Under the current trends of global military dynamics, future wars and conflicts will increasingly move towards automation and intelligence, with drones being widely applied in various fields of future combat. In 1927, Professor A.M. Law successfully test-flew his developed drone, the “Throat” type monoplane, on the British warship “Fortress”, marking the beginning of drone warfare. In 1931, the UK successfully developed the “Fairy Queen” unmanned target aircraft, which was used during naval fleet exercises. In the mid-1950s, the United States launched its first practical reconnaissance drone, the AN/USD-1. During the Vietnam War in 1955, the U.S. introduced the U-2 reconnaissance drone and military drones like the “Flame” – 147 type. In the early 1980s, Israeli military drones launched a surprise attack on Syrian SAM missile positions in the Bekaa Valley, demonstrating their significant combat potential for the first time. In the Gulf War of 1991, the U.S. military utilized drones such as “Pointer” and “Pioneer” to gather radar target parameters from Iraqi forces. In 2001, during the Afghanistan War, the U.S. used the “Predator” drone equipped with Hellfire missiles, transforming drones into multifunctional combat aircraft capable of direct attack, and they began to be used as weapons for direct confrontation on the battlefield.

1. Industry Development Driving Factors: Fundamentals Ready, New Technologies Bring New Opportunities

1. Policy Dividends: Clear Policy Guidance, Strengthened Industry Opportunities

Policy objectives have been continuously upgraded, with the addition of the “New Domain and New Quality” strategic plan. Since the founding of the country, China has continuously strengthened its defense and military modernization. The report of the 18th National Congress of the Communist Party proposed the overall requirement to “accelerate the advancement of national defense and military modernization,” which was upgraded to “comprehensively advance” in the report of the 19th National Congress. The 20th National Congress report explicitly stated the need to “create a new situation in the modernization of national defense and the military,” further mentioning “modernization of military theory, modernization of military organizational forms, modernization of military personnel, and modernization of weapons and equipment,” and added the expression “increase new domain and new quality combat forces.” Military drones are an important part of the “new domain and new quality combat forces.” “New domain and new quality” refers to new types of combat forces in non-standard operational fields such as aerospace and information networks. Military drones, as military equipment that achieves aerospace operations through information technology and intelligence, are a crucial part of the “new domain and new quality” combat forces. In recent years, policies in China’s defense and military industry have frequently mentioned the trends of remote precision, intelligence, stealth, and unmanned development of weapons and equipment, clearly defining the characteristics of future informationized and intelligent warfare, encouraging military-civilian integration and industry-university collaboration to improve the research and development level of weapons and equipment, thus providing a favorable policy environment for the rapid development of China’s military drone industry.

