’s T-head PPU parameters are on par with NVIDIA’s H20 and A800, and are compatible with the CUDA ecosystem, solving the “ecosystem isolation” problem; Materials: In April 2025, high-purity quartz ore was classified as a new mineral type, with proven reserves exceeding 70 million tons in Dongqiling, Henan, and Altay, Xinjiang, promoting the localization of quartz materials and reducing dependence on the US supply chain.

1.4 Capacity Utilization and Inventory Status

In 2025, the semiconductor industryis operating at a high capacity utilization rate, with inventory structure continuously optimizing:

Capacity: SMIC’s capacity utilization rate in the second quarter was 92.5% (up +2.9 percentage points quarter-on-quarter, up +7.3 percentage points year-on-year, setting a new high in nearly six quarters); Huahong Group reached 108.3% (up +5.6 percentage points quarter-on-quarter, up +10.4 percentage points year-on-year), operating at overcapacity for several consecutive quarters, with orders exceeding supply; the top ten global wafer foundries had revenues of 41.718 billion USD in the second quarter (up +14.6% quarter-on-quarter, setting a historical high); Inventory: Showing characteristics of “structural destocking” — 62 semiconductor companies in China had a year-on-year inventory increase of +14% and a quarter-on-quarter increase of +6.5%, but inventory turnover days decreased to 173.78 days (quarter-on-quarter decline), improving management efficiency; the inventory days of the top 60 global semiconductor companies are expected to gradually decrease from 124 days in 2024Q4 to 105-110 days by the end of 2025; Cycle Resonance: The industry may welcome a “long (AI-driven) + medium (capacity utilization recovery) + short (inventory destocking tail end)” cycle resonance, with a potential entry into a replenishment phase in the second half of 2025.

2. Leading Stocks and Core Stocks in the Semiconductor Design Field

2.1 Leading Stock Analysis

HiSilicon (Huawei Subsidiary)

China’s absolute leader in chip design, retaining the top spot in the Chinese chip brand list in 2025, focusing onmobile terminals, communication infrastructure, and AI computing in three major areas:

Technological breakthroughs: The Ascend 910B (3nm process) has entered mass production, becoming a benchmark for domestic AI training chips; the Kirin 9000X processor has passed the security reliability level II certification (the highest level); the AC9610 chip has key performance reaching international leading levels, with a mass production yield of 83%; Capacity / Ecosystem: The Shanghai HiSilicon Lingang base plans to build a dedicated 12-inch wafer production line, targeting a production capacity of 500,000 wafers/month by 2026; in the second half of 2025, it will launch the HarmonyOS cellular watch core, integrating “chip + module + solution + ecosystem,” merging star flash connectivity, OpenHarmony system, and edge-side AI; it is expected that over 50 million smartphones will upgrade to star flash car keys via OTA by Q4 2025, accelerating the layout of the Internet of Things.

Unisoc

One of the only three companies in the global open market for 5G mobile phone chip design, with shipments expected to exceed 1.6 billion units in 2024 (a historical high):

Product innovation: Launching the 5G SoC T8300 (6nm process) at MWC 2025, integrating 5G NR NTN satellite communication and 5G MBS broadcasting functions for the first time; launching the flagship smart cockpit platform A8880 and the 4G wearable platform W527 in 2025; Global expansion: 5G chips have completed field tests in 115 countries, with terminal products shipped to 85 countries (over ten million units), collaborating with international brands such as Nubia, Motorola, HMD, and ZTE.

2.2 Core Stock Analysis

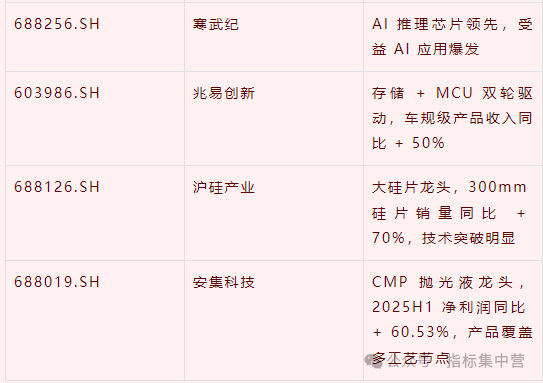

GigaDevice (603986.SH)

A leader driven by both storage and MCU, with stable performance in 2025:

