Major Listed Companies in the Industry: Pegatron Corporation (002938.SZ), Dongshan Precision (002384.SZ), Shenzhen South Circuit (002916.SZ), Jingwang Electronics (603228.SH), Huadian Technology (002463.SZ), Xingsen Technology (002436.SZ), Shiyun Circuit (603920.SH), etc.

Core Data of This Article: Cost Structure of Printed Circuit Boards (PCB); Value Chain of Printed Circuit Boards (PCB)

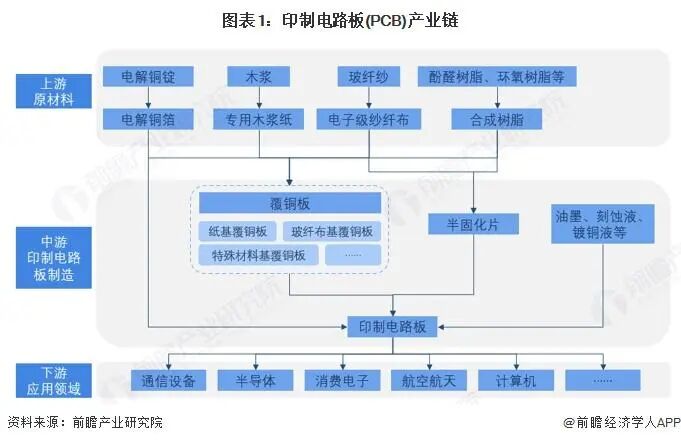

Structure of the Printed Circuit Board (PCB) Industry Chain

The printed circuit board manufacturing industry has a long industry chain, with specialized wood pulp paper, electronic-grade fiberglass cloth, electrolytic copper foil, copper-clad laminates (CCL), and printed circuit boards (PCB) being closely interconnected upstream and downstream products.

From the perspective of the industry chain, the upstream of printed circuit boards (PCB) mainly includes raw material industries such as copper foil, copper foil substrates, fiberglass cloth, and resin; the midstream refers to the manufacturing process of printed circuit boards (PCB), which involves the process of etching to produce PCB boards from copper-clad laminates; the downstream mainly includes application fields of printed circuit boards (PCB), including communications, optoelectronics, consumer electronics, automotive, aerospace, military, and industrial precision instruments.

Ecological Map of the Printed Circuit Board (PCB) Industry Chain

From the perspective of representative enterprises in each link of the industry chain, the upstream raw material segment mainly includes copper foil suppliers such as Nordson Corporation and Jiayuan Technology, fiberglass cloth companies such as China Jushi and Changhai Co., Ltd., epoxy resin companies such as Sinopec, Sanmu Group, and Dongcai Technology, as well as copper-clad laminate companies such as Jiantao Laminates, Shengyi Technology, and Nanya New Materials. The midstream of the industry chain mainly includes PCB manufacturers such as Pegatron Corporation, Dongshan Precision, Shenzhen South Circuit, Huadian Technology, and Jingwang Electronics. The downstream applications are widespread, including communications, computers, automotive electronics, and consumer electronics.

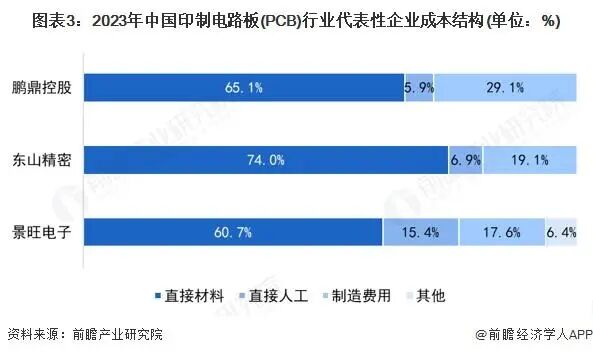

Cost Structure Analysis of the Printed Circuit Board (PCB) Industry

The cost of printed circuit boards (PCB) mainly consists of raw materials, labor costs, and manufacturing expenses. Forward-looking statistics on the product cost data of leading enterprises in the printed circuit board (PCB) industry show that raw materials account for the largest proportion of costs in the printed circuit board (PCB) industry, generally over 60%.

Price Transmission Mechanism of Printed Circuit Boards (PCB)

The market price of printed circuit boards (PCB) is formed and transmitted step by step through the joint action of the industry supply side, manufacturing side, and application side. The cost prices on the supply side include raw material and auxiliary material prices, labor prices, and equipment and factory prices, among which raw material prices are significantly affected by mineral resources, land supply, and international situations; the price transmission from the supply side to the manufacturing side forms the production cost, and the comprehensive supply and demand premium, R&D costs, and enterprise profits in the manufacturing industry form the “manufacturing side price” transmitted to the application side, while the market demand elasticity in application scenarios also reacts back to the supply side and manufacturing side, forming a “price-demand-price” transmission path that influences the market pricing of printed circuit board (PCB) products.

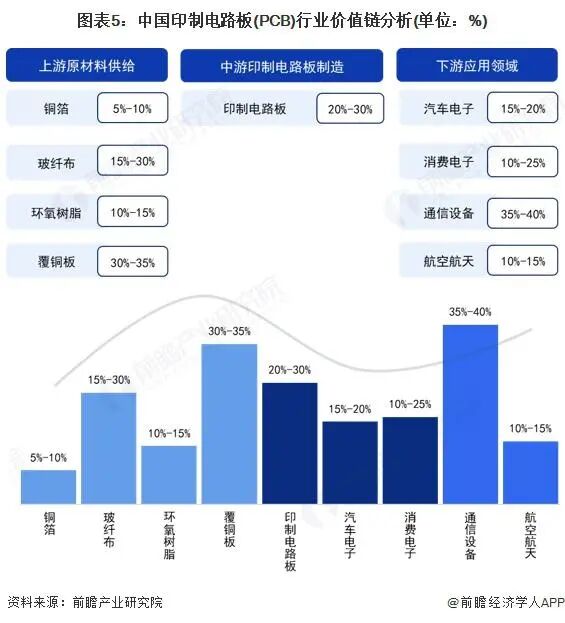

Value Chain Analysis of Printed Circuit Boards (PCB)

In the cost structure of China’s printed circuit boards (PCB), the proportion of raw materials is relatively high. Specifically, the gross profit margin of copper-clad laminates is relatively high, with a product gross profit margin of around 30%-35%; the gross profit margin of midstream printed circuit board (PCB) manufacturing is about 20%-30%; the downstream application fields are very broad, with significant differences in gross profit margin levels across industries, among which the communication equipment industry has a higher gross profit margin, overall around 35%-40%.

For more industry research and analysis, please refer to the “Market Outlook and Investment Strategy Planning Analysis Report of China’s Printed Circuit Board (PCB) Manufacturing Industry” by the Forward-looking Industry Research Institute.

Source: Forward-looking Industry Research Institute, the purpose of sharing is to provide more information and does not represent the position of this account. If there are any copyright issues, please contact the backend, and we will delete it as soon as possible. Thank you.