2. Industry Demand: Defense Budget Growth Returns to 7, Structural Demand for Drones Outstanding

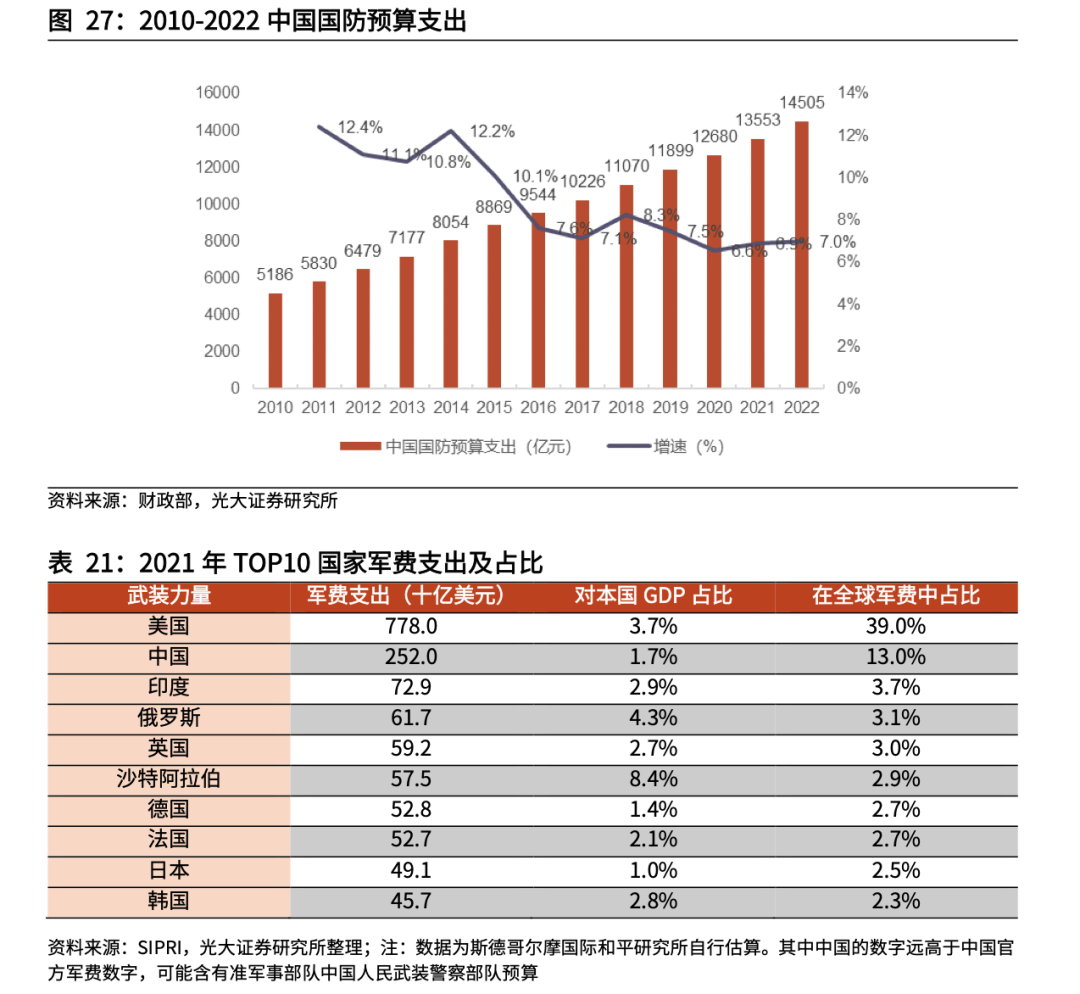

Military spending is the foundation for the development of the military industry, and the return of defense budget growth to 7 solidifies the military’s purchasing power. In the context of international turmoil, countries around the world are gradually increasing their military expenditures. According to data released by China’s Ministry of Finance, since 2014, the total defense expenditure budget has shown a slowing growth trend, with growth rates maintained between 6.5% and 8.5% from 2017 to 2022. In 2022, China’s total defense expenditure budget was 1.45 trillion yuan, a year-on-year increase of 7.0%, exceeding the 5.5% growth target of GDP for 2022. China’s military spending as a proportion of GDP is relatively low compared to major countries, indicating significant room for future growth.

In comparison to the United States, China’s military drone inventory is relatively small but is in a rapid development and deployment phase, indicating greater growth potential for military drone demand in the future. Assuming that the proportion of military drone costs in the U.S. military budget in 2023 is 1.33%, we conservatively estimate that the demand scale for military drone equipment in China in 2022 will exceed 19.3 billion yuan. According to the 2023 defense budget request released by the U.S. Department of Defense, the total defense budget request for 2023 is $773 billion, a year-on-year increase of 2.1%. This includes investments in drone systems such as three MQ-4C “Triton” drones, four MQ-25 “Stingray” drones, and five MQ-9A “Reaper” drones, with procurement prices of $1 billion, $1.2 billion, and $500 million respectively. The total investment in drone systems amounts to $10.3 billion, accounting for approximately 1.33% of the 2023 defense budget request. Given that China’s military drone industry started relatively late but is developing rapidly, we assume that China’s military drone deployment demand scale lags behind the U.S. by one year. Based on the U.S. military drone cost proportion in 2023, we estimate that China’s military drone equipment demand scale in 2022 will be approximately 19.29 billion yuan (2022 China’s defense budget expenditure 1.4505 trillion yuan * 1.33%). Considering that the U.S. military’s 2023 drone investment only includes large drones and does not account for small drone equipment demand such as loitering munitions and target drones which may experience explosive growth, we conservatively estimate that the demand scale for military drone equipment in China in 2022 will exceed 19.3 billion yuan.