Financial performance: Q2 single-quarter revenue of 2.241 billion CNY (up +13.1% year-on-year, up +17.4% quarter-on-quarter), with a net profit attributable to shareholders of 341 million CNY (up +9.2% year-on-year, up +45.3% quarter-on-quarter); total revenue in the first half of the year was 4.150 billion CNY, with a net profit of 588 million CNY (NOR Flash contributing 60% of revenue); Technology / Market: Large-scale production of 45nm SPINOR Flash (leading storage density); 45nm automotive-grade Flash/MCU has passed AEC-Q100 certification, with automotive revenue accounting for 18% in H1 2025 (up +50%), and GD32A7 series supplied in bulk to NIO and Xpeng; NOR Flash has a global market share of 23% (ranking second), with niche DRAM DDR4 (8Gb) ramping up in TV/industrial sectors, and gross margin recovering to double digits; New products: Launching high-speed QSPI NAND Flash (30% faster read speed), focusing on expanding industrial and IoT rapid startup scenarios.

OmniVision (formerly Weir Shares, 603501.SH)

A core enterprise in image sensors (CIS), with revenue/profit growth in H1 2025:

Financial performance: Main business revenue of 13.940 billion CNY (up +15.5% year-on-year), with a net profit attributable to shareholders of 2.028 billion CNY (up +48.3% year-on-year), and a net profit excluding non-recurring items of 1.951 billion CNY (up +42.2% year-on-year); Business structure: CIS business revenue of 10.346 billion CNY (accounting for 74.2%, up +11.1% year-on-year), withautomotive electronics being the biggest highlight — automotive CIS revenue of 3.789 billion CNY (up +30.0% year-on-year), accounting for 37% of CIS revenue, nearly equal to the smartphone sector (38%); Technology / Customers: 200 million pixel CIS has completed customer verification, and the 50 million pixel 1-inch high dynamic range sensor OV50X has entered mass production; entering NVIDIA’s supply chain to support its visual needs; revenue from emerging markets such as panoramic/sports cameras reached 1.173 billion CNY (up +2.5 times, accounting for 11%), becoming a new growth point.

Goodix Technology (603160.SH)

A leading enterprise in human-computer interaction chips, with significant improvement in profitability in Q1 2025:

Financial performance: Q1 revenue of 1.064 billion CNY (down -12.6% year-on-year), with a net profit attributable to shareholders of 200 million CNY (up +20.3% year-on-year), and a net profit margin of 18.4%; Technology / Market: Mass production of ultrasonic fingerprint chips (with better accuracy and anti-interference than optical fingerprints); automotive-grade touch solutions supplied to BYD and Geely; small-sized touch chips introduced in Samsung and vivo flagship projects, with large-sized touch chips leading in market share in PCs/tablets; Revenue structure: Fingerprint recognition chips (accounting for 38.8%, gross margin 37.3%) and touch chips (accounting for 37.2%, gross margin 51.8%) are core; demand in the IoT market is growing, with significant increases in shipments of large-sized touch chips and active pen solutions year-on-year.

2.3 Investment Logic in the Design Field

Short-term focus onAI-driven, domestic substitution, and automotive electronics as the three main lines:

AI Chips: Explosive demand for training/inference/edge AI chips, with technological breakthroughs from Huawei’s Ascend and Alibaba’s T-head, providing significant space for domestic substitution; Domestic Substitution: Geopolitical factors are driving domestic customers to shift towards domestic chips, with communication/storage/analog chips upgrading from “usable” to “well usable,” with some products outperforming imports; Automotive Electronics: The demand for automotive chips is driven by new energy vehicles + intelligent driving (the chip value per vehicle has increased from 80 USD to 800 USD), with accelerated domestic penetration of automotive MCUs, sensors, and smart cockpit chips.