3. Industry Supply: China’s Drone Industry Has Four Major Advantages, Creating a Positive Circular Model for the Industry Chain

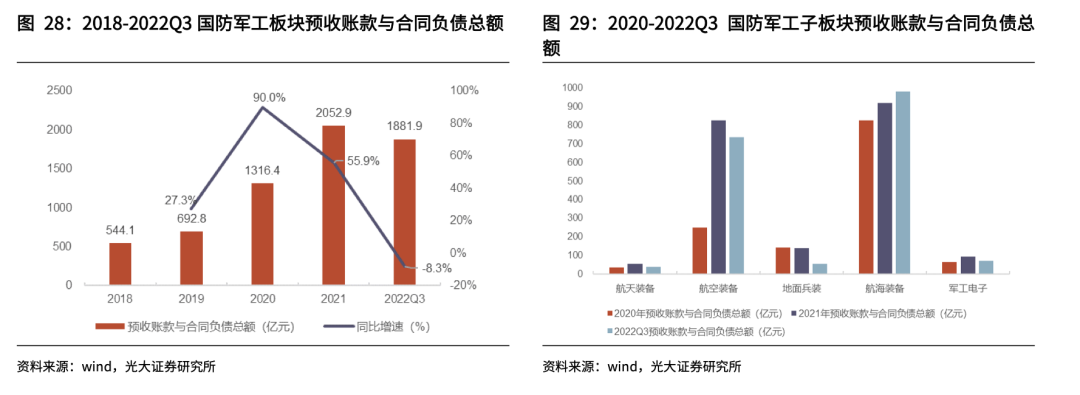

The military drone industry is highly planned, and the “sales determine production” supply model means that companies will procure based on order demand, which helps them fully grasp market trends and supply chain conditions. The enormous space and certainty of defense construction demand will drive a higher structural prosperity in the military drone industry in the next 5-10 years. The high growth of advance payments and contract liabilities in the defense industry indicates sufficient overall orders in the industry. According to Shenwan’s 2021 industry classification, from 2018 to 2021, the total advance payments and contract liabilities in China’s defense industry increased year by year, growing from 54.41 billion yuan at the end of 2018 to 205.29 billion yuan at the end of 2021, with a 3-year CAGR of 55.7%. Among them, the total advance payments and contract liabilities in the defense industry at the end of 2021 increased by 55.9% compared to the end of 2020; by the end of Q3 2022, the total was 188.19 billion yuan, showing a slight decrease compared to the end of 2021. In terms of sub-sectors, compared to the end of 2020, the total advance payments and contract liabilities in the aviation equipment sector grew particularly prominent by the end of 2021, increasing from 24.96 billion yuan to 82.651 billion yuan, a year-on-year growth of 231.1%; by the end of Q3 2022, the total for this sector was 73.59 billion yuan, a decrease of 9.06 billion yuan compared to the end of 2021. The total for the aerospace equipment sector at the end of 2021 was 5.36 billion yuan, a year-on-year growth of 47.2%; by the end of Q3 2022, it was 4.01 billion yuan, only down 1.35 billion yuan from the end of 2021. The total for the military electronics sector at the end of 2021 was 9.39 billion yuan, a year-on-year growth of 44.5%; by the end of Q3 2022, it was 7.07 billion yuan, only down 2.32 billion yuan from the end of 2021.

With the technological advancement and cost reduction of China’s drone industry, China has progressed from a backward state to catching up with the U.S. in high-end drone technology. The development of industrial and consumer drones has significantly promoted the development of China’s military drones. Currently, China’s drone industry supply side possesses four major advantages.

1) The Chinese military-industrial system has a small core and large collaboration, with smooth communication with private enterprises, establishing a prosperous and autonomous drone ecosystem, reducing “bottleneck” and development risks. Military research institutions and universities have strong research capabilities and occupy a core position in the industry chain; private enterprises can lead both economic efficiency and technological expansion through flexible mechanisms to promote innovation; at the same time, the Beidou system promotes the research and development of domestic inertial navigation, enhancing national defense autonomy.

2) Economic benefits drive military drone development, creating a positive circular model for the industry chain. China’s competitive advantage in the drone field compared to the U.S. lies in cost. China has a solid foundation in the drone field and possesses full industrial chain capabilities, with the cost of similar products of the same level in China being much lower than that in the U.S. For example, China’s Wing Loong-2 drone is comparable to the U.S. MQ-9 but costs several times less. China’s cost-effective drone products have achieved significant success in the international market, generating considerable economic benefits that help provide funding and technology for military and civilian projects. The U.S. Arms Export Control Act of 1976 and other regulations have restricted the foreign sale of special weapons, limiting its economic driving force for drone technology research and development.

3) China’s drone industry has diverse military and civilian drone products and continuous iteration capability. U.S.-made drones are mainly large military drones, and U.S. military enterprises do not manufacture “low-end” small and inexpensive drones, which limits the widespread application of drones. In contrast, China’s drone industry produces various sizes and capabilities of drones, providing high flexibility for drone applications and facilitating the development of new combat concepts and promoting innovation.

4) Domestic and international dual demand drives industry growth, and the scale advantage of the manufacturing industry promotes continuous technological progress. In recent years, the scale of exports and domestic sales of various drones in China has rapidly increased. The huge industry demand feeds back into the industry chain, forming a scale advantage in the drone manufacturing industry. Military-civilian integration is conducive to leveraging the innovative capabilities of private enterprises to promote technological iteration, and the drone ecosystem based on the industry chain is increasingly prosperous.