3. Leading Stocks and Core Stocks in the Semiconductor Manufacturing Field

3.1 Leading Stock Analysis

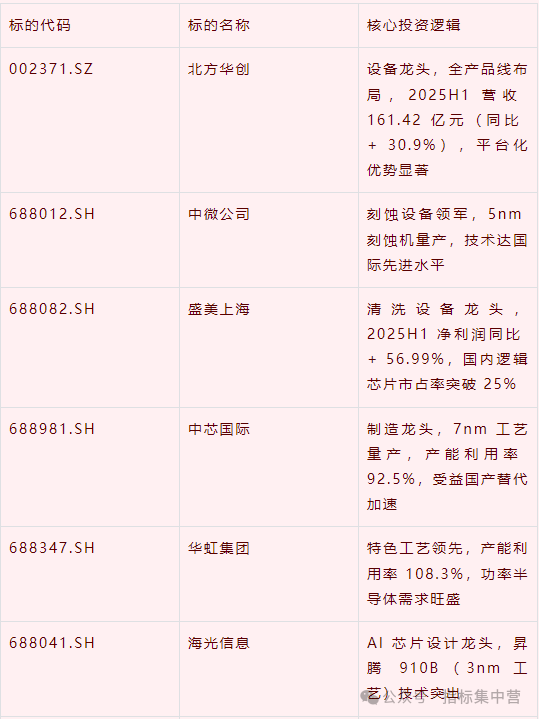

SMIC (688981.SH/00981.HK)

The largest wafer foundry in China, with dual breakthroughs in technology and capacity in 2025:

Financial performance: Revenue in the first half of the year was 4.46 billion USD (up +22% year-on-year), with a gross margin of 21.4% (up +7.6 percentage points year-on-year); Q2 revenue was 2.209 billion USD (down -1.7% quarter-on-quarter), with a capacity utilization rate of 92.5% (up +2.9 percentage points quarter-on-quarter, setting a new high in nearly six quarters); Technical strength: 28nm process yield of 95% (internationally advanced), mass production of high-voltage driver chips (filling the domestic gap for AMOLED driver chips); equivalent 7nm process yield exceeding 90% (small batch trial production), achieving 7nm mass production through DUV multi-patterning (20%-30% higher cost than EUV, but breaking ASML’s monopoly), and has supplied to AI chip manufacturers; Capacity / Customers: Monthly capacity increased from 973,300 wafers (8-inch equivalent) in Q1 to 991,300 wafers (up 1.8%) in Q2, with an additional 20,000 wafers/month of 12-inch capacity added in H1 2025; Q2 revenue from the China region accounted for 84.1% (year-on-year increase), covering applications in smartphones (25.2%), consumer electronics (41%), and industrial/automotive (10.6%); Outlook: Q3 revenue is expected to increase by +5%-7% quarter-on-quarter, with a gross margin of 18%-20%.

Huahong Group (688347.SH/01347.HK)

The second-largest wafer foundry in China, with significant advantages in specialty processes:

Financial performance: Revenue in the first half of the year was 8.01 billion CNY; Q2 revenue was 566 million USD (up +18.3% year-on-year, up +4.6% quarter-on-quarter), with a capacity utilization rate of 108.3% (up +5.6 percentage points quarter-on-quarter, up +10.4 percentage points year-on-year), operating at overcapacity for several consecutive quarters; Core advantages: Focusing on mature processes of 40-90nm, with leading specialty processes in power devices, RF devices, and embedded memory; automotive-grade products have passed certification for 102 chips, with 74 chips selected in the Ministry of Industry and Information Technology’s “Recommended List of Automotive Chips” (industry first); revenue from industrial technology products below 65nm increased by +27.4% year-on-year; Capacity expansion: As of June 2025, total capacity was 447,000 wafers/month (8-inch equivalent, up +18% year-on-year); the Wuxi FAB9 production line had a Q2 capacity utilization rate of 98% (monthly capacity of 42,000 wafers), with the second phase of expansion advanced to the end of 2025 (targeting 83,000 wafers/month); the 22nm process is continuously fully loaded, with a capacity target of 80,000 wafers/month for the 40-55nm production line by the end of 2026; New technology: Layout of SiC and GaN third-generation semiconductors, targeting the new energy vehicle and 5G base station markets.

3.2 Core Stock Analysis

China Resources Microelectronics (688396.SH)

A domestic leader in power semiconductors, driven by new energy + high-end manufacturing:

Financial performance: In H1 2025, revenue was 5.218 billion CNY (up +9.6% year-on-year), with a net profit attributable to shareholders of 339 million CNY (up +20.9% year-on-year); Q2 revenue was 2.863 billion CNY (up +8.3% year-on-year, up +21.6% quarter-on-quarter), with a net profit attributable to shareholders of 256 million CNY (up +207.1% quarter-on-quarter), showing strong growth momentum; Market position: According to Omdia statistics, in 2025, China ranks second among power semiconductor companies, with the largest MOSFET scale; the global power semiconductor market is expected to reach 75.5 billion USD in 2025, with China accounting for 38.6% (29.1 billion USD), benefiting the company significantly; Automotive electronics: In H1 2025, revenue from automotive electronics + new energy business was 1.248 billion CNY (up +37%, accounting for 24%), with nearly a hundred automotive-grade power chips in mass production, providing stable supply to BYD (including blade battery management systems); Technology / R&D: Mass production of SiC MOSFETs and SiC Schottky diodes; mastering IGBT trench gate and field stop technologies; R&D investment in H1 2025 was 548 million CNY (accounting for 10.5%); Product structure: The general new energy sector (new energy vehicles, photovoltaics, wind power) accounts for 44%, becoming the largest application pillar.

3.3 Investment Logic in the Manufacturing Field

Short-term focus onhigh capacity utilization, breakthroughs in advanced processes, and the rise of specialty processes as the three main lines:

Capacity: High capacity utilization rates at SMIC (92.5%) and Huahong (108.3%) bring scale effects, enhancing profitability and supporting expansion plans; Advanced Processes: SMIC’s 7nm mass production and 5nm trial production narrow the gap with international standards, with DUV multi-patterning technology providing an independent path; Specialty Processes: Huahong (power/RF) and China Resources Microelectronics (power semiconductors) are competing in differentiated ways in mature process fields, benefiting from the growth in demand for new energy vehicles and 5G.

4. Leading Stocks and Core Stocks in the Semiconductor Packaging and Testing Field

4.1 Leading Stock Analysis

Changdian Technology (600584.SH)

The third-largest packaging and testing company globally and the largest in mainland China, with significant breakthroughs in advanced packaging:

Financial performance: In H1 2025, revenue was 18.63 billion CNY (up +7.2% year-on-year), with both Q2 and H1 revenue setting historical highs; the subsidiary Changdian Advanced (high-end packaging) had H1 revenue of 1.014 billion CNY (up +37.96% year-on-year), with a net profit of 279 million CNY (up +136.19% year-on-year), and a net profit margin of 27.48%; Technical strength: The XDFOI® multi-dimensional heterogeneous integration platform has entered mass production (supporting multi-chip integration at the 4nm node, with a maximum packaging area of 1500mm²); the 2.5D packaging has been validated as a replacement solution by TSMC CoWoS, with mass production expected in H2 2025, alleviating global high-end packaging capacity tightness; R&D / Market: In H1 2025, R&D expenses were 990 million CNY (up +20.5%, accounting for 6.8%, higher than the industry average of 4%-5%); revenue from Chiplet, 2.5D/3D advanced packaging accounted for over 72% (higher than the industry average); global market share of 10%-12%, with customers including Qualcomm, Broadcom, NVIDIA, and Huawei HiSilicon; the AI chip packaging business benefits from explosive demand.

4.2 Core Stock Analysis

<span (002156.sz)

The fourth-largest packaging and testing company globally and the second-largest in mainland China, with comprehensive growth in H1 2025:

Financial performance: Revenue was 13.038 billion CNY (up +17.67% year-on-year), with a net profit attributable to shareholders of 412 million CNY (up +27.72% year-on-year), and a net profit excluding non-recurring items of 420 million CNY (up +32.85% year-on-year), with operating cash flow of 2.480 billion CNY (up +34.47% year-on-year); Core advantages: Deeply bound to AMD, participating in advanced packaging cooperation for its AI chips and data center chips; global market share of about 8%, with rich experience in high-end packaging for CPU/GPU; Capacity layout: With production bases in Nantong, Suzhou, Hefei, and Xiamen, the scale of capacity and geographical layout advantages are significant.

Huatian Technology (002185.SZ)

The seventh-largest packaging and testing company globally and the third-largest in mainland China, with prominent characteristics in segmented fields:

Financial performance: In H1 2025, revenue was 7.780 billion CNY (up +16.6% year-on-year), with growth slightly lower than Tongfu Microelectronics (19.8%); Core advantages: Leading technology in packaging for memory chips (DRAM/NAND), benefiting from the explosive demand for AI server HBM; outstanding packaging technology for RF/power devices, applied in 5G communication and new energy vehicles; Industry prosperity: In March 2025, domestic packaging and testing leaders (Changdian, Tongfu, Huatian) had capacity utilization rates up +5%-10% year-on-year, with optimistic industry prospects.