2. Industry Development Status: Market Size Continues to Expand, Great Power Competition Intensifies

1. Market Size: Global Growth, China’s Accumulation

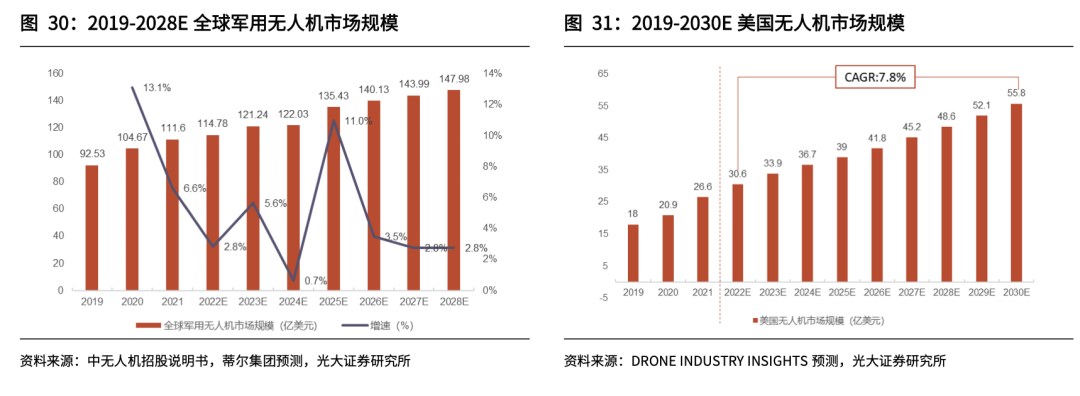

The global military drone market size is considerable, with Asia leading in growth. According to data from the China Drone IPO prospectus and forecasts from the Tiers Group, the global military drone market size, calculated based on annual production value (including procurement), is expected to continue to grow from 2019 to 2028, with an estimated size of $11.478 billion in 2022, a year-on-year increase of 2.8%. The global military drone market size is expected to reach $14.798 billion by 2028, with a compound annual growth rate of approximately 5.36% from 2019 to 2028. TrendForce released a forecast on December 7, 2022, stating that as countries actively invest in military drone procurement, deployment, and research and development, the global military drone market size is expected to grow from $16.5 billion in 2022 to $34.3 billion in 2025, with an annual compound growth rate of 27.6%. Data from Drone Industry Insights shows that the U.S. drone market size reached $2.66 billion in 2021, and it is expected to continue growing at an annual compound growth rate of 7.8% from 2022 to 2030. In terms of market size growth by continent, Asia, North America, and Europe are expected to be the top three regions in growth for 2022, with growth rates of 11.9%, 8.1%, and 6.8% respectively; by 2030, Europe is expected to surpass North America to become the second-largest growth region, while Asia will maintain its first position with a growth rate potentially reaching 19.4%.

2. Industry Chain: Downstream Complete Manufacturers as the Core of the Industry Chain

The military drone industry chain mainly includes upstream raw materials, components/parts, midstream flight platform subsystems, effective payload subsystems, and ground control subsystems, and downstream complete manufacturers.

1) Upstream raw materials and components include batteries, motors, chips, gyroscopes, structural components, and composite materials. Major manufacturers in China include Guangwei Composite Materials, Zhongjian Technology, and Zhongfu Shenying, which provide carbon fiber composite materials; Tongda Co., which provides structural components and cables; Lihang Technology and Guanglian Aviation, which provide drone parts processing and assembly; Aerospace Electronics, which provides precision-guided product systems, intelligent perception, special motors, and high-end intelligent equipment; and Gaode Infrared and Dali Technology, which provide infrared thermal imaging equipment.

2) The midstream flight platform subsystems can be divided into five parts: propulsion systems, flight control systems, power systems, communication systems, and structural components. Specifically, the propulsion system is the “heart” of the drone, primarily consisting of engines, propulsion controls, and propellers, with engine development being a crucial part of the drone industry chain. Major engine development companies in China include Aero Engine Corporation of China, Zongshen Power, and Hangrui Power. The flight control system is the “brain” of the drone, with basic functions including controlling the drone’s hover, roll, pitch, and yaw movements. The drone flight control system typically includes control computers, sensors, and actuators, and is mainly developed and produced by Aviation 618 Institute, AVIC Electromechanical, and Aerospace Electronics. The power system involves the manufacturing of power supplies, distributors, and electrical equipment, with key companies including Aerospace Electric, Xinle Energy, and AVIC Optoelectronics. The communication system is mainly produced and developed by Aviation 615 Institute, CETC 54 Institute, and Aerospace Development. The structural components include the manufacturing of the fuselage and wings, mainly undertaken by Chengfei, Xifei, and Guanglian Aviation.

3) The midstream task payload system consists of two parts: data transmission systems and task payload systems. The task payload system refers to the equipment equipped on the drone to complete missions, directly determining the drone’s functions. Major payloads include reconnaissance equipment, communication devices, and weapons, with components involving electro-optical/radar reconnaissance and monitoring equipment as well as specialized lightweight air-to-ground weapons like AR series missiles. China’s task payload systems are mainly developed by Aviation 618 Institute, Aviation Radar Institute, and Aviation Electro-Optical Institute.

4) The midstream ground control subsystems consist of ground tower control systems, ground communication systems, and ground measurement and control systems. To effectively command and control drones, advanced wireless data links are needed to maintain continuous communication between the control station and the drone. Currently, most medium and large military drones developed by countries worldwide are commanded and controlled by integrated ground control stations. Major companies in China’s ground control systems include CETC 54 Institute, Hengyu Xintong, and Aerospace Communication.

3. Competitive Landscape: The U.S. and Israel Lead, China Shows Significant Progress

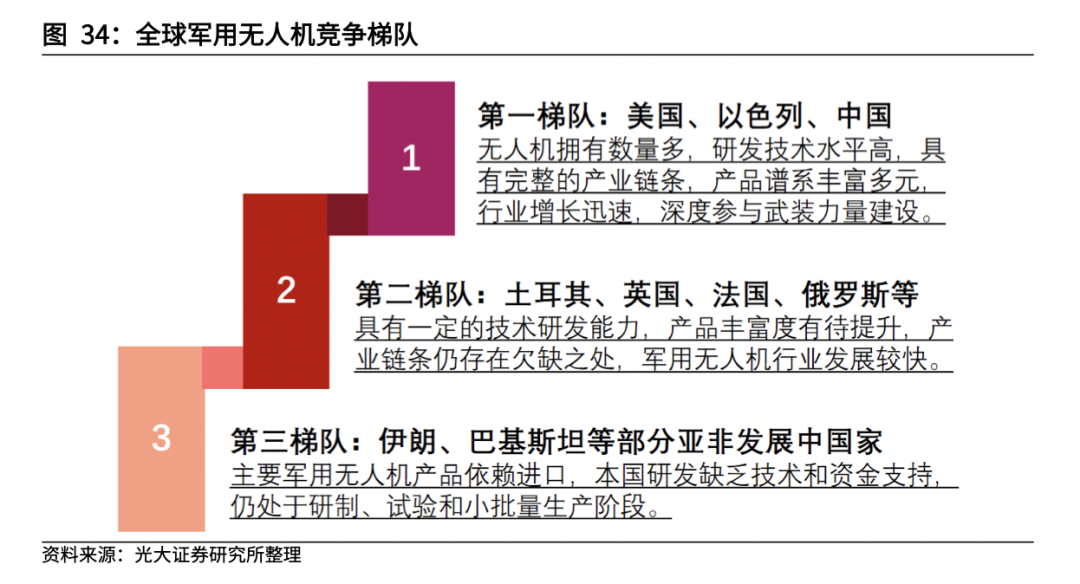

Based on the level of military drone production and research and development technology, product lineage completeness, and degree of external dependence, the global military drone competition can be divided into three tiers: 1) The first tier includes the U.S., Israel, and China, which have a large number of military drones, high research and development technology levels, complete industry chains, diverse product lineages, and heavy involvement of drones in armed forces construction. The U.S. is one of the earliest countries to develop and use drones, with advanced technology and a wide variety of types, forming a complete drone system covering high, medium, and low altitudes, long, medium, and short ranges, large, medium, and small sizes, strategic, tactical, attack, and countermeasures. Major companies developing drones include Northrop Grumman, General Atomics Aeronautical Systems, and Boeing, with typical products including “ScanEagle,” “Shadow,” “Predator,” “Reaper,” and “Global Hawk.” Israel’s drone technology mainly derives from the U.S., gradually developing through imitation, modification, and independent innovation, becoming the world’s second strongest country in drone technology after the U.S., with rich tactical experience in drone operations, forming a relatively complete drone system from long-endurance drones, tactical drones to attack drones. Currently, Israel’s main drone models include “Heron,” “Eitan,” and “Heron TP,” which have been tested in two Middle Eastern wars and are favored by multiple countries.

2) The second tier includes countries such as Turkey, the UK, France, and Russia. These countries have certain military drone research and development capabilities, and their military drone industries are in a rapid rising period, but their industry chains are not yet complete, and the richness of their products still needs improvement. Among this tier, the UK and France lead in military drone development, with relatively complete models; Russia has the capacity for independent research and development, but its progress is somewhat lagging or behind. Russia has been vigorously developing drone technology since the Syrian civil war in 2011. Russia has deployed drones in its army, navy, and air force, with major models including “Orion”-10, “Outpost,” and “Orion.”