4.3 Investment Logic in the Packaging and Testing Field

Short-term focus onexplosive demand for advanced packaging, AI-driven technology upgrades, and accelerated domestic substitution as the three main lines:

Advanced Packaging: The approach of Moore’s Law is nearing its limit, with Chiplet, 2.5D/3D, and system-level packaging becoming key to performance improvement, with the market size expected to grow from 40 billion USD in 2024 to 48.2 billion USD in 2026 (accounting for over 50%); AI-driven: The high computing power/high power consumption demand for AI chips drives high-end packaging technologies such as HBM and CoWoS, with domestic companies like Changdian and Tongfu achieving technological breakthroughs to seize market share; Domestic Substitution: The rapid development of domestic chip design companies is driving growth in local packaging and testing demand, coupled with supply chain security considerations, increasing the share of domestic packaging and testing companies.

5. Leading Stocks and Core Stocks in the Semiconductor Equipment Field

5.1 Leading Stock Analysis

North Huachuang (002371.SZ)

The absolute leader in semiconductor equipment in China, with significant advantages in full product line layout:

Financial performance: In H1 2025, revenue was 16.142 billion CNY (up +30.86% year-on-year), with a net profit attributable to shareholders of 3.208 billion CNY (up +15.37% year-on-year), being the only semiconductor equipment company in China with revenue exceeding 10 billion; Q2 revenue was 7.936 billion CNY (up +22.54% year-on-year, down -3.30% quarter-on-quarter), maintaining a high level; Product layout: Etching equipment (H1 revenue exceeding 5 billion CNY, with a full range of ICP/CCP/high selectivity etching), thin film deposition equipment (H1 revenue exceeding 6.5 billion CNY, accounting for over 40%, with PVD/CVD/ALD fully covered), thermal processing equipment (H1 revenue exceeding 1 billion CNY, with a full range of vertical furnaces/rapid thermal processing), and wet processing equipment (H1 revenue exceeding 500 million CNY, with comprehensive layout for single wafer/slot); in March 2025, launched 12-inch ion implantation equipment, entering new fields; Market position: In 2025, ranked first among semiconductor equipment companies in China and sixth globally; equipment has entered major domestic wafer foundries such as SMIC, Huahong, and Yangtze Memory, with competitive advantages in mature process equipment comparable to international giants.

Zhongwei Company (688012.SH)

The leading domestic etching equipment company, with advanced process technology:

Financial performance: In H1 2025, revenue was 4.961 billion CNY (ranking third among domestic equipment companies); Core advantages: Mass production of 5nm etching machines (technology reaching international advanced levels), applied in TSMC, Samsung, Intel, and other international wafer foundries; supplying to SMIC and Huahong in the domestic market; Technical trends: The increase in etching steps for advanced processes (3nm/2nm) has led the company to accumulate deep expertise in plasma physics and precision control, likely to maintain its leading position.

5.2 Core Stock Analysis

Shengmei Shanghai (688082.SH)

The leading domestic cleaning equipment company, with high growth in H1 2025:

Financial performance: Revenue was 3.265 billion CNY (up +35.83% year-on-year), with a net profit attributable to shareholders of 696 million CNY (up +56.99%, with growth outpacing revenue); Q2 revenue was 1.959 billion CNY (up +32.17% year-on-year, up +50.05% quarter-on-quarter), with a net profit of 449 million CNY (up +23.81% year-on-year, up +82.45% quarter-on-quarter); Core advantages: The market share of cleaning equipment for domestic logic chips has exceeded 25%, with technology covering megasonic/rotary/single wafer cleaning, meeting the needs of different process nodes; New product expansion: Sales of plating equipment (especially TSV plating) have increased, benefiting from the demand for 3D packaging; high-temperature single wafer SPM equipment and photoresist removal equipment continue to innovate; Market prospects: The explosive demand for AI chips and storage chips, along with HBM and advanced packaging, is driving the demand for high-end cleaning equipment, which the company is well-positioned to benefit from.

Other Specialty Equipment Companies

Huahai Qingke (688120.SH): The only company in China providing 12-inch CMP equipment, leading in the CMP field; Tuojing Technology (688072.SH): A core enterprise in thin film deposition equipment, with outstanding PECVD/ALD technology; Jingsheng Mechanical and Electrical (300316.SZ): A leading supplier of crystal growth equipment, primarily for photovoltaic/semiconductor silicon wafer equipment.

5.3 Investment Logic in the Equipment Field

Short-term focus onrapidly increasing localization rates, breakthroughs in high-end equipment, and strong downstream demand as the three main lines:

Localization rate: Increasing from 4% in 2018 to 13%-18% in 2024, with expectations to exceed 20%-25% in 2025, accelerating the replacement of key processes such as etching/cleaning/CMP/PVD; High-end breakthroughs: North Huachuang (ion implantation), Zhongwei Company (5nm etching), and Shengmei Shanghai (high-end cleaning) are achieving breakthroughs in high-end equipment, narrowing the gap with international standards; Downstream demand: The global semiconductor equipment sales are expected to reach 125.5 billion USD in 2025, with the Chinese market at 230 billion CNY (accounting for over 35%), driven by the expansion of domestic wafer foundries (storage/power/compound semiconductors) pushing equipment demand.

6. Leading Stocks and Core Stocks in the Semiconductor Materials Field

6.1 Leading Stock Analysis

Shanghai Silicon Industry (688126.SH)

The leading domestic semiconductor silicon wafer company, with significant breakthroughs in 300mm large wafers:

Financial performance: In H1 2025, revenue was 1.697 billion CNY (up +8.16% year-on-year), with a net loss attributable to shareholders of 367 million CNY (investment period for 300mm business); Q2 revenue increased by +11.75% quarter-on-quarter, with continuous improvement in business; Core advantages: Revenue from 300mm wafers accounts for over 40%, with year-on-year sales growth of +70%, annual shipments exceeding 5 million wafers, and cumulative certification of 750 models (covering logic/storage/CIS); capacity reaches 750,000 wafers/month (300mm) and 400,000 wafers/month (200mm and below), leading in China; Market position: The first in China to achieve mass production of 12-inch silicon wafers, with a domestic market share of 13% and global ranking of 2; products have been certified by SMIC, Huahong, and Yangtze Memory, entering the supply chains of TSMC and GlobalFoundries; Strategic value: Under geopolitical conditions, the importance of supply chain security is increasing, with the company being a core supplier of large silicon wafers in China, providing significant substitution space.

6.2 Core Stock Analysis

Anji Technology (688019.SH)

The leading domestic CMP polishing liquid company, with high growth in H1 2025:

Financial performance: Revenue was 1.141 billion CNY (up +43.17% year-on-year), with a net profit attributable to shareholders of 376 million CNY (up +60.53% year-on-year), and a net profit excluding non-recurring items of 357 million CNY (up +51.91% year-on-year); Q2 revenue was 596 million CNY (up +42.34% year-on-year), with a net profit of 207 million CNY (up +60.42% year-on-year); Core advantages: Revenue from CMP polishing liquids was 930 million CNY (accounting for 81.5%), covering copper and copper barrier layers, oxides, silicon nitride, and tungsten polishing liquids, meeting the needs of multiple process nodes; Technological breakthroughs: Sales of advanced process copper polishing liquids have increased, nitrogen polishing liquids have completed customer verification and are ramping up, domestic polishing particles for oxide polishing liquids are gradually increasing, and tungsten polishing liquids have passed verification in advanced storage/logic processes; Market position: The main supplier of CMP polishing liquids in China, entering the supply chains of SMIC, Huahong, and Yangtze Memory, supplying to TSMC and Samsung.

Jiangfeng Electronics (300666.SZ)

The leading domestic high-purity sputtering target company, with good performance in H1 2025:

Financial performance: Revenue was 2.095 billion CNY (up +28.71% year-on-year), with a net profit attributable to shareholders of 253 million CNY (up +56.79% year-on-year), and a net profit excluding non-recurring items of 176 million CNY (up +3.60% year-on-year); Core advantages: Revenue from ultra-high purity sputtering targets was 1.325 billion CNY (accounting for 63.3%, up +23.9% year-on-year), including aluminum targets, titanium targets, tantalum targets, and tungsten-titanium targets, applied in semiconductors/panel displays/solar energy; Technical strength: Target purity of 99.999%-99.9999% (internationally advanced), entering the supply chains of TSMC, Samsung, and Intel; Market prospects: The explosive demand for AI chips, storage chips, and power semiconductors is driving the growth of high-end target demand, benefiting the company.