Turkey’s armed drones include various types such as the “Bayraktar”-TB2, “Anka S,” and “Kargu 2” quadcopter suicide drones, all of which have demonstrated excellent performance in multiple conflicts and combat situations. For instance, data from China Aerospace News indicates that during the 2020 Nagorno-Karabakh conflict, Azerbaijani forces equipped with Turkish drones destroyed 106 Armenian tanks, 146 artillery pieces, 62 multiple rocket launchers, 18 air defense missile systems, 7 radar systems, and 161 other vehicles, causing losses exceeding $1 billion; in the recent Russia-Ukraine conflict, the Turkish “Bayraktar-TB2” drone destroyed numerous Russian tanks and armored vehicles as well as ground facilities.

3) The third tier includes some developing countries in Asia and Africa, such as Iran and Pakistan. The military drones in these countries mainly come from imports, and due to limitations in technology and funding, their independent research and development capabilities are relatively low, remaining in the stages of development, testing, and small-scale production.

The globally renowned military drone manufacturing companies include General Atomics and Northrop Grumman from the U.S., Israel Aerospace Industries and Elbit Systems from Israel, Turkish Aerospace Industries and Baykar Makina from Turkey, BAE Systems from the UK, and China’s Aerospace Rainbow and Zhong Drone.

China’s military drone industry competition landscape is relatively stable, as the military drone industry has high entry barriers, primarily reflected in technological and policy barriers. 1) Technological barriers: Military drones are characterized by high technological integration, significant research and development investment, and high levels of intelligence and information technology. Whether in the manufacturing of basic materials or the production and design of core components, military drone systems apply numerous advanced technologies, including new materials technology, intelligent control technology, propulsion technology, and stealth technology. Developing a new technology requires substantial financial and time investment, making it challenging for ordinary enterprises to enter; 2) Policy barriers: Military drones are classified as aviation military products, which are critical defensive weapons for national defense, with stringent quality requirements. Thus, customers have high recognition of military drone companies’ brands and manufacturing requirements, imposing significant restrictions on new companies entering the drone industry.

3. Future Development Trends of the Industry: Diversified, Multimodal, Intelligent Integration

1) Pursuing low cost and high efficiency, fully leveraging the low-cost advantages of drones. According to the “Overview of Foreign Military Drone Equipment Technology Development in 2021” (by Zhu Chaolei), in recent years, foreign countries have placed great importance on the development of air-launched drones, swarm drones, and other small, low-cost drone equipment, continuously enhancing the task capabilities of medium and small drones and exploring new combat forms such as bait warfare and swarm warfare, seeking to build scale advantages in high-intensity combat environments. For example, the U.S. military’s X-61A “Gremlin” drone has a unit price of less than $700,000, and the XQ-58A “Valkyrie” drone has a unit price of less than $2 million. To achieve the goal of low-cost unmanned equipment, foreign countries adopt various design and development methods, including vigorously promoting digital engineering, using digital models in all aspects from feasibility analysis, overall planning, detailed design to production, to reduce costs and increase efficiency; secondly, employing limited lifespan design methods, developing consumable, short-lifespan components to reduce drone costs, such as the core components of the U.S. Air Force’s XQ-58A “Valkyrie” engine, which have a lifespan of only about 20-50 uses, significantly reducing operational and maintenance costs; thirdly, extensively using mature task payloads, with foreign manufacturers typically using mature off-the-shelf products and commercial software according to task requirements, greatly reducing upgrade and loss costs.

2) Multipolarity: The development towards high-altitude long-endurance large-scale drones, flexible use of micro-drones, and hypersonic stealth capabilities. On one hand, countries worldwide are striving to develop larger drones with greater coverage and survivability to replace similar manned aircraft and to complete aerial surveillance and reconnaissance tasks alongside space satellites; on the other hand, due to the lightweight, compact size, low cost, good concealment, ease of operation, and maneuverability of micro-drones, miniaturization has become another important development trend for drones, especially in response to global counter-terrorism and special operations needs. Furthermore, to cope with the future advancements in air defense weapon technologies, future unmanned combat aircraft will adopt more advanced stealth technologies, including radar, infrared, optical, acoustic, and visual measures, combined with electronic countermeasures, battlefield situational awareness, mission planning, and even self-defense weapons (including high-energy laser weapons), further enhancing their penetration/survivability, posing threats to well-protected enemy targets. In future aerial combat, hypersonic stealth drones will become typical representatives of high-performance air defense weapons.