Other Specialty Materials Companies

Photoresists: Nanjing University of Technology (300346.SZ), Shanghai Xinyang (300236.SZ) have breakthroughs in KrF/ArF high-end photoresists; Electronic Special Gases: Huate Gas (688268.SH), Jinhong Gas (688106.SH) have outstanding ultra-high purity gas technologies; CMP Polishing Pads: Dinglong Co., Ltd. (300054.SZ) is a major domestic supplier; Photomasks: Qingyi Optoelectronics (688138.SH) has stable market share in mid-to-low-end photomasks.

6.3 Investment Logic in the Materials Field

Short-term focus onaccelerated domestic substitution, breakthroughs in high-end materials, and demand structure upgrades as the three main lines:

Domestic Substitution: Silicon wafers (30%+), CMP polishing liquids (high substitution rate), and targets (global 15%) are progressing rapidly, while photoresists (<5%) and photomasks (low substitution rate) have significant room for growth; High-end breakthroughs: Advanced processes (3nm/2nm) are driving demand for new materials, with domestic companies making breakthroughs in new gate/dielectric materials and storage medium materials; Demand upgrades: AI chips (thermal management/packaging materials), new energy vehicles (power semiconductor materials), and 5G (RF materials) are driving growth in high-end material demand.

7. Overview of the Semiconductor Industry Chain and Investment Opportunities

7.1 Industry Chain Structure and Upstream/Downstream Relationships

The semiconductor industry chain is a complex ecosystem of **“upstream materials/equipment — midstream manufacturing — downstream applications”**:

Upstream: Materials (silicon wafers, photoresists, electronic special gases, targets, polishing liquids, photomasks), equipment (lithography machines, etching machines, thin film deposition, ion implantation, cleaning, CMP); Midstream: Design (chip design), manufacturing (wafer foundry), packaging and testing; Downstream: Consumer electronics, communication equipment, computers, automotive electronics, industrial control, new energy; Market size: The global semiconductor market is expected to reach 700.9-800 billion USD in 2025, with China at 2.5 trillion CNY (accounting for over 35%); global equipment sales are expected to reach 125.5 billion USD, with China at 230 billion CNY; Value distribution: “High at both ends, low in the middle” — design/equipment (high barriers, high added value), manufacturing (capital-intensive, lower profit margins), packaging and testing (lower technical barriers, with advanced packaging increasing added value), materials (high-end materials with high added value).

7.2 Progress and Bottlenecks of Domestic Substitution

Progress: Comprehensive acceleration, with significant differences

Overall self-sufficiency rate: Increased from less than 10% to 18%-26% in 2025, with accelerated breakthroughs expected in the next three years; Segmented links: Storage chips (DRAM self-sufficiency rate expected to be 23% in 2025) > Equipment (20%-25%) > Materials (silicon wafers 30%+, CMP polishing liquids with high substitution rates, targets with global 15%); Mature processes: Rapid improvement in the localization rates of equipment/materials for 28nm and above, with competitive capabilities.

Bottlenecks: High-end fields still face “bottlenecks”

Equipment: EUV lithography machines are fully imported, with a localization rate of 2.5% for DUV lithography machines, and reliance on imports for high-end lithography machines below 28nm; Materials: High-end photoresists (ArF/EUV), high-purity electronic special gases, CMP polishing pads, and photomasks have a localization rate of <5%, monopolized by Japanese, American, and European companies; Technology: Localization rates for advanced process materials/equipment below 14nm are <10%, with key components/core technologies being constrained.

Trends: From “passive defense” to “active breakthrough”

Mature processes: Domestic companies have strong competitiveness, with continuous improvement in substitution rates; Advanced processes: Breakthroughs such as Shanghai Microelectronics’ 28nm lithography machine (localization rate of 90%) and SMIC’s DUV multi-patterning (7nm mass production) are exploring independent paths.

7.3 Risks in the Industry Chain and Response Strategies

Core Risks

Technological iteration risk: Rapid updates in semiconductor technology, reliance on advanced processes (such as EUV), and delays in new material development may lead to investment losses; Supply chain risk: Geopolitical factors and trade frictions may disrupt the supply of key equipment/materials; Market risk: Industry cyclicality and demand forecasting errors may lead to overcapacity (such as excessive investment in AI chips); Competition risk: Intensified competition among domestic companies and increased presence of international giants in China may squeeze domestic market share.

Response Strategies

Technological innovation: Increase R&D investment, collaborate with industry-academia-research to tackle “bottleneck” areas in equipment/materials; Industry collaboration: Joint R&D and procurement among upstream and downstream of the industry chain to build a close ecosystem; Supply chain security: Promote supply chain diversification and establish emergency reserves for key materials; Market strategies: Strengthen demand forecasting, plan capacity reasonably, and avoid blind investments; International cooperation: Participate in global industrial division of labor and expand markets under compliance.

8. Short-term Investment Strategies and Risk Alerts

8.1 Short-term Investment Opportunities Ranking in Various Segmented Fields

1. Semiconductor Equipment (Strongest Certainty)

Driving factors: Localization rate increasing from 20% to 25% (clear increment), domestic wafer foundries expanding (the Chinese equipment market is expected to reach 230 billion CNY in 2025, up +30% year-on-year), breakthroughs in high-end equipment (North Huachuang, Zhongwei, Shengmei); Key targets: North Huachuang (full product line), Zhongwei Company (5nm etching), Shengmei Shanghai (25% market share in cleaning).

2. Semiconductor Materials (Dual-Driven)

Driving factors: Geopolitical factors driving localization, demand upgrades for advanced processes, breakthroughs in some fields (Shanghai Silicon, Anji, Jiangfeng); Key targets: Shanghai Silicon Industry (300mm silicon wafers), Anji Technology (CMP polishing liquids), Jiangfeng Electronics (high-purity targets).

3. Semiconductor Design (AI + Substitution)

Driving factors: Explosive demand for AI chips, accelerated domestic substitution, and incremental automotive electronics; Key targets: Haiguang Information (AI training), Cambrian (AI inference), GigaDevice (storage + MCU).

4. Semiconductor Manufacturing (High Capacity + Breakthrough)

Driving factors: Capacity utilization rates exceeding 90% (SMIC 92.5%, Huahong 108.3%), mass production of 7nm processes, and growth in demand for specialty processes; Key targets: SMIC (advanced processes), Huahong Group (specialty processes), China Resources Microelectronics (power semiconductors).

5. Semiconductor Packaging and Testing (Stable)

Driving factors: Growth in demand for advanced packaging, increased packaging for AI chips, and high industry concentration; Key targets: Changdian Technology (leading in advanced packaging), Tongfu Microelectronics (cooperation with AMD).

8.2 Key Recommended Stocks and Investment Logic

8.3 Risk Alerts

- Technological Iteration Risk: Rapid updates in semiconductor technology, reliance on advanced processes (such as EUV), and delays in new material development may lead to a decline in corporate competitiveness, affecting investment returns;

- Market Volatility Risk: The industry has strong cyclicality, and demand fluctuations (such as a cooling demand for AI chips) may lead to significant fluctuations in corporate performance; international trade frictions and technological blockades may impact the market;

- Valuation Risk: The current A-share semiconductor (Shenwan) index PE (TTM) is 111 times, at the 87% percentile since 2019, with high valuations implying high growth expectations; if performance does not meet expectations, there may be pressure for valuation adjustments;

- Policy Change Risk: The continuity of domestic policies (such as the direction of the big fund, tax incentives) is uncertain, and international export controls (such as equipment/material bans) may affect the operation of the industry chain;

- Intensified Competition Risk: The expansion of domestic companies’ capacity leads to intensified competition, while international giants (such as TSMC, ASML) strengthen their presence in China, squeezing the market share of domestic companies;

- Supply Chain Risk: Reliance on imports for key equipment (such as EUV) and materials (such as high-end photoresists) may lead to production stagnation due to supply interruptions, affecting corporate operations.

Investment Suggestions: Investors should consider their own risk tolerance and avoid excessive concentration in investments; it is recommended to build positions in batches, focusing on high-certainty targets (equipment/materials) in the short term, and closely track industry dynamics (capacity utilization rates, technological breakthroughs) and company fundamentals, adjusting strategies in a timely manner.