3) Intelligence: Enhanced by artificial intelligence to counter electromagnetic attacks. Currently, drones are primarily operated manually, which may be affected by electromagnetic attacks; if operators make erroneous judgments, it can lead to catastrophic outcomes. Therefore, drones must possess a high level of automation and intelligence, autonomously judging emergency strategies for battlefield variables, developing towards intelligent flight of single drones, intelligent collaboration of multiple drones, and autonomous mission intelligence, involving environmental perception and avoidance, collaborative command and control, collaborative situational generation and assessment, autonomous navigation, and autonomous completion of combat missions. The future integration of big data applications into drone intelligence is a significant trend in drone development. a) Intelligent observation and judgment—extremely efficient data analysis. The widespread deployment of unmanned platforms and sensors has led to a rapid increase in data volume in the military field, with its quantity and complexity far exceeding human processing capabilities. Artificial intelligence algorithms, characterized by speed, accuracy, and fatigue-free operation, can continuously analyze vast amounts of data from various sensors quickly and accurately, 24/7. b) Intelligent decision-making—further compression of the kill chain. Speed has always been a key factor for victory; from the perspective of the kill chain, completing the kill chain more quickly can gain a war advantage, and the rapidity of machine algorithms is a key feature distinguishing algorithmic warfare from traditional warfare. Under algorithmic warfare, humans can transfer most of the cognitive burdens of observation and judgment in the kill chain to well-trained intelligent machines, allowing them to focus on making faster and better decisions in warfare.

4) Comprehensive integration: The development of drone systems from single-platform operations to collaborative operations between manned and unmanned systems, and the formation of intelligent drone swarms. In the face of increasingly complex modern warfare methods and environments, relying solely on single systems for reconnaissance, surveillance, and attack cannot fully utilize their combat capabilities in modern warfare. Foreign countries emphasize the collaborative operational capabilities between drones and manned aircraft, as well as between drones, vigorously developing new equipment such as unmanned wingmen, drone swarms, air-launched decoys, and unmanned refueling aircraft, constructing an aerial combat system with characteristics of clustering and distribution to achieve capability multiplication of manned combat equipment. The U.S. Air Force’s Strategic and Budget Assessment Center’s report on “Five Priorities for Future Combat Air Power” proposes various concepts of manned-unmanned collaborative operations, including large fixed-wing drones like RQ-4 and MQ-9 carrying intelligence, surveillance, and reconnaissance, and electronic warfare payloads to assist in homeland defense tasks; unmanned wingmen carrying air-to-air missiles and laser weapons coordinating with fighter jets to provide air escort for AWACS and large tankers; unmanned wingmen grouping with fighter jets to execute offensive and defensive air combat missions in high-contest environments; and drones serving as network nodes for multi-domain command, connecting to space-based networks, E-3G, and other battlefield management command nodes and ground stations to assist in long-range detection tasks.

5) Spatialization: Breaking through task flight heights to leverage the military value of space information operations. In the future, military drones will have breakthroughs in flight height, with near-space becoming a possibility, bringing them close to satellite orbits, reaching altitudes of 30-120 km above the earth’s surface, and leveraging potential military value. Compared to traditional early warning and navigation tasks, near-space will become a transitional platform in space, fundamentally changing the military role of traditional drones, turning them into space drones. The U.S., Russia, and some European countries have already formulated space development plans to compete for war positions in space, with some technological research already entering experimental phases, and technological advancements will promote unmanned vehicles to leverage the military value of space information operations, achieving integration across land, sea, and air.

Source: Military Eagle DynamicsEditor: Wu MinDeputy Editor:Yu WenjingDuty Editor: Yang Xudong Editor: Sun Yiwen

Source: Military Eagle DynamicsEditor: Wu MinDeputy Editor:Yu WenjingDuty Editor: Yang Xudong Editor: Sun Yiwen